|

시장보고서

상품코드

1851406

골암 치료 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Bone Cancer Treatment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

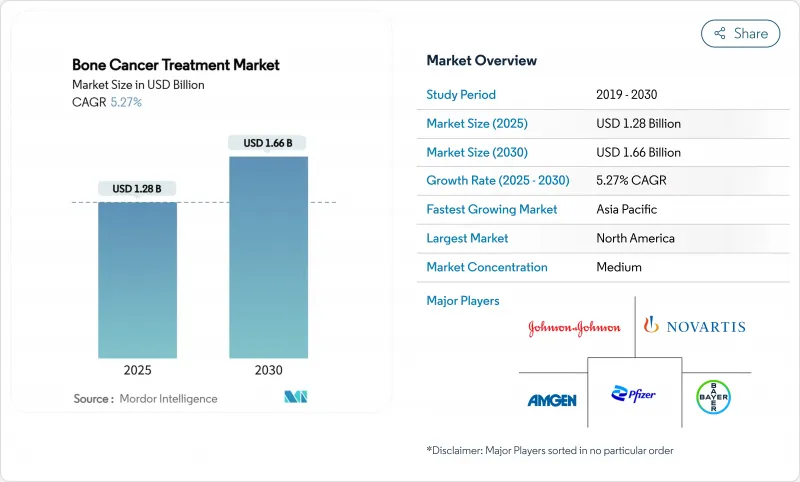

골암 치료 시장 규모는 2025년에 12억 8,000만 달러, 예측 기간(2025-2030년)의 CAGR은 5.27%를 나타내고, 2030년에는 16억 6,000만 달러에 달할 것으로 예측됩니다.

규제 당국의 획기적인 승인, 3D 프린팅 임플란트의 채택 확대, 표적 생물 제제의 꾸준한 보급을 배경으로 수요가 확대되고 있습니다. 시장의 성장은 인공지능을 활용한 영상 진단에 의한 조기 진단, 희귀의약품에 대한 상환의 확대, 사지 구제 처치에 의한 임상 결과의 개선에 의해 더욱 지원되고 있습니다. 북미는 연구개발과 상환에 있어서 구조적인 우위를 유지하고 있지만 아시아태평양은 질병인식 프로그램의 규모가 확대됨에 따라 급속히 생산능력을 증강하고 있습니다. 틈새 생명 공학 기업은 신속한 승인을 얻었으며 기존 기업은 정밀의료를 위해 포트폴리오를 재구성해야하며 경쟁이 치열 해지고 있습니다. 낮은 자원 환경에서 높은 치료 비용과 제한된 의사의 능력은 여전히 주요 대세입니다.

세계 골암 치료 시장 동향과 통찰

원발성 골육종의 세계적 발생률 증가

골육종은 소아와 청소년에게 가장 많은 원발성 골악성 종양으로 지속되고 있으며, 역학적 데이터는 주요 경제 지역에서 유잉 육종 사례가 지속적으로 증가하는 것으로 확인되었습니다. 중국의 국가적 부담에 관한 연구에서는 이환율, 유병률, 장애조정 생존연수 증가가 보고되고 있으며, 2036년까지 계속 증가할 것이라는 예측도 있습니다. 환자 수가 증가함에 따라 각국 정부는 정형외과 종양과의 진료 능력을 확대하고 소아에 특화된 치료법에 대한 벤처 기업의 자금을 모으고 있습니다. 전국적인 MRI 검진의 시험적 실시 등 진단의 개선에 의해 조기의 병태가 파악되어 사지 온존 수술 수요가 높아지고 있습니다.

표적 생물 제제 승인 및 파이프라인 기세

규제 당국은 2024-2025년에 승인 페이스를 가속시켰습니다. 미국 식품의약국은 활막육종에 대한 최초의 유전자 치료인 afamitresgene autoleucel을 승인했습니다. 2025년 2월, 동국은 힘줄막 거세포종에 대한 빔세르티닙도 승인하였고, 주요 시험인 MOTION 시험에서 위약에 대해 40%의 객관적 주효를 나타냈습니다. 재발 골육종에 대한 GSK5764227을 포함한 다른 프로그램에 대한 획기적인 치료제 지정은 표적 접근법을 검증하고 개발주기를 단축하는 것입니다. 이러한 이정표를 종합하면 임상 프로토콜이 확대되고 성숙한 시장에서 지불자 채택이 촉진됩니다.

전이성 및 난치성 종양에 대한 제한된 치료 옵션

전이성 골육종의 5년 생존율은 30% 미만으로 현재 요법이 부적절하다는 것이 밝혀졌습니다. 면역억제적인 골 미세환경은 체크포인트 억제제의 효능을 둔화시키는 반면, 용량 제한적인 독성은 강화 화학요법에 의한 이익을 제한합니다. HER2를 표적으로 한 T 세포와 같은 입양 세포 이식에 대한 연구는 초기 유망성을 나타내지 만 소규모 코호트에 머물러 있습니다. 인도나 브라질의 3차 의료기관에서 얻은 실제 데이터에 따르면 임상시험에 참여할 수 있는 난치성 사례는 전체의 15% 미만이며, 이는 예후 불량의 원인이 되고 있습니다.

부문 분석

원발성 악성 종양은 2024년 골암 치료 시장 점유율의 76.97%를 차지했지만, 이는 정착한 임상 경로와 소아 및 사춘기 집단에서 높은 이환율을 반영하고 있습니다. 골육종은 여전히 전형적인 진단 이름이며 첫 번째 선택 MAP(메토트렉세이트, 독소루비신, 시스플라틴) 프로토콜을 지원합니다. RUNX2를 저해하는 저분자 화합물로부터 전임상 모델에서 폐 전이를 억제하는 GD2 지향성 항체 약물 복합체에 이 부문의 규모는 연구 개발에 불균형할 정도의 주목을 받고 있습니다. 유잉육종은 가장 급성장하는 틈새 영역으로 자리매김하고 있으며, 입양유전자 치료가 실용화됨에 따라 2030년까지의 CAGR은 9.27%로 예측되고 있습니다. 한편, 연골육종의 성장을 지지하고 있는 것은 PD-1/PD-L1 체크포인트 레지멘이 초기 단계의 임상시험에서 부분 주효를 나타냈다는 것입니다.

치료법의 혁신은 과거 생존 기간의 격차를 줄이고 있습니다. 영국에 본사를 둔 프로그램은 RUNX2 전사를 억제함으로써 마우스 골육종의 생존율을 50% 개선하는 데 성공하여 현재 인간 독성 시험에 들어가고 있습니다. 동시에 전이성 병변에 대한 방사성 의약품 접합체가 중국과 유럽의 규제 채널을 통과하면서 원발성 종양 이외에도 적응이 확산되고 있습니다. 이러한 파이프라인을 종합하면 각 조직형에 있어서의 골암 치료 시장 규모의 확대가 기대됩니다.

기존의 세포독성 요법은 2024년 골암 치료시장의 32.89%를 차지했고 대부분의 고악성도 육종에 대한 제1선택요법으로 계속되고 있습니다. 그러나 부작용프로파일과 생존기간의 정체로 인해 정밀한 접근으로 축발이 옮겨가고 있습니다. 세포 및 유전자 치료는 규제 당국의 전례가 추가 승인의 장애물을 낮추면서 CAGR 6.78%로 확대될 것으로 예측됩니다. B7-H3와 GD2를 표적으로 하는 CAR-T 구조물은 다시설 공동 제2상 시험 중이며, 동종 NK 세포 플랫폼은 면역억제성의 종양 환경과 싸우려고 하고 있습니다.

멀티키나제 제제를 포함한 표적 저분자 억제제는 컴패셔네이트 사용 등록에서 무증악 효과가 입증된 후 적응 외 사용이 증가하고 있습니다. 데노스맙은 골격 관련 사건의 예방에서 졸레드론산보다 우수하여 RANKL 차단 요법을 표준 보조 요법으로 확고하게 만들었습니다. 동시에, 3D 프린터에 의한 임플란트 기술과 갈륨 첨가 생물활성 유리제 인서트가 국소 관리 전략을 재정의하여 사지 구제를 위한 도입에 대한 기대를 높이고 있습니다.

