|

시장보고서

상품코드

1911495

하드 디스크 드라이브(HDD) 시장 : 점유율 분석, 업계 동향, 통계, 성장 예측(2026-2031년)Hard Disk Drive (HDD) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

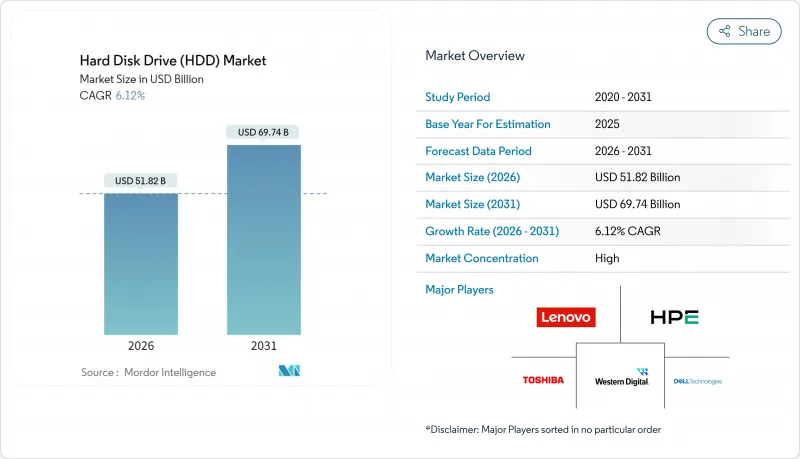

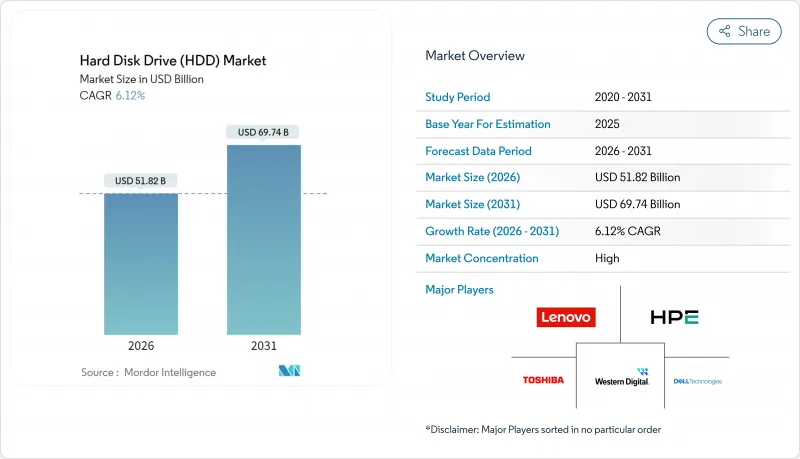

하드디스크 드라이브(HDD) 시장 규모는 2026년에 518억 2,000만 달러로 추정되며, 2025년 488억 3,000만 달러에서 증가한 수치입니다. 2031년에는 697억 4,000만 달러에 이르고, 2026-2031년에 걸친 연평균 복합 성장률(CAGR)은 6.12%를 나타낼 전망입니다.

1테라바이트당 비용 이점, 100TB 이상을 목표로 하는 HAMR 기술을 통한 용량 로드맵, AI 생성으로 인한 콜드 데이터의 급증으로 하드 드라이브는 하이퍼스케일 스토리지 전략의 핵심이 되었습니다. 클라우드 공급자가 2025년 과거 최고가 되는 3,150억 달러의 자본 예산의 약 15-20%를 스토리지 인프라에 할당하는 가운데, 니어라인 엔터프라이즈 도입이 확대되고 있습니다. 한편, 전력 제약이 있는 데이터센터 시장에서는 테라바이트당 에너지 소비 지표가 수요를 지지하고 있습니다. 인터페이스 동향에서는 SATA의 광범위한 도입 기반이 확인되는 반면, 고대역폭이 필수적인 영역에서는 SAS와 신규의 NVMe 패스웨이가 기세를 늘리고 있습니다. 공급 역학은 여전히 섬세한 상황입니다. 3개공급업체가 거의 모든 생산량을 지배하기 때문에 무역 마찰에서 자연 재해에 이르는 모든 혼란이 하드 디스크 드라이브(HDD) 시장에 빠르게 파급되기 때문입니다(WESTERN DIGITAL.COM). 동시에 아시아태평양과 북미의 제조 우대책이 생산 거점의 재편을 촉구하고 미션 크리티컬한 기업용 수주의 최종 조립 프로세스에 있어서의 니어 쇼어링을 뒷받침하고 있습니다.

