|

시장보고서

상품코드

1440260

알루미늄 부품 중력 다이캐스트 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2024-2029년)Aluminum Parts Gravity Die Casting - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

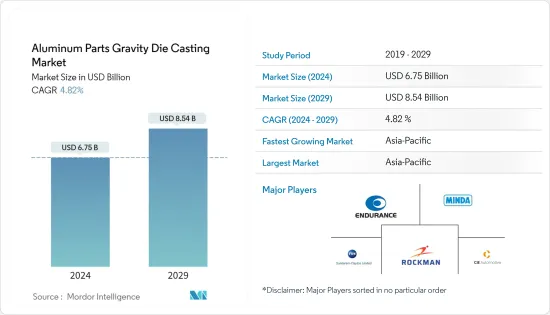

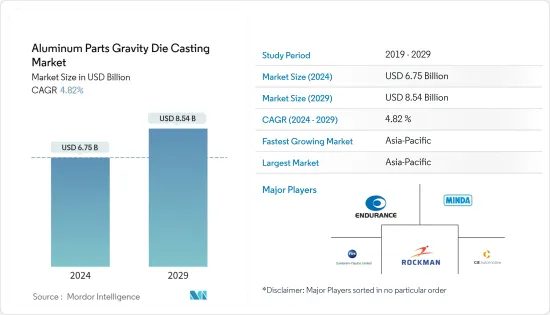

알루미늄 부품 중력 다이캐스트 시장 규모는 2024년 67억 5,0000만 달러에 이를 것으로 추정됩니다. 2029년까지 85억 4,000만 달러에 달할 것으로 예상되며, 예측 기간(2024-2029년) 동안 4.82%의 연평균 복합 성장률(CAGR)을 나타낼 전망입니다.

2020년 코로나19가 발생했을 때, 자동차 산업의 전체 공급망은 큰 영향을 받았습니다. OEM은 사업을 계속하기 위해 고군분투했습니다. 그러나 봉쇄와 제한이 완화됨에 따라 자동차 산업과 알루미늄 부품 중력 다이캐스트 시장은 모멘텀을 되찾았습니다.

이 시장은 주로 다이캐스팅 산업 공급망의 복잡성, 자동차 시장의 확대, 산업기계에서 다이캐스팅 부품의 보급 증가, 건설 분야의 성장, 전기 및 전자 분야에서 알루미늄 주물의 채택에 의해 크게 좌우됩니다.

중력 다이캐스팅은 가장 오래된 다이캐스팅 방법 중 하나입니다. 이 다이캐스팅 공정은 정확한 치수, 선명한 윤곽, 매끄럽거나 질감이있는 표면의 금속 부품을 생산하는 데 사용됩니다. 중력 다이캐스팅의 주요 장점은 빠른 생산 속도입니다.

자동차 배기가스 배출량을 줄이고 연비를 향상시키기 위한 CAFE 기준과 EPA의 정책으로 인해 자동차 제조업체들은 경량 금속을 채택하여 자동차의 무게를 줄이기 위해 노력하고 있습니다. 이후 경량화 전략으로 다이캐스팅 부품을 채택하는 것이 자동차 분야의 경량화 시장을 크게 견인하는 역할을 하고 있습니다.

알루미늄 부품 중력주조 시장 동향

엄격한 EPA 규제와 카페 기준은 시장 수요를 촉진할 가능성이 높습니다.

유럽과 북미의 자동차 규제 프레임워크는 자동차 산업의 지속 가능한 환경 구축에 기여해 왔습니다. 2011년에 도입되어 2014년 9월부터 시행된 최신 규제 프레임워크인 유로6는 이 지역의 자동차 시장 동향을 결정하는 데 중요한 규제 기준을 변경했습니다. 2013년부터 EC(유럽위원회)는 EEA/EMEP와 협력하여 유럽에 등록된 각 신차의 배기가스 성능 기준 기록을 유지하고 있습니다.

