|

시장보고서

상품코드

1639465

태국의 석유 및 가스 다운스트림 시장 - 점유율 분석, 산업 동향, 성장 예측(2025-2030년)Thailand Oil and Gas Downstream - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

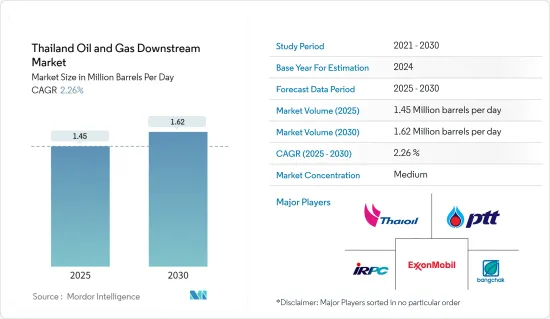

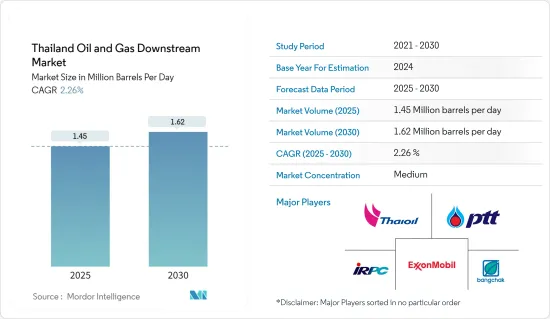

태국의 석유 및 가스 다운스트림 시장 규모는 2025년 145만 배럴/일, 2030년에는 162만 배럴/일에 이를 것으로 예측되며, 예측 기간(2025-2030년)중 CAGR은 2.26%로 예상됩니다.

조사 대상 시장은 2020년에 COVID-19의 악영향을 받은 것, 회복해 유행 전의 수준에 이르고 있습니다. 다양한 정제제품에 대한 수요가 높아지고 있는 가운데, 이 나라는 정유소 능력 개척에 주력하고 있어, 이것이 예측 기간중의 조사 대상 시장의 성장을 견인할 것으로 예상됩니다. 그러나 전기차의 보급 확대 등 보다 깨끗한 대체 에너지로의 전환 동향은 최종 사용자 산업으로부터의 정제 제품 수요를 저해하고 시장 성장을 억제할 것으로 예상됩니다.

안다만해에서는 가스전이 발견되어 수입가스에 대한 의존도와 천연가스 수송 비용 절감에 대한 낙관론이 높아지고 있습니다. 이 요인은 이 부문의 진출기업에 기회를 가져옵니다.

태국의 석유 및 가스 다운스트림 시장 동향

석유 정제 능력이 성장을 확인

태국은 소비하는 석유의 대부분을 생산하고 있지만, 증가하는 수요를 충족하기 위해 여전히 수입에 의존하고 있습니다. 태국 에너지 사업부에 따르면 가솔린 수요는 2020년 1일 3,000만 리터를 넘었지만, 연료(디젤과 가솔린) 소비량은 2021년 첫 10개월 만에 4.4% 감소하여 하루 평균 1억 3,100만 리터로 COVID-19 이전

태국의 정유소 부문은 정제 및 처리 능력에서 싱가포르에 이어 동남아시아 2위입니다. 태국에서는 정유소의 능력은 2016-2019년에 걸쳐 비교적 안정적이며, 2016년은 일량 123만 4,500배럴이었지만, 2021년에는 일량 124만 4,500배럴로 증가합니다. 정유소의 처리 능력은 최근 증가 추세에 있습니다. 이 나라에는 6개의 정유소 컴플렉스가 있으며, 그 대부분은 이 나라의 국영 석유 및 가스 복합기업 PTT가 일부 또는 전부를 소유하고 있습니다. 이 나라는 증가하는 국내 및 지역 수요에 대응하기 위해 정화 능력을 적극적으로 강화하고 있습니다. 예를 들어, Thai Oil의 시라차 정유소 확대 프로젝트는 이 회사의 클린 연료 프로젝트(CFP)의 일환이며, 2023년 말 완성시에는 총 용량이 40만 배럴/일이 될 전망입니다.

태국의 석유 정화 능력은 정유소 확대와 정유 수요 증가로 예측 기간 동안 약간 증가할 것으로 예상됩니다.

석유 및 가스 생산 감소가 시장을 억제

태국은 'Thailand 4.0'으로 전환하고 산업은 기술의 진보와 첨단 서비스로 전환하고 있습니다. 정부는 '차세대자동차' 개발을 최중요 대상 산업으로 지정하고 내연기관차(ICE)에서 동남아시아의 EV생산허브로 전환하는 EV관련 사업을 지원하고 있습니다.

