|

시장보고서

상품코드

1939136

실리콘 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Silicone - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

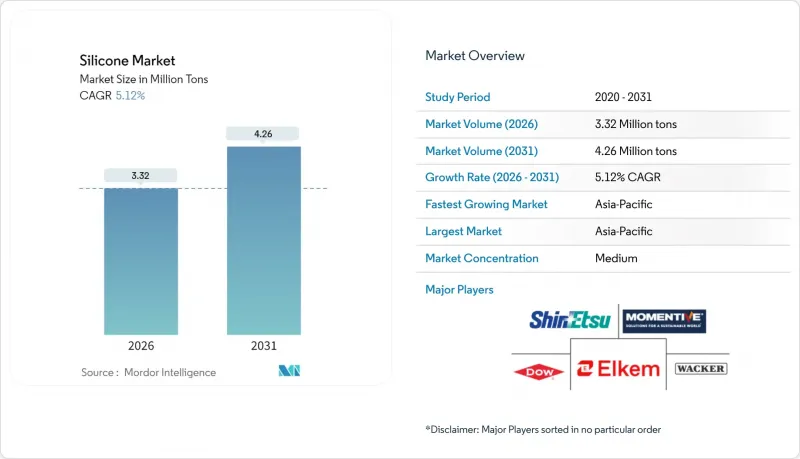

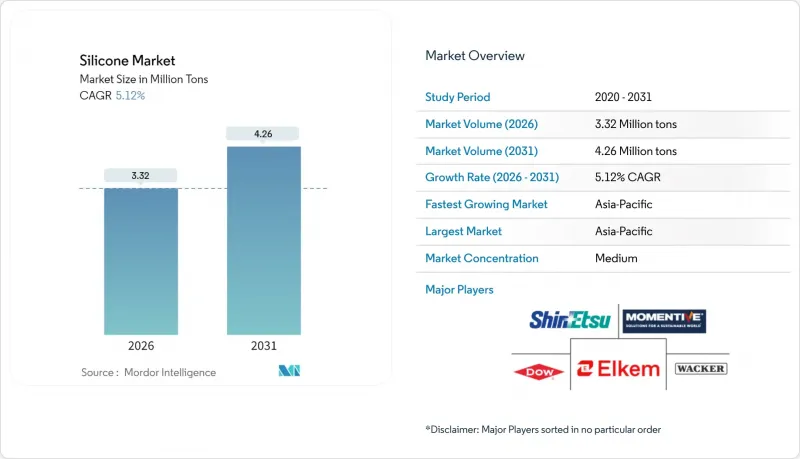

2026년 실리콘 시장 규모는 332만 톤으로 추정되며, 2025년 316만 톤으로부터 성장이 전망됩니다. 2031년의 예측에서는 426만 톤에 달하며, 2026-2031년에 CAGR 5.12%로 확대할 전망입니다.

이러한 꾸준한 성장세는 성숙한 최종 용도 분야에서 소재의 확고한 입지를 반영하는 동시에, 특히 전기 이동성, 재생에너지, 첨단 전자, 의료 기술 등 더 높은 성능과 신뢰성을 요구하는 차세대 용도에서 빠르게 확산되고 있음을 보여줍니다. 아시아태평양의 견고한 인프라 투자, 배터리 전기자동차로의 전환, 그리고 내구성이 높고 유지보수가 적은 소재에 대한 규제 강화로 인해 기준선 성장세가 지속되고 있습니다. 동시에 열 관리, 생체 적합성, 환경 규제 대응을 목적으로 하는 특수 등급은 가격 프리미엄을 창출하여 생산자가 금속 실리콘 가격 변동으로부터 이익률을 보호할 수 있도록 합니다. 경쟁 장벽은 통합된 공급망, 독자적인 배합 기술, 안전성이 매우 중요한 응용 분야에서 요구되는 인증 사이클에 뿌리를 두고 있으며, 이 모든 것이 실리콘 업계의 기존 기업에게 꾸준한 가치 창출의 길을 지원하고 있습니다.

세계 실리콘 시장 동향 및 인사이트

자동차 및 전기 모빌리티 분야에서의 적용 확대

전기자동차(EV)의 보급으로 기존 엘라스토머와의 성능 차이가 확대되면서 실리콘의 사용량이 급증하고 있습니다. 테슬라 모델 Y는 배터리 팩 실링, 열 갭 패드, 고전압 케이블 절연재 등 총 15kg의 실리콘을 사용하며, 이는 내연기관 세단의 약 3배에 해당하는 양입니다. 유럽 자동차 제조업체들은 현재 150℃의 새로운 부동액을 견뎌야 하는 Under-The-Hood 부품에 액상 실리콘 고무(LSR)를 채택하는 경향이 있습니다. 중국 EV 제조업체들은 실리콘 금속 가격의 변동성을 완화하기 위해 고점도 고무와 부가중합형 LSR의 이중 조달을 시작하고 있으며, 통합 공급업체에 장기 계약 체결을 촉구하고 있습니다. 엄격한 무공해 목표가 단계적으로 도입되는 가운데, 주요 자동차 제조업체들은 개스킷, 포팅, 인터페이스 재료의 재설계를 진행하고 있으며, 이는 실리콘 산업 전반에 걸쳐 고급 등급에 대한 지속적인 수요를 창출하고 있습니다.

의료 및 의료기기 분야 사용 확대

의료용 실리콘은 USP Class VI 및 ISO 10993 테스트를 통과해야 하며, 이 프로토콜은 신제품 개발 로드맵을 최대 24개월까지 연장하여 기존 공급업체가 단기 사이클의 가격 압박으로부터 보호받을 수 있도록 합니다. 웨어러블 혈당 모니터, 심장 리드, 신경조절 임플란트는 모두 LSR의 저알레르기 특성과 체온 하에서 안정적인 탄성률에 의존하고 있습니다. 병원에서는 감마선, 증기, 전자선 멸균법과의 적합성을 평가받고 있으며, 저침습 기기의 효율적인 재사용 전략을 지원하고 있습니다. 의료의 디지털화, 특히 원격 모니터링의 발전으로 광학 센서를 통합하면서 굴곡 수명을 손상시키지 않는 반투명 및 광학 투명 실리콘 필름에 대한 OEM 수요가 증가하고 있습니다. 이러한 요인들이 결합되어 의료 분야는 실리콘 산업에서 이익률 향상을 지원하는 기둥으로 확고한 입지를 구축하고 있습니다.

변동하는 실리콘 금속 가격과 공급 병목현상

2024년 실리콘 금속 현물 가격은 에너지 가격 변동과 무역 조치의 영향으로 톤당 1,800-3,200달러 사이에서 변동하여 통합 제조업체와 무역업체 제조업체의 이익률을 압박했습니다. 중국은 세계 생산량의 약 68%를 공급하고 있으므로 지방의 전력 제한은 즉시 하류 실리콘 생산량과 가격에 영향을 미칩니다. 장기 공급 계약이 일부 영향을 완화시키지만, 대부분은 매년 갱신되므로 구매자는 구조적인 에너지 비용 상승에 계속 노출되어 있습니다. 반도체 제조 공정에서 발생하는 단품의 재활용 시험에서는 화학적 등급 수요의 5% 미만을 회수할 수 있으며, 약간의 완화 효과만 얻을 수 있습니다. 저탄소 제련 기술의 다양화와 규모 확대가 진행되기 전까지는 실리콘 산업의 단기 예측은 원자재 가격 변동에 의해 계속 가려질 것입니다.

부문 분석

2025년 기준 엘라스토머는 실리콘 시장 점유율의 49.35%를 차지할 것으로 예상되며, 2031년까지 연평균 복합 성장률(CAGR) 5.33%로 확대될 것으로 전망됩니다. 이 분야에서는 EV 커넥터와 의료용 카테터용 액체 실리콘 고무가 증분 생산량의 대부분을 차지하고 있으며, 고점도 고무는 산업용 개스킷 분야에서 지속적인 수주를 확보하고 있습니다. LSR의 백금계 경화 화학은 사이클 타임을 단축하고, 멀티캐비티 금형의 효율적인 스케일업이 가능하여 대량 생산 부품에 대응할 수 있습니다. 한편, 실온경화형(RTV) 등급은 건설 보수 분야 실란트 사업 강화에 기여하며 매크로 사이클에 영향을 받지 않는 안정적인 수요를 창출하고 있습니다. 이러한 특성이 결합되어 엘라스토머는 실리콘 산업의 핵심 혁신 거점이 되었습니다.

액체 제품은 생산량에서 2위를 차지하고 있으며, 공정 보조제, 윤활유, 퍼스널케어용 연화제로서의 역할이 기반이 되고 있습니다. 실리콘계 화합물에 대한 규제 강화로 범용 순환형 시장에 도전이 되고 있는 반면, 휘발성이 낮은 직쇄형 액체에 대한 수요가 확대되어 손실을 상쇄하는 데 기여하고 있습니다. 수지는 파워 일렉트로닉스 및 태양전지판의 보호용 봉지재로서 틈새 시장으로 성장하고 있으며, 그 열 안정성은 에폭시계 재료를 능가합니다. 젤, 폼, 파우더와 같은 특수 형태가 제품 라인을 보완하고, 첨단 섬유, 3D 프린팅용 수지, 적층 조형용 바인더를 공급하고 있습니다. 경계가 모호해지는 가운데, 이러한 종합적인 발전은 실리콘 시장 규모에 균형 잡힌 기여를 유지하고 있습니다.

본 실리콘 보고서는 형태별(유체, 엘라스토머, 수지, 기타), 용도별(운송 장비, 건축자재, 전자제품, 의료, 산업 공정, 퍼스널케어 및 소비재, 기타), 지역별(아시아태평양, 북미, 유럽, 유럽, 남미, 중동 및 아프리카)로 구분하여 조사했습니다. 시장 예측은 톤 단위로 제공됩니다.

지역별 분석

아시아태평양은 통합된 공급망과 활발한 다운스트림 제조를 배경으로 2025년 세계 실리콘 시장 점유율의 65.10%를 차지했습니다. 중국에는 현지 금속 실리콘 용광로와 엘라스토머 가공 공장을 결합한 완전 후방 통합형 기업이 존재하여 비용 경쟁력과 빠른 규모 확장을 가능하게 합니다.

북미는 기술적으로 가장 앞선 지역이며, 항공우주, 첨단 자동차, 의료기기 제조업체들이 엄격한 재료 사양을 요구하고 있습니다. CHIPS법은 국내 반도체 생산을 촉진하고 초저이온 오염 실리콘 봉지재의 신규 수주를 촉진하고 있습니다. 중서부 지역의 풍력 터빈 리파워링과 남서부 지역의 태양광발전소 확장은 고내구성 실란트에 대한 수요를 지원할 것입니다. 한편, 미국 식품의약국(FDA)의 LSR(액상 실리콘 고무) 부품에 대한 예측 가능한 승인 절차는 의료 분야 수요를 촉진할 것입니다. 이러한 추세에 더해 바이오 실록산 전구체에 대한 활발한 연구와 함께 이 지역은 실리콘 산업에서 혁신을 주도하는 지역으로 자리매김하고 있습니다.

유럽은 특수 용도와 규제 측면에서의 리더십을 통해 그 입지를 확고히 하고 있습니다. 생산업체는 폐 엘라스토머 폐기물을 환형 모노머로 전환하는 폐루프 탈중합 설비에 투자하여 이 지역의 순환 경제 구상에 부합하는 노력을 기울이고 있습니다. 자동차의 전동화 의무화는 고온, 저발열 열패드에 대한 수요를 불러일으키고, 북해 해상풍력발전의 확대는 나셀 봉입용 고내구성 수지를 필요로 하고 있습니다. REACH 규제 의무는 규정 준수 비용을 증가시키지만, 동시에 직접적인 경쟁을 억제하는 장벽이 되어 유럽 실리콘 산업 전체의 가치 밀도를 유지하고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 개요

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KSA 26.03.05Silicone market size in 2026 is estimated at 3.32 million tons, growing from 2025 value of 3.16 million tons with 2031 projections showing 4.26 million tons, growing at 5.12% CAGR over 2026-2031.

