|

시장보고서

상품코드

1549845

재사용 푸드서비스 포장 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2024-2029년)Reusable Foodservice Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

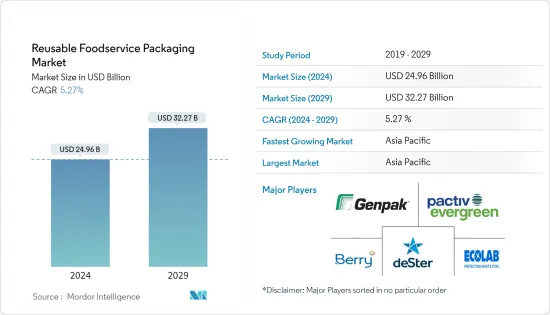

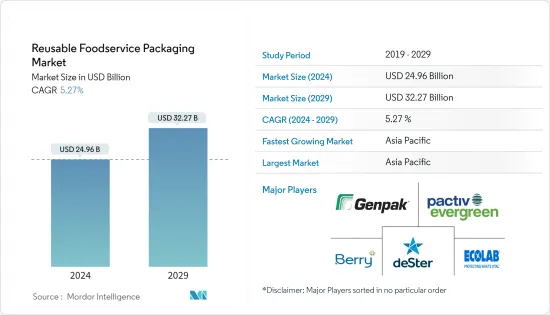

세계 재사용 푸드서비스 포장 시장 규모는 2024 년에 249 억 6,000만 달러로 추정되며, 2029 년에는 322 억 7,000만 달러에 이르렀으며 예측 기간(2024 - 2029)에 CAGR5. 27%로 성장할 것으로 예측됩니다.

세계 재사용 포장 시장은 내구성 있고 지속가능한 자재관리 솔루션에 대한 요구가 증가함에 따라 큰 성장을 이루려고 합니다. 리터너블 포장은 지속가능성에 있어서 매우 중요한 역할을 하며, 일반적으로 매립지로 가는 포장폐기물의 양을 억제함으로써 두드러집니다.

주요 하이라이트

- 다양한 도시 경관이 편리하고 운반에 편리한 경량 식품에 대한 국가 수요를 뒷받침하고 있습니다. 최근 몇 년동안 먹고 편리한 음식은 세계 음식 서비스 중 가장 다양한 부문 중 하나로 발전하고 있습니다. 환경에 대한 관심이 높아지고 포장 매립 쓰레기가 급증하는 가운데 호텔, 풀서비스 레스토랑(FSR), 퀵 서비스 레스토랑(QSR)에서는 재사용 푸드서비스 포장이 사용되고 있습니다.

- 세계의 일부 정부 기관은 부문에 관계없이 재사용 포장을 사용하기위한 엄격한 지침을 부과합니다. 예를 들어, SUP 지령은 EU 회원국에 대해 일회용 플라스틱 폐기물을 적극적으로 삭감할 것을 의무화하고 있으며, 지방 수준과 국가 수준에서 구체적인 삭감 목표를 설정하고 있습니다. 규제와 병행하여, 이들 국가는 이러한 목표를 달성하기 위해 재사용 식품 포장을 제안합니다.

- 프랑스에서는 최근의 법률에 따라 시설 내 식사와 스낵은 모두 재사용 포장과 식기를 사용하여 먹어야합니다.

- 지난 몇 년동안 온라인 식품 주문 및 레스토랑 배달 부문은 20% 성장했습니다. 온라인 식품 배달 시스템이 보급됨에 따라 지속 가능한 푸드서비스 포장에 대한 수요도 급증하고 있습니다. 중국 인터넷 네트워크 정보 센터가 2024년 3월에 발표한 바에 따르면, 중국의 온라인 푸드 딜리버리 이용자 수는 2020년 4억 1,883만명에서 2023년에는 무려 5억 4,454만명으로 증가했습니다. 이 증가로 인해 각 제조업체는 환경 친화적 인 재사용 포장 솔루션으로 이동합니다.

- 그러나 산업용 식품 응용 분야에서 플라스틱 포장의 일회용 모델에서 재사용 모델로의 전환은 특히 위생 및 지각면에서 예기치 않은 과제를 초래할 수 있습니다. 플라스틱 포장의 재사용은 식품 내 화학물질 오염과 미세 플라스틱 입자의 존재를 증가시키는 위험을 수반합니다. 또한 포장된 상품의 위생 기준과 지각적인 일관성이 손상될 수 있습니다.

- 전 세계적으로 대기업은 전통적인 '잡고 채우고 버리는' 모델에서 폐기물 0의 라이프 스타일로 전환하고 있습니다. 이는 푸드서비스 포장을 재사용할 수 있게 함으로써 라이프사이클을 지속가능한 형태로 연장함으로써 실현됩니다. 이 시프트는 포장과 관련된 운영 비용을 줄일뿐만 아니라 지속적으로 새로운 포장을 구입할 필요가 없습니다.

재사용 푸드서비스 포장 시장 동향

퀵서비스 레스토랑(QSR) 수요 증가가 시장을 뒷받침

- 빠른 서비스 레스토랑(QSR)은 서비스 속도에 중점을두고 저렴한 가격의 식사 옵션을 제공합니다. 테이블 서비스는 최소한으로 유지되며 셀프 서비스를 중시하는 점이 기존 레스토랑과 다릅니다. QSR에서 식품 및 음료는 먹기 전에 요금을 지불합니다. 지난 10년간, 특히 이들 국가의 지역 푸드서비스 시장에서는 여러 국제 QSR 체인과 변화하는 소비자의 취향에 맞는 다양한 요리를 제공하는 자국 브랜드의 성장이 보였습니다.

- 환경의 지속가능성에 대한 의식이 높아지는 가운데, 대기업 QSR 체인 몇몇사는 재활용 가능성, 퇴비화 가능성, 재사용 포장에 점점 힘을 쓰게 되고 있습니다. Burger King, McDonald's, and Wendy와 같은 유명 기업은 재사용 포장을 채택한다는 것을 표명합니다.

- 예를 들어, 프랑스 McDonald는 식사를 한 고객에게 21유형의 재사용 용기를 제공합니다. 그 중에는 감자 튀김을 위한 빨간 플라스틱 용기, 투명한 플라스틱 음료용 유리, 치킨 너겟용 백색 플라스틱 컵 등이 있습니다.

- 프랜차이즈 모델은 QSR 체인의 상승에 매우 중요하며 향후 시장 성장을 세계에서 촉진할 것으로 예상됩니다. 국제 프랜차이즈 협회(International Franchise Association)가 발표한 데이터에 따르면, 2024년 4월 미국의 QSR 수는 COVID-19의 대유행 시 약간 감소한 후 지난 수년간 꾸준히 증가하여 2020년의 18만 3,540점에서 2023년에는 19만 5,510점으로 증가했습니다. 특히 추정에 따르면 예측 기간 동안 미국의 QSR 수가 더욱 개선될 것으로 예상됩니다.

- 게다가 이동 중에 식사에 대한 선호도가 높아짐에 따라 식비가 증가함에 따라 QSR 수요가 증가하고 재사용 후드 서비스용 포장의 필요성이 부각되고 있습니다. 국가 통계국(영국)에 따르면 영국 식당과 카페에 대한 소비자 지출은 유행 후 기간에 급증하여 1,328억 9,000만 파운드(1,695억 달러)에 달했습니다. 이 지출 증가는 시장에 긍정적인 영향을 미칠 것으로 예상됩니다.

- 현재, 특히 밀레니얼 세대와 Z 세대는 자신들의 핵심이 되는 가치관에 공명하는 브랜드와 장소를 적극적으로 요구하고 있습니다. 전반적으로 QSR은 자사의 가치관을 적극적으로 어필함으로써 투명성과 신뢰성을 요구하는 소비자의 요구에 부응할 수 있습니다. 이는 지속가능한 방식으로 조달된 재료와 재활용 가능하고 재사용 가능한 포장을 특징으로 하는 모금활동 및 프로모션과 같은 노력을 통해 달성될 수 있습니다.

예측기간 중 아시아태평양이 큰 시장 점유율을 차지할 전망

- 아시아태평양에는 중국과 인도 등 인구 밀도가 높은 신흥 경제국이 있어 푸드서비스 수요가 급증하고 있습니다. 시장은 편의성에 대한 수요의 급증, 보다 건강한 식생활의 선택에 대한 축족에 의해 추진되고 있으며, 그 결과 지속가능한 포장의 채용이 현저하게 증가하고 예측기간 동안 피크에 달할 것으로 예측됩니다. 이러한 동향은 이 지역을 기술 혁신과 비즈니스 성장의 중심지로 변모시킬 전망입니다.

- 이 지역에서는 이동식 푸드서비스 스테이션 수요가 급증하고 있습니다. 이 급증의 주요 요인은 도시화의 진전, 점점 바쁜 라이프 스타일, 이동 중에 식사에 대한 욕구 증가입니다.

- 예를 들어, 2023년 6월, 홍콩의 학생 주도 푸드 서비스 신흥 기업이 재사용 사발의 환경 친화적인 임대 서비스를 시작했습니다. 이 혁신적인 이니셔티브에는 11개의 레스토랑, 300명의 등록 사용자가 참여합니다. 이러한 지역적인 움직임은 외식산업에서 재사용 제품 포장의 인지도를 높일 것으로 보입니다.

- 아시아태평양에서의 플라스틱 오염의 급증은 플라스틱 폐기물의 감소와 지속 가능한 포장 솔루션의 촉진을 목표로 하는 정책의 이행을 아시아태평양 전역의 정부에 촉구하고 있습니다. 2022년 인도 정부는 외식 산업을 비롯한 여러 분야에서 일회용 플라스틱 금지를 도입하여 이 나라 전체에서 여러 번 사용할 수 있는 포장 제품에 대한 수요가 가속화되고 있습니다.

- 게다가 노동 인구 증가와 바쁜 라이프 스타일에 따라 일본, 중국, 인도, 인도네시아 등의 국가에서도 외식에 대한 소비 지출이 증가하고 있습니다. 예를 들면, 총무성·통계국이 2024년 2월에 발표한 보고서에 의하면, 일본에 있어서의 외식에의 연간 평균 세대 지출액은 2021년의 8,110엔(51달러)부터 2023년까지의 불과 3년간으로 1만 1,110엔(70달러)으로 급증하고 있습니다.

재사용 푸드서비스 포장 산업 개요

조사 대상 시장은 단편화되고 있으며, 선도적인 벤더가 시장 점유율의 대부분을 차지하고 있습니다. 시장에 많은 기업이 존재하는 것은 서비스의 가격 설정에 영향을 미치며, 특히 소규모 벤더에게는 직접적인 경쟁 요인이 되고 있습니다. 조사 대상 시장의 벤더는 원 스톱 숍 서비스의 제공에 주력해, 경쟁 우위에 선다고 보여집니다. 시장의 주요 기업으로는 Berry Global Inc., Ecolab Services, Genpak LLC, Enpak Enterprise 등이 있습니다.

- 2024년 2월: Berry Global은 외식 산업에서 지속가능한 포장에 대한 수요 증가에 대응하기 위해 재사용 식기 시리즈를 출시했습니다. 이 움직임은 법률과 소비자의 요구가 보다 환경 친화적인 포장 솔루션으로 이 업계를 밀어 올리고 있기 때문입니다. 이 회사의 푸드서비스 부문 담당 부사장에 따르면, 재사용 식기의 새로운 시리즈는 폐기물을 줄이고 새로운 자원에 대한 의존성을 줄이고 법률 기준을 충족하면서 기능과 내구성을 보장할 목적입니다.

- 2024년 5월: 서비스웨어 및 식품 포장을 개발하는 deSter와 특수 소재 기업인 Eastman이 공동으로 재사용 기내용 드링크웨어를 항공사에 도입했습니다. 이 포장에는 재생 분자 코폴리에스터로 만든 특수 플라스틱인 Tritan Renew가 사용됩니다. 이 소재는 배포 중에 플라스틱 폐기물을 기본 화학 성분으로 분해하여 여러 재활용 사이클을 가능하게합니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

- 시장 개요

- 업계의 매력도 - Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 대체품의 위협

- 신규 참가업체의 위협

- 경쟁 기업간 경쟁 관계

- 업계 밸류체인 분석

- 최근의 지정학적 시나리오가 업계에 미치는 영향의 평가

- 현재 시나리오에서 재사용형 및 단일 사용형 안전한 솔루션

제5장 시장 역학

- 시장 성장 촉진요인

- 온라인 식품 택배 서비스 수요 증가

- 환경 지속성에 대한 의식의 고조와 일회용 플라스틱 포장에 대한 엄격한 규제

- 시장 성장 억제요인

- 플라스틱 포장 재사용으로 인한 예기치 않은 결과와 건강에 대한 우려

제6장 시장 세분화

- 재료 유형별

- 금속

- 플라스틱

- 유리

- 기타 재료 유형

- 제품 유형별

- 골판지와 판지

- 병과 유리

- 트레이, 접시, 식품 용기, 그릇

- 컵과 뚜껑

- 클램쉘

- 기타 제품 유형

- 최종 사용자 산업별

- 퀵 서비스 레스토랑(QSR)

- 풀 서비스 레스토랑(FSR)

- 기관

- 접객

- 기타 최종 사용자 산업

- 지역별

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 아시아태평양

- 중국

- 일본

- 인도

- 호주 및 뉴질랜드

- 라틴아메리카

- 브라질

- 아르헨티나

- 멕시코

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 남아프리카

- 북미

제7장 경쟁 구도

- 기업 프로파일

- Berry Global Inc.

- Ecolab services

- deSter Corporation

- Genpak LLC

- Pactiv Evergreen Inc.

- Limepack

- Re:Dish Co.

- Verive

- Evergreen Packaging

- Enpak Enterprise Co. Ltd

제8장 투자 분석

제9장 시장 기회와 앞으로의 동향

JHS 24.09.24The Reusable Foodservice Packaging Market size is estimated at USD 24.96 billion in 2024, and is expected to reach USD 32.27 billion by 2029, growing at a CAGR of 5.27% during the forecast period (2024-2029).

The global reusable packaging market is set for significant growth, fueled by a rising need for durable and sustainable material handling solutions. Returnable packaging stands out for its pivotal role in sustainability, curbing the volume of packaging waste that typically ends up in landfills.

Key Highlights

- A diverse urban landscape drives the country's demand for convenient, on-the-go, lightweight foods. In recent years, ready-to-eat and convenient food has evolved into one of the most diverse segments of the global food service, with rising concern about the environment and the escalation in packaging landfills, reusable food service packaging in hotels, full-service restaurants (FSRs), and quick-service restaurants (QSRs).

- Several government bodies worldwide impose strict guidelines for using reusable packaging across sectors. For instance, the SUP Directive mandates that EU Member States actively reduce single-use plastic waste, setting specific reduction targets at local and national levels. In tandem with restrictions, these states are advocating for reusable food packaging to achieve these goals.

- In France, recent legislation mandates that all on-site meals or snacks be consumed using reusable packaging or crockery.

- Over the past few years, the online food ordering and restaurant delivery sector has grown by 20%. As the online food delivery system gains traction, there is a corresponding surge in demand for sustainable food service packaging. As per the China Internet Network Information Center publication in March 2024, the number of online food delivery users in China rose from 418.83 million in 2020 to a whopping 544.54 million in 2023. This uptick is prompting manufacturers to pivot toward eco-friendly reusable packaging solutions.

- However, transitioning from a single-use to a reuse model for plastic packaging in industrial food applications can introduce unforeseen challenges, particularly in hygiene and sensory perception. Reusing plastic packaging carries the risk of heightening chemical contamination and the presence of microplastic particles in food products. Additionally, it may compromise the packaged goods' hygienic standards and sensory consistency.

- Globally, large companies are shifting from the traditional 'catch, fill, and waste' model to a zero-waste lifestyle. They achieve this by making foodservice packaging reusable, thus extending its lifecycle sustainably. This shift not only cuts down on operational costs tied to packaging but also eliminates the need for continual new packaging purchases.

Key Highlights

Reusable Foodservice Packaging Market Trends

Growing Demand From Quick-service Restaurants (QSR) Aids the Market

- Quick-service restaurants (QSRs) offer low-cost food options, focusing on speed of service. Minimal table service and an emphasis on self-service distinguish this group from traditional restaurants. Food and beverages are paid for before consumption at QSRs. Over the last decade, the regional foodservice market, specifically for these countries, has witnessed the growth of several international QSR chains and home-grown brands offering varied cuisines suiting changing consumer preferences.

- With rising awareness of environmental sustainability, several major QSR chains are increasingly focusing on recyclability, compostability, and reusable packaging. Notable players, including Burger King, McDonald's, and Wendy's, have pledged to adopt reusable packaging.

- For instance, McDonald's in France offers 21 reusable containers for dine-in customers. These include red plastic containers for fries, clear plastic beverage glasses, and white plastic cups designed for chicken nuggets.

- The franchise model will be crucial to the rise of QSR chains, which is expected to fuel market growth across the globe in the upcoming period. According to the data published by the International Franchise Association, in April 2024, after a slight downfall during the COVID-19 pandemic, the number of QSR in the United States rose steadily in the past few years from 183.54 thousand in 2020 to 195.51 thousand in 2023. Notably, as per the estimates, the number of QSRs across the country is expected to further improve during the forecast period.

- Further, increased spending on food, driven by a rising preference for on-the-go eating, has bolstered the demand for QSRs, fueling the need for reusable food service packaging. As per the Office for National Statistics (United Kingdom), consumer spending on restaurants and cafes in the United Kingdom skyrocketed in the post-pandemic period to GBP 132.89 billion (USD 169.50 billion). This bolstered spending is expected to consequently impact the market positively.

- Presently, millennials and Gen Z, in particular, actively seek out brands and places that resonate with their core values. Overall, QSRs can align with consumer demands for transparency and authenticity by actively showcasing their values. This can be achieved through initiatives like fundraisers and promotions, which feature sustainably sourced ingredients and recyclable and reusable packaging.

Asia-Pacific is Expected to Hold a Significant Market Share During the Forecast Period

- Asia-Pacific is home to densely populated and emerging economies such as China and India, and the demand for food services is surging. The market is propelled by a surge in demand for convenience, a pivot toward healthier dietary choices, and consequently, a notable uptick in adopting sustainable packaging is projected to peak during the forecast period. These trends transform the region into a technological innovation and business growth center.

- The region is witnessing a rapid surge in the demand for mobile food service stations. This uptick is primarily driven by escalating urbanization, increasingly busy lifestyles, and a heightened appetite for on-the-go dining.

- For instance, in June 2023, a Hong Kong student-led food service start-up introduced an eco-friendly rental service for reusable bowls. Eleven restaurants with 300 registered users have joined this innovative initiative. Such regional developments would bolster the awareness of reusable product packaging in the foodservice sector.

- The surge in plastic pollution in Asia-Pacific has prompted governments across the region to implement policies that aim to reduce plastic waste and promote sustainable packaging solutions. In 2022, the Government of India introduced a ban on single-use plastic in several sectors, including food service, thereby accelerating the demand for multiple-use packaging products across the country.

- Further, with the growing working population and busy lifestyles, consumer spending on eating outside is also increasing in countries like Japan, China, India, and Indonesia. For instance, according to the Ministry of Internal Affairs and Communications (Japan) and Statistics Bureau of Japan's report published in February 2024, the annual average household expenditure on dining out in Japan increased rapidly from JPY 8.11 thousand (USD 0.051 thousand) in 2021 to JPY 11.11 (USD 0.070 thousand) in just three years ending 2023.

Reusable Foodservice Packaging Industry Overview

The market studied is fragmented, with major vendors accounting for most of the market share. The presence of many players in the market impacts the pricing of services, making it a direct competing factor, especially for small-scale vendors. The vendors in the market studied are expected to focus on providing one-stop-shop services, giving them a competitive advantage. Some of the major players in the market are Berry Global Inc., Ecolab Services, Genpak LLC, and Enpak Enterprise Co. Ltd.

- February 2024: Berry Global launched its Reusable Tableware Range to address the incremental demand for sustainable packaging across the food service industry. This move comes as legislation and consumer demands push the sector towards more eco-friendly packaging solutions. According to the company's Vice President of Food Service division, the new range of reusable tableware aims to cut waste, lessen reliance on new resources, and ensure functionality and durability while meeting legislative standards.

- May 2024: deSter, a developer of serviceware and food packaging, and Eastman, a specialty materials company, collaborated to introduce reusable in-flight drinkware to the airline sector. The packaging utilizes Tritan Renew, a specialty plastic crafted from recycled molecular copolyester. During its development, plastic waste is broken down into its fundamental chemical components, enabling the material to undergo multiple recycling cycles.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of Substitutes

- 4.2.4 Threat of New Entrants

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of Impact of Recent Geopolitical Scenario on the Industry

- 4.5 Reusable vs Single-user Safer Solution in Current Scenario

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Demand In Online Food Delivery Service

- 5.1.2 Incremental Awareness For Environmental Sustainability and Stringent Regulations Against Single-Use Plastic Packaging

- 5.2 Market Restraints

- 5.2.1 Unforeseen Consequences of Reusing Plastic Packaging and Health Related Concerns

6 MARKET SEGMENTATION

- 6.1 By Material Type

- 6.1.1 Metal

- 6.1.2 Plastic

- 6.1.3 Glass

- 6.1.4 Other Material Types

- 6.2 By Product Type

- 6.2.1 Corrugated Boxes And Cartons

- 6.2.2 Bottles and Glasses

- 6.2.3 Trays, Plates, Food Containers, and Bowls

- 6.2.4 Cups And Lids

- 6.2.5 Clamshells

- 6.2.6 Other Product Types

- 6.3 By End-user Industry

- 6.3.1 Quick-service Restaurants (QSR)

- 6.3.2 Full-service Restaurants (FSR)

- 6.3.3 Institutional

- 6.3.4 Hospitality

- 6.3.5 Other End-user Industries

- 6.4 By Geography

- 6.4.1 North America

- 6.4.1.1 United States

- 6.4.1.2 Canada

- 6.4.2 Europe

- 6.4.2.1 United Kingdom

- 6.4.2.2 Germany

- 6.4.2.3 France

- 6.4.2.4 Italy

- 6.4.2.5 Spain

- 6.4.3 Asia-Pacific

- 6.4.3.1 China

- 6.4.3.2 Japan

- 6.4.3.3 India

- 6.4.3.4 Australia and New Zealand

- 6.4.4 Latin America

- 6.4.4.1 Brazil

- 6.4.4.2 Argentina

- 6.4.4.3 Mexico

- 6.4.5 Middle East and Africa

- 6.4.5.1 Saudi Arabia

- 6.4.5.2 United Arab Emirates

- 6.4.5.3 South Africa

- 6.4.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Berry Global Inc.

- 7.1.2 Ecolab services

- 7.1.3 deSter Corporation

- 7.1.4 Genpak LLC

- 7.1.5 Pactiv Evergreen Inc.

- 7.1.6 Limepack

- 7.1.7 Re:Dish Co.

- 7.1.8 Verive

- 7.1.9 Evergreen Packaging

- 7.1.10 Enpak Enterprise Co. Ltd