세계 HDD 시장 동향과 인사이트

하이퍼스케일 및 클라우드 스토리지 용량에 대한 수요 증가

하이퍼스케일 데이터센터의 수는 2024년 말 1,136곳에 이르렀으며, AI 가속기가 컴퓨팅 발자국을 재구축하는 동안 2030년까지 3배로 증가할 것으로 예측됩니다. 주요 클라우드 사업자의 2025년 설비 투자 계획의 약 5분의 1을 스토리지가 차지하고, 초대용량 랙에 수십억 달러가 투입될 전망입니다. 이로 인해 콜드 티어 배포를 위한 HDD(Hard Disk Drive) 시장이 우수합니다. 웨스턴 디지털사는 주로 HAMR 기술에 의한 밀도 향상을 원동력으로 2024-2028년에 걸쳐 HDD의 엑사바이트 출하량이 23% 증가할 것으로 예측했습니다. 미국은 하이퍼스케일 용량의 54%를 차지하고 있지만, 현지 전력 제약으로 인해 와트/테라바이트 성능이 뛰어난 드라이브가 평가되고 있습니다. 분산 아키텍처는 컴퓨팅과 스토리지를 분리하고 HDD가 방대한 콜드 데이터 풀을 처리하는 반면, SSD는 핫 데이터 액세스를 관리하는 시스템을 갖추고 있습니다.

니어 라인 워크로드에서 SSD에 대한 비용/TB 이점

씨게이트는 2024 회계연도에 출하한 398엑사바이트에서 테라바이트당 15달러를 달성했다고 보고하고 있으며 엔터프라이즈용 SSD와의 비용차는 약 2.5배를 유지하고 있습니다. 30TB 용량 포인트에서는 가격 차이가 약 3-4배로 확대되어, 비용 중시의 콜드 데이터층에 있어서의 하드 디스크 드라이브(HDD) 시장의 우위성을 강화하고 있습니다. 플래시 제조업체는 3D NAND의 미세화에 의해 테라바이트당 비용을 계속 저감하고 있습니다만, 내구성과 기입 비용의 제약에 의해 순차 처리가 중심의 워크로드에서는 드라이브의 총 소유 비용(TCO)이 여전히 유리합니다. 기업 구매자는 지출 및 서비스 수준 목표를 최적화하기 위해 고성능 SSD 계층 구조와 대규모 HDD 용량 풀을 결합한 하이브리드 전략을 점점 더 명확하게 내세우고 있습니다.

SSD의 1TB 당 비용의 급격한 저하와 엔터프라이즈 플래시의 TCO 이점

플래시 벤더는 현재 232층 3D NAND를 생산하고 있으며 분기별로 비트당 비용을 인하하고 있습니다. 퓨어 스토리지의 하이퍼스케일러용 설계 채택 사례는 전력,냉각 및 설치 면적의 절약 효과를 종합적으로 고려한 경우 플래시가 압도적인 총 비용 우위성을 실현하는 시나리오를 나타내고 있습니다. 61.44TB 엔터프라이즈 SSD의 출현은 높은 가격이지만 용량 수렴의 징후를 보여줍니다. QLC NAND는 추가 비트당 비용 절감을 약속하지만 내구성 제약으로 인해 이러한 제품은 읽기 중심 워크로드로 제한됩니다. 엔터프라이즈 바이어가 종합적인 조달 관점을 통합하는 동안 HDD는 플래시가 비용 차이를 줄이는 속도를 초과하는 속도로 용량을 계속 향상시켜야합니다.

