|

시장보고서

상품코드

1536886

데이터센터용 액체 냉각 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2024-2029년)Data Center Liquid Cooling - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

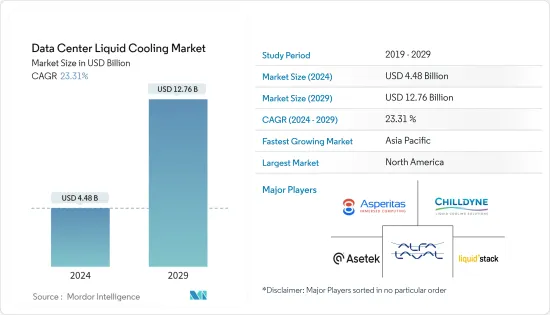

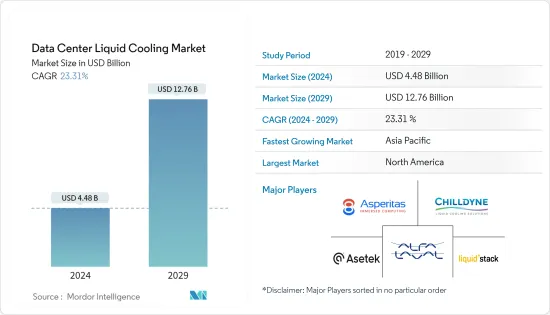

세계 데이터센터용 액체 냉각 시장 규모는 2024년 44억 8,000만 달러로 2024-2029년 연평균 23.31% 성장하여 2029년에는 127억 6,000만 달러에 달할 것으로 예상됩니다.

인구 증가와 디지털 인프라에 대한 의존도가 높아짐에 따라 데이터센터에 대한 요구가 증가하고 있습니다. 최적의 성능을 보장하고 데이터센터의 개발과 성장으로 인한 값비싼 다운타임을 피하기 위해 효과적인 냉각 솔루션이 절실히 요구되고 있습니다.

주요 하이라이트

- 데이터센터의 성장은 클라우드 컴퓨팅 솔루션의 도입과 빅데이터 분석의 확산에 크게 기여하고 있습니다. 기업들은 점점 더 많은 양의 데이터를 처리하고 조사하기 위해 클라우드 기반 서비스에 의존하고 있으며, 방대한 양의 데이터를 저장하고 있습니다. 예를 들어, Amazon Web Services(AWB), Microsoft Azure, Google Cloud Platform과 같은 클라우드 업계 선두주자들은 증가하는 수요에 대응하기 위해 데이터센터를 지속적으로 확장하고 있습니다.

- 인도, 홍콩, 중국, 인도네시아 등 신흥 경제국들의 IT 인프라 구축이 진행 중으로 데이터센터 수요가 증가할 가능성이 높으며, IT 산업에 비용 및 운영 측면에서 유리한 클라우드 모델 도입으로 데이터센터 수요 증가가 예상됩니다.

- 데이터센터 사업자들은 새로운 냉각 시스템으로 전환할 때 발생할 수 있는 다운타임 손실에 대해 우려하고 있습니다. 따라서 운영 비용을 간과하고 구식 냉각 시스템을 계속 사용하고 있습니다. 이러한 추세는 검증되지 않은 신기술의 채택을 지연시키고 있습니다.

- 팬데믹 이후 기업의 디지털 혁신의 새로운 물결이 시장을 주도할 것으로 예상됩니다. 많은 기업들이 데이터센터를 타사 코로케이션 시설에 의존하기 시작했으며, 호스팅 센터의 파워와 멀티 클라우드 환경을 결합한 하이브리드 IT의 추세가 강화되고 있습니다.

데이터센터용 액체 냉각 시장 동향

엣지 컴퓨팅이 급성장

- 예측 기간 동안 기업들은 IP로 연결된 모바일 기기 및 M2M(Machine-to-Machine) 기기가 급증하면서 대량의 IP 트래픽을 처리하게 될 것으로 예상됩니다.

- 더 빠른 Wi-Fi 서비스 및 온라인 제공 업체의 애플리케이션 배포에 대한 수요가 증가할 것으로 예상됩니다. 또한, 자율주행차 등 일부 M2M 디바이스는 안전을 보장하기 위해 로컬 처리 리소스와 실시간 통신을 필요로 합니다.

- 엣지 데이터센터의 도입은 5세대(5G) 네트워크와 사물인터넷(IoT)을 포함한 많은 신기술에 이점을 가져다 줄 것이며, 2028년까지 IoT 연결의 보급이 두 배 이상 증가하여 광역 IoT의 수가 60억 개에 달할 것으로 예상됩니다.

- 또한, 5G 무선 인프라의 출현으로 데이터센터 사업자들은 저지연과 높은 내결함성을 제공하는 네트워크와 연동되는 엣지 컴퓨팅 인프라를 선택하게 되었습니다. 멀티 액세스 엣지 컴퓨팅(MEC)은 네트워크 서비스가 사용자와 긴밀하게 연결될 수 있도록 지원합니다. 따라서 효율적인 엣지 데이터센터에 대한 수요는 전 세계 5G 기술 도입, 자율주행차 및 자율주행차, 스마트 시티의 증가 등 여러 요인으로 인해 증가할 것으로 예상됩니다.

- 그러나 대규모 엣지 컴퓨팅 구축에 있어 중요한 요구사항은 낮은 운영 비용입니다. 엣지 배치에서 침수 냉각은 극적인 에너지 절감 효과를 가져오는 것으로 알려져 있습니다.

- 액체 냉각 솔루션의 신뢰성과 노터치 기능은 원격지 장비의 실행 가능한 운영 및 관리에 필요한 평균 유지보수 시간 연장 및 개입 간격 연장에 대한 요구와 일치합니다.

북미가 가장 큰 시장 점유율을 차지

- 북미는 새로운 기술을 가장 빠르게 도입하는 국가입니다. 데이터센터 투자자들은 침수 및 칩 직하 냉각 솔루션에 대한 투자를 늘리고 있습니다. EdgePresence, EdgeMicro, American Towers 등 많은 미국 사업자들이 엣지 데이터센터에 투자하기 시작했으며, 미국은 5G 네트워크의 출현으로 인해 엣지 데이터센터의 중요성이 더욱 부각되고 있습니다. 투자하고 있습니다.

- Cisco Systems의 보고서에 따르면 미국의 모바일 데이터 트래픽은 매년 크게 증가하고 있으며, 2017년월 1.26 엑사바이트의 데이터 트래픽에서 2022년에는월 7.75 엑사바이트의 데이터 트래픽을 기록할 것으로 예상됩니다. 에릭슨에 따르면, 이 데이터 트래픽은 2030년까지 3배 이상 증가할 것으로 예상됩니다. 따라서 이러한 규모를 쉽게 연결할 수 있는 저지연과 광대역폭을 확보할 수 있는 분산형 클라우드가 실용화되고 있습니다.

- 미국에서는 사람과 기업의 인터넷 사용이 크게 증가하고 있습니다. 미국은 데이터센터 운영의 가장 큰 시장이며, 최종사용자의 데이터 소비 증가로 인해 지속적으로 성장하고 있습니다. 사물인터넷(IoT)의 인기 증가는 미국 하이퍼스케일 데이터센터 시장의 중요한 원동력이 되고 있으며, 비즈니스 사용자와 소비자 모두에서 생성되는 엑사바이트 단위의 데이터를 지원할 수 있는 시설의 증설로 이어지고 있습니다.

- 미국은 향후 몇 년 동안 이 지역에서 가장 빠르게 성장하는 데이터센터 시장이 될 것으로 보입니다. 미국 데이터센터 건설의 가장 큰 원동력은 최근 몇 년간의 경제적 인센티브와 세제 혜택입니다. 약 27개 주에서 데이터센터 프로젝트 유치를 위해 이러한 요소를 활용하고 있습니다. 또한, 미국에서 시행되고 있는 대규모 세금 감면 조치는 정부 주도로 새로운 메가 데이터센터 건설과 기존 데이터센터 리노베이션이 진행되고 있음을 보여줍니다. 이러한 시장의 움직임은 이 지역의 데이터센터용 액체 냉각 서비스에 대한 수요를 더욱 증가시키고 있습니다.

데이터센터용 액체 냉각 산업 개요

데이터센터용 액체 냉각 시장은 세분화되어 있고 경쟁이 치열하며, 알파라발(Alfa Laval Corporate AB), LiquidStack Inc.A/S, AsperitasChilldyne Inc. 시장 점유율 측면에서 현재 소수의 중요한 플레이어가 시장을 독점하고 있습니다. 널리 보급된 냉각 시스템은 여전히 공랭식이며, 수냉식 시스템은 전체 냉각 시스템에서 상대적으로 작은 점유율을 차지하고 있습니다. 상대적으로 높은 비용이 시장의 과제로 간주되기 때문에 침수 냉각 시스템 시장은 대체품의 위협이 큰 것으로 추정됩니다.

