|

시장보고서

상품코드

1441584

자동차용 슈퍼차저 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2024-2029년)Automotive Supercharger - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

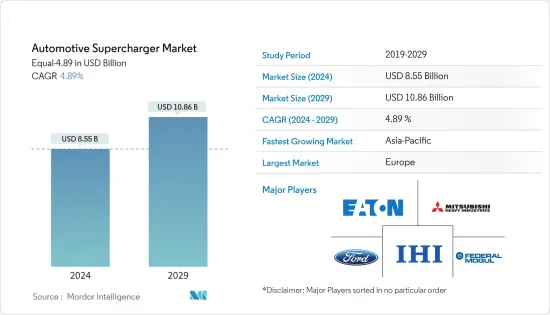

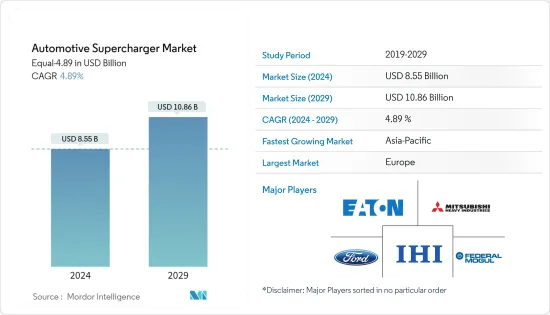

자동차 슈퍼차저 시장 규모는 예측기간(2024-2029년) 동안 4.89%의 연평균 복합 성장률(CAGR)로 성장할 전망이며, 2024년 85억 5,000만 달러에서 2029년까지 108억 6,000만 달러로 성장할 것으로 예상됩니다.

장기적으로는 엔진에 고출력을 제공하고 효율을 향상시키기 위한 자동차용 슈퍼차저 기술의 강화, 연료 효율이 높고 경량인 컴포넌트에 대한 수요 증가가 세계 자동차용 슈퍼차저 시장 성장의 주요 결정 요인이 될 것입니다. 또한 신에너지 자동차 도입을 위한 정부의 적극적인 추진으로 다양한 액화석유(LPG), 압축천연가스(CNG), 수소기반 자동차가 시장에 통합되어 첨단 자동차 수요에 긍정적인 영향을 줄 것입니다. 제조업체는 이러한 차량 모델에 고출력 엔진을 통합하는 것을 점점 선호하기 때문에 수퍼차저 시스템도 마찬가지입니다.

유럽 자동차공업회(ACEA)에 따르면 2022년 유럽연합에 등록된 신차 중 36.4%가 가솔린 기반으로 디젤은 16.4%를 차지했습니다.

그러나 전기 자동차는 일반적인 내연 기관을 갖추고 있지 않기 때문에 탄소 중립 차량의 이용을 요구하는 소비자의 기호 증가에 의한 전기 자동차 도입 증가가 자동차용 슈퍼차저 시장의 성장의 큰 저해 요인이 되었습니다. 게다가 가솔린 및 디젤 기반 자동차를 금지하는 정부의 엄격한 규제는 향후 수년간 슈퍼차저 수요에 악영향을 미칠 것으로 보입니다.

예를 들어, 유럽 연합은 2023년 3월에 유럽에서 판매되는 모든 신차와 밴을 2035년까지 제로 방출해야 하는 새로운 법률을 승인했습니다.

또한 차량의 전동화가 진행됨에 따라 자동차 제조업체는 각 생산 기지를 폐쇄하고 있습니다. 예를 들어, 스텔란티스는 2022년 11월 브라질의 캄포 라르고에 있는 피아트 파워트레인 테크놀로지스(FPT) 엔진 공장의 폐쇄를 발표했지만, 이는 2038년까지 제로 방출을 달성하는 회사의 목표를 위해 발표된 것입니다.

다양한 자동차 제조업체들은 버스, 픽업 트럭, 밴 등의 디젤 구동 상업용 차량에 폭넓게 사용할 수 있는 디젤 기반 슈퍼차저를 개발하기 위한 다양한 전략을 세우고 있습니다. 아시아태평양은 인도와 중국 등 국가에서 예상되는 디젤 차량의 판매 증가로 예측 기간 동안 자동차용 슈퍼차저의 가장 빠르게 성장하는 시장이 될 것으로 예상됩니다. 북미, 유럽, 아시아태평양은 경량, 고출력, 고효율 엔진을 고객에게 제공하기 위해 끊임없이 전략을 세우는 선도적인 자동차 제조업체의 존재와 차세대 자동차 수요로 이 지역에서는 세계의 자동차용 슈퍼차저 시장을 독점하고 있습니다.

자동차용 슈퍼차저 시장 동향

승용차 부문이 예측 기간 동안 시장을 독점합니다.

내연기관(ICE) 승용차가 친숙하고 많은 신흥국에서는 전기자동차의 충전 인프라가 부족한 것이 EV의 보급을 방해하고 있습니다. 따라서 소비자는 여전히 ICE가 장착된 자동차를 사용하기를 선호하며, 결과적으로 고출력이며, 보다 효율적인 자동차를 고객에게 제공하기 위해 이러한 자동차 엔진 시스템의 지속적인 혁신으로 이어졌습니다. 따라서 고출력 승용차에 대한 수요 증가는 세계 자동차용 슈퍼차저 수요의 급증에 기여하고 있습니다. 예를 들어,

2022년 인도 승용차 판매 전체에서 차지하는 가솔린 차량의 비율은 68%에 달했고, 디젤 차량은 전체 시장의 19%를 차지했습니다. 마찬가지로 그리스에서는 2022년 자동차 판매 전체의 71.3%를 가솔린차가 차지했으며, 동기간 디젤차는 17.42%를 차지했습니다.

슈퍼차저 제조업체는 경량으로 출력이 크고 연비가 높은 가장 컴팩트한 제품을 개발함으로써 경쟁에 앞서 노력하고 있습니다. 게다가 이 제조업체들은 차량 전체의 중량을 줄이고 배출가스를 줄이기 위해 슈퍼차저 제품의 소형화에 끊임없이 노력하고 있습니다.

게다가 고급차의 채용 증가에 의해 고출력 엔진의 생산이 대폭 증가하고 있어 슈퍼차저 수요를 뒷받침하고 있습니다. 예를 들어 BMW, 메르세데스 벤츠, 아우디 등 고급 브랜드의 판매량은 2022년 각각 240만대, 207만대, 161만대에 달했습니다. 엔진 제조업체는 지역 전체 가솔린 자동차 및 디젤 자동차 판매 수요 증가에 대응하기 위해 비즈니스 잠재력을 확대하고 있습니다. 예를 들어,

2022년 11월 프랑스 자동차 대형 르노 그룹은 장기 비전에서 IC 엔진 생산에 주력할 계획에 대해 논의했습니다. 이 회사는 미래 하이브리드 자동차 및 IC 엔진 차량용 생산 유닛 설립, 파워트레인 및 IC 엔진 공급에 대한 구속력이 없는 프레임워크 계약을 GeelyHoldings와 체결했습니다.

도요타는 2022년 4월 하이브리드 전기차를 포함한 4기통 엔진의 생산을 지원하기 위해 미국의 4개 제조 공장에 3억 8,300만 달러를 투자할 것이라고 발표했습니다. 또한 알라바마 토요타의 헌츠빌 공장은 114,000평방 피트의 부지를 확장하고 내연 및 하이브리드 전기 파워트레인용 엔진을 생산하기 위한 새로운 4기통 생산 라인을 설치하기 위해 2억 2,200만 달러를 받았습니다.

