|

시장보고서

상품코드

1627138

북미의 유리병/용기 : 시장 점유율 분석, 산업 동향 및 성장 예측(2025-2030년)North America Glass Bottles/Containers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

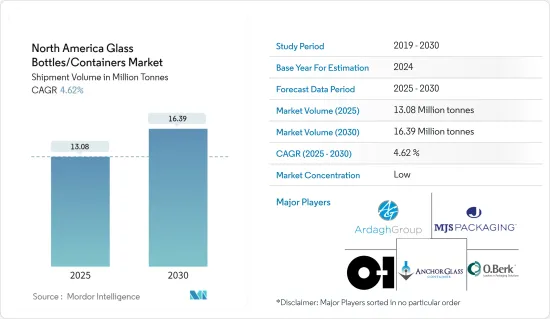

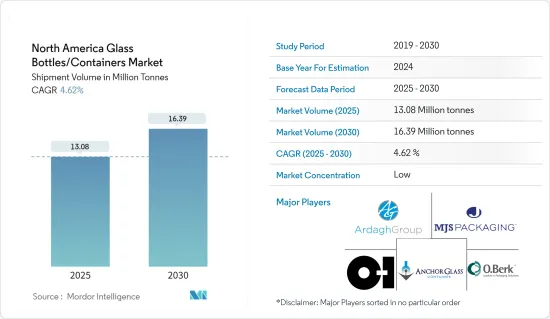

북미의 유리병/용기 시장 규모(출하량 기준)는 2025년 1,308만 톤에서 2030년 1,639만 톤으로 확대될 것이며, 예측 기간(2025-2030년) 동안 4.62%의 연평균 복합 성장률(CAGR)을 나타낼 것으로 예상됩니다.

주요 하이라이트

- 북미의 유리병/용기 시장은 식음료, 화장품, 의약품 등의 부문에서 소비 확대에 힘입어 성장세를 보이고 있습니다. 소비자들이 안전하고 건강한 포장을 점점 더 우선시함에 따라 유리는 다양한 카테고리로 진출하고 있습니다. 특히 음료 부문에서 이러한 추세가 두드러지고 있으며, 고급 제품 및 공예 음료는 종종 유리 병에 담겨 있습니다.

- 또한 엠보싱, 성형 및 예술적 마감의 최첨단 기술은 유리 포장의 매력을 더욱 높여주고 있습니다. 이러한 기술 혁신은 사용자 정의 및 브랜딩을 강화할 뿐만 아니라 눈에 띄는 포장을 원하는 기업에게 유리 용기를 강력한 선택으로 만들고 있습니다. 업계의 경량 유리 기술에 대한 노력은 운송 비용과 환경 영향에 대한 우려를 해결하고 시장 확대에 더욱 박차를 가하고 있습니다.

- 미국에서는 알코올 음료 소비가 급증하면서 포장, 특히 유리병에 대한 수요가 증가하고 있습니다. 이러한 수요는 알코올 음료의 유형이 확대되고 소비자의 고급 포장에 대한 선호도를 반영하고 있습니다. 유리병이 선호되는 이유는 재활용성과 고급스러움뿐만 아니라 음료의 품질과 맛을 유지하는 능력이 뛰어나기 때문입니다. 수제 맥주 트렌드와 장인정신이 깃든 주류의 등장은 최고급 유리 포장에 대한 욕구를 더욱 증폭시키고 있습니다.

- 2023년 미국 약물 남용 및 건강 조사(NSDUH) 데이터에 따르면, 미국 성인 2억 1,870만 명(18세 이상 84.9%)이 알코올을 섭취한 경험이 있는 것으로 나타났습니다. 이러한 대규모 소비자 기반은 음료 부문의 다양한 포장 솔루션에 대한 안정적인 수요를 보장합니다. 다재다능하고 매력적인 유리병은 여전히 주류이며, 제조업체들은 생산자와 소비자 모두의 변화하는 취향에 대응하기 위해 혁신을 거듭하고 있습니다.