This measured expansion reflects the material's entrenched role across mature end-uses while signaling rapid uptake in next-generation applications that demand higher performance and reliability, especially in electric mobility, renewable power, advanced electronics, and medical technology. Robust infrastructure spending in Asia-Pacific, the shift to battery-electric vehicles, and regulatory pushes for more durable, low-maintenance materials continue to underpin baseline growth. At the same time, specialty grades designed for thermal management, biocompatibility, and environmental compliance are unlocking price premiums that help producers protect margins from silicon-metal volatility. Competitive barriers remain rooted in integrated supply chains, proprietary formulations, and the qualification cycles required in safety-critical applications, all of which support a steady value-creation path for incumbents in the silicone industry.

Global Silicone Market Trends and Insights

Rising Applications in Automotive and E-mobility

Electric-vehicle (EV) adoption is multiplying the use of silicone by widening the performance gap versus traditional elastomers. Battery-pack sealing, thermal gap-pads, and high-voltage cable insulation collectively add close to 15 kg of silicone per Tesla Model Y, roughly triple that of an internal-combustion sedan. European OEMs now favor liquid-silicone rubber (LSR) for under-hood parts that must withstand new glycol-free coolants at 150 °C. Chinese EV makers have begun dual-sourcing high-consistency rubber and addition-cure LSR to buffer silicon-metal price swings, encouraging integrated suppliers to lock in long-term contracts. As stringent zero-emission targets phase in, every major automaker is redesigning gasketing, potting, and interface materials, creating an enduring pull for advanced grades across the silicone industry.

Increasing Usage in Healthcare and Medical Devices

Medical-grade silicones must clear USP Class VI and ISO 10993 testing, a protocol that can extend new-product roadmaps by up to 24 months, thereby shielding incumbent suppliers from short-cycle pricing pressure. Wearable glucose monitors, cardiac leads, and neuromodulation implants all hinge on LSR's hypoallergenic profile and stable modulus at body temperature. Hospitals value the polymer's sterilization compatibility with gamma, steam, and e-beam methods, which supports lean re-use strategies in minimally invasive tools. Digitization of care-particularly remote monitoring-has sparked OEM demand for translucent, optically clear silicone films that integrate optical sensors without compromising flex-life. Collectively, these factors cement healthcare as a margin-accretive pillar of the silicone industry.

Volatile Silicon-metal Prices and Supply Bottlenecks

Spot silicon-metal swung between USD 1,800-3,200/ton in 2024 on energy-price gyrations and trade measures, squeezing margin profiles across integrated and merchant producers alike. China supplies nearly 68% of global output, so provincial power rationing immediately reverberates through downstream silicone volumes and pricing. While long-term offtake contracts provide partial insulation, most renew annually, leaving buyers exposed to structural energy-cost inflation. Pilot recycling of semiconductor kerf scrap yields less than 5% of chemical-grade demand, offering only modest relief. Until diversified, low-carbon smelting gains scale, raw-material turbulence will shadow short-term forecasts for the silicone industry.

Other drivers and restraints analyzed in the detailed report include:

- Demand from Power Transmission and Distribution Grids

- 5G Base-station Thermal Interface Materials

- Stringent Siloxane Emission Regulations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Elastomers controlled 49.35% of the silicone market share in 2025 and are forecast to grow at a 5.33% CAGR through 2031. Within this group, liquid-silicone rubber for EV connectors and medical catheters captures the lion's share of incremental tonnage, while high-consistency rubber secures repeat orders in industrial gasketing. LSR's platinum-cure chemistry shortens cycle times, allowing multi-cavity molds that scale efficiently for high-volume parts. Meanwhile, room-temperature-vulcanizing (RTV) grades strength-en sealant franchises in construction rehabilitation, feeding consistent demand regardless of macro-cycles. Collectively, these attributes make elastomers the pivotal innovation hub in the silicone industry.

Fluids rank second in volume, anchored by their role as process aids, lubricants, and personal-care emollients. Although impending siloxane limits challenge commodity cyclics, linear-chain fluids with lower volatility are gaining traction and help offset losses. Resins continue to deliver niche growth as protective encapsulants in power electronics and solar panels, where their thermal stability outperforms epoxy analogs. Specialty formats-gels, foams, and powders-round out the portfolio, supplying advanced textiles, 3-D printing resins, and additive-manufacturing binders. Even as boundaries blur, the cumulative developments sustain a balanced contribution to the silicone market size.

The Silicone Report is Segmented by Form (Fluids, Elastomers, Resins, and Others), Application (Transportation, Construction Materials, Electronics, Healthcare, Industrial Processes, Personal Care and Consumer Products, and Other Applications), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Volume (Tons).

Geography Analysis

Asia-Pacific wielded 65.10% of the global silicone market share in 2025, propelled by integrated supply chains and prolific downstream manufacturing. China features fully backward-integrated players that couple local silicon-metal furnaces to elastomer finishing plants, enabling cost competitiveness and rapid scale-up.

North America remains a technology vanguard, where aerospace, advanced automotive, and biomedical device makers impose stringent material specifications. The CHIPS Act catalyzes domestic semiconductor production, triggering new orders for ultra-low-ionic contamination silicone encapsulants. Wind-turbine repowering in the Midwest and solar-farm expansions in the Southwest anchor demand for high-durability sealants, while the U.S. Food and Drug Administration's predictable pathway for LSR components bolsters healthcare volumes. These trends, paired with active research into bio-based siloxane precursors, position the region as an innovation driver in the silicone industry.

Europe secures its role through specialty applications and regulatory leadership. Producers invest in closed-loop depolymerization units that convert spent elastomer scrap into cyclic monomers, aligning with the bloc's circular-economy vision. Automotive electrification mandates energize demand for high-temperature, low-bleed thermal pads, while offshore-wind build-outs in the North Sea necessitate robust resins for nacelle encapsulation. Although REACH obligations elevate compliance costs, they also create barriers that temper direct price competition, sustaining value density across the European silicone industry.

- BRB International (PETRONAS)

- CHT Germany GmbH

- DIC Corporation

- Dongyue Group

- Dow

- DyStar Singapore Pte Ltd

- Elkem ASA

- Evonik Industries AG

- Hoshine Silicon Industry Co., Ltd

- KANEKA Corporation

- KCC SILICONE CORPORATION

- Momentive

- Shin-Etsu Chemical Co. Ltd

- Siltech Corporation

- Wacker Chemie AG

- Wynca Tinyo Silicone Co., Ltd.

- Zhejiang Hengyecheng Organic Silicone Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising applications in automotive and e-mobility

- 4.2.2 Increasing usage in healthcare and medical devices

- 4.2.3 Demand from power transmission and distribution grids

- 4.2.4 5G base-station thermal interface materials

- 4.2.5 LSR adoption in wearable medical sensors

- 4.3 Market Restraints

- 4.3.1 Volatile silicon-metal prices and supply bottlenecks

- 4.3.2 Stringent siloxane emission regulations

- 4.3.3 Competition from fluoropolymers and thermoplastics

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Form

- 5.1.1 Fluids

- 5.1.2 Elastomers

- 5.1.3 Resins

- 5.1.4 Others

- 5.2 By Application

- 5.2.1 Transportation

- 5.2.2 Construction Materials

- 5.2.3 Electronics

- 5.2.4 Healthcare

- 5.2.5 Industrial Processes

- 5.2.6 Personal Care and Consumer Products

- 5.2.7 Other Applications

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Thailand

- 5.3.1.6 Malaysia

- 5.3.1.7 Indonesia

- 5.3.1.8 Vietnam

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 Turkey

- 5.3.3.8 Nordics

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Nigeria

- 5.3.5.4 Egypt

- 5.3.5.5 Qatar

- 5.3.5.6 United Arab Emirates

- 5.3.5.7 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 BRB International (PETRONAS)

- 6.4.2 CHT Germany GmbH

- 6.4.3 DIC Corporation

- 6.4.4 Dongyue Group

- 6.4.5 Dow

- 6.4.6 DyStar Singapore Pte Ltd

- 6.4.7 Elkem ASA

- 6.4.8 Evonik Industries AG

- 6.4.9 Hoshine Silicon Industry Co., Ltd

- 6.4.10 KANEKA Corporation

- 6.4.11 KCC SILICONE CORPORATION

- 6.4.12 Momentive

- 6.4.13 Shin-Etsu Chemical Co. Ltd

- 6.4.14 Siltech Corporation

- 6.4.15 Wacker Chemie AG

- 6.4.16 Wynca Tinyo Silicone Co., Ltd.

- 6.4.17 Zhejiang Hengyecheng Organic Silicone Co., Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet Need Assessment