|

시장보고서

상품코드

1693597

핵산 기반 치료 시장 : 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Nucleic Acid Based Therapeutics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

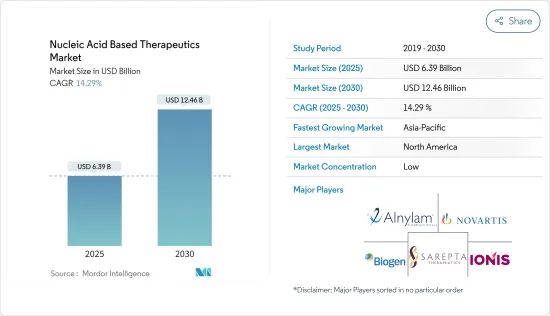

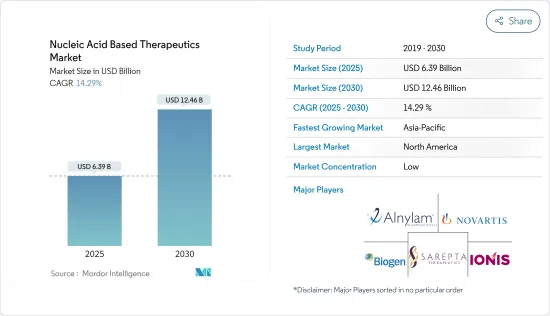

세계의 핵산 기반 치료 시장 규모는 2025년 63억 9,000만 달러로 추정되며, 예측 기간 중(2025-2030년) CAGR 14.29%로, 2030년에는 124억 6,000만 달러에 달할 것으로 예측됩니다.

핵산 기반 치료는 COVID-19 질병 치료의 개발에 효과적으로 사용되었기 때문에 지난 2년간 수요가 증가했습니다. COVID-19 바이러스에 대항하기 위해 가장 유망한 것은, 저분자 간섭 RNA(siRNA), 안티센스 올리고뉴클레오티드(ASO), 마이크로RNA(miRNA)를 포함한 핵산 기반 기술이었습니다. MDPI에 게재된 기사에 따르면, 2022년 8월, 세계 전체에서 400이상의 RNA 표적 의약품 개발 프로젝트가 실시되어, 그 3분의 2가 임험 전 신약(pre-IND) 단계, 3분의 1이 초기 임상 검사(제 I상 또는 II상) 단계, 약 3%가 제III상 단계에 있으며, 일부는 COVID-19 치료로 규제 당국의 승인을 기다리고 있습니다.

유전성 질환의 급증, 의료 부문 투자 증가, 혁신적인 생물학적 제제로의 제약 산업의 급속한 변화 등의 요인이 예측 기간 동안 시장 성장을 가속할 것으로 예측됩니다.

암, 낭포성 섬유증, 겸상 적혈구 빈혈, 두첸느형 근이영양증, 사라세미아 등 유전성 질환의 유병률 증가는 특정 유전자의 이상 발현을 수정함으로써 질병을 치료하는 핵산 기반 치료에 대한 수요를 촉진하는 주요인입니다. 예를 들어, 낭포성 섬유증재단이 2022년 7월 발표한 데이터에 따르면 미국에서는 4만 명의 유아와 성인이 낭포성 섬유증(CF)을 앓고 있습니다. 같은 데이터에 따르면 2022년에는 94개국에서 추정 105,000명이 이 질병으로 진단되었습니다.

만성 질환, 유전성 질환 및 기타 질병의 유병률 증가로 인한 핵산 치료에 대한 투자 건수 증가는 시장 성장을 증가시킬 것으로 예측됩니다. 2023년 3월, Switch Therapeutics는 Insight Partners와 UCB Ventures가 공동 주도하는 시리즈 A 자금 조달 라운드에서 5,200만 달러를 조달했습니다. 2023년 1월, Agilent Technologies Inc.는 핵산 기반 치료에 7억 2,500만 달러를 투자했습니다.

기업의 공동 연구, 제휴, 신제품의 상시, 기타 대처에 대한 주목의 고조는 시장에서의 신규 치료의 가용성을 높여 시장의 성장을 가속할 가능성이 있습니다. 2023년 2월, CMT 연구재단은 Nanite Inc.와 협력하여 2022년 10월 Neuway Pharma GmbH와 Wacker는 EnPC(Engineered Protein Capsules) 단백질 기반 약물전달 기술을 사용하여 중추 신경계 질환 치료를 위한 RNA 기반 치료를 확인하고 제조하는 연구 프로젝트를 시작했습니다.

그 때문에 유전성 질환의 부담이 큰 것, 투자가 증가하고 있는 것, 신제품이 상시되고 있는 것 등으로부터, 예측 기간 중에 시장은 성장할 것으로 전망되고 있습니다. 그러나, 핵산 기반의 치료의 조사 비용이 높은 것이, 시장의 성장을 저해할 가능성이 높습니다.

핵산 기반 치료 시장 동향

안티센스 올리고뉴클레오티드(ASO) 분절은 예측 기간 동안 상당한 성장이 예상된다.

안티센스 올리고뉴클레오티드(ASOs)는 특정 메신저 RNA(mRNA) 서열에 결합할 수 있는 짧은 단일 가닥 DNA 또는 RNA 분자로, 표적 mRNA의 분해 또는 단백질로의 번역의 억제로 이어집니다.

승인된 ASO 치료의 예로는 척수성 근위축증의 치료 Spinraza(누시넬센), 뒤센느형 근이영양증의 치료 Exondys51(에테프릴센), 유전성 트랜스사이레틴 아밀로이드증 치료 Onpattro(파티실란), 유전성 트랜스사이레틴을 통한 아밀로이드증 치료 Tegsedi(이노테르센) 등이 있습니다.

ASOs 부문은 안티센스 올리고뉴클레오티드 의약품에 대한 높은 수요, 주요 기업에 의한 R&D 활동의 활성화, 신제품의 상시 등에 의해 예측 기간 중에 큰 성장이 전망되고 있습니다.

희귀질환과 유전성 질환에 대한 신규 치료의 연구 개발을 가속시키기 위해 제휴, 공동 연구, 인수, 기타 대처 등 다양한 사업 전략을 채용하는 기업의 주목도가 높아지고 있는 것이 같은 부문의 성장을 뒷받침할 것으로 예측됩니다.

안티센스 올리고뉴클레오티드 제제 시장 투입, 기업 활동의 활성화, 신제품의 상시 등에 의해 동 부문은 예측 기간 중에 성장할 것으로 예측됩니다.

예측기간 중 북미가 큰 시장 점유율을 차지할 전망

북미는 다양한 핵산 기반 치료법에 대한 조사 증가, 유전성 질환 및 기타 만성 질환의 유병률 증가, 이 지역의 R&D 투자 증가로 시장에서 큰 점유율을 차지할 것으로 예측됩니다.

인구간에 자가면역질환의 유병률이 상승하고 있기 때문에 핵산기반의 치료에 대한 수요가 높아지고 있어 이것이 시장의 성장을 증대시킬 가능성이 있습니다. Rheumatology Journal에 게재된 기사에 따르면, 캐나다에서는 전신성자가면역성 류마티스 질환(SARDs)의 부담이 크고, 주민 1,000명당 2-5명의 환자가 이환하고 있습니다.

암이 증가함에 따라 암세포의 진행을 억제하는 효과적인 신약 수요가 증가하고 있습니다. Cancer Facts and Figures 2023에 따르면 2023년에는 국내에서 약 190만명이 새롭게 암으로 진단될 것으로 추정되고 있습니다. 캐나다 정부가 2022년 6월 갱신한 통계에 따르면 캐나다에서는 2022년 연말까지 약 23만 3,900명이 암으로 진단되는 것으로 추정되며, 폐암, 유방암, 전립선암, 대장암이 캐나다 대상 인구 중에서 가장 많이 진단되는 암으로 예측되고 있습니다.

혁신적인 제품의 출시 및 승인, 제휴, 인수, 확대, 제휴가 이 지역에서 시장의 성장을 가속할 것으로 예측되고 있습니다. 예를 들어, 2022년 9월 Next Generation Manufacturing Canada(NGen)는 OmniaBio Inc.와 파트너인 ExCellThera, MorphoCell Technologies, Aspect Biosystems, Canadian Advanced Therapies Training Institute(CATTI)가 주도하는 3,480만 달러의 프로젝트에 1,050만 달러의 프로젝트에 투자했습니다. 2021년 12월, NovartisAG는 저비중 리포단백질 콜레스테롤(악옥 콜레스테롤 또는 LDL-C로도 알려져 있음)을 감소시키는 최초의 유일한 siRNA(small interfering RNA) 요법인 Leqvio(잉크비오)에 대해 최초 투여와 3개월 후 1회 투여 후 1년 2회 투여로 FDA 승인을 취득했습니다.

핵산 기반 치료 산업 개요

핵산 기반 치료 시장은 세계 및 지역적으로 많은 대규모 진출기업이 존재하기 때문에 적당히 부문화되어 있습니다. 각 회사는 다양한 만성 질환, 유전성 질환 및 감염성 질환의 치료를 위해 핵산 기반 치료의 연구 개발을 추진하고 있습니다. 이 시장의 주요 기업으로는 Silence Therapeutics PLC, Ionis Pharmaceuticals Inc., Sarepta Therapeutics, Novartis Pharma AG, Alnylam Pharmaceuticals Inc., Biogen Inc. 등이 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 시장 개요

- 시장 성장 촉진요인

- 유전성 질환의 급증

- 의료 부문에 대한 투자 확대

- 혁신적인 생물제제로의 제약산업의 급속한 시프트

- 시장 성장 억제요인

- 높은 핵산 조사 비용

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자/소비자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 세분화

- 제품 유형별

- RNA 간섭(RNAi)과 단쇄 간섭 RNA(siRNA)

- 안티센스 올리고뉴클레오티드(ASOs)

- 기타

- 용도별

- 자가면역질환

- 감염증

- 유전자 질환

- 암

- 기타

- 최종 사용자별

- 병원 및 클리닉

- 학술기관 및 연구기관

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC 국가

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 기업 프로파일

- Silence Therapeutics PLC

- Ionis Pharmaceuticals Inc.

- Novartis Pharma AG

- Arrowhead Pharmaceuticals Inc.

- Stoke Therapeutics Inc.

- Moderna Inc.

- Alnylam Pharmaceuticals Inc.

- Biogen Inc.

- Wave Life Sciences

- Sarepta Therapeutics Inc.

제7장 시장 기회와 앞으로의 동향

JHS 25.05.13The Nucleic Acid Based Therapeutics Market size is estimated at USD 6.39 billion in 2025, and is expected to reach USD 12.46 billion by 2030, at a CAGR of 14.29% during the forecast period (2025-2030).

The demand for nucleic acid-based therapeutics increased over the past two years as they were effectively used to develop COVID-19 disease therapeutics. As per the article published by MDPI in February 2022, nucleic acid-based technologies, including small interfering RNAs (siRNAs), antisense oligonucleotides (ASOs), and micro RNAs (miRNAs), were the most promising ones to combat the COVID-19 virus. These therapeutics can suppress viral gene expression during and after transcription, presenting significant growth opportunities. As per an article published in MDPI, in August 2022, over 400 RNA-targeting drug development projects were conducted globally, two-thirds of which are in the pre-investigational new drug (pre-IND) stage, one-third in early clinical trials (Phase I or II), about 3% in Phase III, and some awaiting regulatory approval for COVID-19 treatment. Thus, with the increasing development of RNA therapeutics, the studied market is expected to grow over the forecast period.

Factors such as the surging prevalence of genetic disease, growing investments in the healthcare sector and rapid shift of the pharmaceutical industry toward innovative biologics are expected to boost the market's growth over the forecast period.

The increasing prevalence of genetic diseases such as cancer, cystic fibrosis, sickle cell anemia, Duchenne muscular dystrophy, thalassemia, and others is the key factor driving the demand for nucleic acid-based therapeutics to treat diseases by correcting the abnormal expression of specific genes. For instance, according to the Cystic Fibrosis Foundation data published in July 2022, in the United States, 40,000 children and adults have cystic fibrosis (CF). As per the same source, an estimated 105,000 people were diagnosed with the disease in 94 countries in 2022. Thus, the high burden of cystic fibrosis among the population is expected to positively impact the market.

The rising number of investments in nucleic acid therapeutics owing to the high prevalence of chronic, genetic, and other diseases is anticipated to augment the market's growth. For instance, in March 2023, Switch Therapeutics raised USD 52 million in a Series A financing round co-led by Insight Partners and UCB Ventures. The company used these funds to select and advance the development of siRNA therapeutic candidates for the treatment of a central nervous system disease, as well as to advance its RNAi technology. Market players are investing in nucleic acid-based therapy R&D to expand the product portfolio in nucleic acid-based therapy. For instance, in January 2023, Agilent Technologies Inc. invested USD 725 million in nucleic acid-based therapeutics. The investment will double the manufacturing capacity to produce active pharmaceutical ingredients (APIs).

Companies' growing focus on collaborations, partnerships, new product launches, and other initiatives increases the availability of novel therapeutic drugs in the market, which may propel the market's growth. For instance, in February 2023, the CMT Research Foundation partnered with Nanite Inc. to enhance the therapeutic efficacy of antisense oligonucleotides in Charcot-Marie-Tooth disease. In October 2022, Neuway Pharma GmbH and Wacker launched a research project to identify and manufacture RNA-based therapeutics for the treatment of central nervous system disorders with the use of EnPC (Engineered Protein Capsules) protein-based drug delivery technology.

Therefore, owing to the high burden of genetic diseases, increasing investments, and new product launches, the market studied is anticipated to grow over the forecast period. However, the high cost of nucleic acid-based therapeutics research is likely to impede the market's growth.

Nucleic Acid-Based Therapeutics Market Trends

Antisense Oligonucleotides (ASOs) Segment is Expected to Witness Significant Growth Over the Forecast Period

Antisense oligonucleotides (ASOs) are short, single-stranded DNA or RNA molecules that can bind to specific messenger RNA (mRNA) sequences, leading to the degradation of the targeted mRNA or inhibition of its translation into protein. This property makes ASOs a promising therapeutic strategy for a variety of diseases, including genetic disorders, infectious diseases, and cancer. These can target specific disease-causing genes, such as those responsible for the production of abnormal proteins or enzymes that contribute to disease progression.

Some examples of approved ASO therapies include Spinraza (nusinersen) for the treatment of spinal muscular atrophy, Exondys51 (eteplirsen) for the treatment of Duchenne muscular dystrophy, Onpattro (patisiran) for the treatment of hereditary transthyretin-mediated amyloidosis, and Tegsedi (inotersen) for the treatment of hereditary transthyretin-mediated amyloidosis.

The ASOs segment is expected to witness significant growth over the forecast period due to the high demand for antisense oligonucleotide drugs, increasing R&D activities by key players, and new product launches.

The increasing focus of the companies to adopt various business strategies such as partnerships, collaborations, acquisitions, and other initiatives to accelerate the R&D of novel therapeutics for rare and genetic disorders is anticipated to fuel the segment's growth. For instance, in September 2022, Vanda Pharmaceuticals Inc. and OliPassCorporation entered an R&D collaboration agreement to jointly develop a set of antisense oligonucleotide (ASO) molecules based on modified peptide nucleic acids. In February 2021, the US FDA approved Sarepta's Amondys 45 (casimersen) injection for the treatment of Duchenne muscular dystrophy (DMD) in patients with a confirmed mutation of the DMD gene.

Therefore, the segment is expected to grow over the forecast period due to the availability of several antisense oligonucleotide products in the market, increasing company activities, and new product launches.

North America is Expected to Have the Significant Market Share Over the Forecast Period

North America is expected to hold a significant share of the market due to the growing research on various nucleic acid-based therapies, the increasing prevalence of genetic disorders and other chronic disorders, and growing R&D investments in the region.

The rising prevalence of autoimmune diseases among the population increases the demand for nucleic acid-based therapies, which may augment the market's growth. For instance, as per the Autoimmune Association in June 2022, autoimmune diseases comprise approximately 80-150 unique, chronic conditions and affect more than 31 million Americans annually. This shows the high burden of autoimmune disorders among the target population. As per an article published in the Clinical Rheumatology Journal in February 2023, the burden of systemic autoimmune rheumatic diseases (SARDs) is large in Canada, affecting between 2 and 5 cases per 1,000 residents.

The increasing burden of cancer raises the demand for effective and novel drugs that inhibit the progression of cancer cells. This fuels the demand for nucleic acid-based drugs in the region. For instance, according to the Cancer Facts and Figures 2023, about 1.9 million new cancer cases are estimated to be diagnosed in the country in 2023. According to the statistics updated by the Government of Canada in June 2022, nearly 233,900 people in Canada were estimated to be diagnosed with cancer by the end of 2022, and lung, breast, prostate, and colorectal cancers were predicted to be the most diagnosed cancers among the target population in Canada.

The innovative product launches and approvals, partnerships, acquisitions, expansions, and collaborations are anticipated to fuel the market's growth in the region. For instance, in September 2022, Next Generation Manufacturing Canada (NGen) invested USD 10.5 million in a USD 34.8 million project led by OmniaBio Inc. and partners ExCellThera, MorphoCell Technologies, Aspect Biosystems, and Canadian Advanced Therapies Training Institute (CATTI). In December 2021, Novartis AG received approval from the FDA for Leqvio (inclisiran), the first and only small interfering RNA (siRNA) therapy to lower low-density lipoprotein cholesterol (also known as bad cholesterol or LDL-C) with two doses a year, after an initial dose and one at three months.

Nucleic Acid-Based Therapeutics Industry Overview

The nucleic acid-based therapeutics market is moderately fragmented due to the presence of many small and large players globally and regionally. The companies are engaging in the research and development of nucleic acid-based therapeutics for the treatment of various chronic, genetic, and infectious diseases. Some of the key companies in the market are Silence Therapeutics PLC, Ionis Pharmaceuticals Inc., Sarepta Therapeutics, Novartis Pharma AG, Alnylam Pharmaceuticals Inc., and Biogen Inc., among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging Prevalence of Genetic Diseases

- 4.2.2 Growing Investments in Healthcare Sector

- 4.2.3 Rapid Shift of the Pharmaceutical Industry Toward Innovative Biologics

- 4.3 Market Restraints

- 4.3.1 High Cost of Nucleic Acid Research

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value in USD million)

- 5.1 By Product Type

- 5.1.1 RNA interference [RNAi] and short interfering RNAs [siRNAs]

- 5.1.2 Antisense Oligonucleotides (ASOs)

- 5.1.3 Other Product Types

- 5.2 By Application

- 5.2.1 Autoimmune Disorders

- 5.2.2 Infectious Diseases

- 5.2.3 Genetic Disorders

- 5.2.4 Cancer

- 5.2.5 Other Applications

- 5.3 By End User

- 5.3.1 Hospitals and Clinics

- 5.3.2 Academic and Research Institutes

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East & Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East & Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Silence Therapeutics PLC

- 6.1.2 Ionis Pharmaceuticals Inc.

- 6.1.3 Novartis Pharma AG

- 6.1.4 Arrowhead Pharmaceuticals Inc.

- 6.1.5 Stoke Therapeutics Inc.

- 6.1.6 Moderna Inc.

- 6.1.7 Alnylam Pharmaceuticals Inc.

- 6.1.8 Biogen Inc.

- 6.1.9 Wave Life Sciences

- 6.1.10 Sarepta Therapeutics Inc.