전기자동차(EV) 산업은 EV 시장 성장을 뒷받침하는 정부의 호의적인 조치에 힘입어 태국에서 관심을 끌고 있습니다. 예를 들어 태국 정부는 이 나라의 EV 시장 개척을 추진하기 위해 세제 우대와 보조금 제도 등 EV 인센티브 제도를 전개했습니다.

National Electric Vehicles Policy Committee 2020은 2021년부터 2035년까지 태국의 EV 개발 프레임워크를 보여주는 로드맵을 도입하여 제로 방출 차량(ZEV) 생산을 위해 태국의 확립된 자동차 공급망을 변화시키고 현대적인 이동성을 위한 기술 능력을 구축했습니다. 로드맵은 EV 생산 및 사용뿐만 아니라 배터리 제조 및 공급, 충전소 및 송전망 관리 등의 지원 인프라, 종합적이고 통합적인 구현을 가능하게 하는 관련 안전 기준 및 규제 개발 계획을 다루고 있습니다. 마스터 플랜의 EV는 이륜차, 삼륜차, 버스, 트럭, 페리 보트 등 다양한 차량을 대상으로합니다.

태국 물품세국은 투자위원회(BOI)가 추진하는 10석 이하의 전동승용차에 대해 2020년 1월 1일부터 2022년 12월 31일까지는 0%, 2023년 1월 1일부터 2025년 12월 31일까지는 2%의 물품 세율을 적용하고 있습니다.

이 나라에서 새로 등록된 배터리 전기차는 2019년 724대에서 2021년 2,079대로 증가했습니다. EV가 증가함에 따라 이 나라에서는 민간인 모두의 투자가 증가하고 충전소의 수가 급증하고 있습니다. EVAT에 따르면 2021년 6월에는 전국 10개 개발업체로부터 2,224기의 충전기가 제공되며 664기 이상의 충전소이 설치되어 있다고 합니다. 태국 정부는 2036년까지 전국에 690개 충전소과 120만대의 전기자동차를 정비하는 것을 목표로 하고 있습니다.

태국의 석유 및 가스 다운스트림 경제에서는 운수부문이 중요한 역할을 하고 있습니다. 따라서 EV의 도입은 태국의 석유 및 가스 다운스트림 시장의 성장을 방해할 것으로 예상됩니다.

태국의 석유 및 가스 다운스트림 산업 개요

태국의 석유 및 가스 다운스트림 시장은 그 특성상 부분적으로 통합되어 있습니다. 시장의 주요 기업(순부동)에는 Exxon Mobil Corporation, PTT Public Company Limited, Thai Oil PCL, IRPC PCL, Bangchak Petroleum Public Company 등이 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사 범위

- 시장의 정의

- 조사의 전제

제2장 조사 방법

제3장 주요 요약

제4장 시장 개요

- 소개

- 2027년까지의 정제 설비 용량과 예측(단위:1,000 배럴/일)

- 최근 동향과 개발

- 정부의 규제와 시책

- 시장 역학

- 성장 촉진요인

- 억제요인

- 공급망 분석

- PESTLE 분석

제5장 시장 세분화

- 정유소별

- 개요

- 기존, 건설 중, 계획중인 프로젝트

- 석유화학 플랜트별

- 개요

- 기설, 건설중, 계획중의 프로젝트

- 연료 소매·판매

제6장 경쟁 구도

- M&A, 합작사업, 제휴, 협정

- 주요 기업의 전략

- 기업 프로파일

- PTT Public Company Limited

- Esso Thailand PLC

- Bangchak Corporation PCL

- Royal Dutch Shell PLC

- Caltex(Chevron Corporation)

- SCG Chemicals Co. Ltd(Siam Cement Group)

- IRPC Public Company Limited

- Total SA

- ExxonMobil Corp.

- PTG Energy PCL

제7장 시장 기회와 앞으로의 동향

JHS 25.02.10The Thailand Oil and Gas Downstream Market size is estimated at 1.45 million barrels per day in 2025, and is expected to reach 1.62 million barrels per day by 2030, at a CAGR of 2.26% during the forecast period (2025-2030).

Although the market studied was negatively impacted by COVID-19 in 2020, it has recovered and reached pre-pandemic levels. With the growing demand for various refined products, the country is focused on developing its refinery capacity, which is expected to drive the growth of the market studied during the forecast period. However, the shifting trend toward cleaner alternatives, such as the increasing adoption of electric vehicles, is expected to hinder the demand for refined products from end-user industries, which is expected to restrain the market's growth.

Gas fields have been discovered in the Andaman Sea, increasing optimism about reducing the dependence on imported gas and the cost of natural gas transportation. This factor is creating an opportunity for the players in the sector.

