|

시장보고서

상품코드

1521777

자동차용 수동 전자부품 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2024-2029년)Automotive Passive Electronic Components - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

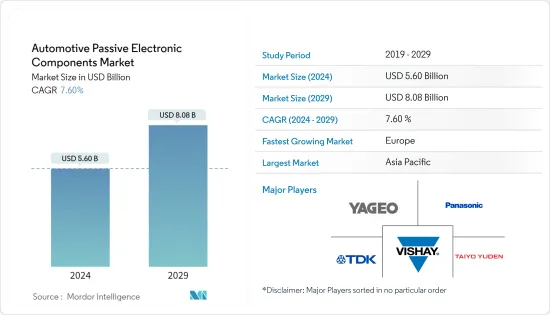

자동차용 수동 전자부품 시장 규모는 2024년 56억 달러로 추정되고, 2029년에는 80억 8,000만 달러에 이를 것으로 예측되며, 예측기간 중(2024-2029년) CAGR은 7.60%로 성장할 것으로 예측됩니다.

주요 하이라이트

- 수동 부품 요구 증가는 자동차 산업이 주도하고 있습니다. 보닛의 전자제어장치(ECU), 인포테인먼트 시스템, ADAS(선진 운전 지원 시스템) 등 다양한 용도로 자동차의 전자 시스템에 대한 수요가 높아지고 있습니다. 차량용 전자 시스템은 필터링 및 에너지 축적용 커패시터, 회로 보호용 배리스터, 소형 ECU용 커넥터, 연결성 지원용 RF 및 마이크로파 수동 부품 및 안테나 등 신뢰할 수 있는 성능을 보장하는 고품질 부품이 필요합니다.

- 자동차 제조업체는 연비 향상, 배출 가스 절감, 차량 전체의 성능 향상을 위해 기존의 내연 엔진 차량에 전자 부품을 통합하는 경우가 늘고 있습니다. 이 추세는 저항기, 커패시터, 인덕터와 같은 수동 전자부품 수요를 끌어올리고 있습니다. 예를 들어 SIAM India에 따르면 2023 회계 연도에는 국내 시장에서 389만 대 이상의 승용차가 판매되었습니다.

- 충돌 회피 시스템 및 적응형 크루즈 컨트롤과 같은 ADAS(첨단 운전 지원 시스템)는 센서 신호 처리, 필터링 및 데이터 전송을 위해 커패시터와 같은 수동 전자부품에 크게 의존합니다. 최근 자동차에는 고급 인포테인먼트 시스템, 텔레매틱스 및 연결 솔루션이 탑재되어 있으며 무선 통신, 신호 처리 및 데이터 전송에 수동 부품이 필요합니다.

- 차량용 전자기기의 소형화 및 집적화가 진행됨에 따라 수동 부품은 점점 엄격해지는 사이즈와 중량 요건을 충족시켜야 합니다. 패키지를 소형화하면서 성능을 유지하는 등 소형화의 과제는 시장 성장을 제한할 수 있습니다. 게다가 자동차 등급의 수동 전자부품을 설계하고 제조하려면 엄청난 연구 개발과 시험이 필요합니다. 높은 개발 비용은 시장 혁신을 제한합니다.

- 지속가능성과 기후 변화와 같은 환경문제는 자동차 산업의 동향과 규제에 영향을 미칩니다. 생태계의 지속가능성을 강조하는 경향이 커지면 자동차 에너지 효율이 높고 친환경 전자 부품의 채용이 촉진될 수 있습니다. 또한, 무역 정책, 관세, 무역 협정은 자동차 부품의 비용과 가용성에 영향을 줄 수 있습니다. 무역 정책의 변화는 공급망을 혼란스럽게 하고 가격 설정에 영향을 미치며 시장 경쟁에 영향을 줄 수 있습니다.

자동차용 수동 전자부품 시장 동향

현저한 성장을 이루는 커패시터

- 커패시터 기술의 발전으로 소형, 경량, 고효율 커패시터가 개발되고 있습니다. 이를 통해 자동차 제조업체는 소형 및 경량의 전자 시스템을 설계할 수 있어 차량 전체의 무게를 줄여 연비를 향상시킬 수 있습니다. ADAS(첨단 운전 지원 시스템), 인포테인먼트 시스템, 자동차 커넥티비티 기능의 채용이 증가하고 있기 때문에 견고하고 신뢰성이 높은 전자 부품이 필요합니다. 커패시터는 안정적인 전원 공급을 제공하고 센서, 카메라 및 통신 모듈의 부드러운 동작을 보장함으로써 이러한 기능의 구현을 지원합니다.

- 예를 들어, 2023년 8월 TDK Corporation in India(Nashik)는 생산 능력을 증강했기 때문에 비즈니스 전망이 열렸습니다. Nashik에 있는 이 특정 시설은 생산 능력을 확대하고 있으며, 약 2만 3,000제곱미터에 달하는 신구조를 도입했습니다. 향후 4년간 자동차 부문에서 사용되는 직류 커패시터용 생산 라인이 증설될 예정입니다. 이 커패시터는 인도 국내 시장 및 해외 수출용으로 제조됩니다. 생산 능력의 향상은 회사의 중기 성장 전략을 지원하는 새로운 전망을 창출합니다.

- 엄격한 정부 규제와 연비 기준은 에너지 효율적인 자동차 시스템 수요를 촉진하고 있습니다. 커패시터는 에너지 사용을 최적화하고 전력 손실을 최소화하고 규제 당국의 요구 사항과 지속가능성 목표에 부합합니다. 커패시터는 자동차 전자 시스템의 기능에 필수적이며 자동차의 전기화, 연결 및 자동화 동향이 가속화됨에 따라 수요가 계속 증가할 것으로 예상됩니다.

- 예를 들어 2024년 5월 현대차는 이미 미국에 확보한 투자를 활용하고 EV 공장에서 하이브리드 자동차를 생산할 계획입니다. 이 세계 3위의 자동차 제조업체는 계열사 기아자동차와 함께 조지아주 EV와 배터리 제조시설에 할당된 자금을 하이브리드차 생산에 충당할 의향입니다. 현대자동차와 키아를 산하한 현대자동그룹의 사우스코리아는 조지아 주에 전기차와 배터리 생산공장을 신설하기 위해 126억 달러를 투자할 계획을 발표했습니다.

유럽이 큰 시장 점유율을 차지

- 유럽에는 영국, 독일, 프랑스 등 세계 최대의 자동차 시장이 있습니다. 유럽은 세계 자동차 생산 및 판매의 대부분을 차지합니다. 이들 국가의 상용차 및 승용차에 대한 수요 증가는 다양한 자동차 시스템에 사용되는 수동 전자부품 시장에 기여하고 있습니다.

- 유럽에서는 전기자동차(EV), 배터리 전기자동차(BEV), 하이브리드 전기자동차(HEV)의 도입이 급속히 진행되고 있습니다. 유럽 정부의 장려책과 기술의 진보가 파워트레인의 전동화로의 전환을 촉진하고 있습니다. 이러한 전환은 전동 드라이브 트레인, 배터리 관리 시스템, 차량용 전자 기기에 사용되는 커패시터, 인덕터, 저항기와 같은 수동 전자부품에 대한 수요를 증가시킵니다. 예를 들어 KBA의 보고서에 따르면 2023년에는 BEV와 PHEV를 모두 포함한 전기차가 독일 승용차의 약 4.8%를 차지합니다. 전기자동차의 비율은 특히 BEV 모델에서 지정된 기간 내에 매년 꾸준히 상승하고 있습니다.

- 영국, 독일, 프랑스 등 유럽 국가의 자동차 산업은 기술 혁신의 최전선에 있으며 선진적인 자동차 기술 개발에 주력하고 있습니다. 여기에는 스마트 기능, 연결 솔루션 및 ADAS 통합이 포함됩니다. 이러한 기술에는 차량 네트워킹과 같은 기능을 지원하기 위해 다양한 수동 전자부품이 필요합니다.

- 예를 들어 2023년 11월 영국 정부는 영국 제조업을 지원하고 경제 확대를 자극하기 위한 45억 유로(570만 달러)의 대규모 투자의 일환으로 1억 5,000만 유로(1억 8,900만 달러)를 할당했습니다. 이 자금은 2030년까지의 연결 이동성 및 자동 모빌리티(CAM) 부문을 대상으로 합니다. CAM을 지원하기 위해 할당된 예산은 산업계의 기여에 의해 보완됩니다. 이를 통해 영국의 커넥티드 및 자율주행차센터(CCAV)는 자율주행 기술, 제품, 서비스의 창조, 진보, 구현, 생산에 있어서 세계적인 리더로서 영국의 지위를 확고하게 할 수 있습니다.

자동차용 수동 전자부품 산업 개요

자동차용 수동 전자부품 시장의 경쟁은 치열합니다. 크고 작은 다양한 진출기업이 존재하기 때문에 시장은 매우 집중되어 있습니다. 대기업은 모두 큰 시장 점유율을 차지하고 있으며, 세계 소비자 기반의 확대에 주력하고 있습니다. 시장의 주요 기업으로는 Yageo Corporation, Panasonic Corporation, TDK Corporation, Vishay Intertechnology Inc., Taiyo Yuden Corporation 등이 있습니다. 각 회사는 예측 기간 동안 경쟁을 획득하기 위해 여러 제휴, 파트너십, 인수를 맺고 신제품 도입에 투자함으로써 시장 점유율을 확대하고 있습니다.

2024년 3월 JF Kilfoil Company는 Knowles 제품의 대리점을 확장하여 중서부 시장에서 Cornell Dubilier 브랜드를 추가했습니다. 이 제휴는 Knowles의 Cornell Dubilier 인수로 필름 커패시터, 전해 커패시터, 특수 커패시터를 보다 폭넓게 제공할 수 있게 되었기 때문입니다. 제품 라인업은 단층 커패시터, 트리머, 알루미늄 전해 커패시터, 알루미늄 폴리머 커패시터, 필름 커패시터, 운모 커패시터, 슈퍼커패시터로 구성됩니다. 이 제품들은 신뢰성이 높고 수명이 길고 엄격한 상황에서도 우수한 성능을 발휘하는 것으로 알려져 있습니다.

2023년 9월 Knowles Precision Devices가 Cornell Dubilier를 현금 2억 6,300만 달러로 인수했습니다. 이 인수에는 필름, 전해 및 운모 커패시터 제품이 포함되어 2024년까지 비GAAP 기반 EPS가 향상될 것으로 예상됩니다. Cornell Dubilier의 다양한 파워 필름, 전해 커패시터 및 운모 커패시터는 Knowles의 Precision Devices 부서와 결합하여 현재 및 미래 고객에게 가치 있는 제안과 제품 포트폴리오의 확대를 설명합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

- 시장 개요

- 업계의 매력-Porter's Five Forces 분석

- 신규 진입업자의 위협

- 구매자 및 소비자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

- 기술 스냅샷

- COVID-19의 영향과 기타 거시 경제 요인이 시장에 미치는 영향

제5장 시장 역학

- 시장 성장 촉진요인

- 산업계에서 첨단 전자 디바이스의 사용 증가

- 소형화 설계에 대한 기호의 고조

- 시장 성장 억제요인

- 수동 전자부품의 제조에 사용되는 중요 금속의 가격 변동 및 다양한 수동 부품의 제조에 있어서의 과제

제6장 시장 세분화

- 유형별

- 커패시터

- 세라믹 커패시터

- 탄탈 커패시터

- 알루미늄 전해 커패시터

- 종이 및 플라스틱 필름 커패시터

- 슈퍼커패시터

- 인덕터

- 저항기

- 표면 실장 칩

- 네트워크 및 어레이

- 기타 특수품

- EMC 필터

- 커패시터

- 지역별

- 북미

- 유럽

- 아시아

- 호주 및 뉴질랜드

- 중동 및 아프리카

- 라틴아메리카

제7장 경쟁 구도

- 기업 프로파일

- Yageo Corporation

- Panasonic Corporation

- TDK Corporation

- Vishay Intertechnology Inc.

- Taiyo Yuden Corporation

- Kyocera Corporation(includes AVX Corporation)

- Knowles Precision Devices

- Murata Manufacturing Co. Ltd

- Samsung Electro-Mechanical

- KOA Corporation

- Rubycon Corporation

- Nippon Chemi-Con Corporation

제8장 투자 분석

제9장 시장의 미래

AJY 24.08.08The Automotive Passive Electronic Components Market size is estimated at USD 5.60 billion in 2024, and is expected to reach USD 8.08 billion by 2029, growing at a CAGR of 7.60% during the forecast period (2024-2029).

Key Highlights

- The automotive industry is leading the way in the increasing need for passive components. The demand for electronic vehicle systems is rising for various uses, such as electronic control units (ECUs) under the hood, infotainment systems, and advanced driver assistance systems (ADASs). Automotive electronic systems require high-quality components to guarantee dependable performance, like capacitors for filtering and storing energy, varistors for circuit protection, connectors for small ECUs, and RF and microwave passive components and antennas for connectivity support.

- Automobile manufacturers increasingly integrate electronic components into traditional combustion engine vehicles to enhance fuel efficiency, reduce emissions, and improve overall vehicle performance. This trend drives the demand for passive electronic components like resistors, capacitors, and inductors. For instance, according to SIAM India, during the fiscal year 2023, more than 3.89 million passenger vehicles were sold in the domestic market.

- ADAS (advanced driver assistance systems), such as collision avoidance systems and adaptive cruise control, rely heavily on passive electronic components like capacitors for sensor signal processing, filtering, and data transmission. Modern vehicles feature advanced infotainment systems, telematics, and connectivity solutions that require passive components for wireless communication, signal processing, and data transmission.

- As automotive electronics become more compact and integrated, passive components must meet increasingly stringent size and weight requirements. Miniaturization challenges, such as maintaining performance while reducing package size, can limit market growth. In addition, designing and manufacturing automotive-grade passive electronic components require significant research, development, and testing. High development costs limit innovation in the market.

- Environmental concerns, including sustainability and climate change, influence automotive industry trends and regulations. Growing emphasis on ecological sustainability may drive the adoption of vehicles' energy-efficient and environmentally friendly electronic components. Moreover, trade policies, tariffs, and trade agreements can impact the cost and availability of automotive components. Changes in trade policies may disrupt supply chains, affect pricing, and influence market competition.

Automotive Passive Electronic Components Market Trends

Capacitors to Witness Significant Growth

- Advancements in capacitor technology have led to the development of smaller, lighter, and more efficient capacitors. This enables automotive manufacturers to design compact and lightweight electronic systems, reducing overall vehicle weight and improving fuel efficiency. The increasing adoption of ADAS (advanced driver assistance systems), infotainment systems, and automobile connectivity features require robust and reliable electronic components. Capacitors support implementing these features by providing a stable power supply and ensuring the smooth operation of sensors, cameras, and communication modules.

- For instance, in August 2023, TDK Corporation in India (Nasik) was set for business prospects as it has enhanced its capacity. This specific facility in Nashik is growing its production capabilities and has introduced a new structure spanning approximately 23,000 square meters. In the coming four years, more production lines will be established for DC capacitors used in automotive sectors. These capacitors will be manufactured for the local market in India and overseas export. The increase in capacity creates new prospects that will support the company's medium-term growth strategy.

- Stringent government regulations and fuel economy standards drive the demand for energy-efficient automotive systems. Capacitors help optimize energy usage and minimize power losses, aligning with regulator requirements and sustainability goals. Capacitors are integral to the functioning of automotive electronic systems, and the demand is expected to continue growing as vehicle electrification, connectivity, and automation trends accelerate.

- For instance, in May 2024, Hyundai Motor Co. planned to utilize the investment already set aside for the United States to manufacture hybrid vehicles at its EV plant. The third-largest automaker globally, along with affiliate Kia Corp, intends to use funds allocated for EV and battery manufacturing facilities in Georgia to produce hybrid cars. Hyundai Motor Group of South Korea, which includes Hyundai Motor and Kia, announced plans to invest USD 12.6 billion in building new electric vehicle and battery production plants in Georgia, marking its most significant investment outside of South Korea.

Europe to Hold Significant Market Share

- Europe is home to some of the world's largest automotive markets, including the United Kingdom, Germany, and France. Europe accounts for a significant portion of worldwide vehicle production and sales. The rising demand for commercial and passenger vehicles in these countries contributes to the market for passive electronic components used in various automotive systems.

- Europe is experiencing rapid growth in the adoption of electric vehicles (EVs), battery electric vehicles (BEVs), and hybrid electric vehicles (HEVs). European government incentives and technological advancements are driving the shift toward electrified powertrains. This transition increases the demand for passive electronic components such as capacitors, inductors, and resistors used in electric drivetrains, battery management systems, and onboard electronics. For instance, in 2023, electric cars, including both BEV and PHEV, accounted for approximately 4.8& of passenger cars in Germany, as reported by KBA. The proportion of electric vehicles has steadily risen each year within the specified time frame, particularly for BEV models.

