|

시장보고서

상품코드

1630327

석유 및 가스 다운스트림 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Oil & Gas Downstream - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

■ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송일정은 문의해 주시기 바랍니다.

가격

※ 부가세 별도

한글목차

영문목차

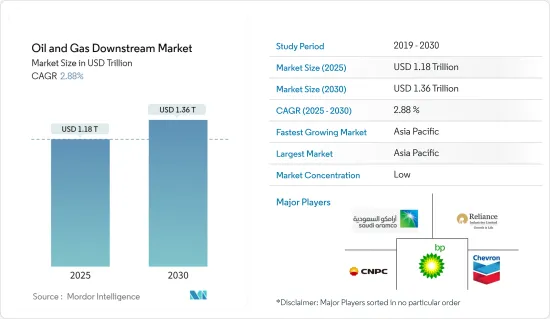

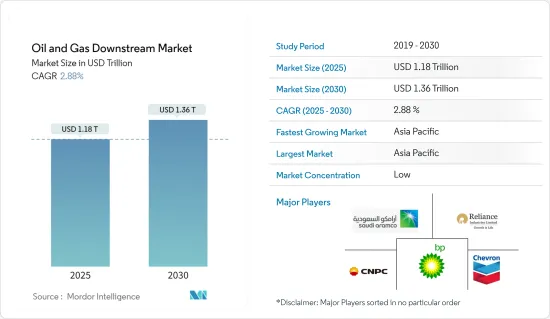

석유 및 가스 다운스트림 시장 규모는 2025년 1조 1,800억 달러로 추정 및 예측되며, 예측 기간(2025-2030년) 동안 2.88%의 CAGR을 기록하여 2030년에는 1조 3,600억 달러에 달할 것으로 예상됩니다.

주요 하이라이트

- 중기적으로는 아시아태평양 및 중동 지역의 정제 능력 증가와 신흥국의 산업화 진전 등의 요인이 예측 기간 동안 석유 및 가스 다운스트림 시장을 견인할 것으로 예상됩니다.

- 선진국과 신흥경제국에서의 저연비 차량 점유율 확대와 전기자동차 보급 확대는 예측 기간 동안 시장 개척에 걸림돌이 될 것으로 예상됩니다.

- 정제 및 석유화학 부문의 디지털화 및 현대화는 정제 비용과 공정 손실을 감소시킬 것으로 예상됩니다. 이는 예측 기간 동안 시장에 기회를 제공할 것으로 예상됩니다.

- 석유 및 가스 다운스트림 시장은 아시아태평양이 지배적이며, 대부분의 수요는 중국, 동남아시아 및 인도에서 발생합니다.

석유 및 가스 다운스트림 시장 동향

정유소 부문이 시장을 독식할 것으로 예상

- 정유소는 원유를 가공하여 휘발유, 디젤, 제트연료, 난방유, 석유화학제품 등 정제된 제품으로 전환하는 산업시설입니다. 정유소는 석유 및 가스 산업의 다운스트림 부문에서 에너지 및 화학제품 수요를 충족시키는 정제된 제품을 공급하는 중요한 역할을 담당하고 있습니다.

- 정유소는 석유 생산지, 주요 항로, 주요 수요지 근처에 전략적으로 배치되어 있습니다. 북미, 유럽, 아시아태평양, 중동 및 아프리카 등의 지역에 중요한 정제 기지가 있습니다.

- 또한, 각국은 처리 능력을 높이기 위해 정유소를 강화하는 데 주력하고 있습니다. 예를 들어, Energy Institute Statistical Review of World Energy에 따르면, 2023년 아시아태평양은 전 세계 정제 능력의 36.2%를 차지할 것으로 예상되며, 북미는 21.2%를 차지할 것으로 예상됩니다.

- 여러 기업이 기존 정유공장에 투자하여 정제능력을 증강하고 있습니다. 예를 들어, 태국석유공사는 2023년 3월 실라차 정유소의 정제 능력을 현재 280kb/d에서 400kb/d로 확대할 계획을 발표했습니다. 이 프로젝트는 2025년까지 약 5억 달러의 비용으로 완공될 예정입니다.

- 또한 여러 기업이 세계 각지에서 정유공장 건설에 투자하고 있습니다. 예를 들어, 2023년 4월, 인도 대사는 최근 몽골 최초의 정유공장이 인도의 지원으로 건설되고 있으며, 2025년까지 완공될 것으로 예상된다고 발표했습니다. 이 프로젝트는 12억 달러의 인도 소프트 론으로 자금을 조달하고 있으며, 몽골 정유소의 첫 번째 단계는 2023년 말까지 완공될 예정입니다. 정유소의 처리 능력은 연간 약 150만 톤에 달합니다.

- 또한 2023년 3월, 태국석유는 사업 성장을 위해 2023-2025년 사이 10억 달러 규모의 자본 투자 계획을 발표했습니다. 여기에는 청정연료 프로젝트(CFP) 전략의 일환으로 정유소 용량을 확장하고 고부가가치 연료 제품으로 전환하기 위한 5억 달러가 포함되어 있습니다. 이 프로젝트는 태국 실라차(Silacha) 정유소 용량을 기존 280kb/d에서 400kb/d로 확장하고, 연료유를 디젤 및 제트 연료와 같은 고부가가치 제품으로 개선할 계획입니다.

- 많은 국가 정부도 정유소 신설에 대한 몇 가지 이니셔티브를 취했습니다. 예를 들어, 인도 정부는 2023년 2월 HPPCL 라자스탄 정유공장(HRRL) 프로젝트를 2024년 1월까지 완공하고 2024년까지 완전 가동할 계획이라고 발표했습니다. 에너지부 장관에 따르면, 정부는 나렌드라 모디 총리에게 2024년 1월 정유소 개장을 요청할 예정입니다.

- 따라서 기존 정유사의 정제 능력 향상과 신규 정유소 설립은 전 세계적으로 석유 및 가스 다운스트림 부문의 성장을 확인할 수 있을 것으로 예상됩니다.

아시아태평양이 시장을 독점할 것으로 예상

- 아시아태평양의 석유 및 가스 다운스트림 시장은 신흥국들의 에너지 수요 증가에 힘입어 강력한 성장세를 보이고 있습니다. 인구 증가와 산업화에 따라 중국과 인도와 같은 국가들의 에너지 소비가 급증하면서 정제 능력 확대, 기존 정제소 현대화, 석유화학 콤비네이션 개발 등 다운스트림 부문에 대한 투자가 활발히 이루어지고 있습니다.

- 세계 에너지 통계에 따르면 2023년 아시아태평양의 석유 정제 능력은 하루 3,740만 배럴에 달할 것이며, 2023년 현재 인도는 세계 석유 정제 능력의 거의 4.9%를 차지할 것으로 예상됩니다. 정유 제품에 대한 수요가 증가함에 따라 다운스트림 기업들은 신규 프로젝트에 투자하고 기존 시설을 확장하고 있습니다.

- 예를 들어, 2023년 9월 인도 총리는 Bharat Petroleum Corp Ltd(BPCL)의 정유공장 확장 및 Bina의 그린필드 석유화학 프로젝트의 초석을 놓았습니다. 이 확장 프로젝트를 통해 BPCL의 정제 능력은 780만 톤/년에서 1,100만 톤/년으로 증가할 것으로 예상됩니다. 또한 연간 220만 톤 이상의 석유화학제품을 생산할 수 있는 생산단지도 건설될 예정입니다. 이 프로젝트의 비용은 59억 달러입니다.

- 2023년 현재 중국은 전 세계 석유 정제 능력의 17.9%를 차지하고 있습니다. 예측 기간 동안 중국의 석유화학 및 정제 부문은 흑자로 전환될 것으로 예상됩니다.

- 2023년 3월, 사우디 아람코와 중국 파트너들은 중국의 석유화학 및 연료 수요 증가에 대응하기 위해 2026년 중국 북동부 지역의 석유화학 및 정유공장 프로젝트가 2026년 본격 가동될 것이라고 발표했습니다. 랴오닝성 반진시 프로젝트는 100억 달러가 소요될 것으로 예상되며, 아람코의 중국 내 두 번째 대규모 정유 및 석유화학 투자로 기록될 예정입니다.

