|

시장보고서

상품코드

1519933

중력 다이캐스팅 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2024-2029년)Gravity Die Casting - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

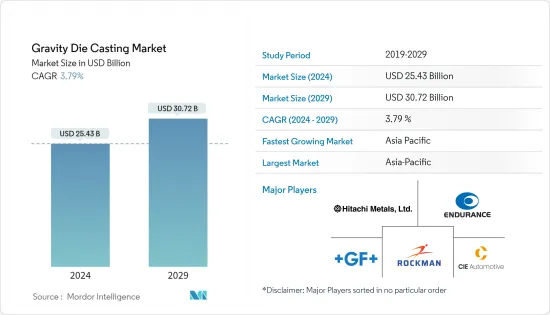

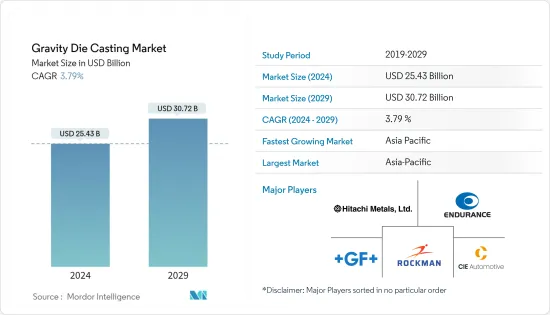

중력 다이캐스팅 시장 규모는 2024년 254억 3,000만 달러, 2029년에는 307억 2,000만 달러에 달할 것으로 예상되며, 예측 기간(2024-2029) 동안 3.79%의 연평균 복합 성장률(CAGR)을 나타낼 전망입니다.

중력 다이캐스팅은 가장 오래된 다이캐스팅 주조 방법 중 하나입니다. 이 다이캐스팅 주조 방법은 정확한 치수, 미세한 모양, 매끄러운 표면 또는 질감이있는 표면의 금속 부품을 만드는 데 사용됩니다. 중력 다이캐스팅의 기본 장점은 빠른 생산 속도입니다. 재사용 가능한 금형을 사용하면 하루에 수백 개의 주물을 생산할 수 있습니다. 고화질 부품은 가공 비용을 절감하고 높은 표면 마감은 마감 비용을 절감합니다.

높은 열전도율로 인해 예측 기간 동안 전기 및 전자 산업에서 알루미늄 다이캐스팅 부품에 대한 수요가 증가 할 가능성이 높습니다. 다이캐스팅 기계는 자동차 산업이 경량 금속을 선호하고 자동차 판매량이 증가함에 따라 수요가 증가하고 있습니다.

장기적으로 재생에너지 발전 시장 개척과 가전, 컴퓨터, 통신 산업의 급속한 확장으로 인해 시장은 혜택을 받을 것으로 예상됩니다.

신기술의 발전에 따라 자동차 부품은 최근 몇 년동안 발전과 혁신을 거듭하고 있습니다. 그 중에서도 경량 소재를 사용한 자동차 부품 제조는 전국적으로 주목을 받고 있습니다. 또한 CAFE 기준과 미국 환경보호청(EPA)의 자동차 배기가스 저감 및 연비 향상 정책으로 인해 자동차 제조업체들은 경량 비철금속을 사용하여 차량 경량화를 추구하고 있습니다. 그 결과, 경량화를 위한 다이캐스팅 부품의 사용으로 과거 자동차 시장은 큰 활기를 띠고 있습니다.

중력 다이캐스팅 시장 동향

자동차 산업이 주요 시장 점유율을 차지할 것으로 예상

중력 다이캐스팅은 일부 고정밀 자동차 부품을 제조하는 표준 공정입니다. 이 공정은 영구 금형에서 용융물이 빠르고 방향성 있게 경화되어 매력적인 기계적 특성을 가진 미세하고 조밀한 구조를 생성하기 때문에 엔진 관련 부품과 같은 부품에 이상적입니다.

그러나 내연기관에서 전기자동차와 같은 대체 엔진으로 전환하는 추세는 다이캐스팅 부품 수요에 불가피한 영향을 미치고 있습니다. 예를 들어, 내연기관에는 약 200개의 주조 부품이 있지만, 전기 구동 시스템에 필요한 주조 부품은 약 25개, 즉 10분의 1에 불과합니다.