Thailand Oil and Gas Downstream Market Trends

Oil Refining Capacity to Witness Growth

Thailand produces a large share of the petroleum it consumes but still relies on imports to meet the increasing demand. Demand for gasoline stood above 30 million liters a day in 2020, while fuel (diesel and gasoline) consumption took a plunge of 4.4% in the first ten months of 2021 to a daily average of 131 million liters, the same level as before COVID-19 level, according to Department of Energy Business, Thailand.

The refinery sector of Thailand is the second largest in Southeast Asia in refining capacity and throughput, just after Singapore. In Thailand, the refineries' capacity has remained relatively stable during 2016-2019, at 1,234,500 barrels per day in 2016, which increased to 1,244,500 barrels per day in 2021. The refinery throughput has been increasing in recent years. The country has six refinery complexes, the majority of which are owned partially or fully by the country's national oil and gas conglomerate PTT. The country has been actively increasing its refining capacity to meet its growing domestic and regional demand. For instance, the expansion project of Thai Oil's Sriracha refinery, a part of the company's Clean Fuel Project (CFP), is expected to have a total capacity of 400,000 b/d when completed at the end of 2023.

Thailand's oil refining capacity is expected to grow slightly during the forecast period due to the expansion of refineries and increased demand for refined oil.

Decreasing Oil and Gas Production to Restrain the Market

Thailand is trying to transform into 'Thailand 4.0,' whose industries transition to technological advances and high-level services. The government designated 'next-generation automotive' development among the top targeted industries and supported EV-related businesses to transform from internal combustion engine (ICE) vehicles to an EV production hub in Southeast Asia.

The electric vehicle (EV) industry is gaining interest in Thailand, supported by favorable government policies to push the EV market's growth. For example, the government of Thailand rolled out EV incentive schemes, i.e., tax benefits and subsidy systems, to propel the development of the EV market in the country.

The National Electric Vehicles Policy Committee 2020 introduced a roadmap that lays out a framework for Thailand's EV development from 2021-2035 to transform the country's well-established automotive supply chain for the production of zero-emission vehicles (ZEVs) and build the technological capacity for modern mobility. The roadmap covers not only EV production and usage but also developing plans for battery manufacturing and supplies, supporting infrastructure, including charging stations and power grid management, and the development of related safety standards and regulations to enable comprehensive and integrated implementation. EVs in the master plan covers various vehicles, including motorcycles, tricycles, buses, trucks, and ferry boats.

The Excise Department of Thailand has been applying an excise tax rate of 0% from 1 January 2020 to 31 December 2022 and 2% from 1 January 2023 to 31 December 2025 to electric-powered passenger vehicles with seating not exceeding ten seats which are promoted by the Board of Investment (BOI).

The country's newly registered battery electric vehicles grew from 724 in 2019 to 2,079 in 2021. With an increase in the number of EVs, the country is also witnessing a surge in the number of charging stations with rising investments from both the public and private sectors. According to EVAT, the country had over 664 charging stations with 2,224 chargers from 10 developers nationwide in June 2021. By 2036, the Thai government aims to have 690 charging stations and 1.2 million electric vehicles nationwide.

The transportation sector plays a vital role in Thailand's downstream oil and gas economy. Therefore, the adoption of EVs is expected to hamper the growth of the downstream oil and gas market in Thailand.

Thailand Oil and Gas Downstream Industry Overview

The Thailand oil and gas downstream market is partially consolidated in nature. Some of the major players in the market (in no particular order) include Exxon Mobil Corporation, PTT Public Company Limited, Thai Oil PCL, IRPC PCL, and Bangchak Petroleum Public Company, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Installed Refining Capacity and Forecast, in thousand barrels per day, till 2027

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.2 Restraints

- 4.6 Supply Chain Analysis

- 4.7 PESTLE Analysis

5 MARKET SEGMENTATION

- 5.1 By Refineries

- 5.1.1 Overview

- 5.1.2 Existing, Under Construction, and Planned Projects

- 5.2 By Petrochemical Plants

- 5.2.1 Overview

- 5.2.2 Existing, Under Construction, and Planned Projects

- 5.3 By Fuel Retail and Marketing

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 PTT Public Company Limited

- 6.3.2 Esso Thailand PLC

- 6.3.3 Bangchak Corporation PCL

- 6.3.4 Royal Dutch Shell PLC

- 6.3.5 Caltex (Chevron Corporation)

- 6.3.6 SCG Chemicals Co. Ltd (Siam Cement Group)

- 6.3.7 IRPC Public Company Limited

- 6.3.8 Total SA

- 6.3.9 ExxonMobil Corp.

- 6.3.10 PTG Energy PCL