|

시장보고서

상품코드

1628767

영국의 유리 포장 : 시장 점유율 분석, 산업 동향 및 성장 예측(2025-2030년)United Kingdom Glass Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

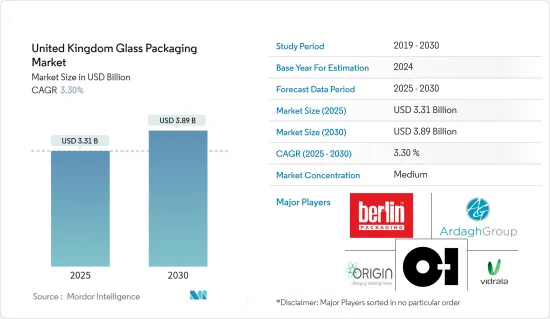

영국의 유리 포장 시장 규모는 2025년 33억 1,000만 달러로 추정 및 예측되며, 예측 기간(2025-2030년) 동안 3.3%의 연평균 복합 성장률(CAGR)로 2030년에는 38억 9,000만 달러에 달할 것으로 예상됩니다.

주요 하이라이트

- 보다 안전하고 건강한 포장에 대한 소비자의 요구가 높아지면서 다양한 카테고리에서 유리 포장의 확장을 촉진하고 있습니다. 엠보싱, 성형, 예술적 마감과 같은 혁신적인 기술은 최종 사용자에게 유리 포장의 매력을 높이고 있습니다. 또한, 친환경 제품에 대한 수요 증가, 특히 식음료 부문에서 친환경 제품에 대한 수요가 증가하면서 시장 성장을 견인하고 있습니다. 맥주와 와인에 대한 소비자의 선호도가 높아짐에 따라 유리 포장 제조업체들은 이에 맞추어 생산량을 늘리고 있습니다. 프리미엄 음료 및 식품 브랜드는 유리의 화학적 불활성, 비다공성, 불투과성 때문에 플라스틱과 같은 대체재보다 유리 용기를 선호하고 있습니다.

- 최근 몇 년동안 식품 포장 산업은 투명성을 추구하는 경향이 강해지고 있습니다. 유리 용기에는 인스턴트 커피, 가공 이유식, 유제품, 설탕에 절인 식품 등 다양한 식품이 담겨 있습니다. 소비자들은 원재료뿐만 아니라 제품을 구매하기 전에 실물을 보고 싶어 합니다. 이러한 추세를 활용하기 위해 많은 기업들이 특히 유제품 부문에서 투명 유리 용기로의 전환을 추진하고 있습니다. Trivium Packaging의 조사에 따르면, 소비자의 약 74%는 지속 가능한 포장에 대해 프리미엄을 지불할 의향이 있으며, 지속 가능한 포장에 대한 수요는 유리 포장 시장을 강화시키고 있습니다.

- 프랑스 유리병 및 용기 시장은 탈탄소화를 위한 안정적인 정책 프레임워크를 요구하고 있으며, 제조업체가 온실 가스 배출 감소에 투자할 수 있도록 2023년 8월 프랑스 정부는 유럽연합(EU)과는 대조적인 움직임으로 잉여 와인을 폐기하고 생산자를 지원하기 위해 1억 7,000만 파운드(2억 1,150만 달러)를 배정했습니다. 160만 파운드(2억 1,150만 달러)를 배정했습니다. 이 이니셔티브는 가격을 안정시키고 와인 생산자들이 수입원을 확보하는 것을 목표로 하고 있습니다. 영국에서도 '블루윕 효과'라고 불리는 유사한 추세가 예상되며, 이는 연구 시장에 도움이 될 수 있습니다.

- 2024년 6월, 에그는 음료 및 식품 포장 라인업의 일환으로 새로운 주류 병 "Gediz"를 발표했습니다."Gediz"는 "Yenice"주류 병의 성공을 바탕으로 눈길을 끄는 디자인을 자랑하며, 인쇄 및 라벨링을위한 넓은 패널이 있어 다양한 주류 기반 제품에 적합합니다. 다양한 주류 기반 제품에 적합합니다.

- 에너지 가격 변동이 예상됨에 따라 기업은 장기 계약을 체결하여 불안정한 원자재 및 에너지 비용을 피해야 합니다. 이는 갑작스러운 가격 변동이 소비자를 경쟁 브랜드로 향하게 할 수 있는 음료 및 식품 부문의 기업들에게 특히 중요합니다. 예를 들어, 영국 와인 산업은 유리잔 부족에 직면하여 병입 가격이 급등하고 있습니다. 이러한 문제 외에도 많은 영국 병입업체들이 브렉시트를 대비해 비축을 하고 있으며, 브랜드 소유주들이 플라스틱 병에서 유리병으로 전환하는 현상이 두드러지게 나타나면서 시장을 더욱 긴장시키고 있습니다.

영국의 유리 포장 시장 동향

음료 부문이 가장 높은 성장률을 나타낼 것

- 유리병은 오랫동안 음료 산업에서 선호되는 포장재였으며, 그 추세는 현재도 안정적입니다. 유리병은 제품의 품질을 유지하고 외부 요인으로부터 내용물을 보호하는 등 많은 장점을 가지고 있습니다.

- 화학적 무균성과 불투과성으로 인해 유리 병과 용기는 주로 알코올 음료와 무알콜 음료에 주로 사용됩니다. 유리는 우수한 배리어 재료로 눈에 띄며 포장용 투명도가 높기 때문에 포장용 투명성이 뛰어납니다. 그 특성은 CO2의 손실과 산소의 침입에 저항하여 장기간의 저장 수명을 보장합니다. 최근 가공 및 코팅의 발전으로 유리 병의 플랜지 특성이 향상되고 최신 경량화 기술로 강도와 사용 편의성이 강화되었습니다.

- OEC(Observatory of Economic Complexity) 데이터에 따르면 2023년 4월영국은 1,580 만 GBP(1,948만 달러)의 유리 병을 수출하고 4,070 만 GBP(5,018만 달러)를 수입하여 2,490 만 GBP(3, 070만 달러)의 무역 적자를 기록했습니다. 2022년 4월부터 2023년 4월까지 영국의 유리병 수출은 931,000파운드(114만 7,965달러) 감소하여 1,670만 파운드(2,059만 달러)에서 1,580만 파운드(1,948만 달러)로 5.57% 감소했습니다. 감소했습니다. 반면 수입은 1,000만 파운드(1,030억 3,045만 6,220달러)로 33.9% 증가해 3,040만 파운드(3,748만 달러)에서 4,007만 파운드(4,940만 달러)로 급등했습니다.

- 영국의 유리병 수입 증가는 주로 주류 및 비주류 음료 부문 수요에 기인하며, 이러한 추세는 앞으로도 지속될 것으로 예상됩니다.

- 프리미엄화 추세는 청량음료를 포함한 다양한 음료 부문에서 유리 포장의 선택에 영향을 미치고 있습니다. 청량음료는 폭넓은 매력과 모든 상황에 맞는 다양한 맛으로 인해 시장에서 큰 비중을 차지하고 있습니다. 특히 UNESDA의 데이터에 따르면 유럽 일부 시장에서는 저칼로리 및 무설탕 음료가 전체 매출의 30%를 차지하고 있습니다.

화장품 부문이 큰 점유율을 차지할 것으로 예상

- 유리 포장은 고급 향수, 스킨케어, 퍼스널케어 제품에 선호됩니다. 화장품과 향수에 사용되는 유리는 주로 모래, 석회석, 소다회 등 천연 재료와 지속 가능한 재료로 만들어집니다. 주목할 만한 점은 유리 포장은 100% 재활용이 가능하며, 품질과 순도를 떨어뜨리지 않고 무한히 재활용할 수 있다는 점입니다. 놀랍게도 재생 유리의 80%는 새로운 유리 제품으로 재사용됩니다.

- 개인용품 산업에서 유리는 고급품의 대명사다. 그 중후함은 대체 포장재를 능가하며, 높은 비용으로 인해 고급품이라는 인식이 형성되어 제품의 인지도가 높아집니다. 화장품 포장에는 스킨케어, 헤어케어, 네일케어, 메이크업 제품에 대응하는 병, 항아리, 바이알, 앰플 등 다양한 용기가 포함됩니다. 이러한 화장품 용기는 특히 고급 제품 부문에서 유리로 만든 용기가 눈에 띕니다. 유리 병과 병은 제트 및 드롭 인서트, 거품 캡, 스프레이 노즐, 펌프 헤드 등 다양한 디스펜서 옵션과 함께 사용할 수 있는 다재다능함이 유리 용기의 장점입니다.

- 화장품 및 향수 시장은 소비자의 외모에 대한 인식이 높아지고 자외선 차단 및 오염 방지에 대한 필요성이 증가함에 따라 괄목할만한 성장을 보이고 있습니다. 이 부문의 기업들은 특히 성숙한 카테고리에서 성장을 유지하고 매년 부가가치가 높은 신제품을 출시하기 위해 혁신에 많은 투자를 하고 있습니다. 이러한 추세는 예방뿐만 아니라 치료에 대한 소비자의 관심도 증가시키고 있습니다. 그 결과, 리프레쉬, 디톡스, 보습 등의 제품에 대한 수요가 급증하고 있습니다. 이러한 움직임은 퍼스널케어 및 화장품 부문에서 유리 병과 용기에 대한 수요를 촉진하고 있습니다.

- Cosmetics, Toiletry, and Perfumery Association(CTPA)의 데이터는 2023년 세면도구 및 미용 부문의 견조한 실적을 강조하며 전년도 지표를 상회하는 것으로 나타났습니다. 전체 산업 평가액은 전년 대비 9.7% 증가한 95억 6,000만 파운드(약 121억 4,000만 달러 상당)에 달했습니다. 인플레이션이 안정되고 미용 및 세면 용품의 사용 빈도가 증가함에 따라 업계는 향후 몇 년동안 더욱 두드러진 성장이 예상되며 이러한 추세는 영국의 유리 포장 시장을 강화할 가능성이 높습니다.

영국의 유리 포장 산업 개요

영국의 유리 포장 시장의 경쟁은 완만하며, Ardagh Packaging, Berlin Packaging, Owens-Illinois Inc.와 같은 기업들은 시장 점유율과 수익성을 높이기 위해 전략적 공동 이니셔티브를 활용하고 있습니다. 그러나 유리 병과 용기의 채택이 증가하고 있는 이유는 유리의 특성과 음료, 화장품 및 기타 산업에 대한 유리의 장점 때문입니다. 공급업체들은 플라스틱을 친환경 제품 유리로 대체하는 데 중점을 두고 있습니다.

2024년 7월 영국에 본사를 둔 유리 포장 회사 Croxsons는 리필용 스킨케어 제품 전문 브랜드 Necessary Good의 새로운 1차 포장 솔루션을 발표한 지 1년이 지났습니다. 이 혁신적인 유리 포장은 라이프 스타일, 미용, 건강 및 웰빙을 전문으로하는 Croxson의 전문 부서에서 제작했습니다. 이 제조업체는 Necessary Goods를 위해 100ml와 200ml의 두 가지 원통형 유리 병을 생산했습니다.

2023년 5월 영국에서 Ardagh Glass Packaging(AGP)은 유리 생산 시 온실 가스 배출을 억제하기 위해 지속 가능한 "고효율 용광로"를 건설할 것이라고 발표했습니다. 활용합니다. 이 용광로에는 첨단 가스 여과 시스템이 장착되어 있으며, 혁신적인 필터 기술을 활용하여 다른 배출 요소를 처리하여 현재 산업 벤치마크보다 훨씬 낮은 수준을 달성할 수 있도록 크게 감소시킬 것입니다. 이 야심찬 프로젝트는 정부의 산업 에너지 전환 기금(IETF)의 지원을 받아 에너지 다소비 기업의 저탄소 미래로의 전환을 지원하기 위한 이니셔티브인 IETF의 지원을 받고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

- 시장 개요

- 산업 매력 - Porter의 Five Forces 분석

- 공급 기업의 교섭력

- 소비자의 교섭력

- 신규 진출업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

- 써큘러·이코노미를 중시한 산업 생태계 분석

- 규제 프레임워크

- 수출입 분석

- 주요 촉진요인(부품과 에너지 소비)을 포함한 비용 분석

- 영국의 유리 재활용 중시 증가와 재활용 가능률 현황 분석

- 영국의 유리 제조 산업 전체 분석

제5장 시장 역학

- 시장 성장 촉진요인

- 음료 산업 유리 포장 수요 증가

- 프리미엄 포장 시장 통합이 성장을 한층 더 촉진

- 시장이 해결해야 할 과제

- 대체 포장 형태가 시장 성장 과제

제6장 시장 세분화

- 제품 유형별

- 보틀

- 바이알

- 앰플

- 전기밥통

- 기타 제품 유형(프리필드 시린지, 파이알, 훌라 콘 등)

- 산업별

- 음료

- 주류

- 맥주와 사이다

- 와인과 증류주

- 기타 주류

- 무알코올

- 탄산음료

- 우유

- 물과 기타 무알코올 음료(주스 등)

- 식품

- 퍼스널케어 및 화장품

- 의료와 의약품

- 기타 최종 이용 산업별

- 음료

제7장 경쟁 구도

- 기업 개요

- Berlin Packaging LLC

- Ardagh Packaging Group

- Owens-Illinois Inc.

- Origin Pharma Packaging

- Vidrala SA

- Beatson Clark

- Ciner Glass Ltd

- Stoelzle Flaconnage Ltd

- Beatson Clark

- Glassworks International Limited

- 히트맵 분석

제8장 투자 분석

제9장 시장의 미래

LSH 25.01.21The United Kingdom Glass Packaging Market size is estimated at USD 3.31 billion in 2025, and is expected to reach USD 3.89 billion by 2030, at a CAGR of 3.3% during the forecast period (2025-2030).

Key Highlights

- Growing consumer demand for safer and healthier packaging is driving the expansion of glass packaging across various categories. Innovative technologies, such as embossing, shaping, and artistic finishes, are enhancing the appeal of glass packaging to end users. In addition, the surging demand for eco-friendly products, particularly from the food and beverage sector, is propelling market growth. As consumers increasingly gravitate toward beer and wine, glass packaging manufacturers are adapting their production accordingly. Premium food and beverage brands favor container glass over alternatives like plastic, citing glass's chemical inertness, non-porous nature, and impermeability.

- In recent years, the food packaging industry has witnessed a growing trend toward transparency. Glass containers house a diverse array of foods, from instant coffee and processed baby foods to dairy products and sugar preserves. Beyond just ingredients, consumers want to see the product physically before buying. To leverage this trend, many companies, especially in the dairy sector, are transitioning to transparent glass containers. The push for sustainable and eco-friendly packaging bolsters the glass packaging market. Research by Trivium Packaging highlights that about 74% of consumers are willing to pay a premium for sustainable packaging.

- The glass bottles and containers market in the country seeks a stable policy framework for decarbonization, enabling manufacturers to invest in reducing greenhouse gas emissions. In August 2023, the French government, in a move contrasting with the European Union, allocated GBP 171.6 million (USD 211.5 million) to destroy surplus wine and bolster producers. This initiative aims to stabilize prices, ensuring winemakers regain revenue sources. A similar trend termed the "bullwhip effect," is anticipated in the United Kingdom, potentially benefiting the studied market.

- In June 2024, Aegg unveiled its new spirit bottle, 'Gediz,' as part of its food and drink packaging lineup. Building on the success of the 'Yenice' spirit bottle, the Gediz boasts an eye-catching design with a spacious panel for printing or labeling, making it ideal for various spirit-based products.

- Anticipated fluctuations in energy prices are pushing businesses to secure long-term contracts to shield against volatile raw material and energy costs. This is especially crucial for those in the food and beverage sector, where sudden price shifts can drive consumers to rival brands. The UK wine industry, for example, is grappling with a glass shortage, leading to steep price increases for bottlers. Beyond these challenges, many UK bottlers have been stockpiling in anticipation of Brexit, and a notable shift from plastic to glass bottles by brand owners has further strained the market.

United Kingdom Glass Packaging Market Trends

Beverage Segment is Set to Witness The Highest Growth

- Glass bottles have long been a favored packaging choice in the beverage industry, a trend that remains steadfast today. They provide numerous advantages, such as preserving product quality and shielding contents from external factors.

- Due to their chemical sterility and non-permeability, glass bottles and containers are predominantly utilized for alcoholic and non-alcoholic beverages. Glass stands out as an excellent barrier material, boasting high transparency for packaging. Its properties ensure a prolonged shelf life by resisting CO2 loss and O2 intrusion. Recent advancements in processing and coatings have enhanced the frangibility of glass bottles, while modern lightweight techniques bolster their strength and user-friendliness.

- Data from the Observatory of Economic Complexity (OEC) reveals that in April 2023, the UK exported glass bottles worth GBP 15.8 million (USD 19.48 million) and imported them at GBP 40.7 million (USD 50.18 million), leading to a trade deficit of GBP 24.9 million (USD 30.70 million). Between April 2022 and April 2023, UK glass bottle exports dipped by GBP 931,000 (USD 1,147,965), marking a 5.57% decline from GBP 16.7 million (USD 20.59 million) to GBP 15.8 million (USD 19.48 million). In contrast, imports surged by GBP 10 million (USD 12,330,456.2), a notable 33.9% increase, rising from GBP 30.4 million (USD 37.48 million) to GBP 40.07 million (USD 49.40 million).

- The rising imports of glass bottles in the United Kingdom are primarily fueled by demand from alcoholic and non-alcoholic beverage sectors, a trend anticipated to persist in the coming years.

- Trends in premiumization have influenced the choice of glass packaging across various beverage segments, including soft drinks. Given their widespread appeal and diverse flavors tailored for every occasion, soft drinks command a substantial share of the market. Notably, data from UNESDA highlights that in several European markets, low-calorie and sugar-free beverages represent up to 30% of sales.

Cosmetic Sector is Expected to Witness Significant Share

- Glass packaging is the preferred choice for exclusive fragrances, skincare, and personal care products. The glass utilized in cosmetics and fragrances is primarily derived from natural and sustainable materials, including sand, limestone, and soda ash. Notably, glass packaging boasts a 100% recyclability rate, allowing it to be recycled infinitely without any degradation in quality or purity. Impressively, 80% of recycled glass is repurposed into new glass products.

- In the personal care industry, glass is synonymous with luxury. Its heft surpasses that of alternative packaging materials, and its higher cost fosters a perception of premium quality, thereby elevating the product's perceived value. Cosmetic packaging encompasses a range of containers, including bottles, jars, vials, and ampoules, catering to skincare, haircare, nail care, and makeup products. These cosmetic containers, especially in luxury segments, prominently feature glass. Glass jars and bottles are favored for their versatility, accommodating various dispensing options like jet and drop inserts, frothing caps, spray nozzles, and pump heads.

- As consumers become more conscious of their appearance and the need for sun and pollution protection, the cosmetics and perfume market is witnessing significant growth. Companies in this sector are heavily investing in innovations, aiming to sustain growth and introduce new, value-added products annually, particularly in mature categories. This trend piques consumer interest not only in preventive measures but also in treatments. Consequently, products like refreshing, detoxifying, and moisturizing solutions are poised for a surge in demand. Such dynamics are propelling the demand for glass bottles and containers in the personal care and cosmetics arena.

- Data from the Cosmetics, Toiletry, and Perfumery Association (CTPA) highlights a robust performance in the toiletries and beauty sectors for 2023, surpassing the previous year's metrics. The industry's total valuation experienced a Y-o-Y surge of 9.7%, reaching a notable GBP 9.56 billion (equivalent to USD 12.14 billion). With inflation rates stabilizing and an uptick in the frequency of beauty and toiletry usage, the industry is optimistic about even more pronounced growth in the forthcoming years, a trend likely to bolster the glass packaging market in the United Kingdom.

United Kingdom Glass Packaging Industry Overview

The United Kingdom glass packaging market is moderately competitive, with many regional and global players such as Ardagh Packaging, Berlin Packaging, Owens-Illinois Inc., and many more. The companies are leveraging strategic collaborative initiatives to increase market share and profitability. However, the properties of glass and its benefits to beverages, cosmetics, and other industries are leading to the increased adoption of glass bottles and containers. Vendors are focusing on replacing plastic with environmentally friendly product glass.

July 2024: United Kingdom-based glass packaging firm Croxsons completed one year of the unveiling of its new primary packaging solution for Necessary Good, a brand specializing in refillable skincare essentials. This innovative glass packaging was manufactured by Croxson's dedicated division focusing on lifestyle, beauty, health, and wellness. The manufacturer produced two cylindrical glass bottle sizes for Necessary Goods, which are 100 ml and 200 ml.

May 2023: In the United Kingdom, Ardagh Glass Packaging (AGP) announced the construction of a sustainable 'Efficient Furnace' aimed at curbing greenhouse gas emissions during glass production. This furnace, set to be installed at AGP's Doncaster facility, leverages advanced industrial technology. The furnace is equipped with an advanced gas filtration system, utilizing innovative filter technology to address and significantly diminish other emission elements, achieving levels well below current industrial benchmarks. This ambitious project receives partial funding from the Government's Industrial Energy Transformation Fund (IETF), an initiative designed to assist energy-intensive businesses in their shift towards a low-carbon future.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Ecosystem Analysis with an Emphasis on Circular Economy

- 4.4 Regulatory Framework

- 4.5 Import and Export Analysis

- 4.6 Cost Analysis with Key Drivers (Components and Energy Consumption)

- 4.7 Analysis of the Increasing Emphasis on Glass Recycling and the Current Recyclability Rate in the United Kingdom

- 4.8 Analysis of the Overall Glass Manufacturing Industry in the United Kingdom

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increased Demand for Glass Packaging in Beverage Industry

- 5.1.2 Increased Integration in the Premium Packaging Market Further Drives the Growth

- 5.2 Market Challenges

- 5.2.1 Alternative Forms of Packaging is Challenging the Market Growth

6 MARKET SEGMENTATION

- 6.1 By Product Type

- 6.1.1 Bottles

- 6.1.2 Vials

- 6.1.3 Ampoules

- 6.1.4 Jars

- 6.1.5 Other Product Type (Pre-Filled Syringes, Phials, Flacons, among Others)

- 6.2 By End-use Vertical

- 6.2.1 Beverages

- 6.2.1.1 Alcoholic**

- 6.2.1.1.1 Beer and Cider

- 6.2.1.1.2 Wine and Spirit

- 6.2.1.1.3 Other Alcoholic Beverages

- 6.2.1.2 Non-alcoholic**

- 6.2.1.2.1 Carbonated Soft Drinks

- 6.2.1.2.2 Milk

- 6.2.1.2.3 Water and Other Non-alcoholic Beverages (Juices, Among others)

- 6.2.2 Food

- 6.2.3 Personal Care and Cosmetics

- 6.2.4 Healthcare and Pharmaceutical

- 6.2.5 Other End-use Verticals

- 6.2.1 Beverages

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Berlin Packaging LLC

- 7.1.2 Ardagh Packaging Group

- 7.1.3 Owens-Illinois Inc.

- 7.1.4 Origin Pharma Packaging

- 7.1.5 Vidrala SA

- 7.1.6 Beatson Clark

- 7.1.7 Ciner Glass Ltd

- 7.1.8 Stoelzle Flaconnage Ltd

- 7.1.9 Beatson Clark

- 7.1.10 Glassworks International Limited

- 7.2 Heat Map Analysis