탄소 배출량 감소, 자동차 경량화를 촉진하는 정부의 이니셔티브, 자동차 다이캐스팅 기계의 급속한 기술 개발 등의 요인이 시장 수요를 증가시킬 것으로 예상됩니다.

생태학적 및 경제적 요구사항에 힘입어 세계 자동차 산업은 구조용 다이캐스팅 부품이 자동차의 무게를 크게 줄이는 데 도움이 되는 새로운 차체 일체형 디자인을 개발하고 있습니다. 또한 다이캐스팅 구조 부품의 생산은 주물에 기능적 통합, 새로운 알루미늄 합금 개념 및 새로운 부품 설계 트렌드로 인해 더욱 증가하고 있습니다. 또한, 승용차뿐만 아니라 상용차 판매량도 증가하고 있으며, 이는 시장 성장을 뒷받침할 것으로 예상됩니다.

자동차 산업은 전 세계에서 사용되는 주조 제품의 60% 이상을 소비하고 있습니다. 따라서 자동차 및 운송 산업과 관련된 성장 기회를 고려하여 이 시장의 여러 기업이 제조 공장 확장에 집중하고 있습니다. 예를 들어

- 2022년 11월: 제너럴 모터스(General Motors)는 전기자동차를 생산하는 메트로 디트로이트의 두 조립 공장에 공급하기 위해 인디애나 주 베드포드에 위치한 알루미늄 다이캐스팅 파운드리 확장에 4,500만 달러를 투자할 것이라고 발표했습니다.

- 2022년 8월: 스텔란티스는 코코모 파운드리에 1,400만 달러를 투자한다고 발표했습니다. 파운드리에 대한 투자는 기존 다이캐스팅 기계와 셀을 하이브리드 전기자동차(HEV) 용도를위한 직접 연료 분사 및 유연성을 갖춘 1.6 리터, i-4 터보 차저 장치 용으로 변환하는 데 사용됩니다.

이 방법은 또한 모래 주조와 같은 다른 방법보다 더 나은 공차와 표면 마감을 제공합니다. 따라서 1,000-1만 개 정도의 대량 생산이 가능한 검증된 기술입니다. 그러나 금형 비용은 다양하며 일반적으로 모래 주조법보다 비싸다는 단점이 있습니다.

따라서 제조업체들은 시장 환경의 변화에 따라 포트폴리오를 개편할 것으로 예상되며, 이는 예측 기간 동안 시장을 주도할 것으로 보입니다.

아시아태평양이 시장을 독점

아시아태평양은 제조업과 인프라에 대한 투자 증가로 인해 급속한 산업화가 진행되고 있습니다. 이 지역에서는 항공우주, 방위, 건설 등의 산업이 크게 성장할 것으로 예상되어 중력 다이캐스팅 시장에 새로운 기회가 창출될 것으로 예상됩니다.

아시아태평양은 경량 부품에 대한 수요 증가, 가처분 소득 증가, 에너지 효율과 지속가능성에 대한 관심 증가 등 여러 요인으로 인해 중력 다이캐스팅 주조 분야에서 가장 크고 빠르게 성장하는 시장입니다.

아시아태평양의 중력 다이캐스팅 시장은 세계 최대 자동차 시장인 중국이 주도하고 있습니다. 중국 정부의 경량화 및 에너지 효율이 높은 부품 사용을 장려하는 정책으로 인해 중력 다이캐스팅에 대한 중국 내 수요가 증가할 것으로 예상됩니다. 또한, 중국 내 전기자동차의 보급은 시장에 새로운 문을 열어줄 것으로 보입니다.

아시아태평양의 또 다른 중요한 시장인 인도는 가처분 소득이 증가하고 연료 효율에 대한 관심이 높아짐에 따라 경량 부품에 대한 수요가 증가하고 있습니다. 인도 정부는 경량 및 에너지 효율이 높은 부품의 사용을 장려하고 있어 중력 다이캐스팅 주조에 대한 수요가 증가할 것으로 예상됩니다. 또한, 이 시장은 인도에서 전기자동차의 인기 상승으로 인한 수혜를 받을 것으로 예상됩니다.

또한, 자동차에 대한 큰 수요로 인해 더 많은 OEM 및 자동차 부품 제조업체가 등장했습니다. 그 결과, 인도는 자동차 및 자동차 부품에 대한 전문성을 발전시켜 인도산 다이캐스팅 자동차 부품에 대한 수요를 증가시켜 시장 성장을 가속했습니다.

자동차부품산업협회(ACMA)의 예측에 따르면, 인도의 자동차 부품 수출은 2026년까지 300억 달러에 달할 것으로 예상됩니다. 자동차 부품 산업은 2026년까지 2,000억 달러의 매출을 기록할 것으로 예상됩니다.

이 지역에서는 중력 다이캐스팅의 활용을 증가시킬 것으로 예상되는 상당한 기술 발전이 이루어지고 있습니다. 재료 과학, 설계 소프트웨어 및 자동화 기술의 발전으로 중력 다이캐스팅의 효율성과 품질이 향상되어 다양한 부문에서 중력 다이캐스팅을 더욱 매력적으로 만들 수 있을 것으로 예상됩니다.

중력 다이캐스팅 산업 개요

시장의 주요 기업으로는 Rockman Industries, Endurance Group, Minda Corporation, Hitachi Metals, Georg Fischer Limited, MAN Group(Alucast), Zollern GmbH, Esko Die Casting, CIE Automotive 등이 있습니다. 시장의 주요 기업들은 수요 증가에 대응하기 위해 생산 능력을 확장하고 있습니다. 예를 들어

- 2023년 6월, 중국 자동차 부품 공급업체 아시아웨이 오토모티브 컴포넌트(Asiaway Automotive Components)는 멕시코 산루이스 포토시에 4,140만 달러를 투자하여 신공장 1기를 가동했습니다. 이 2 단계 공급업체는 다이캐스팅 공정(HPDC 125T - 6600T), CNC, 가공, 가공, 세척, 테스트, 조립, 창고 보관, 산 루이스 포토시 및 멕시코 북부의 다양한 1 단계 기업에 배송을 사용하여 알루미늄 및 아연 자동차 부품을 생산하고 있습니다.

- 2023년 9월, Rox Motor Tech와 베이징자동차가 공동으로 설립한 자동차 브랜드 Polestones는 산동위챠오 선구자 그룹으로부터 10억 달러의 전략적 투자를 받았다고 발표했습니다. 이 자금은 알루미늄 차체 연구 개발, 통합 다이캐스팅 기술, 단공정 지능형 제조 공장 프로젝트에 사용될 예정입니다.

- 2022년 5월: GF의 스위스 샤프하우젠(Schaffhausen) 지사인 GF Casting Solutions는 전기자동차(EV) 부품 개발 개선에 경험을 활용할 것이라고 발표했습니다. 이 회사는 설계 및 개념의 초기 단계부터 고객과 협력하여 고객의 요구 사항을 충족하는 제품을 생산할 수 있습니다. 공동 개발 단계에서 GF Casting Solutions는 르노의 두 가지 하이브리드 모델용 경량 다이캐스팅 배터리 하우징을 제작했습니다. 이 하우징은 알루미늄 합금으로 제작되어 뛰어난 기능 통합과 냉각 회로 통합을 가능하게 합니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 시장 성장 촉진요인

- 시장 성장 억제요인

- 업계의 매력 - Porter의 Five Forces 분석

- 신규 진출업체의 위협

- 구매자/소비자의 교섭력

- 공급 기업의 교섭력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 세분화

- 용도

- 자동차

- 전기 및 전자

- 산업 용도

- 기타 용도

- 원재료

- 알루미늄

- 아연

- 지역

- 북미

- 미국

- 캐나다

- 기타 북미

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 독일

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 세계 기타 지역

- 남미

- 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 벤더의 시장 점유율

- 기업 개요

- Rockman Industries

- Endurance Group

- Minda Corporation

- Hitachi Metals

- Georg Fischer Limited

- MAN Group(Alucast)

- Zollern GmbH

- Harrison Castings

- Esko Die Casting

- CIE Automotive

제7장 시장 기회와 향후 동향

LSH 24.07.30The Gravity Die Casting Market size is estimated at USD 25.43 billion in 2024, and is expected to reach USD 30.72 billion by 2029, growing at a CAGR of 3.79% during the forecast period (2024-2029).

Gravity-die casting is one of the oldest methods of die casting. This die-casting process is used to create accurately dimensioned, finely defined, smooth, or textured surface metal parts. The fundamental benefit of gravity die casting is its fast-manufacturing speed. The reusable die tooling enables the production of hundreds of castings per day. High-definition parts reduce machining costs, while higher surface finish saves finishing expenses.

Due to its high thermal conductivity, the electrical and electronics industry is likely to see an increase in demand for aluminum die-casting parts during the forecast period. Die-casting machinery is in high demand as a result of the automotive industry's growing preference for lightweight metals and rising automobile sales.

Over the long term, the market is anticipated to benefit from the development of renewable power generation and the rapid expansion of the consumer electronics, computers, and communication industries.

With the development of new technologies, automotive parts have seen advancement and innovation in recent years. Among them, auto component manufacturing using lightweight materials has received national attention. In addition, automakers are using lightweight non-ferrous metals to reduce the weight of vehicles as a result of CAFE standards and EPA policies to reduce automobile emissions and improve fuel economy. As a result, the former automotive market is witnessing a significant boost from the use of die-cast parts to reduce weight.

Gravity Die Casting Market Trends

Automotive Industry is Expected Capture Major Market Share

Gravity die casting is a standard process for manufacturing some high-integrity automotive parts. This process produces fine-grained and dense structures with attractive mechanical properties, due to the fast and oriented hardening of the melts in permanent metal molds, which makes it ideal for components like engine-related parts.

But the trend away from the combustion engine toward alternatives like electric powered vehicles has inevitable effects on the demand for die-casted parts. For instance, while a combustion engine contains approximately 200 casted parts, only around 25, i.e., one tenth of them, are needed for an electrical drivetrain.

Factors such as lowering carbon emissions increased government initiatives to promote the usage of lighter vehicles, and rapid development of technology in automotive die-casting machines are anticipated to boost demand in the market.

Driven by ecological and economic requirements, the global automotive industry has been creating new body-in-white designs in which structural die-cast components help significantly reduce weight. Moreover, the production of die-cast structural components has increased even more due to incorporating functions into the castings, new aluminum alloy concepts, and new component design trends. Moreover, growing vehicle sales, not only in the passenger car segment but also for commercial vehicles, are expected to support the market's growth.

The automotive industry consumes over 60% of the cast products used worldwide. Thereby, considering the growth opportunities associated with the automobile and transportation industry, several players in the market are focusing on manufacturing plant expansion. For instance,

- November, 2022: General Motors announced an investment of USD 45 million in expanding its aluminum die-casting foundry in Bedford, Indiana, to feed two metro Detroit assembly plants that will produce electric vehicles.

- August, 2022: Stellantis announced an investment of USD 14 million in the Kokomo casting plant. The investment at the Casting Plant will be used to convert existing die-cast machines and cells for 1.6-liter, I-4 turbocharged units with direct fuel injection and flexibility for hybrid-electric vehicle (HEV) applications.

This method also gives better tolerances and surface finish than other methods, like sand casting. Hence, it represents a proven technology to produce fairly large batch quantities of the order of 1,000 to 10,000. But tooling costs vary and are generally higher than the sand-casting method.

Hence, manufacturers are expected to revamp their portfolio to the changing market conditions, which is expected to drive the market over the forecast period.

Asia-Pacific Dominates the Market

The Asia-Pacific region is witnessing rapid industrialization, driven by increasing investments in manufacturing and infrastructure development. This is expected to create new opportunities for the gravity die-casting market, as several industries such as aerospace, defense, and construction are expected to witness significant growth in the region.