엔진 기술의 급속한 향상과 애프터마켓에서 수요 증가로 인해 예측 기간 동안 자동차 슈퍼차저에 대한 엄청난 수요가 존재할 것으로 예상됩니다.

아시아태평양은 예측 기간 동안 가장 빠르게 성장하는 시장이 됩니다.

아시아태평양은 중국, 인도, 일본 등 주요 자동차 허브의 존재로 세계에서 판매되는 차량의 거의 50%가 이 지역에서 생산되고 있으며 가장 빠르게 성장하는 시장이 될 것으로 예상되고 있습니다. 아시아태평양에서는 향후 몇 년동안 더욱 성장이 예상됩니다. 엔진의 고출력화에 대한 요구는 해마다 증가하고 있습니다. 아시아에서는 엔진의 다운 사이징에 대한 경향이 변화하고 있으며, V6에 슈퍼차저를 장비하는 것이 V8 엔진을 탑재한 차량보다 효율적임이 밝혀졌습니다.

게다가 아시아태평양에서는 자동차 판매가 눈부시고, 엔진 전체에 이어 슈퍼차저 수요가 플러스 방향으로 향하고 있습니다. 예:

중국 기차공업협회(CAAM)에 따르면 2023년 10월 승용차 총 판매량은 24만 8,800대에 달했으며 2022년 동시기에 비해 전년 대비 11.4% 증가했습니다. 그 후, 2023년 1월부터 10월까지의 승용차 총 판매 대수는 206만 6,400대에 달하고, 2022년의 동시기에 비해 전년 대비 7.5%의 성장을 기록했습니다.

마찬가지로 인도의 승용차 판매량은 2022년 10월의 29만 1,113대에 비해 2023년 10월에는 34만 1,377대에 달하고, 전년 대비 17.2%의 성장세를 보였습니다. 동시에 일본 자동차 판매협회 연합회와 전국 소형 자동차 이륜차 협회에 따르면 2023년 10월 배기량 660cc 이상 판매 대수는 전년 대비 14.9% 증가한 24만 3,144대, 배기량 660cc 미만 차량은 4.7% 증가의 15만 4,528대가 되었습니다.

OEM은 높은 토크와 성능을 얻기 위해 기술적으로 첨단 엔진 개발에 주력하고 있으며 이러한 차량에 첨단 슈퍼차저를 통합하여 대응하고 있습니다. 다연료 엔진 기술의 출현은 예측 기간 동안 아시아태평양 전체의 자동차용 슈퍼차저 시장의 적극적인 기업에게 유리한 기회를 제공할 것으로 예상됩니다.

자동차용 슈퍼차저 산업 개요

자동차용 슈퍼차저 시장은 생태계 내에서 활동하는 다양한 국제 및 지역 기업의 존재로 세분화되어 매우 경쟁력이 있습니다. 기업은 슈퍼차저 분야에서 지속적인 제품 혁신을 위해 연구개발 활동에 엄청난 투자를 적극적으로 실시했습니다. 예를 들어, 2023년 12월-텍사스에 본사를 둔 하이퍼커 제조업체로 고성능 자동차 개발 회사인 헤네시는 제너럴 모터스의 V8 엔진을 탑재한 픽업 트럭의 종합적인 업그레이드를 발표했습니다. 이 업그레이드에는 슈퍼차저가 통합되어 최고 출력 650 마력, 최고 출력 658 파운드 피트를 실현할 예정입니다. 또한 이 회사는 슈퍼차저가 기존 시에라와 실버라드의 6.2리터 V8(L87 EcoTec3) 라인업에서 업그레이드되고 있어 순정비로 마력을 55% 향상시킬 수 있다고 말했습니다.

2023년 7월-Whipple Superchargers는 6.6리터(L8T) V8 엔진용 3.0리터 슈퍼차저 시스템 출시를 발표했습니다. 이 V8 가스 엔진은 스톡 형식으로 401 마력과 464 파운드 피트 토크를 발생하며 GMC 시에라 2500 HD 및 3500 HD와 같은 일반 모터의 헤비 듀티 픽업에 표준 장착되어 있습니다. 또한 이 회사는 신개발 슈퍼차저가 토크를 추가로 236lb-ft 증가시키고 총 700파운드 증가시키는 능력이 있다고 말했습니다.

이 기업들이 업계에서 경쟁력을 얻으려고 하기 때문에 시장은 첨단 디젤 슈퍼차저 기술의 급속한 강화와 출시가 예상됩니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제 조건

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 시장 성장 촉진요인

- 시장 성장을 가속하는 고급차 수요 증가

- 시장 성장 억제요인

- 전기 자동차의 보급이 시장의 성장을 방해합니다.

- 업계의 매력-Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체 제품의 위협

- 경쟁 기업간 경쟁 관계의 격렬

제5장 시장 세분화(금액별 시장 규모)

- 기술별

- 원심 슈퍼차저

- 루트 슈퍼차저

- 트윈 스크류 슈퍼차저

- 연료 유형별

- 가솔린

- 디젤

- 전원별

- 엔진 구동

- 전동 모터 구동

- 판매 채널별

- 주문자 상표 부착 생산(OEM)

- 애프터마켓

- 차종별

- 승용차

- 상용차

- 지역별

- 북미

- 미국

- 캐나다

- 북미의 다른 지역

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 기타 아시아태평양

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 사우디아라비아

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 벤더의 시장 점유율

- 기업 프로파일

- Ferarri NV

- Eaton Corporation PLC

- Mitsubishi Heavy Industries Ltd.

- Koenigsegg Automotive AB

- Honeywell Inc.

- IHI Corporation

- Vortech Engineering

- Federal-Mogul Corporation

- A&A Corvette

- Rotrex A/S

- Aeristech

- Daimler AG

- Ford Motor Company

제7장 시장 기회 및 미래 동향

- 디젤 수퍼차저 기술의 급속한 향상으로 시장 수요 증가

The Automotive Supercharger Market size in terms of Equal-4.89 is expected to grow from USD 8.55 billion in 2024 to USD 10.86 billion by 2029, at a CAGR of 4.89% during the forecast period (2024-2029).

Over the long term, the enhancement in the automotive supercharger technology to provide higher-power output to engines, better efficiency, and the growing demand for fuel-efficient and lightweight components will serve as major determinants for the growth of the automotive supercharger market across the world. Further, the government's aggressive push towards the adoption of new-energy vehicles will witness the integration of various liquefied petroleum (LPG), compressed natural gas (CNG), and hydrogen-based vehicles in the market, which will positively impact the demand for advanced supercharger systems, as manufacturers will increasingly prefer to integrate high powered engines in these vehicle models.

According to the European Automobile Manufacturers' Association (ACEA), 36.4% of all new cars registered in the European Union were petrol-based, while diesel accounted for 16.4% of registrations in 2022.

However, the rising adoption of electric vehicles, owing to the increasing consumers' preference towards availing carbon-neutral vehicles, is serving as a major deterrent to the growth of the automotive supercharger market, as electric vehicles do not possess regular internal combustion engines. Coupled with that, strict government regulations to ban petrol and diesel-based cars will negatively impact the demand for superchargers in the coming years.

For instance, in March 2023, the European Union approved a new law requiring that all new cars and vans sold in Europe must be zero-emission by 2035.

Moreover, with the rising electrification of vehicle fleets, automakers are shutting down their respective production bases. For instance, In November 2022, Stellantis announced the closure of its Fiat Powertrain Technologies (FPT) engine plant in Campo Largo, Brazil, which was announced due to the company's aim to achieve zero emissions by 2038.