- 또한 2023년 3월, 한국 롯데그룹의 자회사인 롯데케미칼 인도네시아는 인도네시아 반텐주에 석유화학단지를 건설하기 위한 자금 조달에 성공했으며, 이 프로젝트(LINE)는 PT Lotte Chemical Indonesia에 총 3.9억 달러의 중요한 투자입니다. Chemical Indonesia의 총 39억 달러 규모의 대규모 투자로, 2025년 완공 시 연간 100만 톤의 에틸렌과 52만 톤의 프로필렌 생산능력을 갖추게 됩니다.

- 석유 및 가스 다운스트림 시장은 정유 및 석유화학 부문에 대한 투자 증가와 각국의 기존 다운스트림 인프라 확대로 인해 예측 기간 동안 이 지역이 지배적인 위치를 차지할 것으로 예상됩니다.

석유 및 가스 다운스트림 산업 개요

석유 및 가스 다운스트림 시장은 적당히 세분화되어 있습니다. 이 시장의 주요 기업으로는 Reliance Industry Limited, BP PLC, 사우디 아람코(Saudi Aramco), 중국석유공사(China National Petroleum Corporation), 셰브론(Chevron Corporation) 등이 있습니다.

기타 혜택

- 엑셀 형식의 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 소개

- 조사 범위

- 시장 정의

- 조사 가정

제2장 주요 요약

제3장 조사 방법

제4장 시장 개요

- 소개

- 2029년까지 시장 규모와 수요 예측(단위 : 달러)

- 석유 및 가스 생산 시나리오(2013-2029년)

- 석유 및 가스 소비 시나리오(2013-2029)

- 정유소 처리 능력(2013-2029년)

- 주요 프로젝트 정보

- 기존 프로젝트

- 진행중인 프로젝트

- 향후 프로젝트

- 원유 가격 동향 분석(2013-2023년)

- 최근 동향과 개발

- 정부 규제와 시책

- 시장 역학

- 드라이버

- 아시아태평양과 중동의 정제 능력 증가

- 신흥 국가의 산업화 진전

- 성장 억제요인

- 전기자동차 보급 확대

- 드라이버

- 공급망 분석

- Porter's Five Forces 분석

- 공급 기업의 교섭력

- 소비자의 협상력

- 신규 참여업체의 위협

- 대체품의 위협

- 경쟁 기업 간의 경쟁 관계

제5장 시장 세분화

- 유형

- 정유소

- 석유화학 플랜트

- 시장 분석 : 지역별(2029년까지 시장 규모와 수요 예측)

- 북미

- 미국

- 캐나다

- 기타 북미

- 유럽

- 프랑스

- 이탈리아

- 독일

- 영국

- 스페인

- 북유럽 국가

- 터키

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 인도네시아

- 일본

- 한국

- 말레이시아

- 태국

- 베트남

- 기타 아시아태평양

- 남미

- 브라질

- 아르헨티나

- 콜롬비아

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트

- 남아프리카공화국

- 나이지리아

- 카타르

- 이집트

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- M&A, 합작투자, 제휴, 협정

- 주요 기업의 전략

- 기업 개요

- Reliance Industries Ltd

- Royal Dutch Shell PLC

- The Dow Chemical Company

- BP PLC

- Saudi Aramco

- Indian Oil Corporation Limited

- China National Petroleum Corporation

- Total SA

- Chevron Corporation

- List of Other Prominent Companies

- 시장 순위/점유율(%) 분석

제7장 시장 기회와 향후 동향

- 정제·석유화학 부문의 디지털화와 현대화

The Oil & Gas Downstream Market size is estimated at USD 1.18 trillion in 2025, and is expected to reach USD 1.36 trillion by 2030, at a CAGR of 2.88% during the forecast period (2025-2030).

Key Highlights

- In the medium term, factors such as increasing refining capacity across Asia-Pacific and the Middle East and rising industrialization in developing countries are expected to drive the oil and gas downstream market during the forecast period.

- The growing share of fuel-efficient vehicles and increasing penetration of electric vehicles in developed and emerging economies are expected to hinder the market's growth during the forecast period.

