|

시장보고서

상품코드

1687302

열가소성 폴리에스테르 엘라스토머(TPE-E) 시장 : 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Thermoplastic Polyester Elastomer (TPE-E) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

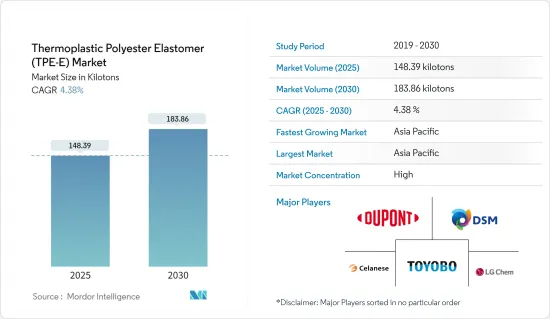

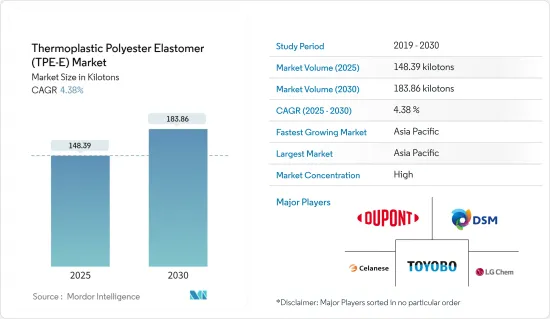

세계의 열가소성 폴리에스테르 엘라스토머(TPE-E) 시장 규모는 2025년 148.39킬로톤으로 추정되며, 예측 기간 중(2025-2030년) CAGR 4.38%로 확대되어, 2030년에는 183.86킬로톤에 이를 것으로 예측됩니다.

시장은 2020년의 COVID-19에 의해 부정적인 영향을 받았습니다.

주요 하이라이트

- 단기적으로는 자동차 산업에서의 수요 증가와 의료와 의료 시설에 대한 지출 증가가 시장 성장의 주요인입니다.

- 그러나, 열가소성 폴리에스테르 엘라스토머의 비용이 높은 것이, 예측 기간중의 대상 산업의 성장을 억제하는 주요인이 되고 있습니다.

- 바이오의 열가소성 폴리에스테르 엘라스토머 시장의 대두는 곧 세계 시장에 유리한 성장 기회를 가져올 것으로 예상됩니다.

- 아시아태평양은 자동차 생산에서 TPEE의 지속적인 사용량 증가, 의료 산업의 성장과 함께 중국, 일본 및 기타 동남아시아 국가에서 열가소성 폴리에스테르 엘라스토머(TPE-E)의 높은 수요로 조사 시장에서 평가 기간 동안 건전한 성장을 볼 수 있을 것으로 추정됩니다.

열가소성 폴리에스터 엘라스토머(TPE-E) 시장 동향

자동차 산업에서의 사용 증가

- 열가소성 폴리에스테르 엘라스토머(TPE-E)는 고성능 재료이며 자동차 산업에서의 용도가 급속히 확대되고 있습니다.

- TPE-E는 자동차 산업의 여러 용도로 유용하며, 그 중에는 고품질의 자동차 계기판, CVJ 부츠, 휠 커버, 에어 흡입 덕트, 에어백 전개 도어, 대시 보드 부품, 필러 트림, 도어 라이너 및 핸들, 시트 백, 안전 벨트 부품 등의 제조가 포함됩니다.

- TPE-E는 내마모성과 내진동성이 뛰어나 임의의 색으로 염색할 수 있기 때문에 설계의 자유도가 높습니다.

- 자동차 산업은 다양한 차량 용도에 경량 재료를 활용하기 위해 노력하고 있습니다.

- OICA에 따르면, 2021년 세계의 전 자동차 판매 대수는 8,015만 4,988대로, 2020년의 1,245만 2,453대에 비해 3%의 성장을 기록했습니다.

- 인도와 중국에서는 시대 지연 차량을 폐차로 하고 공해를 최소화하기 위해 자동차 폐차 정책이 실시되고 있습니다. 이 프로그램은 유효한 적합 증명서를 가지지 않는 구식차나 운행 불능차를 단계적으로 폐지하는 것으로, 공해를 삭감하는 것을 목적으로 하고 있습니다.

- 2021년 세계 EV 판매 대수는 6억 7,500만대에 달했고, 2020년의 EV 판매 대수와 비교해 108% 증가했습니다. 이 대수에는 승용차, 소형 트럭, 소형 상용차가 포함됩니다.

- IEA에 따르면 2030년 세계 전기차 판매 대수는 신정책 시나리오에서는 1억 2,500만대에 이를 전망입니다(이륜차/삼륜차 제외). EV30@30 시나리오에서는 2030년에는 중국에서의 자동차 판매의 약 70%가 EV가 될 것으로 예상되고 있습니다. 또, 지금까지의 추정 판매액에서는 유럽의 EV 판매 대수는 50%, 일본은 37%, 캐나다 및 미국은 30%, 인도는 29%로 추정되고 있습니다.

- 따라서, 상기 요인에 의해 TPE-E 수요는 예측 기간 중에 긍정적인 영향을 받을 것으로 예상됩니다.

시장을 독점하는 아시아태평양

- 아시아태평양이 시장을 독점할 것으로 예상됩니다.

- 중국은 세계 최대의 자동차 제조업체입니다. 이 나라의 자동차 부문은 환경 문제에 대한 관심이 높아 배출 가스를 최소화하면서 연비를 확보하는 제품의 제조에 중점을 두고 제품의 진화를 도모하고 있습니다. 2020년 2,523만대에서 3% 증가했으며, 2025년에는 3,500만대까지 성장할 것으로 예상되고 있습니다.

- 중국은 일반산업부문이 확립하고 있습니다.의 2021년 12월의 공업 생산고는 전년 동월 대비 4.3% 증가(11월 대비 0.42% 증가)해, 이 나라의 열가소성 폴리에스테르 엘라스토머 수요를 증가시켰습니다.

- 중국은 세계 최대급의 전자기기 생산기지를 가지고 있으며, 한국, 싱가포르, 대만 등 기존의 업스트림 제조업체에 엄격한 경쟁을 제공합니다.

- 소득의 지속적인 증가는 인구 1인당 가처분 소득 증가를 가져오며, 이는 중국의 전자제품 수요에 이익을 가져올 것으로 예상됩니다. 중국국가통계국에 의하면 소비자용 전자기기 및 가정용 전기제품 부문의 매출은 2021년에 9억 3,464만 위안(약 1억 3,127만 달러)에 이르렀습니다.

- 게다가 OICA에 따르면, 인도에서는 2021년에 약 439만 9,112대가 생산되어 2020년의 338만 1,819대에 비해 30% 증가했습니다.

- 또, 이 나라의 의료부문은 주로 건강의식의 향상, 보험에 대한 액세스, 소득 증가, 질병에 의해 2022년까지 3,720억 달러에 이를 것으로 예상되고 있습니다.

- 인도에서는 최근 산업 부문이 급성장하고 있습니다. 인도의 산업 생산 지수(IIP)는 2020-2021년 111.7에서 2021-22년에는 128.7로 상승했습니다. 이 성장은 국가 제조업 정책(제조업이 GDP에서 차지하는 비율을 2025년까지 25%로 끌어올리는 것을 목표로 한다)나 제조업용 PLI 제도(2022년에 개시)라고 하는 정부의 여러가지 대처에도 지지되고 있어, 그것에 의해 국내의 열가소성 폴리에스테르 엘라스토머 수요가 증가하고 있습니다.

- India Brand Equity Foundation(IBEF)에 따르면 인도의 전자기기 제조업은 2025년까지 5,200억 달러에 달할 것으로 예상되고 있습니다.

- 이러한 모든 요인으로부터, 이 지역의 열가소성 폴리에스테르 엘라스토머 시장은 예측 기간 중에 안정된 성장이 전망됩니다.

열가소성 폴리에스테르 엘라스토머(TPE-E) 산업 개요

세계의 열가소성 폴리에스터 엘라스토머(TPE-E) 시장은 상위 상장 기업이 세계 시장에서 큰 점유율을 차지하고 있으며, 그 성질상 통합형이 되고 있습니다. 세계기업은 신기술을 개발하고 시장에서의 존재감과 골격을 높이기 위해 연구개발, 인수, 제휴에 크게 주력하고 있습니다. 조사 대상 시장의 주요 제조업체로는 DuPont, Celanese Corporation, Koninklijke DSM NV, LG Chem, Toyobo 등이 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 성장 촉진요인

- 자동차 산업에서의 수요 증가

- 의료 및 의료 시설에 대한 지출 증가

- 억제요인

- 열가소성 폴리에스테르 엘라스토머의 고비용

- 밸류체인 분석

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 세분화

- 유형

- 사출 성형 등급

- 압출 등급

- 기타

- 최종 사용자 산업

- 자동차

- 의료

- 공업용

- 전기 및 전자

- 소비재

- 기타

- 지역

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 이탈리아

- 프랑스

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- M&A, 합작사업, 제휴, 협정

- 시장 랭킹 분석

- 주요 기업의 전략

- 기업 프로파일

- Celanese Corporation

- Chang Chun Group

- DSM

- Kolon Plastic Inc.

- LG Chem

- Mitsubishi Chemical Corporation

- Radici Partecipazioni SpA

- Sichuan Sunshine Plastics Co. Ltd

- SK Chemicals

- Toyobo Co. Ltd

제7장 시장 기회와 앞으로의 동향

- 바이오 베이스 열가소성 폴리에스테르 엘라스토머의 신흥 시장

The Thermoplastic Polyester Elastomer Market size is estimated at 148.39 kilotons in 2025, and is expected to reach 183.86 kilotons by 2030, at a CAGR of 4.38% during the forecast period (2025-2030).

The market was negatively impacted by COVID-19 in 2020. The pandemic had a severe impact on the automotive industry, including manufacturing interruptions and disruption in the supply chain across the globe, thereby negatively affecting the market. However, the market recovered steadily, owing to the increased growth of the automotive industry in 2021.

Key Highlights

- Over the short term, growing demand from the automotive industry, coupled with growing expenditure on healthcare and medical facilities, are major factors driving the growth of the market studied.

- However, the high cost of thermoplastic polyester elastomer is a key factor anticipated to restrain the growth of the target industry over the forecast period.

- Nevertheless, the emerging market for bio-based thermoplastic polyester elastomer is likely to create lucrative growth opportunities for the global market soon.

- Asia-Pacific is estimated to witness healthy growth over the assessment period in the studied market due to the high demand for thermoplastic polyester elastomer (TPE-E) in China, Japan, and other Southeast Asian countries owing to continuous and rising usage of TPEE in automotive production, coupled with the growing medical industry.

Thermoplastic Polyester Elastomer (TPE-E) Market Trends

Increasing Usage in the Automotive Industry

- Thermoplastic polyester elastomers (TPE-E) are high-performance materials whose application in the automotive industry has rapidly increased. TPE-E utilization in the automotive sector extends from the exterior and interior parts to engine components. The high durability, light weight, and cost-effectiveness of TPE-Es make them extremely coveted by automotive materials manufacturers.

- TPE-Es serve the automotive industry in several applications, some of which include the manufacturing of high-quality automotive instrument panels, CVJ boots, wheel covers, air intake ducting, airbag deployment doors, dashboard components, pillar trim, door liners and handles, seat backs, and seat belt components, among others.

- TPE-Es offer high design flexibility by being resistant to abrasion and vibration and dyeable in any desired color. They are highly durable in harsh weather conditions; hence they are preferred for internal mechanisms such as car locks. These properties also support the demand for long-term heat-resistant materials in electric vehicle fabrication.

- The automotive industry is working on utilizing lightweight materials for various vehicle applications. Hence, the growing automotive industry globally is expected to boost the demand for TPE-Es.

- According to OICA, the global sales of all vehicles in 2021 acoounted for 80,154,988 units, registering a growth of 3% as compared to 12,452,453 units sold in 2020.

- Vehicle scrappage policies are being implemented in India and China to scrap outdated vehicles and minimize pollution. It plans to cover 51 lakh light motor vehicles older than 20 years and 34 lakh light motor vehicles older than 15 years. This program aims to reduce pollution by phasing out obsolete or inoperable vehicles that do not have a valid fitness certificate. This approach will raise market demand for new cars.

- The global EV sales reached 675 million units in the entire year of 2021, 108% more as compared to the EV sales in 2020. This volume includes passenger vehicles, light trucks, and light commercial vehicles. The BEVs stood for 71% of total EV sales, while the PHEVs stood at 29% in 2021.

- According to the IEA, in 2030, global electric vehicle sales are expected to reach 125 million, per the New Policies Scenario (excluding two/three-wheelers). In the EV30@30 Scenario, in 2030, around 70% of vehicle sales in China are expected to be EVs. Also, as per the approximate sales value till now, EV sales in Europe was estimated at 50%, while it was 37% in Japan, 30% in Canada and the United States, and 29% in India.

- Therefore, owing to the above factors, the demand for TPE-E is expected to be impacted positively during the forecast period.

Asia-Pacific Region to Dominate the Market

- Asia-Pacific is expected to dominate the market. In the region, China is the largest economy in terms of GDP. China is one of the fastest emerging economies and has become one of the biggest production houses in the world today. The country's manufacturing sector is one of the primary contributors to the country's economy.

- China is the largest manufacturer of automobiles in the world. The country's automotive sector has been shaping up for product evolution, focusing on manufacturing products to ensure fuel economy while minimizing emissions, owing to the growing environmental concerns. In 2021, according to the OICA, the automotive production in the country reached 26.08 million, which increased by 3%, compared to 25.23 million vehicles produced in 2020, and is expected to grow up to 35 million vehicles by 2025. The increase in automotive production is estimated to drive the demand for thermoplastic polyester elastomers in the country from both EVs and IC engine vehicle manufacturing sectors.

- China has a well-established general industrial sector. According to the data published by China's National Bureau of Statistics, the country's value-added industrial output went up 9.6% Year-on-Year in 2021. The country's industrial output grew 4.3% Y-o-Y in December 2021 (a 0.42 % increase from November), thereby increasing the demand for thermoplastic polyester elastomers in the country.

- China has one of the world's largest electronics production bases and offers tough competition to the existing upstream producers, such as South Korea, Singapore, and Taiwan. Electronic products, such as smartphones, OLED TVs, and tablets, have the highest growth rates in the consumer electronics segment of the market in terms of demand. Economic development in China and improving living standards among the population drive the demand for electronic goods.

- The continuous growth of income resulted in the rise in the population's per capita disposable income, which is expected to benefit the demand for electronic goods in China. The expansion of the middle class and high-income population group is expected to propel the demand for electronics. According to the National Bureau of Statistics of China, the revenue in the consumer electronics and household appliances segment reached CNY 934.64 million (approx. USD 131.27 million) in 2021. The revenue is expected to show an annual growth rate of 2.04%, resulting in a projected market volume of USD 175,670 million by 2025.

- Further, in India, as per OICA, around 4,399,112 vehicles were produced in 2021, which increased by 30%, comparison to 3,381,819 units manufactured in 2020.

- Also, the healthcare sector in the country is expected to reach USD 372 billion by 2022, mainly driven by increasing health awareness, access to insurance, rising income, and diseases. The medical sector in India is benefiting from the growing population at a rate of 1.6 % per year.

- India has witnessed rapid growth in the industrial sector in recent years. The index of industrial production (IIP) in India increased from 111.7 in 2020-21 to 128.7 in the 2021-22 period. This growth is also supported by various government initiatives like the National Manufacturing Policy (which aims to increase the share of manufacturing in GDP to 25% by 2025) and the PLI scheme for manufacturing (which was launched in 2022), thereby increasing the demand for thermoplastic polyester elastomers in the country.

- According to the India Brand Equity Foundation (IBEF), the Indian electronics manufacturing industry is expected to reach USD 520 billion by 2025. Electrical and electronics production in India is expected to increase rapidly due to government initiatives with policies, such as Make in India, the National Policy of Electronics, Net Zero Imports in Electronics, and the Zero Defect Zero Effect. Such policies offer a commitment to growth in domestic manufacturing, lowering import dependence and energizing exports and manufacturing, like the 'Make in India' program, to make the country self-reliant.

- Due to all such factors, the market for thermoplastic polyester elastomer in the region is expected to have a steady growth during the forecast period.

Thermoplastic Polyester Elastomer (TPE-E) Industry Overview

The global thermoplastic polyester elastomer (TPE-E) market is consolidated in nature, as the top listing companies hold a significant share of the global market. Global companies are significantly focusing on R&D, acquisitions, and collaborations to develop new technologies and to increase their market presence and foothold. The major manufacturers in the market studied include Dupont, Celanese Corporation, Koninklijke DSM N.V., LG Chem, and Toyobo Co., Ltd., among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand From the Automotive Industry

- 4.1.2 Growing Expenditure on Healthcare And Medical Facilities

- 4.2 Restraints

- 4.2.1 High Cost of Thermoplastic Polyester Elastomer

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Type

- 5.1.1 Injection Molding Grade

- 5.1.2 Extrusion Grade

- 5.1.3 Other Types

- 5.2 End-user Industry

- 5.2.1 Automotive

- 5.2.2 Healthcare

- 5.2.3 Industrial

- 5.2.4 Electrical and Electronics

- 5.2.5 Consumer Goods

- 5.2.6 Other End-user Industries

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East & Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East & Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Celanese Corporation

- 6.4.2 Chang Chun Group

- 6.4.3 DSM

- 6.4.4 Kolon Plastic Inc.

- 6.4.5 LG Chem

- 6.4.6 Mitsubishi Chemical Corporation

- 6.4.7 Radici Partecipazioni SpA

- 6.4.8 Sichuan Sunshine Plastics Co. Ltd

- 6.4.9 SK Chemicals

- 6.4.10 Toyobo Co. Ltd

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Emerging Market for Bio-based Thermoplastic Polyester Elastomer