부문 분석

3.5인치 제품은 2025년 매출액의 65.62%를 차지했고, 2031년까지 연평균 복합 성장률(CAGR) 9.29%로 하드디스크 드라이브(HDD) 시장 전체를 웃도는 성장이 전망됩니다. 대용량 플래터는 우수한 랙당 기가바이트 효율을 실현하고 바닥 면적을 평방 피트당 수천 달러로 평가하는 하이퍼스케일 사업자에게 매우 중요합니다. 3.5인치 제품의 하드디스크 드라이브(HDD) 시장 규모는 2031년까지 452억 달러 이상에 달할 것으로 예측됩니다. HAMR(마그네틱 히트 회전 기록)과 UltraSMR(초밀 기록 기술)의 진보로 벤더는 동일한 케이스에서 40TB를 실현하는 로드맵을 책정 가능하게 되어, 이 부문의 규모의 경제성을 강화하고 있습니다.

소형 2.5인치 드라이브는 노트북과 소형 서버용이지만 SSD에 대한 대안이 진행되고 있으며 성장 전망은 제한적입니다. 1.8인치 이하의 폼 팩터는 틈새 가전 및 산업 장비에 채택됩니다. 3.5인치 플랫폼을 기반으로 하는 고밀도 JBOD 섀시는 적은 스핀들 수로 엑사바이트 규모의 목표를 달성할 수 있으므로 콜드 티어 아키텍처에서 비용 우위를 유지하고 있습니다. Seagate가 최근 일본에서 발표한 20TB와 24TB의 BarraCuda SKU는 소비자를 위한 가격으로 대용량 3.5인치 로드맵에 대한 지속적인 투자를 강조합니다.

니어라인 엔터프라이즈 환경은 2025년 출하량의 44.10%를 차지했고 주요 워크로드 중에서 가장 빠른 CAGR 9.52%로 성장할 전망입니다. 클라우드 아키텍트는 확장되는 AI 교육 세트를 저비용 고밀도 계층에 집계하여 페타바이트 규모 클러스터의 핵심으로 HDD 시장을 유지합니다. 니어라인 용도에서 HDD 시장 점유율은 McKinsey가 예측하는 콜드 데이터의 급증으로 혜택을 받으며, 이는 드라이브의 순차 쓰기 성능과 경제적인 저장 특성과 일치합니다.

소비자용 데스크톱과 게이밍 PC는 꾸준히 SSD로 이동하고 있으며, 1TB 이하의 엔트리 드라이브에 대한 유닛 수요는 감소 경향이 있습니다. 모니터링 어레이 및 NAS 디바이스는 기록 패턴과 용량 요구가 자기 매체에 적합하기 때문에 견고함을 유지합니다. 엔터프라이즈 데이터센터 팀은 SSD와 HDD가 공존하는 분산형 모델을 계속 채택하고 있지만, 니어라인 레이어는 향후 10년간 절대적인 엑사바이트 성장량이 가장 큰 레이어가 됩니다.

지역별 분석

아시아태평양은 2025년 세계 수익의 36.10%를 차지했고 2031년까지 연평균 복합 성장률(CAGR) 6.84%로 성장할 전망입니다. 중국과 일본은 하이퍼스케일 확대와 국내 OEM 출하로 지역 수요를 지원하고 태국은 2024년 8월 승인된 웨스턴 디지털사에 의한 6억 9,300만 달러의 확대 계획을 통해 제조 거점으로서의 지위를 유지하고 있습니다. 인도 소매용 드라이브 출하량은 전자상거래와 재택근무 동향이 지속됨에 따라 2024년 2분기에 전기 대비 12% 증가했습니다. 말레이시아의 170억 달러 규모의 데이터센터 모니터링 프로그램을 포함한 동남아시아 전역의 스마트 시티 예산이 지역의 엑사바이트 수요를 가속화하고 있습니다.