- Glass Global의 보고서에 따르면 북미의 유리병/용기 생산량은 부문별로 838만 9,233톤, 연간 생산 능력은 932만 1,370톤으로 나타났습니다. 이는 이 지역이 유리 포장 부문에서 확고한 입지를 구축하고 있음을 강조합니다. 탄탄한 생산 능력과 생산량은 강력한 인프라뿐만 아니라 식음료, 의약품, 화장품 등 다양한 산업에 걸친 강력한 수요를 보여줍니다.

- 또한 국제 무역 센터의 데이터에 따르면 미국은 약 141,143 톤의 유리 포장을 수출하고 있습니다. 이는 유리 포장 부문에서 빠르게 성장하는 기회를 보여줄뿐만 아니라 북미 유리 제품에 대한 국제적인 수요를 강조합니다. 상당한 국내 생산과 상당한 수출의 조합은 북미 유리 포장 산업의 강점과 성장 궤도를 강조하고 있습니다.

- 이 지역에서는 다양한 분야에서 유리병/용기가 채택되고 있으며, 재활용이 중요한 초점이 되고 있습니다. 식음료, 제약, 화장품 등의 산업에서 유리병/용기의 사용량이 증가함에 따라 유리 폐기물이 대량으로 발생합니다. 효율적인 재활용은 폐기물 관리, 환경 영향 최소화 및 지속가능성 증진에 필수적입니다. 정부 규제가 지속 가능한 포장에 초점을 맞추고 있기 때문에 제조업체는 점점 더 유리 솔루션으로 눈을 돌리고 있습니다. 이러한 역학은 북미 유리 포장 시장의 성장을 가속하고 있습니다.

북미의 유리병/용기 시장 동향

알코올 음료 부문이 큰 성장을 이룰 것으로 예상

- 알코올 음료 제조업체들은 유리병에 담긴 신제품을 출시하고 있으며, 이러한 움직임은 시장에 긍정적인 영향을 미칠 것으로 예상됩니다. 유리 포장을 채택함으로써 이들 제조업체는 제품의 매력을 높이고 소비자의 인식을 재구성하고 유리와 관련된 고급스러운 이미지를 활용하고자 합니다. 유리병은 제품의 맛과 품질을 보다 효과적으로 보존할 뿐만 아니라 재활용성 향상과 고급스러움도 함께 기재하고 있습니다. 많은 소비자들은 유리 포장을 우수한 음료 품질과 동일시하며 종종 프리미엄 가격을 정당화합니다.

- 또한 유리는 독특하고 독창적인 병 디자인을 가능하게 하여 브랜드가 매장에서 차별화를 꾀할 수 있습니다.

- 유리 포장으로의 전환은 지속 가능하고 친환경적인 선택에 대한 소비자의 요구가 높아지는 추세와 맞물려 있습니다.

- 예를 들어, 2024년 9월, Diageo 산하의 Johnnie Walker는 스카치 위스키에 맞게 조정된 세계에서 가장 가벼운 700ml 유리병인 '블루 라벨 울트라(Blue Label Ultra)'를 한정판으로 출시했습니다. 이 선구적인 패키징은 지속가능한 위스키 병입의 획기적인 도약을 보여줍니다.

- 북미 맥주 포장 부문은 진화하는 문화 트렌드, 인구 증가, 도시화, 젊은 층의 맥주 인기 급상승의 영향을 크게 받고 있습니다. 지속적인 투자와 지역 간 맥주 유통망 확대는 이러한 추세를 유지하고 유리병/용기 시장을 활성화시킬 수 있습니다.

- 2024년 3월부터 5월까지 미국의 병맥주 및 캔맥주 생산량은 1,041만 배럴에서 1,247만 배럴 사이를 오가며 포장맥주에 대한 미국 수요를 뒷받침하고 있습니다. 1% 감소할 것으로 예상되는 시장은 맥주 소비량 증가 추세를 뒷받침하고 있습니다.

- 생산량과 수입량 감소는 소비자 선호도 변화, 경제적 요인 또는 규제 변경으로 인한 것일 수 있습니다. 그러나 맥주 소비량 증가는 새로운 맥주 품종, 마케팅 강화 및 소비자 행동의 진화에 의해 촉진될 새로운 맥주 품종, 소비자 행동의 진화에 의해 촉진될 수 있는 산업의 미개척 성장과 혁신의 잠재력을 시사하고 있습니다.

- 북미에서는 지속 가능한 라이프스타일을 추구하는 소비층이 확대되고 있으며, 특히 플라스틱 폐기물을 줄이기 위한 노력이 활발히 진행되고 있습니다. 이러한 움직임은 와인 및 주류 시장에서 유리병으로의 전환을 촉진하고 있습니다. 많은 소비자들이 유리병이 플라스틱보다 친환경적이고 고급스러운 제품으로 인식하고 있습니다. 이러한 인식은 환경에 대한 인식이 높은 소비자들의 공감을 불러일으키며, 지속 가능한 포장에 대한 대가를 기꺼이 지불할 의향이 있는 경우가 많습니다. 또한, 플라스틱 사용량을 줄이기 위한 정부 규제가 곧 시행될 예정이어서 알코올 음료 부문에서 유리병에 대한 수요는 더욱 증가할 것으로 보입니다.

미국이 주요 시장 점유율을 차지할 것으로 예상

- 미국은 세계 최대 포장 시장 중 하나이며, 식음료, 퍼스널케어, 의약품 등 다양한 산업을 위한 유리병과 용기를 제조하는 주요 기업들이 다수 존재합니다. 미국의 경제 성장과 식품, 음료, 의약품, 퍼스널케어 제품에 대한 소비 지출 증가가 유리병 및 용기 포장 솔루션에 대한 수요를 견인하고 있습니다.

- 이러한 추세는 지속 가능하고 재활용 가능한 포장 옵션에 대한 선호도가 높아짐에 따라 더욱 가속화되고 있으며, 유리는 환경 친화적인 특성으로 인해 선호되고 있습니다. 맥주와 증류주를 중심으로 한 크래프트 음료 산업의 성장도 특수 유리 포장에 대한 수요 증가에 기여하고 있습니다. 고령화 사회와 의학의 발전으로 인한 의약품 부문의 확대도 엄격한 안전 및 보존 기준을 충족하는 고품질 유리 용기에 대한 수요를 증가시키고 있습니다.

- 미국은 탄탄한 경제, 종합적인 비즈니스 이민 제도, 다양한 소비자층, 혁신 중심의 문화, 비즈니스 친화적인 정책으로 인해 벤처기업에 유리한 환경을 제공합니다. 이러한 요인들로 인해 미국은 사업을 확장하거나 새로 설립하려는 기업이 및 기업들에게 매력적인 진출지입니다. 탄탄한 인프라, 첨단 기술 분야, 자본에 대한 접근성은 다양한 업종의 기업들에게 더욱 매력적인 요소로 작용하고 있습니다.

- 전자상거래 플랫폼의 성장과 소비자 행동의 진화는 온라인 소매업체에게 큰 비즈니스 기회가 되고 있습니다. 디지털 시장은 인터넷 보급률, 모바일 기기 사용률, 쇼핑 습관의 변화 등을 배경으로 빠르게 성장하고 있습니다. 이러한 추세는 유리 포장을 포함한 다양한 산업에 잠재적인 비즈니스 기회를 제공합니다.

- 소비자들이 환경에 대한 인식이 높아지고 지속 가능한 솔루션을 추구함에 따라 유리 포장 제조업체는 재활용 및 재사용이 가능한 용기에 대한 수요를 활용할 수 있습니다. 또한, 틈새 시장에서 고급 제품이나 장인정신이 깃든 제품에 대한 선호도가 높아지면서 유리 포장의 품질과 미적 매력이 유리 포장의 품질과 미적 매력에 부합하는 경우가 많아 유리 포장 산업에 더 많은 성장 잠재력을 가져다주고 있습니다.

- 미국에서는 밀레니얼 세대와 X세대가 와인 소비 증가를 주도하고 있습니다. 이 소비자층은 와인에 대한 선호도가 높아지면서 시장 트렌드와 제품 제공에 영향을 미치고 있습니다. 그들의 취향과 구매 습관의 진화는 와인 산업의 방향성에 큰 영향을 미치고 있습니다. 2023년 미국 내 와인 소매 총액은 약 1,063억 달러에 달할 것으로 예상됩니다. 이 큰 수치는 미국 와인 시장의 견고한 특성과 지속적인 확장을 반영합니다. 판매액 증가는 소비 증가와 프리미엄 또는 고가 와인 제품으로의 전환 가능성을 보여줍니다.

- 이러한 추세는 와인 포장에서 고품질 유리병에 대한 수요가 증가하고 있음을 보여줍니다. 소비자의 안목이 높아짐에 따라 와인 제품의 전반적인 프레젠테이션과 품질에 더 많은 관심을 기울이고 있습니다. 유리병, 특히 우수한 품질의 유리병은 와인의 무결성을 유지하고 가치를 높이는 데 중요한 역할을 합니다. 와이너리들이 고급 포장 솔루션에 대한 소비자의 기대에 부응하기 위해 노력하고 있기 때문에 포장 산업, 특히 유리 제조업체는 이러한 추세의 혜택을 누릴 수 있을 것으로 보입니다.

북미의 유리병/용기 산업 개요

북미의 유리병/용기 시장은 세분화되어 있으며, 다수의 세계 및 지역 기업들이 시장 점유율을 놓고 경쟁하고 있습니다. 이 부문의 주요 기업으로는 O-I Glass, Inc., Ardagh Group S.A., MJS Packaging, Anchor Glass Container Corporation 등이 있습니다. 이 회사들과 다른 시장 진출기업들은 다양하고 경쟁적인 상황에 기여하고 있습니다.

시장이 진화함에 따라 지속 가능한 경쟁 우위를 유지하고 확대하기 위해서는 기술 혁신이 필수적입니다. 기업들은 연구개발에 투자하여 제품을 개선하고, 제조 공정을 강화하며, 소비자 수요의 변화에 대응하고 있습니다. 이러한 기술 혁신에 대한 집중은 경량 유리 제조의 발전, 재활용 기술 향상, 제품 보호 강화를 위한 특수 코팅의 개발을 촉진하고 있습니다.

지속가능성과 환경에 대한 관심이 높아지는 것도 유리병/용기 시장의 중요한 촉진요인입니다. 많은 기업들이 환경 친화적 인 방법을 채택하고 유리의 재활용 가능성을 중요한 판매 포인트로 홍보하고 있습니다. 이러한 추세는 앞으로도 경쟁 구도를 형성하고 시장 역학에 계속 영향을 미칠 것으로 보입니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

- 시장 개요

- 컨테이너용 유리 수출입 데이터

- 컨테이너용 유리 시장 PESTEL 분석

- 컨테이너 포장용 유리 산업 표준과 규제

- 컨테이너 포장용 유리 원료 분석과 재료 인사이트

- 컨테이너 포장용 유리 지속가능성 동향

- 북미의 컨테이너용 유리 용광로 및 입지

제5장 시장 역학

- 시장 성장 촉진요인

- 시장 성장 억제요인

- 무역 시나리오 - 유리병/용기 산업 수출입 패러다임 역사와 현황 분석

제6장 시장 세분화

- 최종사용자 산업별

- 음료

- 주류(부문별 정성 분석)

- 맥주 및 사이다

- 와인 및 증류주

- 기타 주류

- 무알코올(부문별 정성 분석)

- 탄산음료

- 우유

- 물 및 기타 무알코올 음료

- 식품

- 화장품

- 의약품

- 기타 산업별

- 음료

- 국가별

- 미국

- 캐나다

제7장 경쟁 구도

- 기업 개요

- O-I Glass, Inc

- Ardagh Group S.A.

- Gerresheimer AG

- Arksansas Glass Container Corporation

- MJS Packaging

- O.Berk Company, L.L.C.

- Kaufman Container Company

- Burch Bottle & Packaging, Inc.

- Anchor Glass Container Corporation

- West Coast Container Inc.

- PGP Glass Private Limited

제8장 북미의 유리병/용기 공장에 공급하는 주요 용광로 제조업체 분석

제9장 시장 전망

LSH 25.01.21The North America Glass Bottles/Containers Market size in terms of shipment volume is expected to grow from 13.08 million tonnes in 2025 to 16.39 million tonnes by 2030, at a CAGR of 4.62% during the forecast period (2025-2030).

Key Highlights

- Driven by rising consumption in sectors like food and beverage, cosmetics, and pharmaceuticals, the North American container glass market is on an upward trajectory. As consumers increasingly prioritize safe and healthy packaging, glass has found its way into diverse categories. This is especially pronounced in the beverage sector, where premium products and craft beverages often come in glass bottles.

- Moreover, cutting-edge technologies in embossing, shaping, and artistic finishes are elevating the allure of glass packaging. Such innovations not only offer enhanced customization and branding but also make glass containers a go-to choice for companies aiming for standout packaging. The industry's push towards lightweight glass technologies addresses transportation cost concerns and environmental implications, further fueling market expansion.

- In the U.S., a surge in alcoholic beverage consumption is driving a robust demand for packaging, especially glass bottles. This demand mirrors the expanding range of alcoholic offerings and a consumer tilt towards premium packaging. Glass bottles are preferred not just for their recyclability and premium look, but also for their prowess in preserving beverage quality and taste. The craft beer trend and the emergence of artisanal spirits have amplified the appetite for top-tier glass packaging.

- Data from the 2023 National Survey on Drug Use and Health (NSDUH) reveals that 218.7 million U.S. adults (84.9% of those 18 and older) have consumed alcohol at some point. Such a significant consumer base ensures a steady demand for varied packaging solutions in the beverage sector. Glass bottles, with their versatility and appeal, remain dominant, and manufacturers are innovating to cater to the changing preferences of both producers and consumers.

- Glass Global reports that North America produced 8,389,233 tonnes of glass bottles and containers across sectors, with an annual capacity of 9,321,370 tonnes. This underscores the region's formidable presence in the glass packaging arena. The robust production capacity and volume signal not just a strong infrastructure but also a thriving demand, spanning industries like food and beverage, pharmaceuticals, and cosmetics.

- Additionally, data from the International Trade Centre highlights the U.S. exported around 141,143 tonnes of glass packaging. This not only points to a burgeoning opportunity in the glass packaging realm but also underscores the international demand for North American glass products, likely attributed to their quality and the region's manufacturing prowess. The blend of substantial domestic production and significant export figures accentuates the North American glass packaging industry's strength and growth trajectory.

- As container glass finds increasing adoption across sectors in the region, recycling has emerged as a critical focus. Industries like food and beverage, pharmaceuticals, and cosmetics are generating substantial glass waste due to their heightened use of container glass. Efficient recycling is vital for waste management, minimizing environmental impact, and championing sustainability. With government regulations leaning towards sustainable packaging, manufacturers are increasingly turning to glass solutions. Collectively, these dynamics are propelling the growth of North America's glass packaging market.

North America Glass Bottles/Containers Market Trends

Alcoholic Beverage Segment is Expected to Witness Significant Growth

- Alcohol manufacturers are rolling out new versions of their products in glass bottles, a move anticipated to positively influence the market. By adopting glass packaging, these manufacturers aim to boost product appeal and reshape consumer perceptions, capitalizing on the premium image associated with glass. Glass bottles not only preserve the product's taste and quality more effectively but also offer heightened recyclability and an upscale feel. Many consumers equate glass packaging with superior beverage quality, often justifying a premium price tag.

- Moreover, glass facilitates unique and creative bottle designs, allowing brands to differentiate themselves on store shelves.

- This pivot to glass packaging resonates with the rising consumer demand for sustainable and eco-friendly options, given that glass is entirely recyclable and boasts multiple reuse capabilities.

- For example, in September 2024, Diageo-owned Johnnie Walker unveiled a limited edition Blue Label Ultra, showcasing the world's lightest 700ml glass bottle tailored for Scotch whisky. This pioneering packaging marks a notable leap in sustainable whisky bottling.

- The North American beer packaging sector is largely influenced by evolving cultural trends, a growing population, urbanization, and a surge in beer's popularity among younger demographics. Continued investments and a broadening beer distribution network across regions are likely to uphold these trends, potentially invigorating the market for glass bottles and containers.

- From March to May 2024, U.S. beer production in bottles and cans fluctuated between 10.41 million and 12.47 million barrels, underscoring the nation's demand for packaged beer. Even though the U.S. witnessed a 5% dip in beer production and imports in 2023, and craft brewer volume sales fell by 1%, the market remains buoyed by a rising beer consumption trend.

- The dip in production and imports could stem from shifts in consumer preferences, economic factors, or regulatory changes. Yet, the uptick in beer consumption hints at untapped growth and innovation avenues in the industry, possibly spurred by new beer varieties, intensified marketing, or evolving consumer behaviors.

- In North America, a growing segment of consumers is embracing sustainable lifestyles, notably in their efforts to curb plastic waste. This movement is propelling the wine and spirits market's shift towards glass bottles. Many consumers view glass bottles as more eco-friendly than their plastic counterparts and associate them with premium product quality. This perception resonates with environmentally-conscious consumers, often willing to pay a premium for sustainable packaging. Furthermore, looming government regulations aimed at curbing plastic usage could further amplify the demand for glass bottles in the alcoholic beverage sector.

United States is Expected to Account for Major Market Share

- The United States represents one of the world's largest packaging markets, featuring numerous key players producing glass bottles and containers for various industries, including food and beverage, personal care, and pharmaceuticals. The country's economic growth and rising consumer expenditure on food, drinks, pharmaceuticals, and personal care products drive the demand for glass bottle and container packaging solutions.

- This trend is further supported by the increasing preference for sustainable and recyclable packaging options, with glass being favored due to its eco-friendly properties. The growing craft beverage industry, particularly in beer and spirits, has also contributed to the increased demand for specialized glass packaging. The pharmaceutical sector's expansion, driven by an aging population and advancements in healthcare, has also bolstered the need for high-quality glass containers that meet stringent safety and preservation standards.

- The United States offers a favorable environment for business ventures due to its strong economy, comprehensive business immigration system, diverse consumer base, innovation-driven culture, and business-friendly policies. These factors make the USA an attractive destination for entrepreneurs and companies looking to expand or establish new operations. The country's robust infrastructure, advanced technology sector, and access to capital further enhance its appeal for businesses across various industries.

- The growth of e-commerce platforms and evolving consumer behaviors present significant opportunities for online retailers. The digital marketplace has experienced rapid expansion, driven by increased internet penetration, mobile device usage, and changing shopping habits. This shift has created a fertile ground for businesses to reach a wider audience and implement innovative sales strategies.These trends create potential opportunities for various industries, including glass packaging.

- As consumers become more environmentally conscious and seek sustainable solutions, glass packaging manufacturers can capitalize on the demand for recyclable and reusable containers. Additionally, the growing preference for premium and artisanal products in niche markets often aligns well with the perceived quality and aesthetic appeal of glass packaging, presenting further growth prospects for the industry.

- In the United States, Millennial and Gen X consumers have been driving the growth in wine consumption. These demographic groups have shown an increasing preference for wine, influencing market trends and product offerings. Their evolving tastes and purchasing habits have significantly impacted the wine industry's direction. The total retail value of wine sales in the US reached approximately USD 106.3 billion in 2023. This substantial figure reflects the robust nature of the American wine market and its continued expansion. The sales value growth indicates increased consumption and a potential shift towards premium or higher-priced wine products.

- This trend indicates an increasing demand for high-quality glass bottles in wine packaging. As consumers become more discerning, there is a growing emphasis on the overall presentation and quality of wine products. Glass bottles, particularly those of superior quality, play a crucial role in preserving the wine's integrity and enhancing its perceived value. The packaging industry, especially glass manufacturers, will likely benefit from this trend as wineries seek to meet consumer expectations for premium packaging solutions.

North America Glass Bottles/Containers Industry Overview

The North America container glass market is fragmented, with numerous global and regional players competing for market share. Key companies in this space include O-I Glass, Inc., Ardagh Group S.A., MJS Packaging, and Anchor Glass Container Corporation. These firms and other market participants contribute to a diverse and competitive landscape.

As the market evolves, innovation has become crucial in maintaining and growing sustainable competitive advantage. Companies invest in research and development to improve product offerings, enhance manufacturing processes, and meet changing consumer demands. This focus on innovation drives advancements in lightweight glass production, improved recycling techniques, and the development of specialized coatings for enhanced product protection.

The increasing emphasis on sustainability and environmental concerns has also become a significant driver in the glass bottles and containers market. Many companies are adopting eco-friendly practices and promoting the recyclability of glass as a key selling point. This trend will likely continue shaping the competitive landscape and influencing market dynamics in the coming years.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Export-Import Data of Container Glass

- 4.3 PESTEL Analysis of Container Glass Market

- 4.4 Industry Standard and Regulation For Container Glass Use For Packaging

- 4.5 Raw Material Analysis and Material Consideration For Packaging

- 4.6 Sustainability Trends For Glass Packaging

- 4.7 Container Glass Furnace and Location in North American Region

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Demand from Food and Beverage Industry

- 5.1.2 Sustainability and Recyclability Initiatives Are Expanding End-Users Demand For Glass Packaging

- 5.2 Market Restraints

- 5.2.1 High Carbon Footprint due to Glass Manufacturing

- 5.2.2 Operation and Logistical Concerns

- 5.3 Trade Scenario - Analysis of the Historical and Current Export-Import Paradigm For Container Glass Industry

6 MARKET SEGMENTATION

- 6.1 By End-user Vertical

- 6.1.1 Bevarages

- 6.1.1.1 Alcoholic (Qualitative Analysis For Segment Analysis)

- 6.1.1.1.1 Beer and Cider

- 6.1.1.1.2 Wine and Spirits

- 6.1.1.1.3 Other Alcoholic Beverages

- 6.1.1.2 Non-alcoholic (Qualitative Analysis For Segment Analysis)

- 6.1.1.2.1 Carbonated Soft Drinks

- 6.1.1.2.2 Milk

- 6.1.1.2.3 Water and Other Non-alcoholic Beverages

- 6.1.2 Food

- 6.1.3 Cosmetics

- 6.1.4 Pharmaceutical

- 6.1.5 Other End-user Verticals

- 6.1.1 Bevarages

- 6.2 By Country

- 6.2.1 United States

- 6.2.2 Canada

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 O-I Glass, Inc

- 7.1.2 Ardagh Group S.A.

- 7.1.3 Gerresheimer AG

- 7.1.4 Arksansas Glass Container Corporation

- 7.1.5 MJS Packaging

- 7.1.6 O.Berk Company, L.L.C.

- 7.1.7 Kaufman Container Company

- 7.1.8 Burch Bottle & Packaging, Inc.

- 7.1.9 Anchor Glass Container Corporation

- 7.1.10 West Coast Container Inc.

- 7.1.11 PGP Glass Private Limited