|

시장보고서

상품코드

1628849

아시아태평양의 금속 캔 : 시장 점유율 분석, 산업 동향 및 성장 예측(2025-2030년)Asia Pacific Metal Cans - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

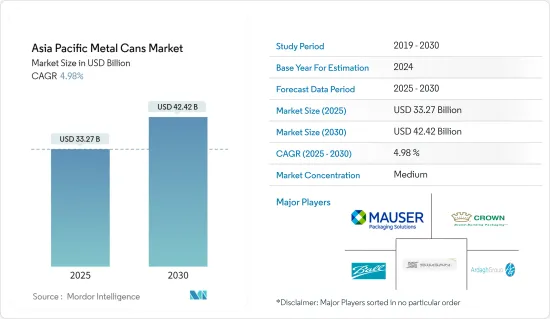

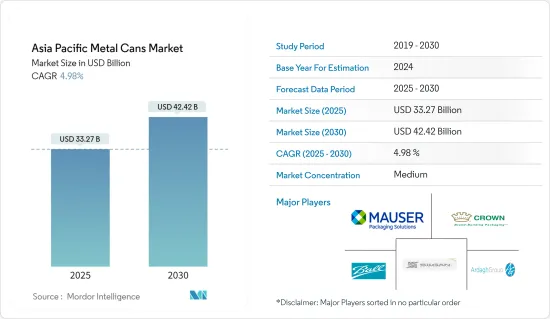

아시아태평양의 금속 캔 시장 규모는 2025년 332억 7,000만 달러로 추정되며, 예측 기간(2025-2030년) 동안 4.98%의 연평균 복합 성장률(CAGR)로 성장을 지속하여 2030년에는 424억 2,000만 달러에 달할 것으로 예상됩니다.

주요 하이라이트

- 금속 캔 시장은 기술 혁신과 지속가능성에 대한 엄격한 추구에 힘입어 패러다임의 전환이 일어나고 있습니다. 환경 친화적인 포장 솔루션을 찾는 전 세계적인 움직임에 발맞추어 제조업체들은 최첨단 소재와 친환경적인 방법을 채택하고 있습니다.

- 캔은 휴대가 간편하고 가볍기 때문에 소비자에게 이상적입니다. 또한 캔을 사용하면 흘림이나 파손의 위험을 최소화할 수 있기 때문에 야외 활동이나 이벤트에서 특히 인기가 높습니다. 캔 음료에 대한 소비자의 선호도 증가, 에너지 음료 및 스포츠 음료의 인기 증가, 지속 가능한 포장재에 대한 수요 증가는 시장의 중요한 촉진요인 중 일부입니다.

- 아시아태평양의 플라스틱 폐기물에 대한 우려는 예측 기간 동안 금속 포장의 성장 요인 중 하나가 될 것으로 보입니다. 제조업체와 소비자는 현재 저비용과 편의성과 같은 다른 고려사항을 우선시하고 있습니다. 그러나 향후 금속 포장의 확대는 포장 폐기물을 규제하고 줄이기 위한 정부 이니셔티브 증가로 인해 촉진될 수 있습니다.

- 아시아 전역에서 식품 포장 산업은 유통기한을 연장하기 위해 금속 캔에 대한 의존도를 높이고 있으며, 이는 이상적인 방부 특성과 구조적 무결성으로 인해 유통기한을 연장할 수 있기 때문입니다. 소비자들이 바쁜 라이프스타일과 업무 스케줄을 소화하는 가운데 편리한 포장 식품은 식생활의 필수품이 되고 있습니다.

- 소형 멀티팩 포맷에 대한 선호가 금속 캔 시장의 성장을 주도하고 있습니다. 인도, 중국, 일본을 포함한 아시아태평양 시장에서는 미니 캔에 대한 수요가 증가하고 있습니다. 이에 따라 많은 지역 음료 제조업체들이 기존 캔보다 소량, 저비용의 미니 캔을 도입하고 있습니다.

- 아시아의 동향은 동남아시아의 성장과 맞물려 있습니다. 중국과 일본 제조업체들은 이 지역에서 존재감을 높이고 있습니다. 예를 들어, 쇼와 알루미늄 캔은 프로젝트를 통해 중기 사업 성장을 위해 동남아시아를 전략적으로 공략하고 있습니다.

- 제조 공정의 혁신, 다양한 형태와 크기, 스마트 패키징의 진보로 인해 금속 캔 제조업체는 시장 트렌드에 부합하고 있습니다. 다단계 인쇄 및 라벨링이 가능한 깨끗한 표면은 중요한 마케팅 혁신을 일으키고 있습니다.

- 일례로 인도의 Hindustan Tin Works Ltd는 산소, 습기, 박테리아에 대한 우수한 장벽을 제공하여 설치류와 해충을 억제하고 소비까지 제품의 안전성을 보장하는 일반 라인 캔을 생산하고 있습니다.

- 금속 캔, 특히 알루미늄 캔은 재활용을 선도하고 있습니다. 알루미늄 캔은 수명 주기가 끝나면 품질 저하 없이 재활용할 수 있기 때문에 플라스틱이나 종이와 같은 대체재를 제치고 브랜드가 선호하는 포장재로 자리 잡았으며, 60일 만에 새 캔으로 다시 판매될 수 있는 신속성은 식품, 음료 및 에어로졸 산업에서 알루미늄 캔의 매력을 더욱 돋보이게 합니다. 알루미늄의 매력을 강조하고 있습니다.

- 그러나 금속 캔은 대체 포장 솔루션과 치열한 경쟁에 직면해 있습니다. 특히 병이나 페트병과 같은 형태의 플라스틱 포장이 주요 경쟁자가 되고 있습니다. 또한, 폴리머 기반 대체품의 출현과 원자재 가격의 변동은 이 지역의 금속 캔 시장에 도전이 되고 있습니다.

아시아태평양의 금속 캔 시장 동향

통조림 식품이 제공하는 편리함과 저렴한 가격이 시장 성장을 견인

- 화학물질이 없는 대안에 대한 수요가 증가함에 따라 통조림 식품 시장에서 혁신적인 포장이 증가하고 있습니다. 많은 통조림 식품 브랜드가 BPA가 없는 용기에 식품을 제공하기 시작했습니다.

- 식품을 유해한 박테리아로부터 보호하기 위해 밀폐되고 장난을 칠 수 없는 스틸 용기 식품에 대한 수요가 높습니다. 또한, 소비자의 바쁜 라이프 스타일로 인해 통조림 식품의 중요성이 더욱 커질 것으로 예상됩니다.

- 반려동물사료 포장은 오염과 부패를 유발하는 습기 및 기타 환경 조건에 대한 장벽을 제공함으로써 식품의 품질과 안전에 큰 영향을 미칩니다. 반려동물사료 포장에는 일반적으로 금속이 사용되며, 일반적으로 주석이나 알루미늄이 사용되며 음식, 냄새, 누출을 방지하기 위해 밀봉되어 있습니다.

- 디자인의 유연성이 제한되고 캔을 여는 것이 불편하다는 것은 금속 반려동물사료 캔의 심각한 단점이었습니다. 이 부문에서는 철강 캔의 안전성과 재활용이 가능하고 재생 가능한 재료를 사용하여 환경 친화적 인 친환경성을 강조하여 경쟁을 강화하려고합니다. 금속 캔으로 포장된 반려동물사료는 캔의 밀폐성과 탬퍼 증거로 인해 플라스틱 대체품보다 선호되고 있습니다.

- 다른 장점으로는 저렴한 비용, 긴 보관 기간, 내구성, 습식 식품 제품에 대한 적합성 등이 있습니다. 또한 개봉이 용이하다는 점도 지속적인 비즈니스 기회로 이어질 것으로 예상됩니다. 금속 식품 캔의 빠른 충전 속도와 라인 효율성은 제조업체들이 생산 시간이 오래 걸리고 생산 비용이 높은 플라스틱 대체품으로 생산 전환을 꺼리게 만드는 요인이기도 합니다.

눈부신 성장세를 보이고 있는 인도

- 최근 몇 년동안 인도 음료 산업에서 주스 포장이 크게 변화하고 있습니다. 이러한 변화는 단순히 트렌드를 따라가는 것뿐만 아니라 소비자의 취향 변화와 환경 문제에 대한 인식의 변화를 반영하고 있습니다. 이에 따라 제조업체들은 인도에서 지속 가능한 제품을 출시하는 것을 우선순위로 삼고 있습니다.

- 2024년, Ball Corporation은 혁신적이고 지속 가능한 알루미늄 포장의 세계 리더인 Del Monte Foods와 파트너십을 맺었습니다. 양사는 지속가능성을 위해 노력하고 있으며, 2030년까지 탄소 집약도를 45% 감축하고 2030년까지 순배출량 제로를 달성하겠다는 인도 정부의 야심찬 목표에 부합하는 델몬테 푸드는 Ball의 지원을 받아 기존 3피스 깡통에서 무한 재활용이 가능한 2피스 알루미늄 음료수 캔으로 전환했습니다. 재활용이 가능한 2피스 알루미늄 음료수 캔으로 전환했습니다.

- 또한, 최근 일회용 플라스틱 금지에 대한 규제는 플라스틱 포장의 성장을 가속할 것으로 예상되며, 모든 이해관계자와의 논의가 끝나는 대로 시행될 예정입니다. 인도 식품안전표준청(Food Safety and Standards Authority of India)은 친환경 대체품에 대응하기 위해 일회용 플라스틱 소재 사용 금지를 재검토하고 있습니다.

- 알코올 음료 및 비알코올 음료 시장의 성장에 따라 금속 캔 포장에 대한 수요는 국내에서 크게 증가할 것으로 예상됩니다. 예를 들어, 인도 크래프트 맥주 협회에 따르면 지난 5년 동안 인도의 양조장 수는 20개에서 120개로 급증했습니다.

- 인도 알루미늄 음료 캔 협회(ABCAI) 컨소시엄은 플라스틱 및 유리 포장재에서 알루미늄으로의 전환을 추진하고 있으며, ABCAI는 2030년까지이 수치를 약 25%까지 끌어 올리는 것을 목표로하고 있습니다.

- 광업부 데이터에 따르면 알루미늄의 1차 생산량은 2022-2023년 40.73라카톤(LT)에서 2023-2024년 41.59LT로 증가해 성장률이 2.1%를 나타낼 것으로 예상됩니다. 이러한 알루미늄 생산량 증가는 금속 캔에 대한 수요가 급증하고 있음을 보여줍니다. 금속 캔 생산은 알루미늄에 크게 의존하고 있기 때문에 생산량 증가는 제조업체가 이러한 소비자의 강력한 수요를 충족시키기 위해 금속 캔 생산을 강화하고 있음을 보여줍니다.

- 또한, 인도 내 신생 기업의 맥주 시장 확대도 인도 금속 캔 부문을 촉진하고 있습니다. 또한 Ball Corporation은 음료 제품의 요구 사항을 충족하는 금속 캔을 제공하고 있으며 인도에서 연간 13 억 캔의 생산 능력을 보유하고 있습니다. Ball Corporation에 따르면 인도의 1인당 맥주 소비량은 1캔 이하로, 금속 포장 및 공급업체에게 신흥 시장을 개척할 수 있는 큰 기회가 되고 있습니다.

- 또한 음료 제조업체와 인도 캔 제조업체의 협력 관계도 금속 캔 시장의 성장을 가속하고 있습니다. 예를 들어, 2024년 하이네켄(HEINEKEN)의 자회사인 United Breweries of India는 CANPACK과 협력하여 여성스러움을 주제로 한 한정판 맥주를 출시했습니다. 'Queenfisher'라는 이름의 이 새로운 프리미엄 라거는 회사의 주력 브랜드인 'Kingfisher'를 보완하기 위해 디자인되었습니다.

아태지역 금속 캔 산업 개요

아시아태평양의 금속 캔 시장은 세분화되어 있으며, Ball Corporation, Crown Holdings, Ardagh Group SA, Silgan Holdings Inc. 등 다양한 주요 기업들로 구성되어 있습니다. 이들 기업은 혁신, 제휴, 인수합병(M&A)을 통해 금속 캔 시장에서의 사업 확장에 적극 나서고 있습니다.

2024년 5월, Ball Corporation은 지속 가능한 포장을 향한 큰 움직임으로 유제품 산업의 선구자인 CavinKare와 파트너십을 맺었습니다. 이 제휴는 CavinKare의 유명한 밀크쉐이크용 레토르트 2피스 알루미늄 캔을 출시하여 유제품 포장을 혁신하는 것을 목표로 하고 있습니다.

유제품 및 유제품 대체품 부문은 인도에서 매우 중요하며, 2028년까지 연간 4.1%의 성장률을 나타낼 것으로 예상된다고 회사 측은 전망했습니다. Ball India는 다양한 맛을 제공함으로써 더 빠른 성장을 예상하여 레디 투 드링크 부문에 집중하고 있으며, 유제품 부문의 요구에 맞게 특별히 설계된 레토르트 알루미늄 캔의 생산 능력을 강화하고 있습니다. 이러한 포트폴리오 확장은 제품 혁신과 지속가능성에 대한 우리의 약속을 강조하며, 다양한 맛의 유제품을 알루미늄 캔에 쉽게 포장할 수 있게 해줍니다.

2023년 7월, 크라운홀딩스는 10월 30일부터 11월 1일까지 태국 방콕에서 열리는 아시아 캔테크 2023(Asia CanTech 2023)의 연사 일정에 참여한다고 발표했습니다. 이 사업에서는 태국, 베트남, 캄보디아를 포함한 음료용 알루미늄 캔의 재활용률에 대한 조사 결과를 논의할 예정입니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

- 시장 개요

- 산업 밸류체인 분석

- 산업의 매력 - Porter의 Five Forces 분석

- 공급 기업의 교섭력

- 바이어의 교섭력

- 신규 진출업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 역학

- 시장 성장 촉진요인

- 시장 성장 억제요인

제6장 시장 세분화

- 재료 유형

- 알루미늄

- 스틸

- 제품 유형

- 2-piece

- 3-piece

- 캔 유형

- 식품 캔

- 채소

- 과일

- 반려동물 사료

- 수프

- 커피

- 기타 식품 캔

- 음료 캔

- 주류

- 무알코올

- 에어로졸 캔

- 화장품 및 퍼스널케어

- 가정용

- 페인트 및 바니시

- 의약품 및 동물

- 자동차 및 산업

- 기타 에어로졸 캔

- 기타 캔 유형

- 식품 캔

- 국가명

- 인도

- 중국

- 한국

- 일본

- 호주 및 뉴질랜드

제7장 경쟁 구도

- 기업 개요

- Amcor PLC

- Ball Corporation

- Mauser Packaging Solutions

- Crown Holdings Inc.

- CANPACK SA

- Toyo Seikan Group Holdings Ltd

- Showa Denko K.K.

- Hindustan Tin Works Ltd

- AJ Packaging Limited

- Nanchang Ever Bright Industrial Trade Co. Ltd(EBI)

- Shanghai Jima Industrial Co. Ltd

제8장 투자 분석

제9장 시장 기회와 향후 동향

LSH 25.01.22The Asia Pacific Metal Cans Market size is estimated at USD 33.27 billion in 2025, and is expected to reach USD 42.42 billion by 2030, at a CAGR of 4.98% during the forecast period (2025-2030).

Key Highlights

- The metal cans market is witnessing a paradigm shift fueled by a severe search for innovation and sustainability. Manufacturers increasingly adopt cutting-edge materials and eco-friendly practices, aligning with the global push for environmentally responsible packaging solutions.

- Cans are easy to carry and light in weight, making them ideal for consumers. Additionally, using cans helps minimize the risk of spills or breakage, making them especially popular for outdoor activities and events. The increasing consumer preference for canned drinks, the rising popularity of energy and sports drinks, and the growing demand for sustainable packaging materials are some of the critical drivers of the market.

- Concerns about plastic waste in various Asia-Pacific countries will likely be one of the growth factors for metal packaging during the forecast period. Manufacturers and consumers now prioritize other considerations, such as low cost and convenience. However, the future expansion of metal packaging may be aided by increased government initiatives to regulate and decrease packaging waste.

- Across Asia, the food packaging industry increasingly relies on metal cans due to their ideal preservative properties and structural integrity, which extend shelf life. Packaged and convenient foods have become dietary staples as consumers juggle hectic lifestyles and work schedules.

- Trends like a preference for smaller and multi-pack formats are driving the growth of the metal cans market. There is a rising demand for mini-cans in the Asia-Pacific markets, including India, China, and Japan. In response, many regional beverage companies are introducing mini-cans, which offer smaller volumes at a lower cost than traditional cans.

- Asian trends are intertwined with the growth of Southeast Asia. Manufacturers from China and Japan are broadening their presence in the region. For instance, Showa Aluminum Can Corporation, through its project, is strategically targeting Southeast Asia for medium-term business growth.

- Innovations in manufacturing processes, diverse shapes and sizes, and advancements in smart packaging are enabling metal can manufacturers to stay aligned with market trends. Clean surfaces that accommodate multi-stage printing and labeling are drawing significant marketing innovations.

- As an illustration, Hindustan Tin Works Ltd from India produces general line cans that offer superior barriers against oxygen, moisture, and bacteria and deter rodents and pests, ensuring product safety until consumption.

- Metal cans, especially aluminum, lead the way in recycling. Their ability to be recycled without any loss of quality at the end of their life cycle makes them the preferred choice for packaging for brands, surpassing alternatives such as plastic and paper. This swift return to shelves as new cans in 60 days underscores aluminum's appeal in the food, beverage, and aerosol industries.

- However, metal cans grapple with stiff competition from alternative packaging solutions. Plastic packaging, especially in forms like bottles and pails, stands as the primary competitor. Additionally, the emergence of polymer-based substitutes and fluctuating raw material prices pose challenges for the metal cans market in the region.

Asia Pacific Metal Cans Market Trends

Convenience and Lower Price Offered by Canned Food to Drive the Market Growth

- The canned food market is seeing a rise in innovative packaging due to the growing demand for chemical-free options. Many brands of canned food products have started offering food in BPA-free containers.

- The demand for sealed and tamper-proof steel container food is high, as they protect food from harmful bacteria. Also, due to consumers' busy lifestyles, canned food is expected to gain more importance.

- Pet food packaging can significantly influence the quality and safety of the food product by providing barriers to moisture and other environmental conditions that may result in contamination and spoilage. Metal is commonly used in pet food packaging, typically tin or aluminum, and is tightly sealed to prevent any food, odors, or leaks from escaping.

- Limited design flexibility and inconvenience in opening the cans have been the significant disadvantages of metal pet food cans. This segment is trying to increase its competitiveness by emphasizing steel cans' safety and environmental friendliness, owing to their recyclability and use of recycled content. Pet food packaged in metal cans is preferred over plastic alternatives due to cans' tight seal and tamper evidence.

- Other advantages include its low cost, long shelf life, durability, and amenability to wet food products. Additionally, easy opening ends are expected to support continued opportunities. Fast-filling speeds and line efficiencies of metal food cans also make manufacturers reluctant to shift production to plastic alternatives, which are slower to manufacture and involve added production costs.

India to Witness Significant Growth

- In recent years, the Indian beverage industry has seen a significant shift in juice packaging. This evolution goes beyond merely following trends; it reflects changing consumer preferences and a growing awareness of environmental issues. In light of this, manufacturers are prioritizing sustainable product launches in India.

- In 2024, Ball Corporation partnered with Del Monte Foods, a global leader in innovative, sustainable aluminum packaging. Both companies are committed to sustainability, aligning with the Indian government's ambitious goals of achieving net-zero emissions by 2070 and cutting carbon intensity by 45% by 2030. With Ball's backing, Del Monte Foods moved from traditional three-piece tin cans to infinitely recyclable two-piece aluminum beverage cans.

- Additionally, the recent regulation on the ban on single-use plastics is expected to grow plastic packaging growth, which is scheduled to be enforced once the discussion with all the stakeholders is concluded. The Food Safety and Standards Authority of India is reviewing the ban on using single-use plastic materials to accommodate eco-friendly alternatives.

- With the growth of the alcoholic and non-alcoholic beverage market, the demand for metal can packages is expected to increase significantly in the country. For instance, according to the Craft Brewers Association of India, the number of microbreweries in India galloped from 20 to 120 in the past five years.

- The Aluminum Beverage Can Association of India (ABCAI) consortium is pushing for a shift from plastic and glass packaging to aluminum. Aluminum cans hold a mere 5% share of the country's packaging landscape, but ABCAI aims to elevate this figure to approximately 25% by 2030.

- Also, the Ministry of Mines data reveals that primary aluminum production rose from 40.73 lakh tons (LT) in FY 2022-2023 to 41.59 LT in FY 2023-2024, marking a growth rate of 2.1%. This increase in aluminum production signals a burgeoning demand for metal cans. Given that producing metal cans heavily relies on aluminum, the increased production volume indicates that manufacturers are ramping up metal can production to cater to this surging consumer appetite.

- Moreover, the proliferation in the beer market by newer companies in the country is helping the Indian metal can segment. Ball Corporations also provide metal cans that meet the requirement of beverage products, with an annual capacity of 1.3 billion cans in India. According to the Ball Corporation, the consumption in India is less than one can per capita, which presents a massive opportunity for metal packaging providers to tap into the emerging market.

- Also, collaborations between beverage companies and can manufacturers in India fuel the growth of the metal cans market. For example, in 2024, United Breweries of India, a subsidiary of HEINEKEN, partnered with CANPACK to unveil a limited-edition beer prominently featuring a feminine theme. This new premium lager, dubbed 'Queenfisher', is designed to complement the company's flagship 'Kingfisher' brand.

Asia Pacific Metal Cans Industry Overview

The Asia-Pacific metal cans market is fragmented and consists of a diverse array of key players, including Ball Corporation, Crown Holdings, Ardagh Group SA, Silgan Holdings Inc., and Mauser Packaging Solution. These companies actively focus on business expansion in the metal cans market through innovations, collaborations, and mergers and acquisitions.

May 2024: As a major move toward sustainable packaging, Ball Corporation teamed up with CavinKare, a trailblazer in the dairy industry. The collaboration aims to transform dairy packaging by rolling out retort two-piece aluminum cans for CavinKare's renowned milkshakes.

The dairy and dairy alternatives segment is pivotal in India and is projected to expand at an annual growth rate of 4.1% by 2028, as per company projections. The company concentrates on the ready-to-drink segment, anticipating quicker growth by diverse flavor offerings. Ball India has bolstered its capabilities to manufacture retort aluminum cans specifically designed for the dairy sector's needs. This portfolio expansion emphasizes the commitment to product innovation and sustainability and facilitates the packaging a diverse range of flavored dairy products in aluminum cans.

July 2023: Crown Holdings announced it would join the schedule of speakers at Asia CanTech 2023, which will be held in Bangkok, Thailand, from October 30 to November 1. The business will discuss the study's findings on the recycling rates of aluminum beverage cans, including Thailand, Vietnam, and Cambodia.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 High Recyclability Rates of Metal Packaging

- 5.1.2 Convenience and Lower Price Offered by Canned Food

- 5.2 Market Restraints

- 5.2.1 Presence of Alternate Packaging Solutions

- 5.2.2 Fluctuating Raw Material Prices in the Region

6 MARKET SEGMENTATION

- 6.1 Material Type

- 6.1.1 Aluminium

- 6.1.2 Steel

- 6.2 Product Type

- 6.2.1 2-piece

- 6.2.2 3-piece

- 6.3 Can Type

- 6.3.1 Food Cans**

- 6.3.1.1 Vegetables

- 6.3.1.2 Fruits

- 6.3.1.3 Pet Food

- 6.3.1.4 Soups

- 6.3.1.5 Coffee

- 6.3.1.6 Other Food Cans

- 6.3.2 Beverages Cans

- 6.3.2.1 Alcoholic

- 6.3.2.2 Non-alcoholic

- 6.3.3 Aerosol Cans**

- 6.3.3.1 Cosmetics and Personal Care

- 6.3.3.2 Household

- 6.3.3.3 Paints and Varnishes

- 6.3.3.4 Pharmaceutical/Veterinary

- 6.3.3.5 Automotive/Industrial

- 6.3.3.6 Other Aerosol Cans

- 6.3.4 Other Cans Types

- 6.3.1 Food Cans**

- 6.4 Country

- 6.4.1 India

- 6.4.2 China

- 6.4.3 South Korea

- 6.4.4 Japan

- 6.4.5 Australia and New Zealand

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Amcor PLC

- 7.1.2 Ball Corporation

- 7.1.3 Mauser Packaging Solutions

- 7.1.4 Crown Holdings Inc.

- 7.1.5 CANPACK SA

- 7.1.6 Toyo Seikan Group Holdings Ltd

- 7.1.7 Showa Denko K.K.

- 7.1.8 Hindustan Tin Works Ltd

- 7.1.9 AJ Packaging Limited

- 7.1.10 Nanchang Ever Bright Industrial Trade Co. Ltd (EBI)

- 7.1.11 Shanghai Jima Industrial Co. Ltd