The Asia-Pacific region is the biggest and fastest-growing market for gravity die casting because of a number of factors, like the growing demand for lightweight components, rising disposable incomes, and a growing emphasis on energy efficiency and sustainability.

The gravity die-casting market in the Asia-Pacific region is largely driven by China, the largest automotive market in the world. Gravity die-casting is expected to be in high demand in China as a result of the government's efforts to encourage the use of lightweight and energy-efficient components. Also, the rising reception of electric vehicles in China is supposed to set out new open doors for the market.

Due to rising disposable incomes and an increasing focus on fuel efficiency, India, another significant market in the Asia-Pacific region, is experiencing a growing demand for lightweight components. Gravity die casting is expected to be in high demand in India as a result of the government's efforts to encourage the use of lightweight and energy-efficient components. Additionally, the market is anticipated to benefit from the rising popularity of electric vehicles in India.

Significant demand for automobiles also led to the emergence of more original equipment and auto components manufacturers. As a result, India developed expertise in automobiles and auto components, which helped boost the demand for Indian die-casted auto components, propelling the market growth.

As per the Automobile Component Manufacturers Association (ACMA) forecast, auto component exports from India is expected to reach USD 30 Billion by 2026. The auto component industry is projected to record USD 200 Billion in revenue by 2026.

The region is seeing substantial technological advancements, which are projected to increase the usage of gravity die casting. Developments in materials science, design software, and automation technologies are predicted to increase gravity die casting efficiency and quality, making it more appealing to a variety of sectors.

Gravity Die Casting Industry Overview

Some of the major players in the market include Rockman Industries, Endurance Group, Minda Corporation, Hitachi Metals, Georg Fischer Limited, MAN Group (Alucast), Zollern GmbH, , Esko Die Casting, and CIE Automotive. Key players in the market are expanding their production capacity to cater to the increased demand. For instance,

- June 2023, Chinese automotive supplier Asiaway Automotive Components inaugurated the first phase of its new plant in San Luis Potosi, Mexico with an investment of USD 41.4 million. The Tier 2 supplier produces aluminum and zinc automotive components using the die-casting process (HPDC 125T - 6600T), CNC, machining, cleaning, testing, assembly, warehousing and distribution to various Tier 1 companies in San Luis Potosi and throughout northern Mexico.

- September 2023, Polestones, an auto brand jointly established by Rox Motor Tech Co., Ltd. and Beijing Automobile Works, announced that it received a USD 1 billion strategic investment from Shandong Weiqiao Pioneering Group. The funds will be used for all-aluminum vehicle body R&D, integrated die casting technologies, and a short-process intelligent manufacturing plant project.

- May, 2022: GF Casting Solutions, a branch of GF, Schaffhausen (Switzerland), said that it will use its experience to improve the development of electric car parts and components (EVs). The company is able to create goods that satisfy the demands of its clients by cooperating with them from the early design and conceptual phases. In a cooperative development phase, GF Casting Solutions created a lightweight die-cast battery housing for Renault's two hybrid models. The enclosure is built of an aluminum alloy, which allows for great functional integration and an integrated cooling circuit.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Growth of the Automotive Industry to Drive Demand in the Gravity Die Casting Market

- 4.2 Market Restraints

- 4.2.1 High Processing Cost May Hamper Market Expansion

- 4.3 Industry Attractiveness - Porter's Five Force Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Application

- 5.1.1 Automotive

- 5.1.2 Electrical and Electronics

- 5.1.3 Industrial Applications

- 5.1.4 Other Appplications

- 5.2 Raw Material

- 5.2.1 Aluminum

- 5.2.2 Zinc

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Germany

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Rest of the World

- 5.3.4.1 South America

- 5.3.4.2 Middle East & Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Rockman Industries

- 6.2.2 Endurance Group

- 6.2.3 Minda Corporation

- 6.2.4 Hitachi Metals

- 6.2.5 Georg Fischer Limited

- 6.2.6 MAN Group (Alucast

- 6.2.7 Zollern GmbH

- 6.2.8 Harrison Castings

- 6.2.9 Esko Die Casting

- 6.2.10 CIE Automotive

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing Adoption of Electric Vehicles