지역 분석

북미는 2024년 골암 치료 시장에서 45.76%의 점유율을 유지했고 미국의 희소질환용 의약품에 대한 조기 접근 틀과 3D 프린팅 임플란트에 대한 성숙한 상환에 힘쓰고 있습니다. 소아육종 컨소시엄에 대한 연방정부의 자금 지원으로 임상시험의 밀도가 높게 유지되고 AI를 활용한 영상진단의 보급으로 진단 지연이 해소되고 있습니다. 캐나다의 국민 모두 보험 제도는 생물학적 제제의 채택을 더욱 확대하고 환자 1인당 비용 상승을 상쇄합니다.

유럽에서는 2주 이내에 지정된 센터에 소개를 의무화하는 일관된 육종 치료 패스웨이가 확립되었습니다. 이 지역에서는 사지 구제의 문화가 확립되고 있으며, 유럽의약청(EEA)에 의한 10년간의 독점권이 기술 혁신을 뒷받침하고 있습니다. 하지만 회원국간에 상환 정책이 다르기 때문에 고비용의 세포 치료가 일률적으로 채택되는 것은 아닙니다. 독일은 첨가제 제조 도입으로 주도권을 잡고 이탈리아는 골육종의 유전체 스크리닝을 국가 수준에서 시험적으로 실시했습니다.

아시아태평양은 가장 빠르게 성장하는 지역으로 중국, 일본, 인도가 정형외과 종양학의 생산 능력을 확대함에 따라 CAGR 7.12%로 성장이 예상됩니다. 중국의 국가의약품감독관리국은 2025년 골전이에 대한 방사성핵종과 약제의 결합체를 승인하여 국내 기업을 지역의 리더로 자리매김하고 있습니다. 일본에서는 대량화학요법과 자가골수이식에 주력하여 생존기간의 연장을 계속하고 있습니다. 인도의 과제는 만기 발병과 전문의의 커버 범위의 좁음이지만, 현지에서 제조된 모듈식 인공 관절과 제2층의 도시에 의한 치료 프로그램에 의해 특정 시설에서는 무병 생존율이 61%까지 개선되고 있습니다.

라틴아메리카와 아프리카는 단편적인 보험 상환과 임상의의 부족으로 인해 지연을 겪고 있습니다. 그럼에도 불구하고 다국적 NGO는 연수 휄로우십을 늘리고 향후 10년 이내에 탁월한 지역 센터가 생길 것으로 예상되는 사지 구제 이니셔티브에 자금을 제공합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트·지원

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 원발성 골육종의 세계적 발생률 증가

- 표적 생물학적 제제의 승인과 파이프라인의 기세

- 정부와 NGO 주도의 육종계발 프로그램 확대

- 조기 발견을 가능하게 하는 기능적 영상 및 AI 진단의 발전

- 3D 프린팅, 환자 맞춤형 정형외과 임플란트로 사지 구제 채택 확대

- 희귀의약품 독점 및 세제 혜택으로 틈새 치료 R&D 가속화

- 시장 성장 억제요인

- 전이성 또는 난치성 골암에 대한 제한된 치료 옵션

- 신규 생물 제제와 세포 치료의 고비용이 접근을 제한한다

- 접근을 제한하는 새로운 생물학적 제제 및 세포 치료의 높은 비용

- 신흥 시장에서 정형외과 종양 전문의의 부족

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 뼈암 유형별

- 원발성 골암

- 골육종

- 연골육종

- 유잉 육종

- 기타 주요 유형

- 2차성(전이성) 골암

- 원발성 골암

- 치료 유형별

- 화학요법

- Anthracyclines

- 알킬화제

- 항대사물 및 기타

- 표적 치료

- RANKL 억제제

- 티로신 키나아제 억제제

- mTOR/MEK &신흥타겟

- 면역요법

- 면역관문억제제

- 세포 및 유전자 치료

- 방사선요법

- 수술과 사지 구제 처치

- 기타

- 화학요법

- 연령층별

- 소아

- 청소년 및 청년

- 성인

- 고령자

- 최종 사용자별

- 병원

- 암 센터 및 정형외과 전문 시설

- 학술기관 및 연구기관

- 외래수술센터(ASC)

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Amgen Inc.

