|

시장보고서

상품코드

1628814

태국의 플라스틱 시장 : 점유율 분석, 산업 동향 및 성장 전망(2025-2030년)Thailand Plastics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

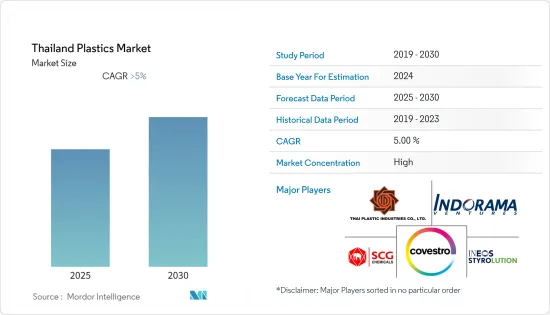

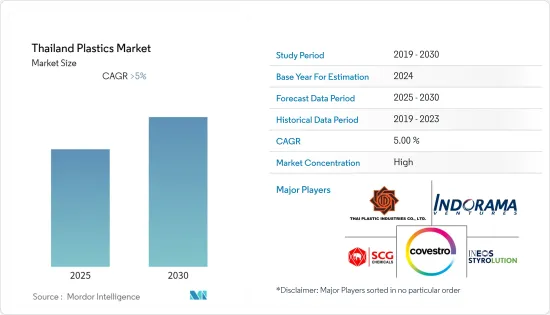

태국의 플라스틱 시장은 예측 기간 동안 5% 이상의 CAGR을 나타낼 것으로 예상됩니다.

시장은 코로나19로 인해 부정적인 영향을 받았습니다. 공급망의 혼란으로 인해 플라스틱 생산이 감소했습니다. 그러나 규제가 해제된 후 순조롭게 회복되고 있습니다. 산업 활동 수준 증가는 조사 대상 시장에 긍정적인 영향을 미칠 것으로 보입니다.

주요 하이라이트

- 단기적으로는 건축 및 건설 부문의 플라스틱 사용량 증가와 식음료 포장 수요 증가가 시장 성장을 견인하는 요인으로 작용하고 있습니다.

- 반면, 플라스틱 금지로 이어지는 엄격한 정부 규제는 예측 기간 동안 시장 성장을 저해할 것으로 예상됩니다.

- 생분해성 플라스틱에 대한 투자 증가는 향후 몇 년동안 시장에 기회를 가져올 것으로 보입니다.

태국의 플라스틱 시장 동향

폴리에틸렌 테레프탈레이트(PET)가 시장을 독점할 것으로 예상

- 폴리에틸렌 테레프탈레이트(PET) 수지는 우수한 용융 흐름 특성, 가까운 성형 공차, 다품종 금형을 통한 높은 생산성으로 유명하며, 기계적 및 전기적 특성으로 인해 모터 하우징, 스위치, 센서 및 기타 전기적 응용 분야에서 금속을 대체하는 데 자주 사용됩니다. 사용됩니다.

- PET와 폴리올레핀은 플라스틱 포장 산업에서 가장 널리 사용되는 재료입니다. 포장재로서 PET의 중요한 특성은 재활용성, 강도 및 다용도성이며, 이러한 특성으로 인해 이러한 제품에 대한 수요를 주도하고 있습니다.

- 이러한 제품에는 테이크아웃 용기, 냉동식품, 탄산음료 및 주스, 케첩, 생수, 병, 구운 과자 용기 등이 포함됩니다. 또한 식품 산업에서는 조개껍데기, 반찬 용기, 전자 레인지용 식품 트레이 등에도 사용됩니다.

- PET는 또한 제품의 내용물을 보호하고 보존하는 우수한 장벽 특성을 가지고 있으며, PET는 탄산음료의 탄산, 주스의 비타민, 케첩의 색을 그대로 유지합니다. 즉, PET는 제품을 보호하고 선반에 놓거나 쓰레기통에 넣지 않도록 보호합니다.

- 2020년 11월, 세계 최고의 PET 제조업체인 태국의 인드라마 벤처스(Indrama Ventures)는 환경 친화적인 음료 제조업체 수요를 늘리기 위해 15억 달러를 투자해 플라스틱 재활용 사업을 3배로 확대할 것이라고 발표했습니다. 인드라마는 최근 몇 년동안 폴리에틸렌 테레프탈레이트 재활용 업체를 인수했습니다. 현재 약 25만 톤의 재활용 능력을 2025년까지 연간 75만 톤으로 확대하는 것을 목표로 하고 있습니다. 목표는 인드라마가 음료 산업에 공급하는 연간 400만 톤의 PET 중 재활용 원료가 약 20%를 차지하도록 하는 것입니다.

- 지난 5월 태국의 ENVICCO Limited는 태국 라용주 맵타풋에 연간 약 4만 5,000톤의 재생 폴리에틸렌 테레프탈레이트를 생산할 수 있는 새로운 재생 플라스틱 공장을 착공했습니다. 이를 통해 태국의 플라스틱 시장에서 PET의 보급률이 높아질 것으로 보입니다.

- 위와 같은 요인으로 인해 예측 기간 동안 PET에 대한 수요가 증가할 것으로 보입니다.

시장을 독점하고 있는 자동차 산업

- 자동차 산업은 주로 엔지니어링 플라스틱을 사용합니다. 엔지니어링 플라스틱은 고성능으로 유명하며 자동차 부품을 자동차 산업의 엄격한 요구 사항에 맞게 조정할 수 있습니다. 대부분의 경우 엔지니어링 플라스틱은 매우 다재다능하기 때문에 자동차 산업에서 필요한 기술 혁신을 실현하는 데 적합합니다. 또한, 이러한 플라스틱은 가볍기 때문에 연료 소비를 줄일 수 있습니다.

- 자동차 산업에서 널리 사용되는 플라스틱에는 폴리프로필렌, 폴리우레탄, 폴리염화비닐, 폴리부틸렌테레프탈레이트(PBT) 등이 있습니다.

- 폴리프로필렌은 프로파일렌으로 생산되는 매우 내구성이 강한 폴리머입니다. 폴리프로필렌은 내화학성과 내구성이 뛰어나 범퍼에서 케이블 절연재, 카펫 섬유에 이르기까지 다양한 자동차 부품에 사용됩니다.

- 폴리우레탄은 방사선, 용제 및 환경 마모에 매우 강합니다. 이러한 특성으로 인해 타이어, 시트, 서스펜션 브러시 등의 제조 등 다양한 용도에 적합합니다.

- 열가소성 엔지니어링 폴리머는 고품질 대시보드 부품, 기둥 트림, 자동차 계기판, 휠 커버, 도어 라이너, 시트백, 스티어링 휠, 안전벨트 부품 등의 제조 등 다양한 용도로 자동차 산업에서 활용되고 있습니다. 이는 예측 기간 동안 조사 대상 시장 수요를 증가시킬 것으로 예상됩니다.

- 또한 플라스틱은 금속보다 경제적이며, 경량화, 내구성, 강인성, 설계 유연성, 탄력성, 내식성, 고성능을 제공하여 자동차의 에너지 효율을 높이는 데 도움이 됩니다. 또한 일부 플라스틱은 전기 절연성이 우수합니다.

- 태국에는 약 1,800개의 자동차 관련 기업이 있으며, 그 중 30-40개의 대기업, 약 700개의 1차 부품업체, 1,000개 이상의 2차 및 3차 부품업체가 있습니다. 많은 대기업들이 태국에 진출해 있다는 것은 자동차 공급망이 방대하다는 것을 의미할 뿐만 아니라, 향후 몇 년동안 자동차 산업이 더욱 성장할 수 있는 여건이 마련되었습니다는 것을 의미합니다.

- 태국산업연맹(FTI)의 보고서에 따르면, 2022년 11월 태국의 자동차 생산량은 전년 동월 대비 15% 가까이 증가한 약 19,155대를 기록했으며, 반도체 부족이 계속 완화되어 지난 44개월 동안 최고치를 기록했다고 합니다.

- 또한 FTI에 따르면, 2022년 1-11월 태국의 자동차 생산량은 172만 대에 육박하며 전년 동기 대비 약 21% 성장해 2022년 목표치인 약 175만 대에 크게 근접한 것으로 나타남. 태국 전기차 시장은 2022-2025년 동안 약 22%의 연평균 복합 성장률(CAGR)을 나타낼 것으로 예상됩니다. 이는 조사 대상 시장 수요를 증가시킬 가능성이 높습니다.

- 태국 국토 교통부에 따르면 2022년 1월부터 4월까지 태국 방콕에서 등록된 승용차 신규 등록 대수는 약 152,400대라고 합니다. 태국 수도의 승용차 신규 등록 대수는 지난 10년동안 변동이 있었으며 2021 년과 2020년방콕의 신차 등록 대수는 각각 269.83 대와 292.3 대를 기록했습니다.

- 이러한 요인으로 인해 태국의 플라스틱 시장은 예측 기간 동안 안정적인 성장을 보일 것으로 예상됩니다.

태국의 플라스틱 산업 개요

태국의 플라스틱 시장은 부분적으로 통합되어 있습니다. 주요 기업으로는 Indorama Ventures Public Company Limited, SCG Chemicals, INEOS Styrolution Group GmbH, COVESTRO AG, THAI PLASTIC INDUSTRIES 등이 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 성장 촉진요인

- 성장 억제요인

- 밸류체인 분석

- Porter의 Five Forces 분석

- 공급 기업의 교섭력

- 바이어의 교섭력

- 신규 진출업체의 위협

- 대체품의 위협

- 경쟁 정도

제5장 시장 세분화(금액 기준 시장 규모)

- 유형

- 기존 플라스틱

- 폴리에틸렌

- 폴리프로필렌

- 폴리스티렌

- 폴리염화비닐

- 엔지니어링·플라스틱

- 폴리에틸렌 테레프탈레이트(PET)

- 폴리아미드

- 폴리카보네이트

- 스티렌 공중합체(ABS와 SAN)

- 폴리부틸렌 테레프탈레이트(PBT)

- 폴리 메타크릴산메틸(PMMA)

- 기타 엔지니어링 플라스틱

- 바이오플라스틱

- 기존 플라스틱

- 용도

- 포장

- 전기 및 전자

- 건축 및 건설

- 자동차 및 운송

- 가구 및 침구

- 기타

제6장 경쟁 구도

- 인수합병(M&A)/합작투자(JV)/협업/협정

- 시장 점유율(%)**/순위 분석

- 주요 기업의 전략

- 기업 개요

- Covestro AG

- HMC Polymers Thailand

- Indorama Ventures Public Company Limited

- INEOS Styrolution Group GmbH

- PTT Global Chemical Public Company Limited

- SCG Chemicals Co. Ltd

- Thai Plastic Industries Co. Ltd

제7장 시장 기회와 향후 동향

LSH 25.01.22The Thailand Plastics Market is expected to register a CAGR of greater than 5% during the forecast period.

The market was negatively impacted by COVID-19. The production of plastics was reduced due to disruptions in the supply chain. However, the sector has been recovering well since restrictions were lifted. The rise in the level of industrial activities is likely to positively impact the studied market.

Key Highlights

- Over the short term, increasing usage of plastics in building and construction, and rising demand for food and beverage packaging, are some factors driving the market growth.

- On the flip side, stringent government regulations resulting in the plastic ban are expected to hinder market growth during the forecast period.

- Increasing investments in biodegradable plastics will likely create opportunities for the market in the coming years.

Thailand Plastic Market Trends

Polyethylene Terephthalate (PET) is Expected to Dominate the Market

- Polyethylene Terephthalate (PET) resins are known for their excellent melt flow characteristics, close molding tolerances, and high productivity from multi-cavity molds. Owing to its mechanical and electrical properties, PET is often used to replace metals in motor housings, switches, sensors, and other electrical applications.

- PET and polyolefins are the most widely used materials in the plastic packaging industry. Some of the significant properties of PET as a packaging material are recyclability, strength, and versatility, which drive the demand for these products.

- These products include take-out containers, frozen foods, carbonated drinks and juices, ketchup, bottled water, jars, and baked goods containers. They are also used in the food industry for clamshells, deli containers, and microwave food trays.

- PET also has excellent barrier properties that protect and preserve the product's contents. PET keeps the fizz in carbonated soft drinks, the vitamins in juices, and the color in ketchup intact. In other words, it protects products and keeps them on the shelves and out of the rubbish bin.

- Thailand's Indorama Ventures, the world's top producer of PET, in November 2020, announced spending USD 1.5 billion to triple its plastics recycling operations to increase the demand among green-minded beverage producers. Indorama has been acquiring companies that recycle polyethylene terephthalate in recent years. It aims to expand its recycling capacity to 750,000 tons a year by 2025 from the current roughly 250,000 tons. The goal is to have recycled materials account for around 20% of the 4 million tons of PET Indorama supplies to the beverage industry a year.

- In May 2022, a Thailand-based company named ENVICCO Limited started a new recycled plastic plant with the capacity to manufacture around 45,000 metric tons per year of recycled polyethylene terephthalate at Map Ta Phut, Rayong, Thailand. This will likely increase PET penetration in Thailand's plastics market.

- Owing to the abovementioned factors, the demand for PET will increase in the country over the forecast period.

Automotive Industry to Dominate the Market

- The automotive industry mainly uses engineering plastics as they are known for their high performance, thereby making the automotive parts compatible with the rigorous demands of the automotive sector. Mostly, engineering plastics are very versatile, which makes them suitable for achieving the needed innovation in the automotive industry. Moreover, these plastics are lightweight, which reduces fuel consumption.

- Some of the widely used plastics in the automotive industry include polypropylene, polyurethane, Polyvinyl chloride, Polybutylene Terephthalate (PBT), and others.

- Polypropylene is a very durable polymer that is manufactured from propylene. Owing to its chemical resistance and durability, polypropylene is used in various automotive components ranging from bumpers to cable insulation to carpet fibers.

- Polyurethanes are exceptionally resistant to radiation, solvents, and environmental wear. Owing to these qualities, they are well-suited for different applications, including the manufacturing of tires, seating, suspension brushes, etc.

- Thermoplastic-engineered polymers serve the automotive industry in different applications, such as the production of high-quality dashboard components, pillar trim, automotive instrument panels, wheel covers, door liners, seat backs, handles, and seat belt components, among others. This is expected to boost the demand for the studied market over the forecast period.

- Plastics are also more economical than metals and help to make automobiles energy-efficient by reducing weight, and offering durability, toughness, design flexibility, resiliency, corrosion resistance, and high performance. Some plastics also exhibit good electrical insulation properties.

- There are around 1,800 companies in Thailand in the automotive segment, which includes nearly 30 to 40 major players, about 700 Tier 1 automotive part manufacturers, and more than 1,000 Tier 2 and 3 producers. The presence of many major companies in the country not only signifies a vast automotive supply chain but also that the automotive industry is primed for further industry growth in the coming years.

- Car production in Thailand increased by nearly 15% year-on-year (Y-o-Y) to around 190,155 units in November 2022, which is the highest in the last 44 months, as the shortage of semiconductors continued to ease, according to the report of the Federation of Thai Industries (FTI).

- Furthermore, as per the FTI, the total number of car production in Thailand for the first 11 months of 2022 reached nearly 1.72 million units, registering a year-on-year growth of around 21%, and very close to the 2022 target of about 1.75 million units. The EVs market in Thailand is likely to register a CAGR of around 22% from 2022 to 2025. This is likely to boost the demand for the market studied.

- As per the Department of Land Transport (Thailand), around 152.4 thousand new private cars were registered in Bangkok, Thailand, from January to April 2022. The number of new registrations for passenger cars in the capital city of Thailand has fluctuated over the past 10 years. The number of new private cars registered in Bangkok in 2021 and 2020 was 269.83 and 292.3, respectively.

- Due to all such factors, the market for plastics in Thailand is expected to have steady growth during the forecast period.

Thailand Plastic Industry Overview

The plastics market in Thailand is partially consolidated in nature. The major companies include Indorama Ventures Public Company Limited, SCG Chemicals Co. Ltd, INEOS Styrolution Group GmbH, COVESTRO AG, and THAI PLASTIC INDUSTRIES CO. LTD, among others (not in any particular order).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Usage of Plastics in Building and Construction

- 4.1.2 Rising Demand from Food and Beverage Packaging

- 4.2 Restraints

- 4.2.1 Stringent Government Regulations Resulting in Plastic Ban

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Type

- 5.1.1 Traditional Plastics

- 5.1.1.1 Polyethylene

- 5.1.1.2 Polypropylene

- 5.1.1.3 Polystyrene

- 5.1.1.4 Polyvinyl Chloride

- 5.1.2 Engineering Plastics

- 5.1.2.1 Polyethylene Terephthalate (PET)

- 5.1.2.2 Polyamides

- 5.1.2.3 Polycarbonates

- 5.1.2.4 Styrene Copolymers (ABS and SAN)

- 5.1.2.5 Polybutylene Terephthalate (PBT)

- 5.1.2.6 Polymethyl Methacrylate (PMMA)

- 5.1.2.7 Other Engineering Plastics

- 5.1.3 Bioplastics

- 5.1.1 Traditional Plastics

- 5.2 Application

- 5.2.1 Packaging

- 5.2.2 Electrical and Electronics

- 5.2.3 Building and Construction

- 5.2.4 Automotive and Transportation

- 5.2.5 Furniture and Bedding

- 5.2.6 Other Applications

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Covestro AG

- 6.4.2 HMC Polymers Thailand

- 6.4.3 Indorama Ventures Public Company Limited

- 6.4.4 INEOS Styrolution Group GmbH

- 6.4.5 PTT Global Chemical Public Company Limited

- 6.4.6 SCG Chemicals Co. Ltd

- 6.4.7 Thai Plastic Industries Co. Ltd

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Investments in Biodegradable Plastics