- The automotive industry in European countries like the United Kingdom, Germany, and France is at the forefront of innovation, strongly focusing on developing advanced vehicle technologies. This includes the integration of smart features, connectivity solutions, and ADAS. These technologies require various passive electronic components to support functions such as vehicle networking.

- For instance, in November 2023, the United Kingdom government allocated EUR 150 million (USD 189 million) as part of a larger EUR 4.5 billion (USD 5.7 million) investment to support British manufacturing and stimulate economic expansion. This funding is aimed at the connected and automated mobility (CAM) sector up to 2030. The budget allocated to help CAM will be supplemented by industry contributions, which will allow the United Kingdom's Centre for Connected and Autonomous Vehicles (CCAV) to solidify the UK's position as a global leader in the creation, advancement, implementation, and production of self-driving technologies, products, and services.

Automotive Passive Electronic Components Industry Overview

The automotive passive electronic components market is very competitive. The market is highly concentrated due to various small and large players. All the major players account for a significant market share and focus on expanding the global consumer base. Some significant players in the market are Yageo Corporation, Panasonic Corporation, TDK Corporation, Vishay Intertechnology Inc., Taiyo Yuden Corporation, and many more. Companies are increasing their market share by forming multiple collaborations, partnerships, and acquisitions and investing in introducing new products to earn a competitive edge during the forecast period.

March 2024: JF Kilfoil Company expanded its representation of Knowles' products to include the Cornell Dubilier brand in the Midwest market. This partnership was established due to Knowles' acquisition of Cornell Dubilier, which allowed the company to offer a broader range of film, electrolytic, and specialty capacitors. The product range comprises single-layer capacitors, trimmers, aluminum electrolytic capacitors, aluminum polymer capacitors, film capacitors, mica capacitors, and supercapacitors. These items are known for their reliability, longevity, and excellent performance in challenging situations.

September 2023: Knowles Precision Devices acquired Cornell Dubilier for USD 263 million in cash. This acquisition will include film, electrolytic, and mica capacitor products and is anticipated to enhance non-GAAP EPS by 2024. Cornell Dubilier's diverse range of power film, electrolytic, and mica capacitors, combined with Knowles' Precision Devices segment, will offer a valuable proposition and expanded product portfolio to current and potential customers.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Buyers/Consumers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Technology Snapshot

- 4.4 Impact of COVID-19 Aftereffects and Other Macroeconomic Factors on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Usage of Advanced Electronic Devices in the Industry

- 5.1.2 Increasing Preference for Miniaturized Designs

- 5.2 Market Restraints

- 5.2.1 Fluctuating Prices of Critical Metals Used in Manufacturing of Passive Electronic Components/ Challenges in the manufacturing of various Passive Components

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Capacitors

- 6.1.1.1 Ceramic Capacitors

- 6.1.1.2 Tantalum Capacitors

- 6.1.1.3 Aluminum Electrolytic Capacitors

- 6.1.1.4 Paper and Plastic Film Capacitors

- 6.1.1.5 Supercapacitors

- 6.1.2 Inductors

- 6.1.3 Resistors

- 6.1.3.1 Surface-mounted Chips

- 6.1.3.2 Network and Array

- 6.1.3.3 Other Specialty

- 6.1.4 EMC Filters

- 6.1.1 Capacitors

- 6.2 By Geography***

- 6.2.1 North America

- 6.2.2 Europe

- 6.2.3 Asia

- 6.2.4 Australia and New Zealand

- 6.2.5 Middle East and Africa

- 6.2.6 Latin America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles*

- 7.1.1 Yageo Corporation

- 7.1.2 Panasonic Corporation

- 7.1.3 TDK Corporation

- 7.1.4 Vishay Intertechnology Inc.

- 7.1.5 Taiyo Yuden Corporation

- 7.1.6 Kyocera Corporation (includes AVX Corporation)

- 7.1.7 Knowles Precision Devices

- 7.1.8 Murata Manufacturing Co. Ltd

- 7.1.9 Samsung Electro-Mechanical

- 7.1.10 KOA Corporation

- 7.1.11 Rubycon Corporation

- 7.1.12 Nippon Chemi-Con Corporation