|

시장보고서

상품코드

1849958

글리포세이트 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Glyphosate - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

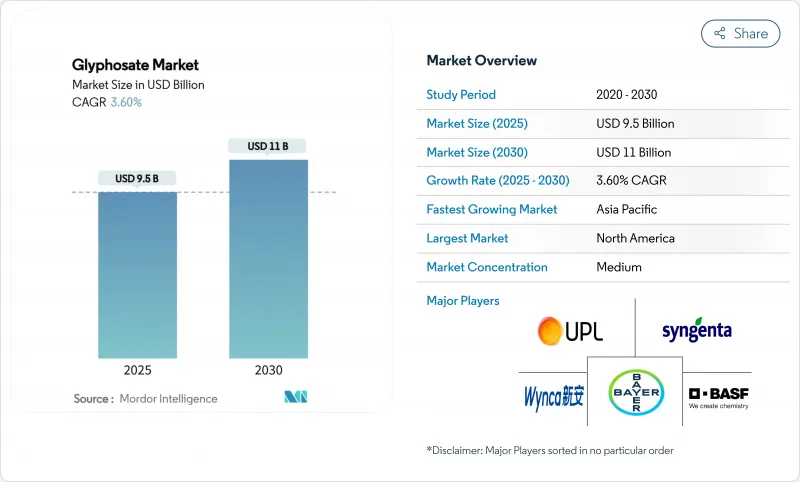

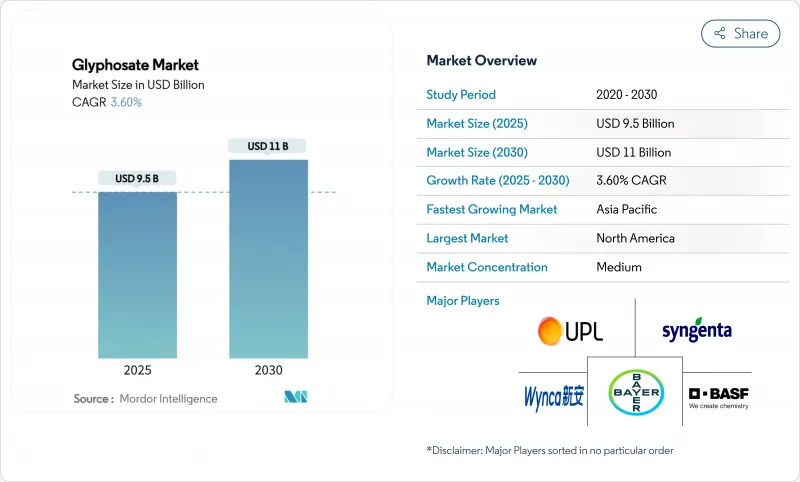

세계의 글리포세이트 시장은 2025년에 95억 달러에 이를 것으로 예측되며, 2030년에 CAGR은 3.6%를 나타낼 것으로 예측되며, 110억 달러로 성장할 전망입니다.

글리포세이트의 수요가 안정적인 것은 보전경운, 대규모 줄경작 시스템, 탄소 배출권 연계 무경운 프로그램에서 확고한 위치를 차지하고 있기 때문입니다. 북미의 제초제 내성 작물 조기 도입이 꾸준한 사용량을 뒷받침하는 반면, 아시아태평양 지역의 급속한 기계화와 바이오기술 재배 면적 증가는 물량 증가를 가속화하고 있습니다. 글로벌 수출의 80% 이상을 공급하는 중국 공장들이 환경 규제를 충족하기 위해 생산량을 줄이고 있으며, 바이엘은 소송 비용 속에서 생산 중단 가능성을 경고함에 따라 공급 기반은 여전히 타이트한 상태입니다. 생산 능력 통합으로 극심한 변동성이 제한되면서 가격 가시성이 개선되어 재배자들에게 명확한 비용 예측을 제공하고 규제 역풍에도 불구하고 꾸준한 채택을 뒷받침하고 있습니다. 경쟁 역학도 글리포세이트 시장을 형성합니다. 중국 기술 등급 생산업체들이 글로벌 수출량의 80% 이상을 장악하고 있는 반면, 바이엘은 여전히 가장 가시적인 브랜드 제형사입니다.

세계의 글리포세이트 시장 동향 및 인사이트

유전자 변형 제초제 내성 작물의 상용화

2024년 중국의 글리포세이트 내성 종자 특성 승인으로 100만 무 이상의 농지가 바이오기술 품종에 개방되었으며, 이는 미국과 브라질에서 오랫동안 이어져 온 채택 추세를 반영합니다. 글리포세이트를 포함한 5가지 제초제에 내성을 가진 바이엘의 바이코닉(Vyconic) 대두와 같은 새로운 복합 기술은 더 넓은 잡초 방제 기간을 약속합니다. 지속적인 형질 업그레이드는 제초제 프로그램의 효과를 유지시켜 대규모 경작 작물 전반에 걸친 장기적인 글리포세이트 수요를 확보합니다.

효과적인 잡초 방제 솔루션에 대한 수요 증가

전 세계적으로 530종의 제초제 내성 잡초 생물형이 확인되면서 신뢰할 수 있는 광범위 제초제 옵션에 대한 필요성이 시급해지고 있습니다. 글리포세이트의 작용 방식, 적용 유연성, 정밀 살포 플랫폼과의 호환성은 통합 잡초 관리에 필수적입니다. 많은 아프리카 시장에서 제네릭 제형의 가격 경쟁력 향상으로, 기존에 수작업 제초에 의존하던 소규모 농가의 도입이 촉진되고 있습니다.

규제 제한

유럽연합(EU)은 2023년 글리포세이트 사용을 10년간 재승인했으나 회원국에 더 엄격한 제한을 부과할 수 있는 재량권을 부여했습니다. 독일은 2024년 전면 금지에서 제한적 사용으로 전환했으며 법적 도전은 계속되고 있습니다. 뉴질랜드에서도 잔류 허용 기준 상향 제안에 3,100건의 공개 의견이 제출되는 등 유사한 불확실성이 대두되었습니다. 분산된 규정은 관리 복잡성을 가중시키고 준수 비용을 증가시키며, 명확한 승인 체계를 갖춘 국가로의 수요 이동을 유발할 수 있습니다.

부문 분석

곡물 및 곡류 부문은 2024년 글리포세이트 시장의 43.5%를 차지했으며, 이는 전 세계적으로 옥수수 및 밀 보존 시스템에서 대량 사용된 것을 반영합니다. 브라질의 지속적인 이모작과 중국의 수수 재배 면적 확대가 수요를 견인하고 있습니다. 콩류 및 유종 부문은 남미의 대두 재배 면적과 인도의 겨자 재배 증가로 2030년까지 연평균 5.6%의 성장률을 기록할 것으로 전망됩니다.

가변 속도 분무기 같은 기술 발전으로 투여량이 최적화되었으나, 총 처리 면적은 사용량을 안정적으로 유지합니다. 수작업 제초 비용이 높은 열대 지역에서는 면화와 사탕수수가 여전히 중요합니다. 원예 생산자들은 더 제한적인 방식을 적용하지만, 과수원과 포도원에서는 드립라인 주입 및 차폐 분무기가 기본 사용량을 유지합니다.