북미는 두 번째 주요 지역이며, 설치된 클라우드 용량의 54%를 차지하는 미국의 하이퍼스케일 사업자에 의해 견인되고 있습니다. 무역 시책의 역풍으로 인해 비용 불확실성이 발생하고 있지만, 제안된 우대 조치는 공급망 단축으로 이어지는 국내 조립을 촉진할 수 있습니다. 버지니아의 데이터센터 회랑 주변에서 증가하는 전력망의 제약으로 인해 설계자는 와트/테라바이트 효율을 강조하고 올플래시 어레이보다 하드 디스크 드라이브(HDD) 시장을 선호합니다. 캐나다와 멕시코는 토지, 재생 가능 전력, 월경 물류에 대한 우위를 제공함으로써 지원적인 역할을 수행합니다.

유럽에서는 엄격한 데이터 주권 규제 하에서 기업을 위한 교체 주기를 안정적으로 유지하고 있습니다. 독일과 영국은 컴플라이언스 보유 기간 대응을 위해 콜드 티어 클러스터를 도입하고 프랑스는 공공 부문의 클라우드 워크로드를 확대하고 있습니다. 이 지역의 순환형 경제에 대한 주력은 벤더의 재활용 프로그램과 연동하고 있으며, 예를 들어 웨스턴 디지털사는 2024년에 폐기 드라이브 5만 파운드에서 희토류 원소를 회수했습니다. 장기 탄소세 논의는 기록기술 선택에 영향을 미칠 수 있습니다. HDD 제조업체는 경쟁 스토리지 미디어보다 라이프사이클 CO2 배출량이 낮음을 나타냅니다.

기타 혜택

- 엑셀 형태 시장 예측(ME) 시트

- 애널리스트 서포트(3개월간)

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 하이퍼스케일 및 클라우드 스토리지 용량에 대한 수요 증가

- 근거리 워크로드에서 SSD보다 비용 대비 TB 우위성

- 스마트 시티 전개에 수반하는 비디오 모니터링 데이터 증가

- AI 구동형 콜드 데이터 계층화의 도입

- 대용량 HAMR 로드맵(50TB 드라이브까지)

- 순환형 경제 리사이클 프로그램에 의한 부품 원가(BOM) 절감

- 시장 성장 억제요인

- SSD의 $/TB의 급격한 저하와 엔터프라이즈 플래시의 TCO 개선

- 공급자의 극단적인 집중과 공급망의 혼란

- 에너지 집약형 HDD 생산에 대한 잠재적 탄소세

- 플래시 기반 아키텍처를 선호하는 랙 밀도 한계

- 가치/공급망 분석

- 규제 상황

- 기술 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

- 거시 경제적 영향 평가

제5장 시장 규모와 성장 예측

- 폼 팩터별

- 2.5인치

- 3.5인치

- 기타(1.8인치 이하, 엔터프라이즈 JBOD)

- 용도별

- 모바일 / 휴대용

- 소비자 데스크톱과 게임

- NAS와 SOHO

- 엔터프라이즈 및 데이터센터

- 니어라인 / 콜드 데이터

- 감시 및 스마트 시티

- 스토리지 용량별

- 1TB 미만

- 1-3TB

- 3-5TB

- 5TB 초과

- 인터페이스별

- SATA

- SAS

- PCIe/NVMe(U.2, U.3)

- 최종 사용자 산업별

- IT 및 통신

- 가전 제조업체

- 클라우드 및 하이퍼스케일 제공업체

- 산업용 및 비디오 모니터링

- 정부 및 방위

- 기록기술별

- CMR/PMR

- SMR

- HAMR 및 에너지 보조

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 기타 중동

- 아프리카

- 남아프리카

- 이집트

- 기타 아프리카

- 중동

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Western Digital Corporation

- Toshiba Electronic Devices & Storage Corporation

- Hewlett Packard Enterprise Company

- Dell Technologies Inc.

- Lenovo Group Limited

- Huawei Technologies Co., Ltd.

- Transcend Information Inc.

- ADATA Technology Co., Ltd.

- Buffalo Inc.

- Nidec Corporation

- Showa Denko KK

- Hoya Corporation

- NetApp Inc.

- Pure Storage Inc.

- Samsung Electronics Co., Ltd.(external HDD brand)

- Micron Technology Inc.(external storage systems)

- Violin Systems LLC

- Synology Inc.

- QNAP Systems Inc.