- Nevertheless, digitalization and modernization of the refining and petrochemical sectors are expected to reduce refining costs and process losses. This, in turn, is expected to create an opportunity for the market during the forecast period.

- Asia-Pacific has dominated the oil and gas downstream market, with the majority of the demand coming from China, Southeast Asia, and India.

Oil & Gas Downstream Market Trends

The Refineries Segment is Expected to Dominate the Market

- Refineries are industrial facilities where crude oil is processed and converted into refined products such as gasoline, diesel, jet fuel, heating oil, and petrochemicals. Refineries play a critical role in the downstream sector of the oil and gas industry by supplying refined products to meet energy and chemical demands.

- Refineries are located strategically near oil production regions, major shipping routes, and key demand centers. Significant refining hubs exist in regions such as North America, Europe, Asia-Pacific, and the Middle East and Africa.

- Further, countries are focused on enhancing their refineries to increase the throughput. For instance, according to the Energy Institute Statistical Review of World Energy, in 2023, Asia-Pacific holds nearly 36.2% of the global refining capacity, whereas North America has 21.2%.

- Several companies are investing in the existing refineries to increase their refining capacity. For instance, in March 2023, Thai Oil Public Company Limited announced that it plans to increase the refining capacity in the Sriracha refinery by 400 kb/d from the current 280 kb/d. The project is expected to be completed by 2025 at approximately USD 500 million.

- Several companies are also investing in the construction of refineries in many regions across the world. For instance, in April 2023, the Indian Ambassador recently announced that Mongolia's first oil refinery, which is being built with Indian assistance, is expected to be completed by 2025. The project is being funded through a USD 1.2 billion Indian soft loan, and the first stage of the Mongol Oil Refinery is set to be completed by the end of 2023. The refinery will have approximately 1.5 million metric tons of processing capacity annually.

- Further, in March 2023, Thai Oil announced plans to invest USD 1 billion in the capital between 2023 and 2025 to grow its business, including USD 500 million to expand its refinery capacity and transition to higher added-value fuel products as part of its Clean Fuel Project (CFP) strategy. The business intends to expand its oil refinery capacity in Sriracha (Thailand) to 400 kb/d, up from 280 kb/d, and upgrade fuel oil to higher-value products such as diesel and jet fuel.

- Governments in many countries also took several initiatives to establish new refineries. For instance, in February 2023, the Government of India announced that the HPPCL Rajasthan Refinery (HRRL) project is anticipated to be completed by January 2024 and be completely operational by 2024. According to the energy minister, the government will ask Prime Minister Narendra Modi to open the refinery in January 2024.

- Hence, increasing the refining capacity of the existing refineries and establishing new refineries are expected to witness the growth of the oil and gas downstream sector globally.

Asia-Pacific is Expected to Dominate the Market

- The Asia-Pacific oil and gas downstream market is witnessing robust growth driven by increasing energy demand in the region's emerging economies. With a growing population and industrialization, countries like China and India are experiencing a surge in energy consumption, boosting investments in downstream activities, including refining capacity expansion, modernization of existing refineries, and the development of petrochemical complexes are key trends in this market.

- According to a Statistical Review of World Energy data, in 2023, Asia-Pacific's oil refining capacity reached 37.4 million barrels per day. As of 2023, India accounted for almost 4.9% of global oil refinery capacity. The increasing demand for refined petroleum products has driven downstream companies to invest in new projects and expand existing facilities.

- For instance, in September 2023, the prime minister of India laid the foundation stone for Bharat Petroleum Corp Ltd's (BPCL) refinery expansion and greenfield petrochemical project in Bina. The expansion project is expected to increase BPCL's refinery capacity to 11m tonnes/year from 7.8m tonnes/year. A manufacturing complex will also be built to produce more than 2.2m tonnes/year of petrochemical products. The cost of this project is USD 5.9 billion.

- As of 2023, China accounted for 17.9% of global oil refining capacity. The country's petrochemical and refinery sector is expected to be positive during the forecast period.

- In March 2023, Saudi Aramco and its Chinese partners announced that they aim to start entire operations at a petrochemical and refinery project in northeast China in 2026 to meet the country's increasing demand for petrochemicals and fuel. The project in Liaoning province's city of Panjin, expected to cost USD 10 billion, will be Aramco's second significant refining-petrochemical investment in China.

- Further, in March 2023, Lotte Chemical Indonesia, a South Korea-based Lotte Group subsidiary, successfully secured financing for constructing a petrochemical complex in Banten Province, Indonesia. The project, known as the LINE, is a significant investment for PT Lotte Chemical Indonesia, with a total cost of USD 3.9 billion. Upon completion in 2025, the LINE petrochemical complex will have the capacity to manufacture 1 million tons of Ethylene and 520,000 tons of Propylene annually.

- Hence, the region is expected to dominate the oil and gas downstream market during the forecast period owing to the increasing investment in the refining and petrochemical sector and the expansion of existing downstream infrastructure in respective countries.

Oil & Gas Downstream Industry Overview

The oil and gas downstream market is moderately fragmented. Some of the key players in the market are Reliance Industry Limited, BP PLC, Saudi Aramco, China National Petroleum Corporation, and Chevron Corporation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Oil and Gas Production Scenario (2013 - 2029)

- 4.4 Oil and Gas Consumption Scenario (2013 - 2029)

- 4.5 Refinery Throughput Capacity (2013 - 2029)

- 4.6 Key Projects Information

- 4.6.1 Existing Projects

- 4.6.2 Projects in Pipeline

- 4.6.3 Upcoming Projects

- 4.7 Crude Oil Price Trend Analysis (2013 - 2023)

- 4.8 Recent Trends and Developments

- 4.9 Government Policies and Regulations

- 4.10 Market Dynamics

- 4.10.1 Drivers

- 4.10.1.1 Increasing Refining Capacity across Asia-Pacific and the Middle East

- 4.10.1.2 Rising Industrialization in Developing Countries

- 4.10.2 Restraints

- 4.10.2.1 Increasing Penetration of Electric Vehicles

- 4.10.1 Drivers

- 4.11 Supply Chain Analysis

- 4.12 Porter's Five Forces Analysis

- 4.12.1 Bargaining Power of Suppliers

- 4.12.2 Bargaining Power of Consumers

- 4.12.3 Threat of New Entrants

- 4.12.4 Threat of Substitutes Products and Services

- 4.12.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Refineries

- 5.1.2 Petrochemical Plants

- 5.2 Geography (Regional Market Analysis {Market Size and Demand Forecast till 2029 (for regions only)})

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.1.3 Rest of North America

- 5.2.2 Europe

- 5.2.2.1 France

- 5.2.2.2 Italy

- 5.2.2.3 Germany

- 5.2.2.4 United Kingdom

- 5.2.2.5 Spain

- 5.2.2.6 Nordic Countries

- 5.2.2.7 Turkey

- 5.2.2.8 Russia

- 5.2.2.9 Rest of Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 China

- 5.2.3.2 India

- 5.2.3.3 Indonesia

- 5.2.3.4 Japan

- 5.2.3.5 South Korea

- 5.2.3.6 Malaysia

- 5.2.3.7 Thailand

- 5.2.3.8 Vietnam

- 5.2.3.9 Rest of Asia-Pacific

- 5.2.4 South America

- 5.2.4.1 Brazil

- 5.2.4.2 Argentina

- 5.2.4.3 Colombia

- 5.2.4.4 Rest of South America

- 5.2.5 Middle East and Africa

- 5.2.5.1 Saudi Arabia

- 5.2.5.2 United Arab Emirates

- 5.2.5.3 South Africa

- 5.2.5.4 Nigeria

- 5.2.5.5 Qatar

- 5.2.5.6 Egypt

- 5.2.5.7 Rest of Middle East and Africa

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Reliance Industries Ltd

- 6.3.2 Royal Dutch Shell PLC

- 6.3.3 The Dow Chemical Company

- 6.3.4 BP PLC

- 6.3.5 Saudi Aramco

- 6.3.6 Indian Oil Corporation Limited

- 6.3.7 China National Petroleum Corporation

- 6.3.8 Total SA

- 6.3.9 Chevron Corporation

- 6.4 List of Other Prominent Companies

- 6.5 Market Ranking/Share (%) Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Digitalization and Modernization of the Refining and Petrochemical Sector