지역 분석

2024년 글리포세이트 시장에서 북미가 차지하는 34%의 점유율은 광범위한 무경운 콩 및 옥수수 재배 시스템에서 비롯됩니다. 이 지역 재배자의 80% 이상이 제초제 소각 및 작물 재배 중 살포에 의존하고 있습니다. 캐나다는 대초원 밀과 카놀라 재배에서도 유사한 관행을 보이며, 멕시코의 기계화 옥수수 농업 전환은 꾸준한 수요 증가를 가져옵니다. 소송은 주요 불안정 요인으로 남아 있으며, 바이엘이 철수할 경우 진행 중인 소송이 국내 공급을 위협할 수 있습니다. 조지아 주 및 기타 관할 구역에서 시행된 주 차원의 책임 면제 조치는 지속적인 생산을 보호하기 위한 것입니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR)은 5.86%에서 가장 빠른 성장을 이룰 것으로 예측됩니다. 중국의 농약 생산량은 24만-25만톤 정도로 안정되어 있지만, 글리포세이트는 여전히 톱 10의 유효 성분입니다. 인도의 농약 밸류체인이 확대되고 있으며, 농부가 저비용 잡초 방제를 채택함에 따라 글리포세이트 제네릭의 수량이 증가하고 있습니다. 인도네시아, 베트남, 태국에서는 이모작을 지원하기 위한 프리플랜트 번다운의 채택이 확대되고 있습니다. 호주의 경작 면적이 넓은 곡물 농장은 성숙하면서도 안정적인 수요를 유지하고 있으며, 살포를 미세 조정하는 정밀 유도 시스템에 의해 강화되고 있습니다.

남미는 전체 소비량에서 2위를 차지하며, 2025년 브라질의 3억 2,230만 톤 곡물 수확량이 높은 제초제 사용량을 주도하고 있습니다. 무경운 재배 면적이 3,500만 헥타르를 넘어서면서, 파종 전 잡초 방제를 위한 글리포세이트 사용이 필수적입니다. 아르헨티나의 통화 문제로 가격 민감도는 높아졌으나 재배 면적 의존도는 줄지 않았습니다. 신젠타의 파울리니아 6,500만 달러 시설과 같은 새로운 지역 기술 허브는 고습도 환경에서도 효능을 유지하는 열대 기후용 제형 개발에 집중하며 장기 성장을 뒷받침합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 유전자 변형 제초제 내성 작물의 상용화

- 효과적인 잡초 방제 솔루션 수요 증가

- 농지 확대와 농업 집약화

- 유전자 편집 작물에서 글리포세이트 내성 형질 통합

- 재생형 무경운 탄소 배출권 프로그램 사용 촉진

- 생산 능력 통합에 의해 장기적인 가격 안정

- 시장 성장 억제요인

- 규제상의 제한

- 유기농 및 생물학적 제초제로의 전환

- 브랜드 공급업체 시장 이탈 위험

- 주요 작물 재배 지역에서 가속화된 잡초 내성

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 작물 유형별

- 곡물 및 곡류

- 콩류 및 유지종자

- 과일 및 채소

- 상업 작물

- 기타 작물

- GMO 채택에 의한

- 유전자 변형 작물

- 비유전자 재조합 작물

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 기타 북미

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 독일

- 프랑스

- 이탈리아

- 스페인

- 영국

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 기타 아시아태평양

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Bayer AG

- Zhejiang Xinan(Wynca)

- Syngenta AG

- BASF SE

- UPL Ltd

- Corteva, Inc.

- FMC Corporation

- Nufarm Ltd

- Zhejiang Jiangshan Agrochemical(Jiangshan Chemical Co.)

- Jiangsu Yangnong Chemical(Sinochem Holdings)

- Albaugh LLC(Albaugh Group)

- Bharat Rasayan

- Jiangsu Good-Harvest(Good Harvest Weien Co.)

- King Quenson Industry(King Quenson Group)

제7장 시장 기회와 장래의 전망

HBR 25.11.10The global glyphosate market stands at USD 9.5 billion in 2025 and is forecast to reach USD 11 billion by 2030, advancing at a 3.6% CAGR.

Stable demand reflects glyphosate's entrenched role in conservation tillage, large-scale row-crop systems, and carbon-credit-linked no-till programs. North America's early adoption of herbicide-tolerant crops underpins consistent usage, while Asia-Pacific's rapid mechanization and rise in biotech acreage accelerate volume growth. Supply fundamentals remain tight because Chinese plants that supply more than 80% of global exports are curbing output to meet environmental rules, and Bayer has warned of a possible production exit amid litigation costs. Price visibility has improved as capacity consolidation limits extreme volatility, giving growers clearer cost forecasts and supporting steady adoption despite regulatory headwinds. Competitive dynamics also shape the glyphosate market: Chinese technical-grade producers control more than 80% of global export volume, while Bayer remains the most visible branded formulator.

Global Glyphosate Market Trends and Insights

Commercialization of GM Herbicide-Tolerant Crops

China's 2024 approval of glyphosate-tolerant seed traits opened more than 1 million mu to biotech varieties, echoing long-running adoption in the United States and Brazil. New stacked technologies, such as Bayer's Vyconic soybeans, tolerant to five herbicides, including glyphosate, promise broader weed-control windows. Continuous trait upgrades ensure herbicide programs remain effective, anchoring long-term glyphosate demand across large acreage crops.

Rising Demand for Effective Weed Control Solutions

Farmers face 530 confirmed herbicide-resistant weed biotypes worldwide, increasing the urgency for reliable broad-spectrum options. Glyphosate's mode of action, application flexibility, and compatibility with precision spraying platforms make it integral to integrated weed management. In many African markets, generic formulations have improved affordability, driving uptake among smallholders who previously relied on manual weeding.

Regulatory Restrictions

The European Union renewed glyphosate for 10 years in 2023 but gave member states leeway to impose stricter limits. Germany moved from an outright ban to restricted use in 2024, and legal challenges continue. Similar uncertainties have surfaced in New Zealand, where proposals to raise residue limits prompted 3,100 public submissions. Fragmented rules complicate stewardship, raise compliance costs, and may shift demand toward countries with clearer approval frameworks.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Agricultural Land and Intensified Farming

- Integration of Glyphosate-Tolerant Traits in Gene-Edited Crops

- Shift Toward Organic and Bio-Herbicides

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Grains and cereals generated 43.5% of the glyphosate market in 2024, reflecting heavy use in corn and wheat conservation systems worldwide. Continued double-cropping in Brazil and expanded sorghum acreage in China anchor demand. The pulses and oilseeds segment is forecast to post a 5.6% CAGR through 2030 as South American soybean hectares and Indian mustard cultivation rise.

Technology advances such as variable-rate sprayers optimize doses, yet total treated hectares keep volumes steady. Cotton and sugarcane remain important in tropical zones where manual weeding costs are high. Although horticultural producers apply more restrictive regimes, dripline injection, and shielded sprayers maintain a baseline of usage in orchards and vineyards.

The Glyphosate Market is Segmented by Crop Type (Grains and Cereals, Commercial Crops, and More), by GMO Adoption (GM Crops and Non-GM Crops), and by Geography (Asia-Pacific, North America, South America, Europe, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America's 34% share of the glyphosate market in 2024 stems from extensive no-till soy and corn systems, where over 80% of growers depend on herbicides for burndown and in-crop applications. Canada mirrors these practices across prairie wheat and canola, while Mexico's transition to mechanized maize farming introduces steady incremental demand. Litigation remains the main destabilizer, with pending cases threatening domestic supply if Bayer exits. State-level liability shields enacted in Georgia and other jurisdictions aim to safeguard continued manufacture.

Asia-Pacific is projected to deliver the fastest regional growth at a 5.86% CAGR by 2030. China's pesticide volumes have stabilized at around 240,000-250,000 tons, yet glyphosate remains a top-10 active ingredient. India's agrochemical value chain is scaling, and generic glyphosate volumes rise as farmers adopt low-cost weed control. Indonesia, Vietnam, and Thailand show growing adoption of pre-plant burndown to support double-cropping. Australia's broadacre cereal farms maintain mature but steady demand, reinforced by precision guidance systems that fine-tune application.

South America ranks second in overall consumption, anchored by Brazil's 322.3 million-ton grain harvest in 2025, which drives high herbicide intensity. No-till covers more than 35 million hectares, making glyphosate indispensable for grass weed control before planting. Argentina's currency challenges add price sensitivity but do not diminish acreage reliance. New regional tech hubs, such as Syngenta's USD 65 million facility in Paulinia, focus on tropical-climate formulations that preserve efficacy under high humidity, supporting long-term growth.

- Bayer AG

- Zhejiang Xinan (Wynca)

- Syngenta AG

- BASF SE

- UPL Ltd

- Corteva, Inc.

- FMC Corporation

- Nufarm Ltd

- Zhejiang Jiangshan Agrochemical (Jiangshan Chemical Co.)

- Jiangsu Yangnong Chemical (Sinochem Holdings)

- Albaugh LLC (Albaugh Group)

- Bharat Rasayan

- Jiangsu Good-Harvest (Good Harvest Weien Co.)

- King Quenson Industry (King Quenson Group)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Commercialization of GM herbicide-tolerant crops

- 4.2.2 Rising demand for effective weed control solutions

- 4.2.3 Expansion of agricultural land and intensified farming

- 4.2.4 Integration of glyphosate-tolerant traits in gene-edited crops

- 4.2.5 Regenerative no-till carbon-credit programmes boost usage

- 4.2.6 Capacity consolidation stabilises long-term prices

- 4.3 Market Restraints

- 4.3.1 Regulatory restrictions

- 4.3.2 Shift toward organic and bio-herbicides

- 4.3.3 Litigation-driven exit risk of branded suppliers

- 4.3.4 Accelerating weed resistance in major crop belts

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 By Crop Type

- 5.1.1 Grains and Cereals

- 5.1.2 Pulses and Oilseeds

- 5.1.3 Fruits and Vegetables

- 5.1.4 Commercial Crops

- 5.1.5 Other Crops

- 5.2 By GMO Adoption

- 5.2.1 GM Crops

- 5.2.2 Non-GM Crops

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.1.4 Rest of North America

- 5.3.2 South America

- 5.3.2.1 Brazil

- 5.3.2.2 Argentina

- 5.3.2.3 Rest of South America

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 France

- 5.3.3.3 Italy

- 5.3.3.4 Spain

- 5.3.3.5 United Kingdom

- 5.3.3.6 Russia

- 5.3.3.7 Rest of Europe

- 5.3.4 Asia-Pacific

- 5.3.4.1 China

- 5.3.4.2 India

- 5.3.4.3 Japan

- 5.3.4.4 Australia

- 5.3.4.5 Rest of Asia-Pacific

- 5.3.5 Middle East

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 UAE

- 5.3.5.3 Turkey

- 5.3.5.4 Rest of Middle East

- 5.3.6 Africa

- 5.3.6.1 South Africa

- 5.3.6.2 Rest of Africa

- 5.3.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Bayer AG

- 6.4.2 Zhejiang Xinan (Wynca)

- 6.4.3 Syngenta AG

- 6.4.4 BASF SE

- 6.4.5 UPL Ltd

- 6.4.6 Corteva, Inc.

- 6.4.7 FMC Corporation

- 6.4.8 Nufarm Ltd

- 6.4.9 Zhejiang Jiangshan Agrochemical (Jiangshan Chemical Co.)

- 6.4.10 Jiangsu Yangnong Chemical (Sinochem Holdings)

- 6.4.11 Albaugh LLC (Albaugh Group)

- 6.4.12 Bharat Rasayan

- 6.4.13 Jiangsu Good-Harvest (Good Harvest Weien Co.)

- 6.4.14 King Quenson Industry (King Quenson Group)