- 2024년 3월 - Summer는 산업용 냉각수 제조업체, 주문자 상표 부착 제조 장비 제조업체, 주문자 상표 부착 장비 제조업체, 고성능 컴퓨팅 애플리케이션 운영자, 데이터센터 제공업체 등 이해관계자로 구성된 선도적인 산업 포럼인 최근 설립된 액체 냉각연합(LCC)에 가입한다고 발표했습니다.

- 2024년 3월 - 중요 인프라 및 연속성 솔루션 제공업체인 버티브(Vertiv)가 솔루션 어드바이저(Solution Advisor) 인증을 획득했습니다. 엔비디아 파트너 네트워크(NPN)의 솔루션 어드바이저(Solution Advisor: Consultant) 파트너가 되어 버티브의 경험과 전원 및 냉각 솔루션 포트폴리오를 보다 포괄적으로 활용할 수 있게 됐습니다.

기타 혜택

- 엑셀 형식의 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 소개

- 조사 가정과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

- 데이터센터 냉각의 진화

- 에어컨/핸들러

- 칠러와 이코노마이저 시스템

- 액체 냉각 시스템

- 로우/랙/도어/오버헤드 냉각 시스템

- 데이터센터 냉각 시장 개요

- 에너지 소비, 계산 밀도 지표 및 액랭의 주요 검토사항

- 산업 이해관계자 분석

- 산업의 매력 - Porter's Five Forces 분석

- 구매자의 교섭력

- 공급 기업의 교섭력

- 신규 참여업체의 위협

- 경쟁 정도

- 대체품의 위협

제5장 시장 역학

- 시장 성장 촉진요인

- 지역의 IT 인프라 발전

- 그린 데이터센터의 출현

- 시장 성장 억제요인

- 비용, 적응 요건, 정전

- COVID-19의 산업에 대한 영향 평가

제6장 데이터센터의 리어 도어식 열교환기(RDHx) 전망

- 데이터센터의 RDHx와 액체 냉각(직접·간접) 기술 비교

- RDHx와 액랭 시장과 관련된 데이터센터 냉각 기술 벤더의 최근의 동향

- RDHx의 대략적인 세계 시장 점유율(10억 달러)

- RDHx의 주요 벤더 리스트(사업 개요, 포트폴리오, 최근의 동향)

제7장 직접 냉각 또는 액침 냉각 시장

- 직접 냉각 시장 개요와 예측

- 액침 냉각 - 주요 용도

- 고성능 컴퓨팅

- 엣지 컴퓨팅

- 암호화폐 채굴

- 액침 냉각 유체

- 플루오로카본계 유체

- 탄화수소계 유체

제8장 간접·직접 칩 냉각 시장

- 간접 냉각 시장 개요와 예측

- 간접·직접 칩 냉각의 주요 용도

제9장 시장 세분화

- 지역별

- 북미

- 유럽

- 아시아

- 호주·뉴질랜드

- 라틴아메리카

- 중동 및 아프리카

제10장 경쟁 상황

- 기업 개요

- Alfa Laval Corporate AB

- LiquidStack Inc.

- Asetek Inc. A/S

- Asperitas

- Chilldyne Inc.

- CoolIT Systems Inc.

- Fujitsu Ltd.

- Mikros Technologies

- Kaori Heat Treatment Co. Ltd

- Lenovo Group Limited

- LiquidCool Solutions Inc.

- Midas Green Technologies

- Iceotope Technologies Ltd

- USystems Ltd(Legrand Group)

- Rittal GmbH & Co. KG

- Schneider Electric

- Submer Technologies & Submer Inc.

- Vertiv Group Corp.

- Wakefield Thermal Solutions Inc.

- Wiwynn Corporation

- 3M Company

- Engineered Fluids Inc.

- Green Revolution Cooling Inc.

- Solvay SA

제11장 밸류체인의 냉각 기술 혁신

제12장 투자 분석과 시장 전망

ksm 24.08.29The Data Center Liquid Cooling Market size is estimated at USD 4.48 billion in 2024, and is expected to reach USD 12.76 billion by 2029, growing at a CAGR of 23.31% during the forecast period (2024-2029).

The need for data centers has grown as the population grows increasingly connected and dependent on digital infrastructure. Effective cooling solutions are urgently needed to ensure optimal performance and avoid expensive downtime due to the data center development and growth spike.

Key Highlights

- Data center growth has been significantly aided by the uptake of cloud computing solutions and the spread of big data analytics. Businesses increasingly rely on cloud-based services and storing enormous amounts of data for processing and research. For instance, to meet the rising demand, cloud industry giants like Amazon Web Services (AWB), Microsoft Azure, and Google Cloud Platform continuously extend their data center footprints.

- Growing developments in IT infrastructure in emerging economies, such as India, Hong Kong, China, Indonesia, and other emerging countries, are likely to boost the demand for data centers. The demand for data centers is expected to increase due to the adoption of the cloud model, which has cost and operational benefits for the IT industry.

- Data center operators are wary of potential downtime losses while shifting to new cooling systems. Hence, they overlook operational expenditures and continue using outdated cooling systems. This trend slows the adoption of new technologies that are perceived to be untested.

- A new wave of post-pandemic digital transformation among businesses is expected to drive the market. Many companies have started to rely on third-party colocation facilities to house their data centers, and there's a growing trend towards hybrid IT - combining the power of hosted centers with multi-cloud environments.

Data Center Liquid Cooling Market Trends

Edge Computing to Witness Significant Growth

- In the forecast period, organizations are expected to witness rapid growth in the number of IP-connected mobile and machine-to-machine (M2M) devices, which will handle significant amounts of IP traffic.

- The demand is expected to rise for faster Wi-Fi service and application delivery from online providers. Also, some M2M devices, such as autonomous vehicles, will require real-time communications with local processing resources to guarantee safety.

- The deployment of edge data centers benefits many new technologies, including fifth-generation (5G) networks and the Internet of Things (IoT), as the adoption of (IoT) connections is expected to more than double, with the number of wide-area IoT 6 billion by 2028. and Industrial Internet of Things (IIoT) of devices, autonomous vehicles, virtual and augmented reality, artificial intelligence and machine learning, data analytics, and video streaming and surveillance.

- Moreover, the emergence of 5G wireless infrastructure has urged data center operators to opt for edge computing infrastructure to work with networks offering lower latency and higher resiliency. Multi-access edge computing (MEC) aids network services in connecting to users closely. Hence, the demand for efficient edge data centers is expected to be augmented by many factors, including the introduction of 5G technology across the world and the growing trend of autonomous or self-driving vehicles and smart cities.

- However, a key requirement of large-scale edge computing roll-outs will be low operating costs. In edge deployments, immersive liquid cooling is known to provide dramatic energy-saving benefits.

- The reliability and no-touch features of liquid cooling solutions will match the need for extended mean time to maintenance and longer intervention intervals needed for viable operation and management of remotely located equipment.

North America to Hold the Largest Market Share

- North America is an early adopter of newer technologies. The data center investors are increasingly investing in liquid immersion and direct-to-chip cooling solutions. The importance of edge data centers has been aided by the emergence of 5G networks worldwide, and the United States is among the earliest adopters of the technology. Many operators in the United States, such as EdgePresence, EdgeMicro, and American Towers, have started investing in these centers.

- The mobile data traffic in the United States increased considerably over the years, from 1.26 exabytes per month of data traffic in 2017 to 7.75 exabytes per month of data traffic by 2022, as reported by Cisco Systems. Ericsson says this data traffic is expected to triple further by 2030. Thus, the distributed cloud that may secure the low latency and high bandwidth required to connect such scale easily is coming into action.

- The United States is witnessing massive growth in internet usage by people and businesses. The country is the largest market in data center operations, and it continues to grow due to the higher consumption of data by end-users. The growing popularity of the Internet of Things (IoT) is a significant driver for the US hyper-scale data center market, leading to additional facilities that can support exabytes of data generated by both business users and consumers.

- The United States will be the fastest-growing data center market in the region in the coming years. The significant drivers of data center construction in the United States. have been recent economic incentives and tax benefits. Approximately 27 states leverage these factors to attract data center projects. In addition, the heavy tax breaks implemented in the United States indicate a government-front aim to construct new mega data centers or renovate existing ones. Such instances in the market create more of a need for data center liquid cooling services in the region.

Data Center Liquid Cooling Industry Overview

The data center liquid cooling market is fragmented and highly competitive and consists of several significant players like Alfa Laval Corporate AB, LiquidStack Inc., Asetek Inc. A/S, AsperitasChilldyne Inc., etc. In terms of market share, few important players currently dominate the market. The widely deployed cooling system is still air cooling, and liquid cooling systems have a relatively small share in the overall cooling landscape. As relatively high costs are considered market challenges, the immersion cooling systems market is estimated to have a significant threat of substitutes.