- Bayer AG

- Novartis AG

- Johnson & Johnson(Janssen)

- Pfizer Inc.

- Takeda Pharmaceutical Company Ltd.

- Eli Lilly and Company

- Hikma Pharmaceuticals PLC

- Recordati SpA

- Spectrum Pharmaceuticals Inc.

- Debiopharm Group

- Atlanthera

- Adaptimmune Therapeutics plc

- Daiichi Sankyo Company Ltd.

- F. Hoffmann-La Roche Ltd.

- Ipsen SA

- OncoTherapy Science Inc.

- Legend Biotech

- Merck & Co., Inc.

- Gilead Sciences(Kite Pharma)

제7장 시장 기회와 장래의 전망

SHW 25.11.21The Bone Cancer Treatment Market size is estimated at USD 1.28 billion in 2025, and is expected to reach USD 1.66 billion by 2030, at a CAGR of 5.27% during the forecast period (2025-2030).

Demand is expanding on the back of breakthrough regulatory approvals, wider adoption of 3D-printed implants, and steady diffusion of targeted biologics. The market's growth is further sustained by earlier diagnosis through AI-enabled imaging, wider reimbursement for orphan drugs, and improved clinical outcomes delivered by limb-salvage procedures. North America holds structural advantages in R&D and reimbursement, while Asia-Pacific is adding capacity rapidly as disease-awareness programmes scale. Competition is intensifying as niche biotechnology firms win fast-track approvals, forcing incumbents to recalibrate portfolios toward precision-medicine assets. High treatment costs and limited physician capacity in low-resource settings remain the main countervailing forces.

Global Bone Cancer Treatment Market Trends and Insights

Increasing Global Incidence of Primary Bone Sarcomas

Osteosarcoma continues to be the most common primary bone malignancy among children and adolescents, and epidemiological data confirm a sustained rise in Ewing sarcoma cases in major economies. A national burden study in China reported higher incidence, prevalence and disability-adjusted life-years, with projections indicating continued growth to 2036. Larger patient pools are prompting governments to expand orthopaedic oncology capacity and are attracting venture funding for paediatric-focused therapies. Diagnostic improvements, such as nationwide MRI screening pilots, are capturing earlier-stage presentations and fuelling demand for limb-preserving procedures.

Approvals & Pipeline Momentum of Targeted Biologics

Regulatory agencies accelerated the pace of approvals in 2024-2025. The United States Food and Drug Administration cleared afamitresgene autoleucel, the first gene therapy for synovial sarcoma, after the product delivered a 43.2% overall response in heavily pre-treated patients. In February 2025 the agency also approved vimseltinib for tenosynovial giant cell tumour, with a 40% objective response versus placebo in the pivotal MOTION trial. Breakthrough therapy designations for additional programmes, including GSK5764227 in relapsed osteosarcoma, validate targeted approaches and shorten development cycles. Collectively, these milestones are expanding clinical protocols and hastening payor adoption across mature markets.

Limited Therapeutic Options for Metastatic or Refractory Tumours

Five-year survival drops below 30% for metastatic osteosarcoma, underscoring the inadequacy of current regimens. The immunosuppressive bone micro-environment blunts checkpoint inhibitor efficacy, while dose-limiting toxicities cap the gains from intensified chemotherapy. Investigational adoptive cell transfers, such as HER2-targeted T-cells, are showing early promise but remain confined to small cohorts. Real-world data from tertiary centres in India and Brazil illustrate that less than 15% of refractory cases gain access to clinical trials, perpetuating poor outcomes.

Other drivers and restraints analyzed in the detailed report include:

- Government & NGO-Led Sarcoma Awareness Programmes

- Advances in Functional Imaging & AI Diagnostics

- High Cost of Novel Biologics & Cell Therapies Limiting Access

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Primary malignancies accounted for 76.97% of bone cancer treatment market share in 2024, reflecting entrenched clinical pathways and high incidence among paediatric and adolescent populations. Osteosarcoma remains the prototypical diagnosis and anchors first-line MAP (methotrexate, doxorubicin, cisplatin) protocols. The segment's scale is drawing disproportionate R&D attention, from RUNX2-inhibiting small molecules to GD2-directed antibody-drug conjugates that cut pulmonary metastasis in preclinical models. Ewing sarcoma is positioned as the fastest-growing niche, registering a projected 9.27% CAGR to 2030 as adoptive gene therapies enter commercialisation. Meanwhile, chondrosarcoma growth is supported by PD-1/PD-L1 checkpoint regimens demonstrating partial responses in early-phase trials.

Therapeutic innovation is narrowing historical survival gaps. A UK-based programme achieved a 50% survival improvement in murine osteosarcoma by blocking RUNX2 transcription now entering human toxicology studies. At the same time, radiopharmaceutical conjugates for metastatic lesions are moving through Chinese and European regulatory channels, broadening indications beyond primary tumours. Collectively, these pipelines are expected to expand the bone cancer treatment market size across each histology subtype.

Conventional cytotoxic regimens accounted for 32.89% of the bone cancer treatment market in 2024 and remain first-line therapy for most high-grade sarcomas. However, adverse-event profiles and plateauing survival are catalysing a pivot toward precision approaches. Cell and gene therapies are forecast to expand at a 6.78% CAGR as regulatory precedents lower the bar for additional approvals. CAR-T constructs targeting B7-H3 and GD2 are in multi-centre phase II trials, while allogeneic NK-cell platforms seek to combat the immunosuppressive tumour milieu.

Targeted small-molecule inhibitors, including multi-kinase agents, are gaining off-label traction after demonstrating progression-free benefits in compassionate-use registries. Denosumab's head-to-head superiority over zoledronic acid in preventing skeletal-related events has cemented RANKL blockade as standard adjunct therapy. Concurrently, 3D-printed implant technology and gallium-doped bioactive glass inserts are redefining local control strategies, raising expectations for limb-salvage uptake.

The Bone Cancer Treatment Market Report Segments the Industry Into Bone Cancer Type (Primary Bone Cancer, Secondary (Metastatic) Bone Cancer), Therapy Type (Chemotherapy, Targeted Therapy, and More), Age Group (Pediatric, Adolescent & Young Adult, Adult, Geriatric), End User (Hospitals, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained a 45.76% hold on the bone cancer treatment market in 2024, propelled by the United States' early-access framework for orphan drugs and mature reimbursement for 3D-printed implants. Federal funding for paediatric sarcoma consortia keeps trial density high, and widespread adoption of AI-augmented imaging is eliminating diagnostic delays. Canada's universal coverage further broadens biologic uptake, offsetting higher per-patient costs.

Europe follows with cohesive sarcoma-care pathways that require referral to designated centres within two weeks. The region's established limb-salvage culture and the European Medicines Agency's ten-year exclusivity bolster innovation. Nevertheless, divergent reimbursement policies across member states temper uniform adoption of high-cost cell therapies. Germany retains leadership in additive-manufacturing deployments, while Italy is piloting national genomic screening for bone sarcomas.

Asia-Pacific is the fastest-growing bloc, forecast at a 7.12% CAGR as China, Japan and India expand orthopaedic oncology capacity. China's National Medical Products Administration cleared a radionuclide-drug conjugate for bone metastases in 2025, positioning domestic companies as regional leaders. Japan's focus on high-dose chemotherapy and autologous marrow rescue continues to yield incremental survival gains. India's challenge remains late presentation and limited specialist coverage, but locally fabricated modular prostheses and tier-two city treatment programmes are improving disease-free survival to 61% in selected centres.

Latin America and Africa lag behind due to fragmented reimbursement and clinician shortages. Nonetheless, multinational NGOs are increasing training fellowships and funding limb-salvage initiatives that are expected to seed regional centres of excellence within the next decade.

