|

시장보고서

상품코드

1445723

세계 원료의약품 CDMO 시장 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2024-2029년)Global Active Pharmaceutical Ingredients CDMO - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

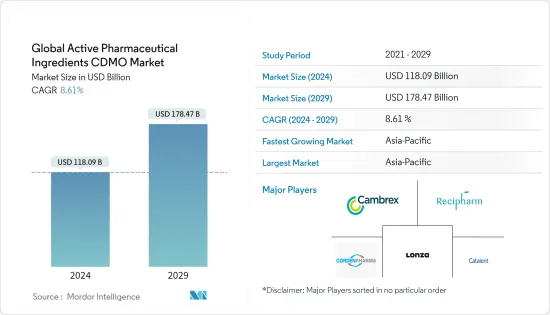

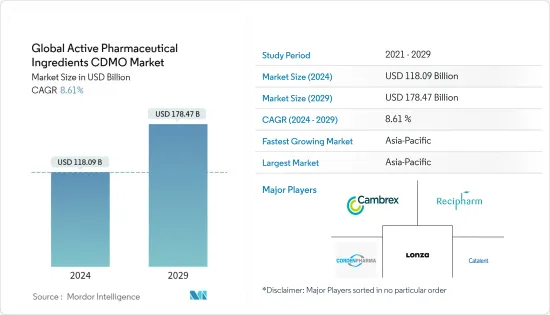

세계 원료의약품 CDMO 시장 규모는 2024년 1,180억 9,000만 달러로 추정되고, 2029년까지 1,784억 7,000만 달러에 이를 것으로 예측되며, 예측 기간(2024년부터 2029년) 동안 복합 연간 성장률(CAGR) 8.61%로 성장할 전망입니다.

COVID-19의 유행은 API CDMO 시장에 큰 영향을 미쳤습니다. 코로나바이러스 백신과 치료제가 전 세계적으로 전개됨에 따라 CDMO 서비스에 대한 수요가 급증했습니다. CDMO는 위기 동안 제약 회사의 고객 요구를 충족시키기 위해 엄청난 노력을 기울였습니다. CDMO는 의약품 개발 및 공급망, 상용 API 및 의약품 제조, 패키징 등의 광범위한 서비스를 제약 회사에 제공합니다. 이러한 서비스를 통해 제약 회사는 최첨단 기술의 혜택을 누리면서 개발 및 제조 비용, 자본 투자 및 일정을 줄일 수 있습니다.

예를 들어 2021년 상반기에는 CDMO의 COVID-19 백신 제조 참여와 강력한 합병,인수 활동이 두드러졌습니다. 또한 바이오/의약품 업계에서 CDMO의 필수성도 강조했습니다. 이것은 COVID-19 바이러스와 싸우는 백신과 치료법의 출시를 성공시키는 데 필수적이었습니다.

Drug, Chemical &Associated Technologies Association Inc.(DCAT)의 "연오 CDMO 검토 : COVID-19 백신 제조 및 M&A"에 대한 밸류체인 인사이트에 따르면, 유행의 처음 몇 달 동안 공개적으로 알려져 있습니다. 한 CDMO는 10개 미만이었습니다. CDMO는 백신의 활성 성분과 주요 부형제의 생산에 종사했습니다. 백신 생산 능력에 대한 수요로 인해 이전에는 오래된 제품과 제네릭에 의존했던 많은 CDMO의 지위와 프로파일이 증가했습니다. 예를 들어, Rovi Contract Manufacturing과 같은 일부 기업은 의약품과 의약품 계약을 맺고 있습니다.

게다가 2021년 상반기에는 투자자들이 업계 진출을 목표로 기존 기업이 자사의 능력을 확대, 심화시키려는 다수의 합병,인수 활동도 보였습니다. 2021년 첫 5개월 동안 총 32건의 거래가 발표되거나 완료되었습니다. 이 중 5건의 거래는 저분자 API 사업에 관한 것이고, 4건은 대분자 API 자산에 관한 것이었습니다.

CDMO에 아웃소싱함으로써 기업은 고도로 전문화된 전문가를 포함한 유연한 노동력에 대한 액세스를 얻을 수 있습니다. 최근에는 제약회사에서 바이오의약품회사에 이르기까지 중소기업에서 대기업에 이르기까지, 초기단계부터 후기단계 개발 프로젝트까지 제약회사에 의한 CDMO로의 아웃소싱이 증가하고 있습니다.

API의 품질은 의약품의 효능과 안전성에 현저한 영향을 미칩니다. 따라서 필요한 강도, 순도 및 품질로 정확한 API를 제공할 수 있는 CDMO를 선택하는 것은 의약품 개발 회사에게 중요한 결정입니다.

원료의약품 CDMO 시장 동향

상업 부문이 주요 시장 점유율을 유지할 것으로 예상

COVID-19의 유행에 따라 의약품 수요가 증가하고 생산 중단으로 일부 국가가 공급을 사들임으로써 수출이 증가했습니다. COVID-19의 사례가 급속히 증가했을 때 새로운 COVID-19의 백신과 치료제가 필요했습니다. 충분한 양의 치료제가 국내에서 생산되는 것을 보장하기 위해 일부 정부는 현지화 규제를 고려하기 시작했습니다.

그 결과, 많은 제약 회사들이 제조 기지를 확대하기 시작했고, 일부 제약 회사들은 앞으로 수년간의 계획을 수립하기 위해 제조 기지를 검토하기 시작했습니다. 추가 용량의 가장 큰 공급원은 CDMO였습니다.

게다가, 제약 회사는 계약 제조자와 상당한 공간을 예약했고, 경우에 따라서는 이중 예약을 하기도 했습니다. AstraZeneca, 모델나, 파이저는 Lonza, Catalent, Emergent Biosolutions 등 많은 CDMO와 파트너십 계약을 체결했다고 선언했습니다. 이 기회를 최대한 활용하여 Cambrex Corporation, Catalent, Samsung Biologics, 기타 많은 개발도상국 CDMO는 공장의 대규모 확장을 선언했습니다.

아시아태평양은 예측 기간 동안 시장에서 큰 점유율을 잡을 것으로 예상

중국과 인도는 미국과 유럽에 비해 제조 비용이 크게 낮습니다. Invest India에 따르면 인도의 제조 비용은 미국보다 약 33% 낮습니다. 중국과 인도는 API 제조 서비스의 중요한 공급자로서의 지위를 확립하고 있지만, 미국은 여전히 의약품 개발의 주요 아웃소싱 허브입니다. 이것은 대규모 자금 조달과 대학 관련 제약 조사 기지의 독점적 집중의 조합 때문입니다.

기존 의약품의 중요성 확대와 지속성 감염의 발생률의 급속한 증가는 인도의 API CDMO 시장의 순조로운 성장의 중요한 추진력이 되었습니다. 2020년 PHRMABIZ.com에 게재된 기사에 따르면, 제네릭 API는 인도에서 선진국으로 수출되고 있으며, 인도 총 매출의 41.6%를 차지하는 반면 중국에서는 24.7%를 차지하고 있습니다. Chemical Pharmaceutical Generic Association 조사에 따르면 인도는 미국 시장에 대한 제네릭 API의 두 번째로 큰 공급자이며 24.4%의 점유율을 차지하고 있습니다. 이 나라는 서유럽로공급도 늘고 있으며, 이 지역의 총 공급량의 19.2%를 차지합니다. 또한 중국은 세계 비독점적 API 공급업체 시장의 30%를 차지합니다. 중국에 이어 미국과 인도는 비독점적 API의 주요 생산국입니다.

원료의약품 CDMO 산업 개요

원료의약품 CDMO시장은 세분화되어 있으며 여러 주요 기업으로 구성되어 있습니다. 시장 점유율 측면에서 소수의 대기업은 시장을 독점하고 있습니다. 그 중 일부는 Cambrex Corporation, Patheon(Themo Fisher Scientific Inc.), Recipharm AB, CordenPharma International, Samsung Biologics, Lonza, Siegfried, Piramal Pharma Solutions, Abby Inc., Catalent Inc입니다.

의약품 공급망에서 API 제조업체의 역할은 고객의 새로운 요구와 세계 경쟁업체 증가하는 압력에 부응하여 진화하고 있습니다. 기존 제네릭 의약품 기업은 중국과 인도에 벌크 사업을 요구하고 있는 반면, 특수 제약 기업은 기존 제네릭 의약품에서 요구되는 것보다 전문적인 능력에 대한 새로운 수요를 창출하고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 시장 개요

- 시장 성장 촉진요인

- 의약품의 연구개발 투자 증가

- 제네릭 의약품 수요 증가

- 복잡한 제조

- 특허 유효기간

- 시장 성장 억제요인

- 아웃소싱 시 컴플라이언스 문제

- 데이터의 품질과 보안에 대한 우려

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체 제품의 위협

- 경쟁 기업간 경쟁 관계의 격렬

제5장 시장 세분화

- 분자유형별

- 저분자

- 고분자

- 합성별

- 생명공학

- 합성

- 약제유형별

- 혁신적

- 제네릭

- 워크플로우별

- 임상

- 상업

- 용도별

- 심장학

- 종양학

- 안과

- 신경내과

- 정형외과

- 기타

- 지역

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 기업 프로파일

- Cambrex Corporation

- Patheon(Thermo Fisher Scientific Inc.)

- Recipharm AB

- CordenPharma International

- Samsung Biologics

- Lonza

- Siegfried

- Piramal Pharma Solutions

- AbbVie Inc.

- Catalent Inc.

제7장 시장 기회와 미래 동향

BJH 24.03.15The Global Active Pharmaceutical Ingredients CDMO Market size is estimated at USD 118.09 billion in 2024, and is expected to reach USD 178.47 billion by 2029, growing at a CAGR of 8.61% during the forecast period (2024-2029).

The COVID-19 pandemic had a huge impact on the API CDMO market. As the vaccines and therapeutics for the coronavirus were rolled out globally, the demand for CDMO services skyrocketed. CDMOs went to great lengths to meet the needs of their pharmaceutical customers during the crisis. CDMOs provide a broad range of services to pharmaceutical companies, such as drug development and supply chain, commercial API and drug manufacturing, and packaging. These services permit pharmaceutical firms to reduce their development and manufacturing costs, along with capital investments and timelines, while benefiting from the most advanced technologies.

For instance, in the first half of 2021, there was marked participation of CDMOs in COVID-19 vaccine manufacturing and robust merger acquisition activities. It also highlighted the indispensability of CDMOs in the bio/pharmaceutical industry. This has been vital to the successful launch of vaccines and therapies to combat the COVID-19 virus.

According to the Drug, Chemical & Associated Technologies Association Inc. (DCAT) Value Chain Insights on "Mid-Year CDMO Review: COVID-19 Vaccine Manufacturing and M&A", in the first months of the pandemic, less than 10 CDMOs were known publicly to be working with the bio/pharma companies and government agencies to develop and manufacture vaccines. Contracts were going to CDMOs that had the accessible capacity or could expand it rapidly, including Catalent and Lonza. CDMOs were engaged in producing the vaccine's active ingredients and key excipients. The demand for vaccine capacity elevated the status and profiles of many CDMOs that were earlier dependent on the older products and generics. Some companies, for instance, Rovi Contract Manufacturing, have got both drug substance and drug product contracts.

Besides, the first half of 2021 also saw a high number of merger and acquisition activities as investors sought to buy their way into the industry and incumbents sought to broaden and deepen their capabilities. A total of 32 deals were announced or closed during the first five months of 2021. Out of these, five deals were for small molecule API businesses and four for large molecule API assets.

Outsourcing to CDMOs can also offer companies access to a flexible workforce, including highly-specialized experts. In recent times, increased outsourcing to CDMOs has been seen for drug owners from pharmaceutical to biopharmaceutical companies, from small to large firms, and for early to late-stage development projects.

The quality of APIs has a noteworthy effect on the efficacy and safety of medications. Hence, selecting a CDMO that can provide the precise API at the required strength, purity, and quality is a vital decision for drug development companies.

Active Pharmaceutical Ingredients CDMO Market Trends

The Commercial Segment is Expected to Hold the Major Market Share

The COVID-19 pandemic led to an increase in the demand for pharmaceutical products, and the hoarding of supplies by some nations in the wake of production disruptions boosted exports. When COVID-19 cases rapidly increased, there was a need for new COVID-19 vaccines and therapeutics. Some governments even started considering localization regulations to ensure that sufficient quantities of therapeutics would be produced domestically.

As a result, many pharmaceutical companies started expanding their manufacturing footprint, and some began to rethink their manufacturing footprint to plan for the years ahead. The largest source of additional capacity was CDMOs.

Additionally, pharmaceutical firms reserved and sometimes even double-booked a considerable space with the contract manufacturers. AstraZeneca, Moderna, and Pfizer have declared their partnership agreements with a number of CDMOs, including Lonza, Catalent, and Emergent Biosolutions. Making the most of the opportunity, Cambrex, Catalent, Samsung Biologics, and many other developing country CDMOs have declared a major expansion of their plants.

Asia-Pacific is Expected to Hold a Significant Share in the Market during the Forecast Period

China and India have a significantly low cost of manufacturing compared to the United States and Europe. As per Invest India, the cost of manufacturing in India is approximately 33% lower than that of the United States. While China and India have established themselves as significant providers of API manufacturing services, the United States continues to be the main outsourcing hub for pharmaceutical development. This is due to the combination of enormous amounts of financing and an exclusive concentration of university-affiliated pharmaceutical research hubs.

The expanding importance of traditional pharmaceuticals and the rapidly rising incidence of persistent infections are critical drivers of the Indian API CDMO market's favorable growth. As per an article published in PHRMABIZ.com in 2020, generic APIs are exported to developed countries from India, accounting for 41.6% of the total sales in India versus 24.7% in China. As per the Chemical Pharmaceutical Generic Association Research, India is the second-largest provider of generic API to the US market, with a 24.4% share. The country is also increasing its supply to Western Europe, which accounts for 19.2% of the region's total supply. Also, China accounts for 30% of the global nonexclusive API vendor market. Following China, the United States and India are the leading producers of nonexclusive APIs.

Active Pharmaceutical Ingredients CDMO Industry Overview

The active pharmaceutical ingredients CDMO market is fragmented and consists of several major players. In terms of market share, a few major players dominate the market. A few of them are Cambrex Corporation, Patheon (Themo Fisher Scientific Inc.), Recipharm AB, CordenPharma International, Samsung Biologics, Lonza, Siegfried, Piramal Pharma Solutions, Abbvie Inc., and Catalent Inc.

The role of API manufacturers in the pharmaceutical supply chain is evolving in response to the newfound demands from customers and increasing pressures from global competitors. Traditional generic firms are looking to China and India for bulk activities, while specialty pharmaceutical companies have generated new demands for more specialized capabilities than those required by traditional generics.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Pharmaceutical R&D Investment

- 4.2.2 Rising Demand for Generic Drugs

- 4.2.3 Complex Manufacturing

- 4.2.4 Patent Expiration

- 4.3 Market Restraints

- 4.3.1 Compliance Issues while Outsourcing

- 4.3.2 Concerns about Data Quality and Security

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Molecule Type

- 5.1.1 Small Molecule

- 5.1.2 Large Molecule

- 5.2 By Synthesis

- 5.2.1 Biotech

- 5.2.2 Synthetic

- 5.3 By Drug Type

- 5.3.1 Innovative

- 5.3.2 Generics

- 5.4 By Workflow

- 5.4.1 Clinical

- 5.4.2 Commercial

- 5.5 By Application

- 5.5.1 Cardiology

- 5.5.2 Oncology

- 5.5.3 Ophthalmology

- 5.5.4 Neurology

- 5.5.5 Orthopedic

- 5.5.6 Other Applications

- 5.6 Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East & Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East & Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Cambrex Corporation

- 6.1.2 Patheon (Thermo Fisher Scientific Inc.)

- 6.1.3 Recipharm AB

- 6.1.4 CordenPharma International

- 6.1.5 Samsung Biologics

- 6.1.6 Lonza

- 6.1.7 Siegfried

- 6.1.8 Piramal Pharma Solutions

- 6.1.9 AbbVie Inc.

- 6.1.10 Catalent Inc.