- March 2024 - Summer announced its membership in the recently established Liquid Cooling Coalition (LCC), a premier industry forum comprised of stakeholders, including industrial coolant producers, original equipment manufacturers, original device manufacturers, high-performance computing application operators, and data center providers.

- March 2024 - Vertiv, a significant provider of critical infrastructure and continuity solutions, is now a Solution Advisor: Consultant partner in the Nvidia Partner Network (NPN), providing more comprehensive access to Vertiv's experience and complete power and cooling solutions portfolio.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Evolution Of Data Center Cooling

- 4.1.1 Air Conditioners/Handlers

- 4.1.2 Chillers And Economizer Systems

- 4.1.3 Liquid Cooling Systems

- 4.1.4 Row/Rack/Ddoor/Over-head Cooling Systems

- 4.2 Overview of Data Center Cooling Market

- 4.3 Energy Consumption, Computing Density Metrics and Key Considerations For Liquid Cooling

- 4.4 Industry Stakeholder Analysis

- 4.5 Industry Attractiveness - Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Buyers

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Threat of New Entrants

- 4.5.4 Degree of Competition

- 4.5.5 Threat of Substitutes

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Development of IT Infrastructure in the Region

- 5.1.2 Emergence of Green Data Centers

- 5.2 Market Restraints

- 5.2.1 Costs, Adaptability Requirements, and Power Outages

- 5.3 Assessment of COVID-19 Impact on the Industry

6 OUTLOOK OF REAR DOOR HEAT EXCHANGERS (RDHX) IN DATA CENTERS

- 6.1 Technical Comparison of RDHx and Liquid Cooling (Direct and Indirect) in Data Centers

- 6.2 Recent Developments by Data Center Cooling Technology Vendors in the Context Of RDHx and Liquid Cooling Market

- 6.3 Approximate Global Market Share of RDHx (in USD Billion)

- 6.4 List of Key RDHx Vendors (Business Overview, Portfolio and Recent Developments)

7 DIRECT COOLING OR IMMERSION COOLING MARKET

- 7.1 Direct Cooling Market Overview And Estimate

- 7.2 Immersion Cooling - Key Application

- 7.2.1 High-performance Computing

- 7.2.2 Edge Computing

- 7.2.3 Cryptocurrency Mining

- 7.3 Immersion Cooling Fluids

- 7.3.1 Fluorocarbon-based Fluids

- 7.3.2 Hydrocarbons Fluids

8 INDIRECT OR DIRECT-TO-CHIP COOLING MARKET

- 8.1 Indirect Cooling Market Overview and Estimates

- 8.2 Indirect or Direct-to-chip Cooling Key Applications

9 MARKET SEGMENTATION

- 9.1 By Geography***

- 9.1.1 North America

- 9.1.2 Europe

- 9.1.3 Asia

- 9.1.4 Australia and New Zealand

- 9.1.5 Latin America

- 9.1.6 Middle East and Africa

10 COMPETITIVE LANDSCAPE

- 10.1 Company Profiles*

- 10.1.1 Alfa Laval Corporate AB

- 10.1.2 LiquidStack Inc.

- 10.1.3 Asetek Inc. A/S

- 10.1.4 Asperitas

- 10.1.5 Chilldyne Inc.

- 10.1.6 CoolIT Systems Inc.

- 10.1.7 Fujitsu Ltd.

- 10.1.8 Mikros Technologies

- 10.1.9 Kaori Heat Treatment Co. Ltd

- 10.1.10 Lenovo Group Limited

- 10.1.11 LiquidCool Solutions Inc.

- 10.1.12 Midas Green Technologies

- 10.1.13 Iceotope Technologies Ltd

- 10.1.14 USystems Ltd (Legrand Group)

- 10.1.15 Rittal GmbH & Co. KG

- 10.1.16 Schneider Electric

- 10.1.17 Submer Technologies & Submer Inc.

- 10.1.18 Vertiv Group Corp.

- 10.1.19 Wakefield Thermal Solutions Inc.

- 10.1.20 Wiwynn Corporation

- 10.1.21 3M Company

- 10.1.22 Engineered Fluids Inc.

- 10.1.23 Green Revolution Cooling Inc.

- 10.1.24 Solvay SA