- Amgen

- Bayer

- Novartis

- Johnson & Johnson

- Pfizer

- Takeda Pharmaceuticals

- Eli Lilly and Company

- Hikma Pharmaceuticals

- Recordati S.p.A

- Spectrum Pharmaceuticals

- Debiopharm Group

- Atlanthera

- Adaptimmune Therapeutics plc

- Daiichi Sankyo

- Roche

- Ipsen

- OncoTherapy Science Inc.

- Legend Biotech

- Merck

- Gilead Sciences

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Global Incidence of Primary Bone Sarcomas

- 4.2.2 Approvals & Pipeline Momentum of Targeted Biologics

- 4.2.3 Expanded Government & NGO-Led Sarcoma Awareness Programmes

- 4.2.4 Advances In Functional Imaging & AI Diagnostics Enabling Earlier Detection

- 4.2.5 3D-Printed, Patient-Specific Orthopedic Implants Boosting Limb-Salvage Adoption

- 4.2.6 Orphan-Drug Exclusivity and Tax Incentives Accelerating Niche Therapy R&D

- 4.3 Market Restraints

- 4.3.1 Limited Therapeutic Options for Metastatic or Refractory Bone Tumours

- 4.3.2 High Cost of Novel Biologics & Cell Therapies Limiting Access

- 4.3.3 Post-Operative Morbidity and Lengthy Rehabilitation Deterring Surgery Uptake

- 4.3.4 Shortage of Specialised Orthopaedic Oncologists in Emerging Markets

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value in USD)

- 5.1 By Bone Cancer Type

- 5.1.1 Primary Bone Cancer

- 5.1.1.1 Osteosarcoma

- 5.1.1.2 Chondrosarcoma

- 5.1.1.3 Ewing Sarcoma

- 5.1.1.4 Other Primary Types

- 5.1.2 Secondary (Metastatic) Bone Cancer

- 5.1.1 Primary Bone Cancer

- 5.2 By Therapy Type

- 5.2.1 Chemotherapy

- 5.2.1.1 Anthracyclines

- 5.2.1.2 Alkylating Agents

- 5.2.1.3 Antimetabolites & Others

- 5.2.2 Targeted Therapy

- 5.2.2.1 RANKL Inhibitors

- 5.2.2.2 Tyrosine Kinase Inhibitors

- 5.2.2.3 mTOR/MEK & Emerging Targets

- 5.2.3 Immunotherapy

- 5.2.4 Immune Check-point Inhibitors

- 5.2.5 Cell & Gene Therapies

- 5.2.6 Radiation Therapy

- 5.2.7 Surgery & Limb-Salvage Procedures

- 5.2.8 Others

- 5.2.1 Chemotherapy

- 5.3 By Age Group

- 5.3.1 Pediatric

- 5.3.2 Adolescent & Young Adult

- 5.3.3 Adult

- 5.3.4 Geriatric

- 5.4 By End User

- 5.4.1 Hospitals

- 5.4.2 Specialty Cancer Centres & Orthopaedic Institutes

- 5.4.3 Academic & Research Institutes

- 5.4.4 Ambulatory Surgical Centres

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East & Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Amgen Inc.

- 6.3.2 Bayer AG

- 6.3.3 Novartis AG

- 6.3.4 Johnson & Johnson (Janssen)

- 6.3.5 Pfizer Inc.

- 6.3.6 Takeda Pharmaceutical Company Ltd.

- 6.3.7 Eli Lilly and Company

- 6.3.8 Hikma Pharmaceuticals PLC

- 6.3.9 Recordati S.p.A

- 6.3.10 Spectrum Pharmaceuticals Inc.

- 6.3.11 Debiopharm Group

- 6.3.12 Atlanthera

- 6.3.13 Adaptimmune Therapeutics plc

- 6.3.14 Daiichi Sankyo Company Ltd.

- 6.3.15 F. Hoffmann-La Roche Ltd.

- 6.3.16 Ipsen S.A.

- 6.3.17 OncoTherapy Science Inc.

- 6.3.18 Legend Biotech

- 6.3.19 Merck & Co., Inc.

- 6.3.20 Gilead Sciences (Kite Pharma)

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment