|

시장보고서

상품코드

1851714

소매용 포장(RRP) : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Retail Ready Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

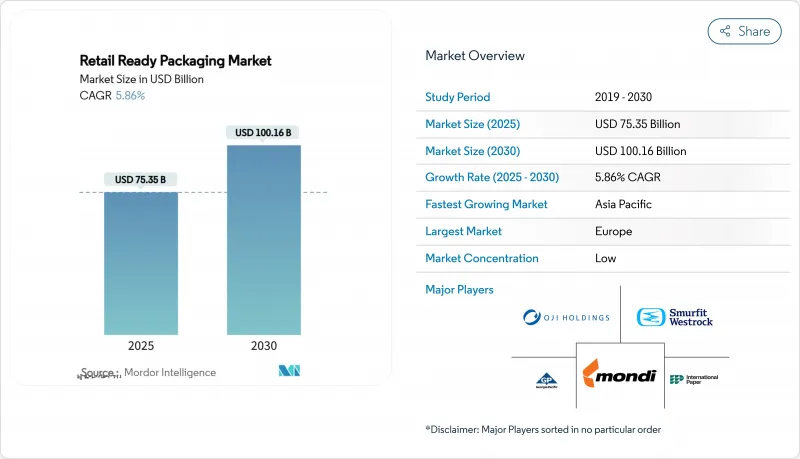

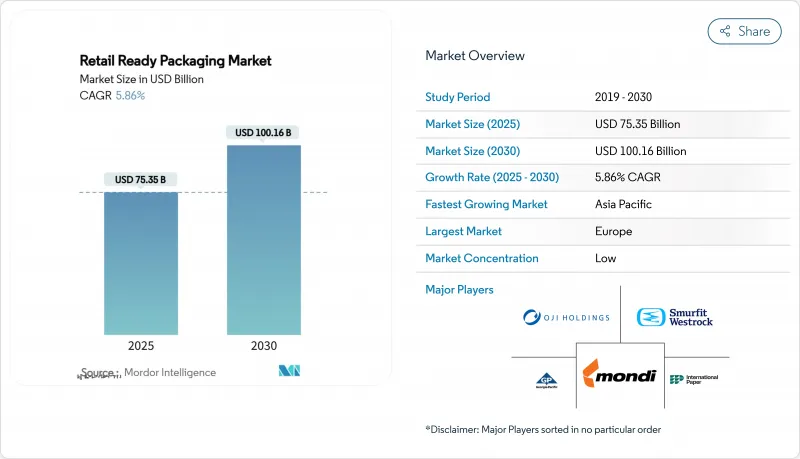

소매용 포장 시장 규모는 2025년에 753억 5,000만 달러로 평가되었고, 2030년에는 1,001억 6,000만 달러에 이를 것으로 예측되며, 5.86%의 연평균 복합 성장률(CAGR)을 나타낼 전망입니다.

전자상거래 매출 확대, 유통업체의 선반 준비형 포맷 요구 증가, 매장 내 인력 부족 현상이 수요를 지속적으로 높이고 있습니다. 대형 체인점들은 이제 정확한 케이스 치수와 개봉 디자인을 지정하여 보충 시간을 최대 40%까지 단축하고 있습니다. 동시에 유럽과 미국 여러 주의 생산자 책임 확대 제도는 폐기 비용을 절감하고 재활용을 단순화하는 단일 소재 섬유 솔루션으로 공급업체를 유도하고 있습니다. 암코(Amcor)의 베리 글로벌(Berry Global) 합병 및 소노코(Sonoco)의 에비오시스(Eviosys) 인수와 같은 합병은 자동화와 신속한 디자인 맞춤화를 지원할 수 있는 수직 통합 플랫폼을 확장하여 글로벌 브랜드 소유주와의 경쟁 우위를 제공합니다. 이에 대응하여 중견 변환업체들은 라인 전환 시간을 시간 단위에서 분 단위로 단축하는 AI 기반 장비에 대한 투자를 늘려, 지역별 프로모션에 부응하는 수익성 있는 소량 배치 생산을 가능하게 합니다.

세계의 소매용 포장 시장 동향 및 인사이트

순환경제 규제로 가속화되는 단일 소재 섬유 SRP 채택

2025년 1월 발효되는 유럽연합의 포장재 및 포장 폐기물 규정(PPWR)은 재활용 가능성 기준을 도입하여 다층 라미네이트의 경제적 매력을 떨어뜨립니다. 제한된 조합에 대한 준수 비용은 톤당 최대 739달러에 달해, 소매업체와 브랜드 소유자들이 기존 가정용 재활용 프로그램에 원활히 통합되는 단일 섬유 구조로 수렴하도록 장려합니다. 글로벌 소비재 기업들은 중복 사양 관리를 피하기 위해 지역 간 이러한 포맷을 표준화하며, 규정을 준수하는 변환업체에게 선점 우위를 부여합니다. 미국에서도 유사한 추세가 형성되고 있는데, 캘리포니아주의 SB 343 법안은 대규모 재활용이 입증된 기판에만 재활용 기호 사용을 허용합니다. 캐나다, 일본 및 주요 라틴 아메리카 시장에서도 유사한 규정이 등장함에 따라 단일 소재 디자인은 지역적 선호에서 글로벌 입찰의 기본 요건으로 전환되고 있습니다.

전자상거래 초고속 성장으로 인한 선반 준비형 포장 규정 준수 수요 증가

온라인 주문량이 물류 센터를 압박함에 따라 대형 소매업체들은 엄격한 선반 준비 요건을 도입하고, 공급업체가 비준수 케이스를 배송할 경우 청구서 금액의 3%를 초과할 수 있는 차감 벌금을 적용합니다. GS1 선라이즈 2027 로드맵에 부합하는 일련화된 2D 바코드와 확대되는 RFID 의무화는 재고 정확도를 케이스에 직접 내장하여 자동 분류 및 실시간 재고 확인을 가능하게 합니다. 포장은 이제 데이터 캐리어 역할을 수행하여 비용이 많이 드는 수동 스캔을 줄여 고가의 스마트 포맷 도입을 정당화합니다. 통합된 NFC 태그는 브랜드가 제품 진위성을 검증하고 개봉 시점에 앱 기반 프로모션을 시작할 수 있게 하여, 소매용 포장 시장 참여자들에게 추가적인 마케팅 활용 사례를 창출합니다.

골판지 가격 변동

라이너보드 가격은 단 1년 만에 15-25% 변동했으며, 북미 주요 제지공장이 2025년 1월 톤당 70달러 인상을 발표하자 몇 주 만에 가공업체 청구서에 반영되었습니다. 후가공 단계에서 추가로 20-30%의 마진이 붙기 때문에 브랜드 소유사는 케이스 비용이 급격히 변동하는 것을 목격하며 프로모션 예산 수립이 복잡해집니다. 수직 통합형 대기업은 제지 공장 보유로 노출을 완화하지만, 소규모 독립 업체들은 마진 압박에 직면하거나 입찰 경쟁력을 저해하는 추가 요금을 전가해야 합니다. 아시아태평양 지역의 추가 생산 능력 가동으로 변동성이 완화될 수 있으나, 유럽의 높은 에너지 비용으로 원자재 전망은 불확실합니다.

부문 분석

2024년 소매용 포장 시장 점유율의 55.34%를 차지한 종이 및 판지는 대량 생산되는 FMCG(일상 소비재)의 기본 소재로 자리매김하고 있습니다. 골판지 용기용지는 내구성 있는 운송 보호 기능을 제공하면서 인쇄 가능한 크라프트 표면을 통해 브랜딩 및 재활용 가능성 주장을 충족시킵니다. 접이식 박스용지는 고급 그래픽과 강성이 공존하는 분야에서 입지를 확대하고 있으며, 특히 과자류 선물용 패키지에서 두드러집니다. 고형 표백 황산지지는 내유성과 밝은 백색도가 필요한 냉장 유제품 출시를 보호합니다. 백색 코팅 칩보드는 수용 가능한 진열 마감과 함께 비용 효율성을 추구하는 중저가 시리얼 및 가정용 필수품을 지원합니다.

하이브리드 및 기타 소재는 2030년까지 연평균 7.43% 성장률을 보일 전망입니다. 가공업체들이 바이오 폴리머, 차단 코팅, 센서 층을 단일 구조로 융합하기 때문입니다. PLA와 PHA 혼합물은 농산물용 퇴비화 가능 옵션을 제공하며, 초기 상용화 사례에서 습한 공급망 환경에서의 진열 성능을 입증했습니다. 전도성 잉크를 활용한 스마트 라벨은 PET 창에 완벽하게 통합되어 2차 포장을 스캔 가능한 상거래 노드로 전환합니다. 플라스틱은 수분 또는 천공 보호가 필요한 틈새 역할을 유지하지만, 수성 분산 코팅 기술의 발전으로 섬유 기판이 냉동 환경에서도 기존 다층 필름에 도전할 수 있게 되었습니다. 글로벌 브랜드가 기능성을 저하시키지 않으면서 지역별 상이한 폐기물 감축 목표를 충족하기 위해 이러한 하이브리드 소재를 채택함에 따라 소매용 포장 시장이 혜택을 보게 됩니다.

소매용 포장 시장은 소재 유형(종이 및 판지, 플라스틱, 하이브리드, 기타 소재), 패키지 유형(다이컷 디스플레이 용기, 골판지 상자, 수축 포장 트레이, 기타), 최종 사용자 용도(식품 및 음료, 가정용품 및 홈 케어 용품, 퍼스널케어 및 화장품, 기타), 지역별로 구분되고 있습니다. 시장 예측은 금액(달러)으로 제공됩니다.

지역별 분석

아시아태평양 지역은 2030년까지 9.01%의 최고 연평균 성장률(CAGR)을 기록할 것으로 예상되며, 중국, 인도 및 동남아시아 국가들이 공급망을 현대화하고 자동화된 주문 처리 시설을 구축하고 있습니다. 현지 골판지 제조업체들은 프리미엄 소비자 가전 출시를 겨냥해 다색 플렉소 인쇄기로 업그레이드하고 있으며, 지역 펄프·제지 대기업들은 급증하는 전자상거래 케이스 수요를 충족시키기 위해 컨테이너보드 공장의 병목 현상을 해소하고 있습니다. 호주와 뉴질랜드의 특정 일회용 플라스틱 금지 정책은 유제품 및 농산물 수출업체 전반에 걸쳐 섬유 기반 SRP(소매용 포장) 채택을 가속화하고 있습니다. 다국적 컨버터 기업들은 싱가포르와 상하이에 디자인 센터를 확장해 글로벌 브랜드 이미지를 지역 문화적 특성에 맞게 현지화함으로써 소매용 포장 시장의 물량 성장을 뒷받침하고 있습니다.

유럽은 2024년 기준 35.63%의 점유율로 최대 단일 지역 블록을 유지합니다. PPWR(플라스틱 포장재 규제)에 따른 엄격한 재활용 목표가 2025년 시행되면서 독일, 프랑스, 북유럽 국가에서 표준화된 단일 섬유 포맷이 확산되고 있습니다. 영국의 '코트울드 커밋먼트'와 같은 소매 동맹은 소비 후 재활용 내용물 목표를 높여 폐쇄형 골판지 공장 투자 촉진을 이끌었습니다. 이탈리아는 전통 그래픽을 활용해 고부가가치 와인 및 과자 수출품 포지셔닝을 강화하며, 찢어 여는 SRP에 장식적 엠보싱을 통합했습니다. 스페인 온실 농산물 부문은 안달루시아 포장 현장에서 북유럽 유통 허브까지 공기 흐름을 최적화하는 통기성 다이컷을 도입했습니다.

북미는 매장 픽업과 소비자 직배송이 결합된 옴니채널 유통으로 성숙하지만 탄력적인 수요를 보여줍니다. 미국 대형 유통업체들은 일반 상품으로 RFID 적용을 확대하며, 2차 포장에 일련번호 태그를 내장해 품절률을 낮춥니다. 캐나다 식료품점들은 다가오는 연방 플라스틱 감축 규정에 부합하기 위해 수성 코팅으로 라미네이팅된 섬유 기반 육류 트레이를 시범 운영합니다. 멕시코 마킬라도라(가공 수출 기업)는 근거리 아웃소싱(nearshoring)의 혜택을 누리며 미국으로의 국경 간 운송용 골판지 케이스 주문이 증가하고 있습니다. 전반적으로, 자동화 투자는 인력 부족 시장에서 서비스 수준을 유지하는 핵심 수단으로 남아 있으며, 소매용 포장 시장의 건전한 단위 확장세를 지속시키고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 단일 소재 섬유 SRP 채택을 가속화하는 순환 경제 규정

- 전자상거래의 급성장이 선반 준비형 포장(SRP)의 준수 수요 증가

- 소매업체 인력 부족 - SRP로 매장 내 인건비 40% 절감

- AI 기반 포장 라인 자동화로 전환 속도 향상

- 브랜드 제조사, SRP 활용으로 진열대 전환율 향상

- 디지털 인쇄 경제성으로 SRP 내 소량 배치 프로모션 가능

- 시장 성장 억제요인

- 골판지 가격 변동

- 글로벌 SRP 표준화 부재로 인한 공급망 비용 증가

- SRP 형식 내 RFID/스마트 라벨 통합 비용

- 슈퍼마켓 규정 미준수 벌금 및 차감 청구

- 공급망 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 소재 유형별

- 종이 및 판지

- 골판지

- 폴딩 박스 보드(FBB)

- 고체 표백 황산염(SBS)

- 백색 라이닝 칩보드(WLC)

- 플라스틱

- PET

- 고밀도 폴리에틸렌

- PP

- 바이오플라스틱(PLA, PHA)

- 하이브리드 및 기타 소재

- 종이 및 판지

- 패키지 유형별

- 다이컷 및 디스플레이 용기

- 표준 RSC 다이컷

- 고화질 프리프린트 다이컷

- 골판지 상자

- 선반 준비형 RSC

- 핸들 일체형 SRP

- 수축 포장 트레이

- PE 수축

- 컴포스터블 수축

- 개조 케이스

- 하이월 케이스

- 소매 진열 케이스

- 플라스틱 용기

- 네스타블 크레이트

- 경질 플라스틱 트레이

- 기타(스탠드업 파우치, 재사용 가능 토트)

- 다이컷 및 디스플레이 용기

- 최종 사용자 용도별

- 식품 및 음료

- 조리 식품

- 신선 식품

- 고기 및 닭고기

- 베이커리 및 과자류

- 음료

- 청량 음료

- 알코올 음료

- 우유 음료

- 가정용품

- 퍼스널케어 및 화장품

- 가전제품

- 기타(DIY 및 가든, 반려동물 먹이)

- 식품 및 음료

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주, 뉴질랜드

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- 아랍에미리트(UAE)

- 사우디아라비아

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 나이지리아

- 이집트

- 기타 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Mondi Group

- Smurfit Westrock

- International Paper Company

- Georgia-Pacific LLC

- Oji Holdings Corporation

- Rengo Co., Ltd.

- Klabin SA

- Pratt Industries

- Graphic Packaging International

- STI Group

- Cardboard Box Company

- Weedon Group

- Caps Cases Limited

- Vanguard Packaging Inc.

- TricorBraun

- Huhtamaki Oyj

- Orora Limited

- Sealed Air Corporation

- Amcor PLC

- Sonoco Products Company

- Visy Industries

- Packaging Corporation of America

제7장 시장 기회와 장래의 전망

HBR 25.11.17The retail ready packaging market size is valued at USD 75.35 billion in 2025 and is projected to touch USD 100.16 billion by 2030, advancing at a 5.86% CAGR.

Expanding e-commerce sales, growing retailer mandates for shelf-ready formats and acute in-store labor shortages keep demand elevated. Large chains now specify exact case dimensions and opening designs, cutting replenishment time by as much as 40%. At the same time, Extended Producer Responsibility schemes in Europe and multiple US states push suppliers toward single-material fiber solutions that reduce disposal costs and simplify recycling. Mergers such as Amcor's union with Berry Global and Sonoco's Eviosys acquisition expand vertically integrated platforms able to fund automation and rapid design customization, giving them an edge with global brand owners. In response, mid-tier converters increase spending on AI-enabled equipment that trims line-changeover from hours to minutes, unlocking profitable micro-batch runs that meet localized promotions

Global Retail Ready Packaging Market Trends and Insights

Circular-economy regulations accelerating single-material fiber SRP adoption

The European Union's Packaging and Packaging Waste Regulation (PPWR) effective January 2025 introduces recyclability thresholds that make multi-layer laminates financially unattractive. Compliance fees on restricted combinations run as high as USD 739 per tonne, encouraging retailers and brand owners to converge on mono-fiber structures that slide seamlessly into existing curbside programs. Global consumer-goods companies standardize these formats across regions to avoid managing duplicate specifications, giving compliant converters first-mover advantage. Similar momentum builds in the United States where California's SB 343 limits the use of recycling symbols to substrates proven recyclable at scale.As comparable rules emerge in Canada, Japan and key Latin American markets, single-material designs transition from regional preference to baseline requirement for global tenders.

E-commerce hyper-growth raising shelf-ready packaging compliance demand

Online order volumes strain fulfillment centers, so large retailers institute strict shelf-ready requirements and apply charge-back penalties that can exceed 3% of invoice value when suppliers ship non-compliant cases. Serialized 2D barcodes aligned with the GS1 Sunrise 2027 roadmap and expanding RFID mandates embed inventory accuracy directly into the case, allowing automated sortation and real-time stock checks. Packaging now acts as a data carrier that lowers costly manual scans, justifying higher-priced smart formats. Integrated NFC tags additionally let brands validate product authenticity and launch app-based promotions at the point of unboxing, creating an incremental marketing use-case for retail ready packaging market participants.

Corrugated containerboard price volatility

Linerboard prices moved 15-25% within a single year, and a USD 70 per-ton increase announced for January 2025 by a leading North American mill flows through converter invoices within weeks. Because finishing adds a further 20-30% mark-up, brand owners see case costs swing sharply, complicating promotion budgets.Vertically integrated majors smooth exposure by owning mills, yet small independents face margin compression or must pass on surcharges that hurt competitiveness in tenders. Volatility may ease once additional capacity comes online in Asia-Pacific, but elevated energy costs in Europe keep the input outlook uncertain.

Other drivers and restraints analyzed in the detailed report include:

- Retailer labor shortages driving SRP adoption for 40% man-hour reduction

- AI-enabled packaging line automation boosting changeover speed

- Lack of global SRP standardization inflating supply-chain costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Paper and paperboard controlled 55.34% of retail ready packaging market share in 2024 and remains the default substrate for high-volume FMCG goods. Corrugated containerboard supplies durable transit protection while presenting printable kraft surfaces that align with branding and recyclability claims. Folding boxboard gains ground where premium graphics and rigidity coexist, notably in confectionery gift packs. Solid bleached sulfate safeguards chilled dairy launches that need grease resistance and bright whiteness. White-lined chipboard supports value-tier cereals and household staples that seek cost efficiency with acceptable shelf finish.

Hybrid and other materials expand at a 7.43% CAGR through 2030 as converters fuse bio-polymers, barrier coatings and sensor layers into single structures. PLA and PHA blends open compostable options for produce, and early commercial runs demonstrate shelf performance in humid supply chains. Smart labels relying on conductive inks integrate seamlessly onto PET windows, turning secondary packs into scan-ready commerce nodes. Although plastics retain niche roles demanding moisture or puncture protection, advances in aqueous dispersion coatings allow fiber substrates to challenge incumbent multilayer films even in freezer environments. The retail ready packaging market benefits as global brands adopt these hybrids to meet diverging regional waste-reduction targets without sacrificing functionality.

Retail Ready Packaging Market is Segmented by Material Type (Paper and Paperboard, Plastics, Hybrid and Other Materials), Package Type (Die-Cut Display Containers, Corrugated Cardboard Boxes, Shrink-Wrapped Trays, and More), End-User Application (Food, Beverage, Household and Home-Care Products, Personal Care and Cosmetics, and More), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific delivers the highest 9.01% CAGR through 2030 with China, India and Southeast Asia modernizing supply chains and installing automated fulfillment facilities. Local corrugators upgrade to multi-color flexo machines to target premium consumer electronics launches, while regional pulp-and-paper majors debottleneck containerboard mills to satisfy surging e-commerce case demand. Government policies in Australia and New Zealand banning certain single-use plastics accelerate fiber SRP adoption across dairy and produce exporters. Multinational converters expand design centers in Singapore and Shanghai to localize global brand imagery for regional cultural nuances, underpinning volume growth for the retail ready packaging market.

Europe retains 35.63% 2024 share, the largest single regional block. Strict recycling targets under PPWR take effect in 2025, driving standardized mono-fiber formats in Germany, France and the Nordics. Retail alliances such as the United Kingdom's Courtauld Commitment elevate post-consumer content goals, spurring investment in closed-loop containerboard mills. Italy leverages heritage graphics to position high-value wine and confectionery exports, integrating embellished embossing into tear-open SRP. Spain's greenhouse produce sector adopts vented die-cuts that optimize airflow from Andalusia packing sites to Northern European distribution hubs.

North America exhibits mature but resilient demand as omnichannel retailing blends store pick-up and direct-to-consumer flows. US mass merchants broaden RFID rollouts to general merchandise, embedding serialized tags in secondary packs to cut out-of-stock rates. Canadian grocers pilot fiber-based meat trays laminated with aqueous coatings to comply with upcoming federal plastic reduction rules. Mexican maquiladoras benefit from nearshoring, stimulating corrugated case orders for cross-border shipments into the United States. Overall, automation investment remains the key lever for maintaining service levels in a tight labor market, sustaining healthy unit expansion for the retail ready packaging market.

- Mondi Group

- Smurfit Westrock

- International Paper Company

- Georgia-Pacific LLC

- Oji Holdings Corporation

- Rengo Co., Ltd.

- Klabin S.A.

- Pratt Industries

- Graphic Packaging International

- STI Group

- Cardboard Box Company

- Weedon Group

- Caps Cases Limited

- Vanguard Packaging Inc.

- TricorBraun

- Huhtamaki Oyj

- Orora Limited

- Sealed Air Corporation

- Amcor PLC

- Sonoco Products Company

- Visy Industries

- Packaging Corporation of America

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Circular-economy regulations accelerating single-material fibre SRP adoption

- 4.2.2 E-commerce hyper-growth raising shelf-ready packaging (SRP) compliance demand

- 4.2.3 Retailer labour shortages - SRP cuts in-store man-hours by 40 %

- 4.2.4 AI-enabled packaging line automation boosting change-over speed

- 4.2.5 Branded manufacturers using SRP to lift on-shelf conversion rates

- 4.2.6 Digital-printing economics enabling micro-batch promotions in SRP

- 4.3 Market Restraints

- 4.3.1 Corrugated containerboard price volatility

- 4.3.2 Lack of global SRP standardisation inflating supply-chain cost

- 4.3.3 RFID / smart-label integration costs in SRP formats

- 4.3.4 Supermarket non-compliance fines and charge-backs

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material Type

- 5.1.1 Paper and Paperboard

- 5.1.1.1 Corrugated Containerboard

- 5.1.1.2 Folding Boxboard (FBB)

- 5.1.1.3 Solid Bleached Sulfate (SBS)

- 5.1.1.4 White-lined Chipboard (WLC)

- 5.1.2 Plastics

- 5.1.2.1 PET

- 5.1.2.2 HDPE

- 5.1.2.3 PP

- 5.1.2.4 Bio-plastics (PLA, PHA)

- 5.1.3 Hybrid and Other Materials

- 5.1.1 Paper and Paperboard

- 5.2 By Package Type

- 5.2.1 Die-cut Display Containers

- 5.2.1.1 Standard RSC Die-cuts

- 5.2.1.2 High-graphic Pre-print Die-cuts

- 5.2.2 Corrugated Cardboard Boxes

- 5.2.2.1 Shelf-ready RSC

- 5.2.2.2 Handle-integrated SRP

- 5.2.3 Shrink-wrapped Trays

- 5.2.3.1 PE Shrink

- 5.2.3.2 Compostable Shrink

- 5.2.4 Modified Cases

- 5.2.4.1 High Wall Cases

- 5.2.4.2 Retail-display Cases

- 5.2.5 Plastic Containers

- 5.2.5.1 Nestable Crates

- 5.2.5.2 Rigid Plastic Trays

- 5.2.6 Others (Stand-up Pouches, Re-usable Totes)

- 5.2.1 Die-cut Display Containers

- 5.3 By End-User Application

- 5.3.1 Food

- 5.3.1.1 Ready-to-eat Meals

- 5.3.1.2 Fresh Produce

- 5.3.1.3 Meat and Poultry

- 5.3.1.4 Bakery and Confectionery

- 5.3.2 Beverage

- 5.3.2.1 Soft Drinks

- 5.3.2.2 Alcoholic Beverages

- 5.3.2.3 Dairy Drinks

- 5.3.3 Household and Home-care Products

- 5.3.4 Personal Care and Cosmetics

- 5.3.5 Consumer Electronics and Appliances

- 5.3.6 Others (DIY and Garden, Pet Food)

- 5.3.1 Food

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Russia

- 5.4.2.7 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Australia and New Zealand

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 Middle East

- 5.4.4.1.1 United Arab Emirates

- 5.4.4.1.2 Saudi Arabia

- 5.4.4.1.3 Turkey

- 5.4.4.1.4 Rest of Middle East

- 5.4.4.2 Africa

- 5.4.4.2.1 South Africa

- 5.4.4.2.2 Nigeria

- 5.4.4.2.3 Egypt

- 5.4.4.2.4 Rest of Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Mondi Group

- 6.4.2 Smurfit Westrock

- 6.4.3 International Paper Company

- 6.4.4 Georgia-Pacific LLC

- 6.4.5 Oji Holdings Corporation

- 6.4.6 Rengo Co., Ltd.

- 6.4.7 Klabin S.A.

- 6.4.8 Pratt Industries

- 6.4.9 Graphic Packaging International

- 6.4.10 STI Group

- 6.4.11 Cardboard Box Company

- 6.4.12 Weedon Group

- 6.4.13 Caps Cases Limited

- 6.4.14 Vanguard Packaging Inc.

- 6.4.15 TricorBraun

- 6.4.16 Huhtamaki Oyj

- 6.4.17 Orora Limited

- 6.4.18 Sealed Air Corporation

- 6.4.19 Amcor PLC

- 6.4.20 Sonoco Products Company

- 6.4.21 Visy Industries

- 6.4.22 Packaging Corporation of America

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment