|

시장보고서

상품코드

1444055

항공용 C4ISR : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2024-2029년)Air-based C4ISR - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

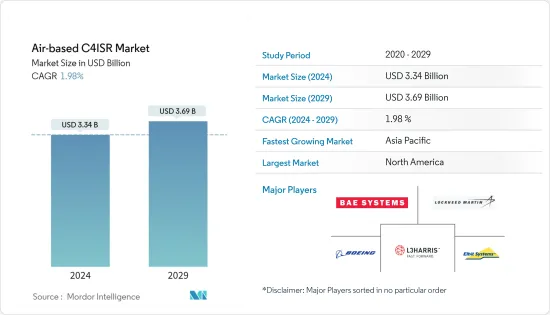

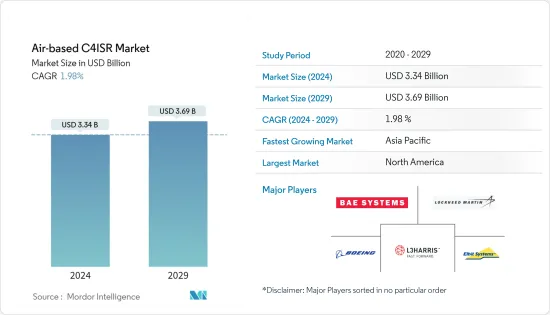

항공용 C4ISR 시장 규모는 2024년 33억 4,000만 달러로 추정되며, 2029년까지 36억 9,000만 달러에 달할 것으로 예상되며, 예측 기간(2024-2029년) 동안 1.98%의 CAGR로 성장할 것으로 예상됩니다.

COVID-19가 세계 경제에 심각한 타격을 입혔음에도 불구하고, 2020년과 2021년에 계속 증가한 세계 군사비 지출에는 영향을 미치지 않았습니다. 2021년 세계 군사비 지출은 총 2조 1,130억 달러에 달할 것으로 예상되며 계속 증가하고 있습니다. 이러한 막대한 지출은 COVID-19 팬데믹이 국방 시스템 개발 및 조달에 미치는 영향이 미미하다는 것을 보여줍니다. 군비 지출 증가는 내년 항공용 C4ISR 시장을 견인할 것으로 예상됩니다.

전 세계적으로 정치적, 지리적 긴장이 고조되면서 항공용 C4ISR 시스템에 대한 수요가 증가하고 있습니다. 신호 인식 및 생존성 강화를 위한 무인항공기(UAV), 전자 지원/대응 조치(ESM/ECM), 공수용 C2, 첨단 전술 항공 정찰 시스템, 공중 감시 및 통제 시스템(AWACS)에 대한 수요가 빠르게 증가하면서 항공용 C4ISR 시장의 성장을 촉진하고 있습니다.

항공용 C4ISR 시스템 수요의 대부분은 현대화 계획과 각국의 위협 인식 증가 등의 요인으로 인해 예측 기간 동안 아시아태평양에서 발생할 것으로 예상됩니다.

항공용 C4ISR 시장 동향

세계 국방비 증가

국제 전략 정세의 중대한 변화로 인해 국제 안보 시스템의 구성은 패권주의, 일국주의, 강대국 정치의 증가로 인해 훼손되어 현재 진행 중인 여러 가지 세계 분쟁을 유발하고 있습니다.

영토권의 불확실성, 정치적 긴장, 군사 강대국 간의 보편적 우위 추구는 지정학적 시나리오를 방해하는 주요 원인 중 하나입니다. 이와 관련하여 정부의 가장 일반적인 반응은 각국의 안보를 개선하기 위해 군사 지출을 늘리는 것입니다.

COVID-19의 경제적 영향에도 불구하고 2020년과 2021년에도 세계 국방비 지출은 계속 증가했으며, 2021년 최대 군사비 지출 국가는 미국, 중국, 인도, 영국, 러시아로, 이들 국가를 합치면 세계 군사비의 62%를 차지했습니다.

각국에 대한 위협이 증가함에 따라 군대의 C4ISR 능력을 강화하는 것이 모든 국가에 중요해지고 있습니다. 이와 관련하여 여러 국가의 C4ISR 능력을 효과적으로 향상시키기 위한 여러 군사 계획이 현재 진행 중입니다. 이러한 프로그램을 촉진하기 위해 각국은 토착 개발 또는 세계 공급업체로부터의 조달을 통해 이러한 능력을 강화하기 위해 막대한 투자를하고 있습니다. 이러한 투자는 국방비 지출 증가에 의해 더욱 촉진될 것입니다.

최근 이 지역 국가들은 C4ISR 시스템을 통합한 차세대 플랫폼과 장비를 주문하고 있으며, 이러한 개발 프로그램도 몇 가지 진행 중입니다. 이러한 프로그램들은 예측 기간 동안 실행될 예정입니다.

이러한 플랫폼과 장비의 개발 및 조달에는 막대한 시스템 비용이 소요되기 때문에 각국의 막대한 국방비가 필요합니다. 따라서 국방비 지출의 증가는 향후 몇 년 동안 시장 성장을 촉진할 것으로 예상됩니다.

아시아태평양, 예측 기간 동안 가장 높은 성장률 기록

아시아태평양은 중국, 인도, 일본 등 군사비 지출이 높은 국가들의 존재로 인해 다른 지역에 비해 가장 높은 성장률을 보일 것으로 예상됩니다. 여러 국가의 육상 및 해상 국경에 지정학적 긴장이 존재하기 때문에 C4ISR 조달은 지역 전체에서 증가할 수 있습니다. 아시아태평양 전체의 강제적인 현대화 노력으로 인해 C4ISR 시스템 조달도 증가할 것으로 예상됩니다. 중국과 인도는 군대 역량 강화에 큰 진전을 보이고 있으며, 세계 국방비 지출 상위권 국가에 속해 있습니다.

기술과 전자전의 발전으로 전자전에 효과적으로 대응할 수 있는 기술에 대한 수요가 증가하고 있습니다. 이에 발맞춰 세계 기술을 따라잡기 위해 군대에서도 새로운 개발이 이루어지고 있습니다. 예를 들어, 2022년 3월 인도 국방부는 인도 공군 전투기에 첨단 전자전 스위트를 공급하기 위해 BEL과 파트너십을 체결했습니다.

한국은 군사적 목적의 통신 기술을 향상시키기 위한 노력의 일환으로 기존 기술을 업그레이드하는 데 투자해 왔습니다. 그 결과, 군용 통신 수요를 충족시키기 위한 새로운 계약과 파트너십이 관찰되고 있습니다. 예를 들어,

한화시스템과 LIG넥스원은 2021년 9월, 한국 국방조달계획국(DAPA)으로부터 국내 최초 군 전용 통신위성인 아나시스-II 관련 계약을 체결했다고 밝혔습니다. 한화시스템은 2020년 7월 우주로 발사된 아나시스-II 위성 시스템과 관련해 2024년까지 네트워크 제어 시스템 구축과 휴대용 지상 단말기 제조를 위한 3,600억 원(3억 7천만 달러) 규모의 계약을 체결했다고 밝혔습니다.

이러한 발전으로 인해 예측 기간 동안 시장은 상당한 성장률을 보일 것으로 예상됩니다.

항공용 C4ISR 산업 개요

C4ISR 시스템의 기술 발전과 다기능 시스템에 대한 수요로 인해 제조업체는 비용 효율적인 솔루션의 연구 개발에 대한 투자를 촉진하고 있습니다. 예를 들어, Hindustan Aeronautics Limited(HAL)는 회전익 UAV 프로토타입을 발표했으며, 2021년 5월 Aeronautics는 장거리 해상 순찰 임무를 위한 소형 전술 드론 Orbiter 4를 발표했습니다. 이 UAS는 24시간 이상 지속될 수 있으며, 여러 개의 페이로드를 동시에 운반하고 운용할 수 있습니다. 활주로에 의존하지 않고(모든 유형의 선박에서 이착륙 가능), 고급 영상 처리 기능, 자동 이륙 및 회수 시스템, GPS/데이터 링크 유무에 관계없이 항해할 수 있는 기능을 갖추고 있습니다. 지역 기업의 기술 및 제품 포트폴리오의 이러한 발전은 가까운 장래에 전략적 확장 계획에 도움이 될 것으로 예상됩니다.

기타 혜택

- 엑셀 형식의 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

목차

제1장 서론

- 조사 가정

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 시장 개요

- 시장 성장 촉진요인

- 시장 성장 억제요인

- Porter's Five Forces 분석

- 신규 참여업체의 위협

- 구매자의 교섭력

- 공급 기업의 교섭력

- 대체 제품의 위협

- 경쟁 정도

제5장 시장 세분화

- 유형

- C4시스템

- ISR

- 전자전

- 지역

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 프랑스

- 독일

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트

- 남아프리카공화국

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 상황

- 벤더의 시장 점유율

- 기업 개요

- The Boeing Company

- General Dynamics Corporation

- Elbit Systems Ltd

- Lockheed Martin Corporation

- Northrop Grumman Corporation

- BAE Systems PLC

- CACI International Inc.

- Kratos Defense &Security Solutions Inc.

- Rheinmetall Defense

- L3Harris Technologies Inc.

- Denel SOC Ltd

- ThalesRaytheonSystems

제7장 시장 기회와 향후 동향

ksm 24.03.14The Air-based C4ISR Market size is estimated at USD 3.34 billion in 2024, and is expected to reach USD 3.69 billion by 2029, growing at a CAGR of 1.98% during the forecast period (2024-2029).

Despite the COVID-19 pandemic hitting the global economy severely, the impact of the same is not felt on the global military expenditure, which continued to increase in 2020 and 2021. The global military expenditure reached a total of USD 2.113 trillion in 2021, increasing by about 0.7% compared to 2020. Such high expenditure indicates the negligible impact the COVID-19 pandemic had on defense systems development and procurements. The growth in military spending is expected to drive the air-based C4ISR market in the coming year.

The increasing political and geographical tensions around the world are propelling the demand for airborne C4ISR systems. The rapid growth in demand for unmanned aerial vehicles (UAVs), electronic support/countermeasures (ESM/ECM), airborne C2, advanced tactical air reconnaissance system, and airborne warning and control systems (AWACS) to enhance signal awareness and survivability is driving the growth of the air-based C4ISR market.

A majority of the demand for air-based C4ISR systems is anticipated to be generated in the Asia-Pacific region during the forecast period, due to factors, like modernization plans and an increase in the threat perception of countries.

Air-based C4ISR Market Trends

Growth in the Global Defense Expenditure

Owing to profound changes in the international strategic landscape, the configuration of international security systems has been undermined by the growing hegemonism, unilateralism, and power politics, which fueled several ongoing global conflicts.

Uncertainties in territorial rights, political tensions, and the quest for universal dominance among the military powerhouses are among the major causes disturbing the geopolitical scenario. In this regard, the most common reaction of the governments is to increase their military spending, to improve security in their respective countries.

Despite the economic impact of the COVID-19 pandemic, global defense expenditure continued to increase in 2020 and 2021. According to SIPRI, the global military expenditure in 2021 rose to USD 2113 billion, an increase of 0.7% in from 2020. billion. Global spending in 2021 was 12% higher than in 2012. The five largest military spenders in 2021 were the United States, China, India, the United Kingdom, and Russia, which together accounted for 62% of world military spending.

As the threats for the countries become higher, enhancing the militaries' C4ISR capabilities becomes important for every country. In this regard, several military programs are currently underway to effectively upgrade the C4ISR capabilities of various countries. To facilitate these programs, countries are investing huge amounts into the enhancement of such capabilities, either through indigenous development or through procurement from global vendors. These investments are further driven by the growth in defense expenditures.

In recent years, countries in these regions have placed orders for newer generation platforms and equipment that incorporate C4ISR systems whereas several such development programs are also underway. These programs are expected to run during the forecast period.

The development and procurement of such platforms and equipment demands huge defense spending from the countries, as the cost of the systems is immense. Thus, the growth in defense spending is expected to drive the growth of the market in the coming years.

The Asia-Pacific region to Register Highest Growth During the Forecast Period

The Asia-Pacific region is expected to witness the highest growth rate as compared to the other regions, due to the presence of high military spending countries, such as China, India, and Japan. With the presence of geopolitical tensions in the land and sea borders in multiple countries, the procurement of C4ISR is likely to increase across the region. Forced modernization efforts across the Asia-Pacific region are also expected to increase the procurement of C4ISR systems. China and India are taking huge strides toward strengthening the capabilities of their armed forces and are among the top five defense-spending countries in the world.

The increasing technology and electronic warfare have been driving the demand for technologies to effectively tackle electronic warfare. In line with this, new developments have been occurring in the army, to keep up with global technology. For instance, In March 2022, the Defence Ministry of India signed a partnership with BEL to supply an Advanced Electronic Warfare suite for the Indian Air Force fighter jets. The contract was signed between the Ministry of Defense and Bharat Electronics Limited (BEL), with an estimated value of INR 1993 Crore.

In efforts to increase communications technology for military purposes, south Korea has been investing in upgrading its existing technologies. As a result, new contracts and partnerships have been observed, to cater to the demand for military-grade communications. For instance,

In September 2021, Hanwha Systems and LIG Nex1 have announced that they have secured contracts from South Korea's Defense Acquisition Program Administration (DAPA) linked to ANASIS-II, the country's first dedicated military communications satellite. Hanwha Systems stated that they was awarded a KRW360 billion (USD307 million) contract to both establish a network control system and manufacture portable ground terminals by 2024 linked to the ANASIS-II satellite system, which launched into space in July 2020.

Such developments are expected to drive the market towards significant growth rates during the forecast period.

Air-based C4ISR Industry Overview

The prominent players in the air-based C4ISR market are Lockheed Martin Corporation, the Boeing Company, BAE Systems PLC, L3Harris Technologies Inc., Lockheed Martin Corporation, and Elbit Systems Ltd. However, there are many manufacturers that provide C4ISR solutions for air, land, and sea platforms. The regional manufacturers are gradually growing their presence in the market due to the support of their governments and partnerships with global players. Technological advancement in C4ISR systems and the demand for multi-functional systems are propelling the investments of manufacturers in the research and development of cost-effective solutions. For instance, a prototype of a rotary-wing UAV was unveiled by Hindustan Aeronautics Limited (HAL), In May 2021, Aeronautics introduced its Orbiter 4 small tactical drone for long-range maritime patrol missions. The UAS has an endurance of more than 24 hours and can carry and operate multiple payloads simultaneously. It is airstrip independent (can take off and land on any type of vessel) and features advanced image processing capabilities, an automatic takeoff and recovery system, and the ability to navigate with or without GPS/data link. Such advancements in technology and product portfolio of the regional companies are anticipated to help the strategic expansion plans in the near future.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 C4 Systems

- 5.1.2 ISR

- 5.1.3 Electronic Warfare

- 5.2 Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.2 Europe

- 5.2.2.1 United Kingdom

- 5.2.2.2 France

- 5.2.2.3 Germany

- 5.2.2.4 Rest of Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 China

- 5.2.3.2 India

- 5.2.3.3 Japan

- 5.2.3.4 South Korea

- 5.2.3.5 Rest of Asia-Pacific

- 5.2.4 Latin America

- 5.2.4.1 Brazil

- 5.2.4.2 Rest of Latin America

- 5.2.5 Middle-East and Africa

- 5.2.5.1 Saudi Arabia

- 5.2.5.2 United Arab Emirates

- 5.2.5.3 South Africa

- 5.2.5.4 Rest of Middle-East and Africa

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share**

- 6.2 Company Profiles*

- 6.2.1 The Boeing Company

- 6.2.2 General Dynamics Corporation

- 6.2.3 Elbit Systems Ltd

- 6.2.4 Lockheed Martin Corporation

- 6.2.5 Northrop Grumman Corporation

- 6.2.6 BAE Systems PLC

- 6.2.7 CACI International Inc.

- 6.2.8 Kratos Defense & Security Solutions Inc.

- 6.2.9 Rheinmetall Defense

- 6.2.10 L3Harris Technologies Inc.

- 6.2.11 Denel SOC Ltd

- 6.2.12 ThalesRaytheonSystems