Various automakers are extensively strategizing to pivot towards the development of diesel-based superchargers as they can be extensively used in diesel-operated commercial vehicles such as buses, pickup trucks, and vans, among others. The Asia-Pacific region is anticipated to become the fastest-growing market for automotive superchargers during the forecast period, owing to the increasing diesel vehicle sales expected in countries such as India and China. North America, Europe, and Asia-Pacific regions dominate the global automotive supercharger market due to the presence of leading automakers in these regions which are constantly strategizing to offer lightweight, high-power, and efficient engines to customers and the subsequent demand for luxury vehicles in these regions.

Automotive Supercharger Market Trends

Passengers Cars Segment to Dominate the Market during the Forecast Period

The familiarity with internal combustion engine (ICE) passenger cars and the lack of electric vehicle charging infrastructure in many emerging countries hampers the penetration of EVs. Hence, consumers still prefer availing of ICE-powered cars, which in turn leads to constant innovations in the engine systems of these vehicles to offer higher-powered and more efficient vehicles to customers. Therefore, the increasing demand for higher-powered passenger cars contributes to the surging demand for automotive superchargers across the world. For instance,

In 2022, the share of petrol cars in the overall passenger car sales in India touched 68%, while diesel cars accounted for 19% of the overall sales in the market. Similarly, in Greece, sales of petrol cars accounted for 71.3% of the overall car sales in 2022, while diesel-operated cars accounted for 17.42% during the same period.

Supercharger manufacturers try to stay ahead of the competition by building the most compact products that are lightweight, have greater power output, and have a higher fuel economy. Moreover, these manufacturers are constantly working towards downsizing their supercharger offerings to assist in decreasing the overall curb weight of the vehicle and reducing emissions.

Furthermore, the production of high-powered engines is witnessing a massive surge due to the increasing adoption of luxury vehicles, which, in turn, assists the demand for superchargers. For instance, sales of luxury brands, such as BMW, Mercedes-Benz, and Audi, touched 2.4 million units, 2.07 million units, and 1.61 million units, respectively, in 2022. Engine manufacturers are expanding their business potential to meet the rising demand for gasoline and diesel vehicle sales across the geography. For instance:

In November 2022, French automotive giant Renault Groupe discussed its plans to focus on producing IC engines during its longer-term vision. The company has signed a non-binding framework agreement with GeelyHoldings for establishing production units, supply power trains, and IC engines for upcoming mild hybrid and IC engine vehicles.

In April 2022, Toyota announced an investment of USD 383 million in four of its US manufacturing plants to support the production of its four-cylinder engines, including hybrid electric vehicles. In addition, Toyota Alabama in Huntsville plant received USD 222 million to expand 114,000 sq ft and install a new four-cylinder production line to produce engines for both combustion and hybrid electric powertrains.

With the rapid enhancement in engine technology and the rising demand in the aftermarket, there will exist a massive demand for automotive superchargers during the forecast period.

Asia-Pacific Region to become the Fastest Growing Market during the Forecast Period

Asia-Pacific is expected to become the fastest-growing market, as almost 50% of the vehicles sold globally are from this region due to the presence of major automotive hubs like China, India, and Japan, which is further anticipated to grow in the coming years. The need for higher-powered engines has been increasing year-on-year. Asia has witnessed a change in the trend toward downsizing engines, wherein equipping a V6 with a supercharger is found to be more efficient than equipping a vehicle with a V8 engine.

Further, the Asia-Pacific region is witnessing impressive vehicle sales, which have taken the overall engine and, subsequently, supercharger demand on the positive side. For instance:

According to the China Association of Automobile Manufacturers (CAAM), total passenger car sales in October 2023 touched 248.8 thousand units, showcasing a Y-o-Y growth of 11.4% compared to the same period in 2022. Subsequently, total passenger car sales between January and October 2023 touched 2,066.4 thousand units, witnessing a Y-o-Y growth of 7.5% compared to the same period in 2022.

Similarly, passenger car sales in India touched 341,377 units in October 2023, compared to 291,113 units in October 2022, representing a Y-o-Y growth of 17.2%. Simultaneously, according to the Japan Automotive Dealers Association and Japan Light Motor Vehicle and Motorcycle Association, in October 2023, sales with engine displacements above 660cc increased 14.9% to 243,144 units, while vehicles with engine displacements below 660cc increased 4.7% to 154,528 units compared to the previous month.

OEMs have been focusing on developing technologically advanced powered engines to gain high torque and performance, which is being catered to by integrating advanced superchargers in these vehicles. The emergence of multi-fuel engine technology is expected to provide lucrative opportunities to the active players in the automotive supercharger market across the Asia-Pacific region during the forecast period.

Automotive Supercharger Industry Overview

The automotive supercharger market is fragmented and highly competitive due to the presence of various international and regional players operating in the ecosystem. Some of the major players include Eaton Corporation PLC, Mitsubishi Heavy Industries Ltd., IHI Corporation, Federal-Mogul Corporation, Ford Motor Company, Honeywell Inc., Vortech Engineering, Aeristech, and Daimler AG, among others. These players are actively engaged in investing hefty sums in their R&D activity for constant product innovation in the realm of superchargers. For instance, in December 2023, Hennessey, the Texas-based hypercar manufacturer and high-performance vehicle creator announced comprehensive upgrades for General Motor's V8-powered pickup trucks, which will be integrated with a supercharger to deliver 650 bhp and 658 lb-ft of torque. Further, the company stated that its supercharger is upgraded from its existing Sierra and Silverado's 6.2-liter V8 (L87 EcoTec3) lineup, which can increase horsepower over stock by 55%.

In July 2023, Whipple Superchargers announced that the launch of its 3.0-liter supercharger system for the 6.6-liter (L8T) V8 engine. This V8 gas engine produces 401 horsepower and 464 lb-ft of torque in stock form and is standard fitment on General Motors' Heavy Duty pickups like the GMC Sierra 2500 HD and 3500 HD. Further, the company stated that the newly developed supercharger has the capability of boosting the torque by an additional 236 lb-ft for a total of 700.

The market is anticipated to witness a rapid enhancement and launch of advanced diesel supercharger technology as these players try to gain a competitive edge in the industry.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Increasing Demand for Luxury Vehicles to Foster the Growth of the Market

- 4.2 Market Restraints

- 4.2.1 Rising Adoption of Electric Vehicles Deter Market Growth

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size in Value - USD)

- 5.1 By Technology

- 5.1.1 Centrifugal Supercharger

- 5.1.2 Roots Supercharger

- 5.1.3 Twin-Screw Supercharger

- 5.2 By Fuel Type

- 5.2.1 Gasoline

- 5.2.2 Diesel

- 5.3 By Power Source

- 5.3.1 Engine Driven

- 5.3.2 Electric Motor Driven

- 5.4 By Sales Channel

- 5.4.1 Original Equipment Manufacturer (OEM)

- 5.4.2 Aftermarket

- 5.5 By Vehicle Type

- 5.5.1 Passenger Cars

- 5.5.2 Commercial Vehicles

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Rest of North America

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Rest of South America

- 5.6.5 Middle East and Africa

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 Rest of Middle East and Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles*

- 6.2.1 Ferarri N.V.

- 6.2.2 Eaton Corporation PLC

- 6.2.3 Mitsubishi Heavy Industries Ltd.

- 6.2.4 Koenigsegg Automotive AB

- 6.2.5 Honeywell Inc.

- 6.2.6 IHI Corporation

- 6.2.7 Vortech Engineering

- 6.2.8 Federal-Mogul Corporation

- 6.2.9 A&A Corvette

- 6.2.10 Rotrex A/S

- 6.2.11 Aeristech

- 6.2.12 Daimler AG

- 6.2.13 Ford Motor Company

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Rapid Enhancement in Diesel Supercharger Technology Fuels the Market Demand