배출가스 규제는 자동차 제조업체를 하나로 묶는 요소입니다. 화물 회사와 차량 소유자는 평균 배출량을 줄일 것으로 예상되는 기술을 더 많이 도입하는 방향으로 빠르게 움직이고 있습니다. 따라서 배기가스 배출량을 줄이기 위해 차량 무게를 줄여야 하기 때문에 차량에 다이캐스팅 부품의 채택이 크게 촉진되고 있습니다.

자동차 제조업체들은 차량의 연비를 개선하고 탄소 배출량을 줄이기 위해 차량 구성품의 효율을 높이는 방법을 끊임없이 모색하고 있습니다. 이 목표를 달성하기 위해서는 효율적이고 비용에 최적화된 알루미늄 다이캐스팅 부품을 사용한 경량 구조가 중요한 역할을 합니다. Nemak과 같은 회사는 "경량화"트렌드에 초점을 맞추고 전기 자동차 제품(HPDC 공정을 사용하여 제조)을 자동차 산업에 도입하고 있습니다. 앞서 언급 한 환경 정책으로 인해 시장 수요가 증가할 것으로 예상됩니다.

아시아태평양이 시장에서 큰 비중을 차지할 것으로 예상

아시아태평양은 인도, 중국과 같은 주요 경제 국가의 존재, 주요 기업의 적극적인 참여 및 여러 정부의 이니셔티브으로 인해 세계 최대의 자동차 시장이며, 이는 알루미늄 중력의 발전에 더욱 기여할 것으로 예상됩니다. 다이캐스팅 시장. 중국은 세계 최고의 알루미늄 및 알루미늄 제품 수출국입니다. 2022년 중국의 알루미늄 수출은 전년 대비 741.4% 증가한 1 억 톤으로 2021년12월39 억 6,900 만 톤에 불과했지만 2022년 12 월에는 57 억 3,349 만 톤에 달했습니다.

아시아태평양도 전 세계적으로 중국 제품에 대한 높은 수요로 인해 코로나19 전염병의 영향에서 빠르게 회복하고 있습니다. 제조 능력의 향상과 함께 알루미늄 부품 중력 다이캐스트 시장 수요는 예측 기간 동안 성장할 것으로 예상됩니다.

2022년, 베단타(1,696,960톤), 힌달코(969,180톤), 나르코(343,460톤)는 알루미늄 생산의 3대 유명 기업이 되었습니다. 인도는 세계에서 두 번째로 주물을 생산하는 세계 2위의 주조 산업입니다. 인도의 파운드리은 국제 표준에 따라 다양한 용도의 중력 다이캐스팅 제품을 생산할 수 있습니다.

정부의 '메이크 인 인디아'에 대한 집중, 자동차 산업의 발전, 엄격한 배기가스 배출 기준은 시장 성장을 가속하고 있습니다. 2022-23년 승용차(PV) 총 수출량은 2021-22년 57만 7,875대, 2021-22년 66만 2,891대를 기록했습니다. 현대, 기아, 멀티 스즈키, 폭스바겐과 같은 기업들은 아프리카에 공장을 설립하는 대신 저렴한 제조 비용과 인도 내 부품 공급업체의 가용성을 이유로 인도산 자동차를 아프리카에 수출하고 있습니다. 이러한 모든 요인은 예측 기간 동안 아시아태평양의 알루미늄 부품 중력 다이캐스트 시장의 전반적인 발전에 기여할 것입니다.

알루미늄 부품 중력 다이캐스트 산업 개요

알루미늄 부품 중력 다이캐스트 시장은 본질적으로 세분화되어 있으며, 대규모/ 국제적인 기업뿐만 아니라 여러 국가에 걸친 지역 중소규모 기업도 많이 있습니다.

주요 기업들은 또한 다양한 합병, 확장, 제휴, 합작 투자 및 인수를 통해 전 세계적으로 사업을 확장하고 있습니다. 이 주요 기업들은 더 나은 생산 공정과 합금을 고안하기 위해 연구 개발에 수익을 집중하고 있습니다. 이 전략은 전 세계 자동차 및 산업 부문을위한 고품질 다이캐스팅 부품 생산에 도움이 될 수 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 시장 성장 촉진요인

- 시장 성장 억제요인

- 업계의 매력 - Porter의 Five Forces 분석

- 신규 진출업체의 위협

- 바이어의 교섭력

- 공급 기업의 교섭력

- 대체 제품의 위협

- 경쟁 기업간 경쟁도

제5장 시장 세분화(시장 규모, 금액)

- 용도

- 자동차

- 부품 및 컴포넌트

- 변속기 부품

- 엔진 부품

- 브레이크 부품

- 기타 부품 및 컴포넌트

- 차량 유형

- 승용차

- 상용차

- 기타 차량

- 전기 및 전자

- 산업 용도

- 기타 용도

- 자동차

- 지역

- 북미

- 미국

- 캐나다

- 기타 북미

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 기타 아시아태평양

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 남아프리카공화국

- 터키

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 벤더의 시장 점유율

- 기업 개요

- Rockman Industries

- Endurance Technologies Limited

- Minda Corporation Limited

- Hitachi Metals Ltd

- MAN Group Co.

- MRT Castings Ltd

- Harrison Castings Limited

- Vostermans Companies

- CIE Automotive

- Sundaram Clayton Ltd

- GWP Manufacturing Services AG

제7장 시장 기회와 향후 동향

LSH 24.03.14The Aluminum Parts Gravity Die Casting Market size is estimated at USD 6.75 billion in 2024, and is expected to reach USD 8.54 billion by 2029, growing at a CAGR of 4.82% during the forecast period (2024-2029).

During the COVID-19 outbreak in 2020, the entire supply chain of the automotive industry was significantly impacted. The OEMs struggled to keep their operations going. However, as the lockdowns and restrictions were relaxed, the automotive industry and the aluminum parts gravity die-casting market regained their momentum.

The market is largely driven by supply chain complexities in the die-casting industry, the expanding automotive market, increasing penetration of die-casting parts in industrial machinery, the growing constructional sector, and employing aluminum castings in the electrical and electronics sector.

Gravity die casting is one of the oldest methods of die casting. This die-casting process is used for producing accurately dimensioned, sharply defined, and smooth or textured-surface metal parts. The main advantage of gravity die casting is its high speed of production.

The CAFE standards and EPA policies to cut down automobile emissions and increase fuel efficiency are driving the automakers to reduce the weight of automobiles by employing lightweight metals. Subsequently, employing die-cast parts as a weight reduction strategy is acting as a major driver for the former market in the automotive segment.

Aluminum Parts Gravity Die Casting Market Trends

Stringent EPA Regulations and Cafe Standards are Likely to Drive Demand in the Market

The automobile regulatory frameworks in Europe and North America have been instrumental in creating a sustainable environment in the automobile industry. The latest regulatory framework, Euro 6, which was introduced in 2011 and came into effect from September 2014 onward, changed the regulatory standards that have been crucial in determining the dynamics of the automotive market in the region. Since 2013, the EC (European Commission), along with EEA/EMEP, has been maintaining the record of emission performance standards for each new vehicle registered in Europe.

The emission regulations bind the automotive manufacturers together. Freight companies and fleet owners are rapidly moving toward incorporating more technologies that are expected to reduce the average emission rate. Thereby, a need to reduce vehicle weight to lowering emission levels has greatly encouraged the employment of die-cast parts in vehicles.

Automobile manufacturers are always looking for ways to make vehicle components more efficient to improve the fuel efficiency of vehicles and reduce carbon emissions. Lightweight construction, using efficient and cost-optimized aluminum die-casted parts, plays a key role in achieving this goal. Companies like Nemak are focusing on the 'lightweight' trend and introducing electric vehicle products (manufactured by using the HPDC process) into the automotive industry. Such aforementioned environmental policies are expected to drive the demand in the market.

The Asia-Pacific Region is Expected to Hold a Significant Share in the Market

Asia-Pacific is the largest automotive market in the world due to the presence of key economies like India, China, etc., and active engagements of key players and several government initiatives, which are expected to further contribute to the development of the aluminum gravity die-casting market. China is the world's leading exporter of aluminum and aluminum products. In 2022, China's exports of aluminum increased by 741.4% year on year to 1 million mt and reached 57,349 mt in December 2022 compared to only 3,969 mt in December 2021.

The Asia-Pacific region has also recovered quickly from the impact of the COVID-19 pandemic due to the high demand for Chinese products across the world. With growing manufacturing capabilities, the demand in the aluminum parts gravity die-casting market is expected to grow during the forecast period.

In 2022, Vedanta (1,696,960 mt), Hindalco (969,180 mt), and Nalco (343,460 mt) were the three prominent companies in aluminum production. India stands as the second-largest foundry industry that produces castings in the world. Foundries in India are capable of producing gravity die-casting products that serve a wide range of applications conforming to international standards.

The government's focus on 'Make in India', developing the automotive industry, and the stringent emission norms is driving the market growth. In FY 2022-23, total passenger vehicle (PV) exports stood at 6,62,891 units in compare to 5,77,875 units in 2021-22. Companies such as Hyundai, Kia, Maruti Suzuki, and Volkswagen are exporting Indian-made cars to the African region instead of setting up their factories there because of low-cost manufacturing and availability of parts suppliers in India. All these factors contribute to the overall development of the Asia-Pacific aluminum parts gravity die casting market during the forecast period.

Aluminum Parts Gravity Die Casting Industry Overview

The market for aluminum parts gravity die casting is fragmented in nature, with the presence of many regional small-medium scale players across several countries, as well as large-scale/international players.

Key players have also expanded their operations globally through various mergers, expansions, partnerships, joint ventures, and acquisitions. These key players are focusing their revenues on R&D to come up with better production processes and alloys. This strategy may assist in the production of premium-quality die-cast parts for the global automotive and industrial sectors.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Emphasis on Lightweight Materials in Automobile and Aerospace sector

- 4.2 Market Restraints

- 4.2.1 Limited Design Flexibility

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size in Value USD Billion)

- 5.1 Application

- 5.1.1 Automotive

- 5.1.1.1 Parts and Components

- 5.1.1.1.1 Transmission Parts

- 5.1.1.1.2 Engine Parts

- 5.1.1.1.3 Brake Parts

- 5.1.1.1.4 Other Parts and Components

- 5.1.1.2 Vehicle Type

- 5.1.1.2.1 Passenger Cars

- 5.1.1.2.2 Commercial Vehicles

- 5.1.1.2.3 Other Vehicles

- 5.1.2 Electrical and Electronics

- 5.1.3 Industrial Applications

- 5.1.4 Other Applications

- 5.1.1 Automotive

- 5.2 Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.1.3 Rest of North America

- 5.2.2 Europe

- 5.2.2.1 Germany

- 5.2.2.2 United Kingdom

- 5.2.2.3 France

- 5.2.2.4 Italy

- 5.2.2.5 Rest of Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 China

- 5.2.3.2 Japan

- 5.2.3.3 India

- 5.2.3.4 South Korea

- 5.2.3.5 Rest of Asia-Pacific

- 5.2.4 South America

- 5.2.4.1 Brazil

- 5.2.4.2 Argentina

- 5.2.4.3 Rest of South America

- 5.2.5 Middle-East and Africa

- 5.2.5.1 South Africa

- 5.2.5.2 Turkey

- 5.2.5.3 Rest of Middle-East and Africa

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Rockman Industries

- 6.2.2 Endurance Technologies Limited

- 6.2.3 Minda Corporation Limited

- 6.2.4 Hitachi Metals Ltd

- 6.2.5 MAN Group Co.

- 6.2.6 MRT Castings Ltd

- 6.2.7 Harrison Castings Limited

- 6.2.8 Vostermans Companies

- 6.2.9 CIE Automotive

- 6.2.10 Sundaram Clayton Ltd

- 6.2.11 GWP Manufacturing Services AG

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Adoption of Electric Vehicles

- 7.2 Improved Tooling Design, Computer-aided Simulation, and Process Control Systems