|

시장보고서

상품코드

1689899

클로르 알칼리 시장 : 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Chlor-alkali - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

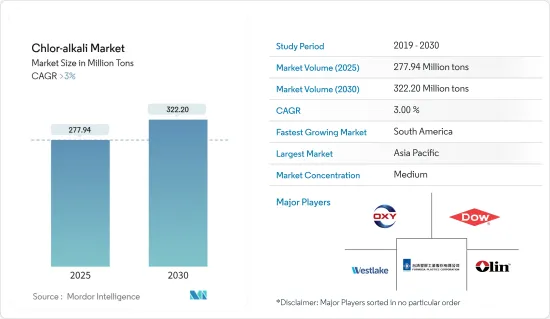

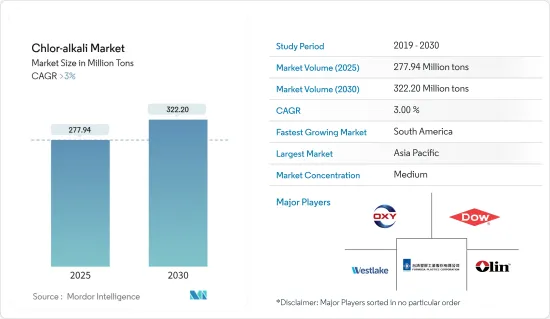

세계의 클로르 알칼리 시장 규모는 2025년 2억 7,794만 톤으로 추정되고, 2030년에는 3억 2,220만 톤에 이를 것으로 예측되며, 예측 기간 중(2025-2030년) CAGR 3%를 초과할 것으로 예측됩니다.

COVID-19의 유행은 세계 클로르 알칼리 수요에 부정적인 영향을 미쳤습니다. 유행 기간 동안 록다운, 공급망 혼란, 경제 활동 저하로 건설, 자동차, 제조 등의 분야에서 클로르 알칼리 제품에 대한 수요가 감소했습니다. 이 수요감퇴는 PVC 제조용 염소 소비에 영향을 미쳤습니다. 그러나 각국이 봉쇄규제를 완화하고 경제를 재개하기 시작하면 염소알칼리제품 수요는 회복되었습니다. 혼란에 휩싸인 산업도 점차 조업을 재개해 염소와 수산화나트륨 수요가 증가했습니다.

주요 하이라이트

- 시장 성장을 가속하는 주요 요인은 화학제조에서 수요가 급증하고 PVC가 수요를 확대하는 것입니다.

- 그러나 환경에 미치는 영향과 엄격한 환경 규제가 염소 알칼리 시장의 방해가 될 것으로 예상됩니다.

- 클로르 알칼리의 연구개발에 대한 투자 증가와 새로운 용도의 개척은 업계에 새로운 성장 기회를 제공할 것으로 예상됩니다.

- 아시아태평양은 클로르 알칼리 제품과 그 유도체의 대규모 생산과 소비로 인해 가장 큰 시장 점유율을 유지할 것으로 보입니다.

클로르 알칼리 시장 동향

시장을 독점하는 유기화학 부문

- 클로르 알칼리 제조 시 식염수의 전기분해로 제품별로 생성되는 염소는 많은 유기화학제품을 제조하는데 있어서 매우 중요한 원료로서 기능합니다. 염소는 유기 합성의 범용성이 높은 구성 요소이며 염소화 용매, 플라스틱, 농약, 의약품 및 기타 유기 화합물의 생산의 기초를 형성합니다.

- 염소의 가장 큰 소비자는 플라스틱 산업, 특히 PVC의 생산입니다. PVC는 건축자재, 포장, 자동차 부품 및 각종 소비재에 널리 사용됩니다. PVC 수요는 염소의 대량 소비를 촉진하고 유기 화학 부문은 염소 알칼리 시장의 주요 공헌자가되었습니다.

- 염소의 생산과 소비는 다양한 최종 사용자 산업에서 계속 증가하고 있습니다. Euro Chlor에 따르면 2023년 12월 말까지 유럽의 염소 생산량은 60만 9,418톤으로 증가했습니다. 2023년 12월 1일 평균 생산량은 2023년 11월(1만 9,659톤)에 비해 1.7% 감소했지만, 2022년 12월(1만 6,573톤)에 비해 18.6% 증가했습니다.

- Euro Chlor가 발표한 데이터에 따르면 독일은 2022년 540만 톤의 염소를 생산하여 국내 최대의 염소 생산 능력을 차지했습니다.

- BASF Report 2023에 따르면, 제약업계를 제외한 세계의 화학제조업은 2024년에는 전년(2023년: 1.7% 증가)을 상회하는 2.7% 확대가 전망됐습니다. 세계 화학시장의 선두를 차지하는 중국에서는 전년(2023년: 7.5%)의 견조한 성장에 비해 성장률이 저하되지만, 4.0%의 대폭적인 확대가 전망됐습니다.

- 이와 같이, 상기 요인에 의해 클로르 알칼리 수요는 향후 증가할 것으로 예상됩니다.

아시아태평양이 시장을 독점

- 아시아태평양에는 중국, 인도, 동남아시아 등 급속히 경제 성장을 이루고 있는 지역이 있으며, 이들 지역은 견조한 산업성장을 이루고 있습니다. 이 성장은 건설, 제조, 화학 및 섬유를 포함한 다양한 산업에서 클로르 알칼리 제품 수요를 촉진합니다.

- 아시아태평양에는 대규모 제조 거점이 있으며, 특히 PVC, 섬유, 화학제품 등 클로르 알칼리 제품의 중요한 소비자인 산업이 많습니다. 이 지역의 제조업은 세계의 클로르 알칼리 소비량의 대부분을 차지하고 있습니다.

- 게다가 중국 국무원 정보국에 따르면 중국의 주요 섬유 기업의 총 이익은 2023년 전년 대비 7.2% 증가했습니다. 같은 해 중국의 섬유 및 의류 수출은 2,936억 달러에 달했습니다. 섬유 및 의류품의 수출은 2023년 12월에 다시 증가로 전환해 전년대비 2.6% 증가를 나타냈습니다.

- 또한 Invest India에 따르면 인도는 세계 섬유 및 의류 무역의 4%를 차지합니다. 2030년에는 섬유 제조업에서 2,500억 달러, 수출로 1,000억 달러에 이를 것으로 예측됩니다.

- 또한 중국 국가 통계국이 발표한 데이터에 따르면 중국은 2023년 12월에 698만 톤의 플라스틱 제품을 생산했습니다.

- 따라서 위의 요인은 아시아태평양에서 클로르 알칼리 시장 수요를 증가시킬 것으로 예상됩니다.

클로르 알칼리 산업 개요

클로르 알칼리 시장은 부분적으로 단편화됩니다. 시장의 주요 기업(순부동)은 Olin Corporation, Occidental Petroleum Corporation, Formosa Plastics Corporation, Dow, Westlake Vinnolit GmbH & Co.KG 등입니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트·지원

목차

제1장 서론

- 조사의 전제조건

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 성장 촉진요인

- 화학제품 제조에서 수요 급증

- 폴리염화비닐(PVC) 수요 증가

- 억제요인

- 환경에 대한 영향과 엄격한 환경 규제

- 업계 밸류체인 분석

- Porter's Five Forces 분석

- 공급기업의 협상력

- 소비자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

- 수출입 동향

제5장 시장 세분화

- 제품

- 가성소다

- 염소

- 소다회

- 제조 공정

- 멤브레인 셀

- 다이어프램 셀

- 기타 제조 공정

- 용도

- 펄프 및 종이

- 유기화학제품

- 무기화학제품

- 비누 및 세제

- 알루미나

- 섬유

- 기타 용도(식품산업)

- 지역

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 말레이시아

- 태국

- 인도네시아

- 베트남

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 터키

- 러시아

- 노르딕

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 콜롬비아

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 나이지리아

- 이집트

- 카타르

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- M&A, 합작사업, 제휴, 협정

- 시장 점유율(%)**/랭킹 분석

- 주요 기업의 전략

- 기업 프로파일

- ANWIL SA(ORLEN SA)

- BorsodChem(Wanhua)

- Ciner Group

- Covestro AG

- Dow

- Ercros SA

- Formosa Plastics Corporation

- Genesis Energy LP

- Hanwha Solutions Chemical Division Corporation

- INEOS

- KEM ONE

- Kemira

- Micro Bio Ireland Limited

- NIRMA

- Nouryon(NOBIAN)

- Occidental Petroleum Corporation

- Olin Corporation

- PCC SE

- Shandong Haihua Group Co. Ltd

- Solvay

- Spolchemie(Euro Chlor)

- Tata Chemicals Ltd

- Tosoh Asia Pte Ltd

- Vynova Group

- Westlake Vinnolit GmbH & Co. KG

제7장 시장 기회와 앞으로의 동향

- 염소 알칼리의 새로운 용도 개척

The Chlor-alkali Market size is estimated at 277.94 million tons in 2025, and is expected to reach 322.20 million tons by 2030, at a CAGR of greater than 3% during the forecast period (2025-2030).

The COVID-19 pandemic negatively affected the demand for chlor alkali across the world. During the pandemic, demand for chlor alkali products decreased in sectors such as construction, automotive, and manufacturing due to lockdowns, supply chain disruptions, and reduced economic activity. This decline in demand affected the consumption of chlorine for PVC production. However, as countries began to ease lockdown restrictions and reopen their economies, the demand for chlor alkali products rebounded. Industries that had experienced disruptions gradually resumed operations, leading to increased demand for chlorine and sodium hydroxide.

Key Highlights

- The major factors driving the market's growth are the surging demand in chemical manufacturing and the growing demand for polyvinyl chloride (PVC).

- However, the environmental impact and stringent environmental regulations are expected to hinder the chlor alkali market.

- The increasing investment in research and development and exploration of new applications of chlor alkali are expected to offer new growth opportunities to the industry.

- Asia-Pacific is likely to hold the largest market share due to the large-scale production and consumption of chlor alkali products and their derivatives.

Chlor Alkali Market Trends

The Organic Chemical Segment to Dominate the Market

- Chlorine, produced as a co-product in the electrolysis of brine during chlor alkali production, serves as a crucial feedstock in producing numerous organic chemicals. Chlorine is a versatile building block in organic synthesis, forming the basis for the production of chlorinated solvents, plastics, agrochemicals, pharmaceuticals, and other organic compounds.

- The largest consumer of chlorine is the plastics industry, particularly the production of polyvinyl chloride (PVC). PVC is widely used in construction materials, packaging, automotive parts, and various consumer goods. The demand for PVC drives significant consumption of chlorine, making the organic chemicals segment a major contributor to the chlor alkali market.

- Chlorine production and consumption continue to increase in its various end-user industries. According to Euro Chlor, by the end of December 2023, chlorine production in Europe climbed to 609,418 tonnes. On average, in December 2023, there was a decrease of 1.7% in daily production compared to November 2023 (which saw 19,659 tonnes) but an increase of 18.6% compared to December 2022 (with 16,573 tonnes).

- According to the data published by the Euro Chlor, Germany produced 5.4 million metric tons of chlorine in 2022, accounting for the country's largest chlorine production capacity.

- As per the BASF Report 2023, chemical manufacturing worldwide, not including the pharmaceutical industry, is anticipated to expand by 2.7% in 2024, a rate higher than the year before (2023: +1.7%). In China, which holds the top position in the global chemical market, a decrease in growth but still significant expansion of 4.0% compared to the robust growth in the year prior (2023: +7.5%) is anticipated.

- Thus, the factors mentioned above are expected to increase the demand for chlor alkali in the upcoming period.

Asia-Pacific to Dominate the Market

- Asia-Pacific is home to rapidly growing economies such as China, India, and Southeast Asia, which are experiencing robust industrial growth. This growth drives the demand for chlor alkali products in various industries, including construction, manufacturing, chemicals, and textiles.

- Asia-Pacific has a large manufacturing base, particularly in industries that are significant consumers of chlor alkali products such as PVC, textiles, and chemicals. The region's manufacturing sector accounts for a significant portion of global chlor alkali consumption.

- Additionally, as per China's State Council Information Office, the total profits of China's leading textile companies increased by 7.2% Y-o-Y in 2023. In the same year, China's exports of textiles and clothing reached USD 293.6 billion. The exports of textiles and clothing began to grow again in December 2023, showing a 2.6% increase from the previous year.

- Moreover, according to Invest India, India accounts for 4% of the worldwide textile and clothing trade. It is projected to reach USD 250 billion in textile manufacturing and USD 100 billion in exports by 2030.

- Furthermore, according to the data released by the National Bureau of Statistics of China, 6.98 million metric tons of plastic products were produced in December 2023 in China.

- Thus, the factors mentioned above are expected to increase the market demand for chlor alkali in Asia-Pacific.

Chlor-alkali Industry Overview

The chlor alkali market is partially fragmented. The major players in the market (not in any particular order) include Olin Corporation, Occidental Petroleum Corporation, Formosa Plastics Corporation, Dow, and Westlake Vinnolit GmbH & Co. KG.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Surging Demand in Chemical Manufacturing

- 4.1.2 Growing Demand for Polyvinyl Chloride (PVC)

- 4.2 Restraints

- 4.2.1 Environmental Impact and Stringent Environmental Regulations

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

- 4.5 Import and Export Trends

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Product

- 5.1.1 Caustic Soda

- 5.1.2 Chlorine

- 5.1.3 Soda Ash

- 5.2 Production Process

- 5.2.1 Membrane Cell

- 5.2.2 Diaphragm Cell

- 5.2.3 Other Production Processes

- 5.3 Application

- 5.3.1 Pulp and Paper

- 5.3.2 Organic Chemical

- 5.3.3 Inorganic Chemical

- 5.3.4 Soap and Detergent

- 5.3.5 Alumina

- 5.3.6 Textile

- 5.3.7 Other Applications (Food Industry)

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Malaysia

- 5.4.1.6 Thailand

- 5.4.1.7 Indonesia

- 5.4.1.8 Vietnam

- 5.4.1.9 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Turkey

- 5.4.3.7 Russia

- 5.4.3.8 NORDIC

- 5.4.3.9 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Nigeria

- 5.4.5.4 Egypt

- 5.4.5.5 Qatar

- 5.4.5.6 UAE

- 5.4.5.7 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 ANWIL SA (ORLEN SA)

- 6.4.2 BorsodChem (Wanhua)

- 6.4.3 Ciner Group

- 6.4.4 Covestro AG

- 6.4.5 Dow

- 6.4.6 Ercros SA

- 6.4.7 Formosa Plastics Corporation

- 6.4.8 Genesis Energy LP

- 6.4.9 Hanwha Solutions Chemical Division Corporation

- 6.4.10 INEOS

- 6.4.11 KEM ONE

- 6.4.12 Kemira

- 6.4.13 Micro Bio Ireland Limited

- 6.4.14 NIRMA

- 6.4.15 Nouryon (NOBIAN)

- 6.4.16 Occidental Petroleum Corporation

- 6.4.17 Olin Corporation

- 6.4.18 PCC SE

- 6.4.19 Shandong Haihua Group Co. Ltd

- 6.4.20 Solvay

- 6.4.21 Spolchemie (Euro Chlor)

- 6.4.22 Tata Chemicals Ltd

- 6.4.23 Tosoh Asia Pte Ltd

- 6.4.24 Vynova Group

- 6.4.25 Westlake Vinnolit GmbH & Co. KG

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Exploring New Applications of Chlor Alkali