- LaCie SAS(Seagate brand)

제7장 시장 기회와 장래의 전망

SHW 26.02.05Hard Disk Drive market size in 2026 is estimated at USD 51.82 billion, growing from 2025 value of USD 48.83 billion with 2031 projections showing USD 69.74 billion, growing at 6.12% CAGR over 2026-2031.

Cost-per-terabyte advantages, HAMR-driven capacity roadmaps that point to 100 TB and beyond, and the explosion of AI-generated cold data keep hard drives central to hyperscale storage strategies. Near-line enterprise deployments expand as cloud providers allocate roughly 15-20% of their record USD 315 billion 2025 capital budgets to storage infrastructure, while energy-per-terabyte metrics sustain demand in power-constrained data-center markets. Interface trends reveal SATA's broad installed base, yet SAS and emerging NVMe pathways gain momentum where higher bandwidth is essential. Supply dynamics remain delicate because three suppliers control nearly all output; any disruption, from trade friction to natural disasters, propagates quickly through the Hard Disk Drive market [WESTERN DIGITAL.COM]. At the same time, regional manufacturing incentives in Asia-Pacific and North America are rewriting production footprints and favoring near-shoring of final assembly for mission-critical enterprise orders.

Global Hard Disk Drive (HDD) Market Trends and Insights

Rising Demand for Hyperscale and Cloud Storage Capacity

Hyperscale data-center count reached 1,136 at year-end 2024 and is projected to triple by 2030 as AI accelerators reshape computing footprints. Storage represents roughly one-fifth of the 2025 capex plans of major cloud operators, channeling billions into very-large-capacity racks that favor the Hard Disk Drive market for cold-tier deployments. Exabyte shipments of HDDs are forecast by Western Digital to grow at 23% between 2024 and 2028, driven primarily by HAMR-enabled density gains. The United States holds 54% of installed hyperscale capacity, yet local power constraints reward drives that deliver superior watts-per-terabyte performance. Disaggregated architectures now separate compute from storage, letting HDDs handle vast cold data pools while SSDs manage hot data access.

Cost/TB Advantage Over SSDs in Near-line Workloads

Seagate reported achieving USD 15 per terabyte across 398 exabytes shipped in fiscal 2024, preserving an estimated 2.5X cost gap against enterprise SSDs. At 30 TB capacity points, the price delta widens to roughly 3-4X, reinforcing the Hard Disk Drive market in cost-sensitive cold-data tiers. Flash manufacturers continue lowering dollars-per-terabyte through 3D NAND scaling, yet endurance and write-cost constraints keep total-cost-of-ownership favorable to drives for sequential-heavy workloads. Enterprise buyers increasingly articulate hybrid strategies that blend high-performance SSD tiers with large pools of HDD capacity to optimize spend and service-level objectives.

Rapid SSD $/TB Declines and Enterprise Flash TCO Gains

Flash vendors now produce 232-layer 3D NAND, pushing bit costs lower each quarter. Pure Storage's design wins at hyperscalers highlight scenarios where flash achieves compelling total cost when energy, cooling, and floor space savings are lumped into the equation. The arrival of 61.44 TB enterprise SSDs signals capacity convergence, albeit at a premium price. QLC NAND promises further dollar-per-bit gains, yet endurance constraints confine such products to read-heavy workloads. As corporate buyers increasingly adopt a holistic procurement lens, HDDs must continue to elevate capacity faster than flash narrows its cost gap.

Other drivers and restraints analyzed in the detailed report include:

- Growth of Video-Surveillance Data for Smart-City Roll-outs

- AI-Driven Cold-Data Tiering Adoption

- Extreme Supplier Concentration and Supply-Chain Shocks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

3.5-inch units delivered 65.62% revenue in 2025, outpacing the overall Hard Disk Drive market with a 9.29% CAGR to 2031. Their large platters enable superior gigabytes-per-rack metrics, critical for hyperscale operators that price floor space in thousands of dollars per square foot. The Hard Disk Drive market size for 3.5-inch products is projected to eclipse USD 45.2 billion by 2031. HAMR and UltraSMR advances let vendors roadmap 40 TB on the same envelope, reinforcing the segment's scale economics.

Smaller 2.5-inch drives cater to notebooks and compact servers but face SSD substitution, limiting growth prospects. Sub-1.8-inch form factors occupy niche consumer electronics and industrial gear. High-density JBOD chassis relying on 3.5-inch platforms retain cost leadership in cold-tier architectures because fewer spindles meet exabyte targets. Seagate's recent Japan launch of 20 TB and 24 TB BarraCuda SKUs at consumer-friendly pricing underscores continued investment in the high-capacity 3.5-inch roadmap.

Near-line enterprise environments garnered 44.10% of 2025 shipments and will grow at a 9.52% CAGR, the fastest among major workloads. Cloud architects funnel expanding AI training sets onto low-cost, high-density tiers, keeping the Hard Disk Drive market central to petabyte-scale clusters. The Hard Disk Drive market share for near-line roles benefits from the cold-data swell forecast by McKinsey, which aligns with drives' sequential write and economical retention strengths.

Consumer desktop and gaming PCs move steadily to SSD, trimming unit demand for entry drives below 1 TB. Surveillance arrays and NAS devices remain resilient because write patterns and capacity needs suit magnetic media. Enterprise data-center teams continue adopting disaggregated models where SSD and HDD coexist, but the near-line layer commands the highest absolute exabyte growth through the decade.

The Hard Disk Drive Market Report is Segmented by Form Factor (2. 5-Inch, 3. 5-Inch, Others), Application (Mobile/Portable, Consumer Desktop and Gaming, and More), Storage Capacity (<1TB, 1-3TB, 3-5TB, >5TB), Interface (SATA, SAS, PCIe/NVMe), End-User Industry (IT and Telecommunications, and More), Recording Technology (CMR/PMR, SMR, HAMR and Energy-Assisted), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific commanded 36.10% of global revenue in 2025 and is growing at a 6.84% CAGR through 2031. China and Japan anchor regional demand through hyperscale build-outs and domestic OEM shipments, while Thailand continues as a manufacturing hub with Western Digital's USD 693 million expansion approved in August 2024. India's retail drive volumes expanded 12% quarter-over-quarter in Q2 2024 as e-commerce and home-office trends persisted. Smart-city budgets across Southeast Asia, including Malaysia's USD 17 billion data-center and surveillance programs, intensify regional exabyte uptake.

North America is the second-largest territory, propelled by U.S. hyperscale operators that hold 54% of installed cloud capacity. Trade-policy headwinds inject cost uncertainty, though proposed incentives encourage domestic assembly that could shorten supply chains. Growing power-grid constraints around Virginia's data-center corridor steer architects toward watts-per-terabyte efficiencies that favor the Hard Disk Drive market versus all-flash arrays. Canada and Mexico play supportive roles by providing land, renewable electricity, and cross-border logistics advantages.

Europe maintains consistent enterprise replacement cycles amid stringent data-sovereignty mandates. Germany and the United Kingdom deploy cold-tier clusters to meet compliance retention windows, while France expands public-sector cloud workloads. The region's circular-economy focus dovetails with vendor recycling programs, such as Western Digital's recovery of rare-earth elements from 50,000 pounds of retired drives in 2024. Long-term carbon tax discussions may influence recording-technology choices as HDD makers showcase lower lifecycle CO2 than competing storage media.

- Western Digital Corporation

- Toshiba Electronic Devices & Storage Corporation

- Hewlett Packard Enterprise Company

- Dell Technologies Inc.

- Lenovo Group Limited

- Huawei Technologies Co., Ltd.

- Transcend Information Inc.

- ADATA Technology Co., Ltd.

- Buffalo Inc.

- Nidec Corporation

- Showa Denko K.K.

- Hoya Corporation

- NetApp Inc.

- Pure Storage Inc.

- Samsung Electronics Co., Ltd. (external HDD brand)

- Micron Technology Inc. (external storage systems)

- Violin Systems LLC

- Synology Inc.

- QNAP Systems Inc.

- LaCie S.A.S. (Seagate brand)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand for hyperscale and cloud storage capacity

- 4.2.2 Cost/TB advantage over SSDs in near-line workloads

- 4.2.3 Growth of video-surveillance data for smart-city roll-outs

- 4.2.4 AI-driven cold-data tiering adoption

- 4.2.5 Large-capacity HAMR roadmap up to 50 TB drives

- 4.2.6 Circular-economy recycling programs lowering BOM costs

- 4.3 Market Restraints

- 4.3.1 Rapid SSD $/TB declines and enterprise flash TCO gains

- 4.3.2 Extreme supplier concentration and supply-chain shocks

- 4.3.3 Prospective carbon taxes on energy-intensive HDD output

- 4.3.4 Rack-density limits favouring flash-based architectures

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Macroeconomic Impact Assessment

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Form Factor

- 5.1.1 2.5-inch

- 5.1.2 3.5-inch

- 5.1.3 Others (<1.8-inch, Enterprise JBOD)

- 5.2 By Application

- 5.2.1 Mobile/Portable

- 5.2.2 Consumer Desktop and Gaming

- 5.2.3 NAS and SOHO

- 5.2.4 Enterprise and Data-Center

- 5.2.5 Near-line / Cold-Data

- 5.2.6 Surveillance and Smart-City

- 5.3 By Storage Capacity

- 5.3.1 <1 TB

- 5.3.2 1 - 3 TB

- 5.3.3 3 - 5 TB

- 5.3.4 >5 TB

- 5.4 By Interface

- 5.4.1 SATA

- 5.4.2 SAS

- 5.4.3 PCIe / NVMe (U.2, U.3)

- 5.5 By End-User Industry

- 5.5.1 IT and Telecommunications

- 5.5.2 Consumer Electronics OEMs

- 5.5.3 Cloud and Hyperscale Providers

- 5.5.4 Industrial and Video-Surveillance

- 5.5.5 Government and Defence

- 5.6 By Recording Technology

- 5.6.1 CMR / PMR

- 5.6.2 SMR

- 5.6.3 HAMR and Energy-Assisted

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 Europe

- 5.7.2.1 Germany

- 5.7.2.2 United Kingdom

- 5.7.2.3 France

- 5.7.2.4 Russia

- 5.7.2.5 Rest of Europe

- 5.7.3 Asia-Pacific

- 5.7.3.1 China

- 5.7.3.2 Japan

- 5.7.3.3 India

- 5.7.3.4 South Korea

- 5.7.3.5 Australia

- 5.7.3.6 Rest of Asia-Pacific

- 5.7.4 Middle East and Africa

- 5.7.4.1 Middle East

- 5.7.4.1.1 Saudi Arabia

- 5.7.4.1.2 United Arab Emirates

- 5.7.4.1.3 Rest of Middle East

- 5.7.4.2 Africa

- 5.7.4.2.1 South Africa

- 5.7.4.2.2 Egypt

- 5.7.4.2.3 Rest of Africa

- 5.7.4.1 Middle East

- 5.7.5 South America

- 5.7.5.1 Brazil

- 5.7.5.2 Argentina

- 5.7.5.3 Rest of South America

- 5.7.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Western Digital Corporation

- 6.4.2 Toshiba Electronic Devices & Storage Corporation

- 6.4.3 Hewlett Packard Enterprise Company

- 6.4.4 Dell Technologies Inc.

- 6.4.5 Lenovo Group Limited

- 6.4.6 Huawei Technologies Co., Ltd.

- 6.4.7 Transcend Information Inc.

- 6.4.8 ADATA Technology Co., Ltd.

- 6.4.9 Buffalo Inc.

- 6.4.10 Nidec Corporation

- 6.4.11 Showa Denko K.K.

- 6.4.12 Hoya Corporation

- 6.4.13 NetApp Inc.

- 6.4.14 Pure Storage Inc.

- 6.4.15 Samsung Electronics Co., Ltd. (external HDD brand)

- 6.4.16 Micron Technology Inc. (external storage systems)

- 6.4.17 Violin Systems LLC

- 6.4.18 Synology Inc.

- 6.4.19 QNAP Systems Inc.

- 6.4.20 LaCie S.A.S. (Seagate brand)

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment