|

시장보고서

상품코드

1440362

의료비 지불자 서비스 : 세계 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2024-2029년)Global Healthcare Payer Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

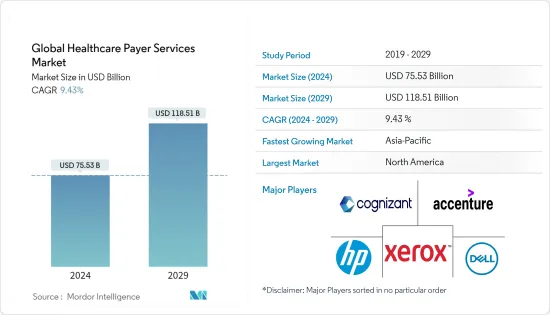

세계의 의료비 지불자 서비스 시장 규모는 2024년 755억 3,000만 달러로 추정되고, 2029년까지 1,185억 1,000만 달러에 이를 것으로 예측되며, 예측기간(2024-2029년) 중 9.43%의 연평균 복합 성장률(CAGR)로 성장할 전망입니다.

COVID-19는 의료비 지불자 서비스 시장에 큰 영향을 미칩니다. 많은 지불자는 의료 제공업체의 안정화를 지원하기 위해 독자적으로 재정적 지원과 자금을 투입하고, 비의료 서비스의 조정으로부터 예방접종의 대처의 지원까지, 기술 능력과 커뮤니티와의 연결을 이용해 아웃 브레이크에 대한 대응을 지원했습니다.

시장 성장을 견인하는 주요 요인으로는 건강 보험 도입 증가, 건강 관리 사기 증가, 만성 질환 부담 증가 등이 있습니다.

2022년 5월에 갱신된 경제협력개발기구 통계에 따르면 체코공화국, 덴마크, 핀란드, 아일랜드 등 유럽의 많은 국가들은 2020년에 100% 정부 및 사회건강보험을 도입하고 있습니다. 국민을 위한 정부의 건강보험은 의료지급자 서비스의 도입으로 시장을 견인하게 될 것입니다.

또한 2021년 8월 아시아의 선도적인 민간 대체 투자 회사 중 하나인 베어링 프라이빗 주식 아시아(BPEA)는 건강 관리 서비스 사업을 힌두자 세계 솔루션과 관련된 펀드에 인수하는 공식 계약을 체결했습니다. 이러한 인수는 기업의 성장을 더욱 촉진할 것으로 보입니다. 성장을 통한 의료비 지불자 서비스 시장.

또한, 만성 질환 증가는 의료 보험에 대한 길을 더욱 열어 의료비 지불자 서비스의 도입으로 이어지고 시장 성장을 가속합니다. 예를 들어 국제 당뇨병 연합 2021년판에 따르면 20세부터 79세까지 약 5억 3,700만 명이 당뇨병을 앓고 있습니다. 2030년까지 당뇨병 환자의 총 수는 6억 4,300만 명에 달했으며 2045년까지 7억 8,300만 명에 이를 것으로 예상됩니다. 또한 Globocan 2020에 따르면 2020년에는 전 세계적으로 새로운 암 환자 수가 19,292,789명, 사망자 수가 9,958,133명에 달했다고 보고되었습니다. 이러한 만성질환의 상당한 부담이 의료용 의약품의 채용 증가로 이어져 시장의 대폭적인 성장을 가속할 것으로 예상됩니다.

그러나 데이터 침해 발생률, 기밀성 상실, 아웃소싱과 관련된 예기치 않은 비용 등의 요인이 시장을 방해할 것으로 예상됩니다.

의료비 지불자 서비스 시장 동향

보험금 청구 관리 서비스 부서는 시장에서 큰 점유율을 차지할 것으로 예상됩니다.

보험금 청구 관리 서비스 부서는 의료비 지불자 서비스 시장에서 큰 점유율을 차지할 것으로 예상되며, 예측 기간 동안에도 유사한 점유율을 유지할 것으로 예상됩니다.

전통적으로 건강 관리 종사자는 환자에게 서비스를 제공하고 지불자는 그것을 확인하고 환불합니다. 환자의 참여가 없으면 사기와 남용의 가능성이 높아집니다.

또한 2021년 10월에는 Blue Shield of California와 Google Cloud가 협력하여 회원을 위한 실시간 결제를 처리하는 결제 제공업체에 대한 새로운 접근 방식을 만들었습니다. 헬스케어 청구를 디지털화하고 청구 정보의 품질과 적시성을 높이기 위해 기업은 클라우드 프로세싱, 자동화, 인공지능 및 머신러닝 기술을 도입합니다. 이러한 협업은 보험금 청구 관리 서비스 채택 증가로 시장 성장을 가속합니다.

게다가 2020년 9월 Journal of Medical Internet 조사에 게재된 「헬스케어의 부정행위 및 남용와의 싸움 : 블록체인 사기대책 프레임워크의 개념화와 프로토타이핑 연구」라는 제목의 연구에 따르면, 의료 사기와 남용으로 인해 26억 달러의 손실이 발생한 것으로 추정됩니다. 이러한 발생률은 보험금 청구관리서비스 채용 증가로 이어져 예측기간 동안 시장의 성장을 가속합니다.

따라서 이 부문은 위의 요인으로 인해 시장 성장을 이끌 것으로 예상됩니다.

북미가 주요 점유율을 차지하고 있으며 예측 기간 동안에도 비슷한 성장이 예상됩니다.

북미는 조사 대상 시장에서 큰 점유율을 차지하고 있으며 예측 기간 동안 비슷한 점유율을 차지할 것으로 예상됩니다. 의료비 지불자 서비스 시장의 대폭적인 성장 요인으로는 헬스케어 정책 채용 증가, 이 지역의 고급 헬스케어 시스템, 이 지역의 주요 시장 기업의 강력한 발판 등이 있습니다.

의회 조사국이 발행한 「미국의 의료 보험의 적용 범위와 지출」(2022년 4월 갱신)이라는 타이틀의 기사에 의하면, 2020년에는 대부분의 사람이 민간의 의료 보험에 가입되어 있거나 정부의 프로그램(메디케어나 메디케이드 등)의 대상이 되어 있었다고 합니다. 또한 같은 출처에 따르면 2020년에는 개인(무보험자 포함), 의료보험회사, 연방 및 주정부가 다양한 유형의 의료소비 지출(HCE)에 3조 9,000억 달러를 지출했으며 국가 총 지출의 18.8%를 차지했다고 합니다. 이 지역의 건강 관리 소비에 대한 이러한 엄청난 투자는 보험 청구를 위한 의료비 지불자 서비스의 채택으로 이 지역의 이 시장 성장을 가속할 수 있습니다.

게다가 2021년 12월 미국 메디케어 메디케이드 서비스 센터에 따르면 COVID-19 감염의 팬데믹은 미국 사회의 다른 많은 부분과 마찬가지로 2020년 의료 분야에 중대한 영향을 미쳤고, 9.7% 증가를 밀어 올렸다고 합니다. 국민 건강 관리의 총액은 4조 1,000억 달러에 달했습니다. 국민 건강 관리를 통한 엄청난 투자는 의료비 지불자 서비스 채택 증가로 이어져 시장 성장을 가속합니다.

게다가 이 지역에서 선도적인 기업들의 강력한 발판은 최종 사용자가 다양한 서비스를 채택함으로써 시장 성장을 견인하고 시장 성장을 견인할 것으로 예상됩니다. 예를 들어 Cognizant Technology Solutions, Hewlett-Packard, Xerox Corporation 등 주요 기업은 미국에 본사를 두고 있습니다.

따라서 위의 요인으로 인해 이 지역 시장이 성장할 것으로 예상됩니다.

의료비 지불자 서비스 산업 개요

의료비 지불자 서비스 시장은 적당한 경쟁이 계속되고 있습니다. 시장은 주요 시장 기업이 선택한 전략, 최종 사용자가 서비스를 채택하고, 건강 관리 정책을 높이는 등의 요인에 의해 움직입니다. 주요 시장 기업에는 Cognizant Technology Solutions, Accenture PLC, Hewlett-Packard, Xerox Corporation, Dell, Inc., Genpact Limited 및 HCL Technologies Ltd. 등이 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제 조건 및 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 시장 개요

- 시장 성장 촉진요인

- 건강 보험 가입 증가

- 헬스케어 사기 증가

- 증대하는 만성질환의 부담

- 시장 성장 억제요인

- 데이터 침해 및 기밀 유지 손실의 높은 발생률

- 아웃소싱에 따른 예기치 않은 비용

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체 제품의 위협

- 경쟁 기업간 경쟁 관계의 격렬

제5장 시장 세분화

- 서비스 유형별

- 비즈니스 프로세스 아웃소싱

- IT 아웃소싱 서비스

- 지식 프로세스 아웃소싱(KPO) 서비스

- 용도별

- 클레임 관리 서비스

- 프론트 오피스 서비스 및 백 오피스 업무 통합

- 회원 관리 서비스

- 공급자 관리 서비스

- 청구 및 계정 관리 서비스

- 분석 및 부정행위 관리 서비스

- 인재 서비스

- 최종 사용자별

- 민간 지불자

- 공적 지불자

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 기업 프로파일

- Cognizant Technology Solutions

- Accenture PLC

- Synnex Corporation(Concentrix Corporation)

- Hewlett-Packard

- Xerox Corporation

- Dell, Inc.

- Genpact Limited

- HCL Technologies Ltd.

- Wipro Limited

- Change Healthcare Inc.

- HMS Holding Corp.

- McKESSON Corporation

제7장 시장 기회 및 미래 동향

AJY 24.03.15The Global Healthcare Payer Services Market size is estimated at USD 75.53 billion in 2024, and is expected to reach USD 118.51 billion by 2029, growing at a CAGR of 9.43% during the forecast period (2024-2029).

Covid-19 has significantly impacted the healthcare payer services market. For instance, according to the article published in the National Academy of Medicine, titled 'Health Care Payers COVID-19 Impact Assessment: Lessons Learned and Compelling Needs' in May 2021, payers took steps to expand access to health care for COVID-19 and non-COVID-19 health issues in the spring of 2020, based on regulatory requirements and recommendations (e.g., waiving administrative requirements, reimbursing telehealth). Many payers also deployed financial support and capital on their own to help providers stabilize, and they used their technological capabilities and community links to help with outbreak response, from coordinating non-medical services to supporting immunization efforts.

The major factors driving the market growth include the rise in the adoption of health insurance, the rise in healthcare frauds, the growing burden of chronic diseases, and others.

According to the Organisation for Economic Co-operation and Development statistics updated in May 2022, many European Countries, such as the Czech Republic, Denmark, Finland, and Ireland, among others have 100% Government/Social health insurance in 2020. Such adoption of health insurance from the government for its citizens will drive the market due to the adoption of healthcare payer services.

Furthermore, in August 2021, Baring Private Equity Asia (BPEA), one of Asia's major private alternative investment firms, signed formal agreements with Hinduja Global Solutions to buy its Healthcare Services business to funds linked with Such acquisitions will further lead to drive the growth of healthcare payer services market due to growth.

In addition, the rise in chronic diseases will further pave the way for health insurance, leading to the adoption of healthcare payer services and driving the market growth. For instance, according to the International Diabetic Federation 2021, diabetes affects around 537 million persons aged 20 to 79. By 2030, the overall number of diabetics is expected to reach 643 million, and by 2045, it will reach 783 million. Furthermore, according to Globocan 2020, there were 19,292,789 new cancer cases seen in 2020 across the globe, and 9,958,133 deaths were reported globally in 2020. Such a huge burden of chronic diseases will lead to increased adoption of ethical medication, driving the market growth significantly.

However, factors such as high incidences of data breaches, loss of confidentiality, and unpredicted costs associated with outsourcing are expected to hinder the market.

Healthcare Payer Services Market Trends

Claims Management Services Segment Is Expected To Hold A Major Share In The Market.

The claim management services segment is expected to hold a major share in the healthcare payer services market and will do the same over the forecast period.

Traditionally, a healthcare practitioner provides services to a patient, which the payer then confirms and reimburses. The absence of patient involvement raises the possibility of fraud and abuse.

Additionally, in October 2021, Blue Shield of California and Google Cloud collaborated to create a new approach to paying providers that will process claims in real-time for members. To digitize healthcare claims and enhance the quality and timeliness of billing information, the firms would deploy automated processing, artificial intelligence, and machine learning technologies on a cloud platform. Such collaborations will drive market growth due to the rise in the adoption of claim management services.

In addition, according to the study published in the Journal of Medical Internet Research, titled 'Combating Health Care Fraud and Abuse: Conceptualization and Prototyping Study of a Blockchain Antifraud Framework' in September 2020, It is estimated USD 2.6 billion loss is attributed to health care fraud and abuse. Such incidences will lead to increased adoption of claim management services, driving the market growth over the forecast period.

Therefore, this segment is expected to drive market growth owing to the abovementioned factors.

North America Holds a Major Share and Expected to do Same Over the Forecast Period

North America holds a significant share in the market studied and is expected to do the same over the forecast period. The factors attributed to the significant growth of the healthcare payer services market include the rise in adoption of healthcare policies, the sophisticated healthcare system in this region, and the strong foothold of key market players in this region, among others.

According to the article published by the Congressional Research Service, titled 'The United States Health Care Coverage and Spending,' updated in April 2022, most people had private health insurance or were covered by a government program (such as Medicare or Medicaid) in 2020. Furthermore, according to the same source, in 2020, individuals (including the uninsured), health insurers, and federal and state governments spent USD 3.9 trillion on various types of health consumption expenditures (HCE), accounting for 18.8% of the country's gross domestic product. Such a huge investment in healthcare consumption in this region will lead to driving the growth of this market in this region due to the adoption of healthcare payer services to claim insurance.

Furthermore, in December 2021, according to the United States Centers for Medicare and Medicaid Services, the COVID-19 epidemic, like so many other parts of American society, had a significant impact on the country's health sector in 2020, pushing a 9.7% increase in total national healthcare spending to USD 4.1 trillion. The high investments by national healthcare will lead to higher adoption of healthcare payer services, driving the market growth.

In addition, the strong foothold of major players in this region is also expected to drive the market growth due to the adoption of various services by the end user, driving the market growth. For instance, key players such as Cognizant Technology Solutions, Hewlett-Packard, and Xerox Corporation are headquartered in the United States.

Therefore, the market is expected to propel in this region due to the abovementioned factors.

Healthcare Payer Services Industry Overview

The market for healthcare payer services is moderately competitive. The market is driven by the factors such as the strategies opted by the key market players, adoption of services by the end-users, and rise in healthcare policies, among others. Some of the key market players include Cognizant Technology Solutions, Accenture PLC, Hewlett-Packard, Xerox Corporation, Dell, Inc., Genpact Limited, and HCL Technologies Ltd., among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rise In Adoption of Health Insurance Policies

- 4.2.2 Rise In Healthcare Frauds

- 4.2.3 Growing Burden of Chronic Diseases

- 4.3 Market Restraints

- 4.3.1 High Incidences of Data Breaches and Loss of Confidentiality

- 4.3.2 Unpredicted Costs Associated With Outsourcing

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD million)

- 5.1 By Service Type

- 5.1.1

Business Process Outsourcing

- 5.1.2 IT Outsourcing Services

- 5.1.3 Knowledge Process Outsourcing (KPO) Services

- 5.2 By Application

- 5.2.1 Claims management services

- 5.2.2 Integrated front office service and back office operations

- 5.2.3 Member management services

- 5.2.4 Provider management services

- 5.2.5 Billing and accounts management services

- 5.2.6 Analytics and fraud management services

- 5.2.7 Human Resource Services

- 5.3 By End User

- 5.3.1 Private Payers

- 5.3.2 Public Payers

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle-East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle-East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Cognizant Technology Solutions

- 6.1.2 Accenture PLC

- 6.1.3 Synnex Corporation (Concentrix Corporation)

- 6.1.4 Hewlett-Packard

- 6.1.5 Xerox Corporation

- 6.1.6 Dell, Inc.

- 6.1.7 Genpact Limited

- 6.1.8 HCL Technologies Ltd.

- 6.1.9 Wipro Limited

- 6.1.10 Change Healthcare Inc.

- 6.1.11 HMS Holding Corp.

- 6.1.12 McKESSON Corporation