|

시장보고서

상품코드

1630344

폴리프로필렌 포장 필름 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Polypropylene Packaging Films - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

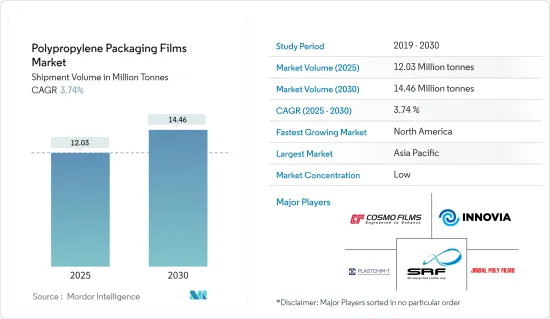

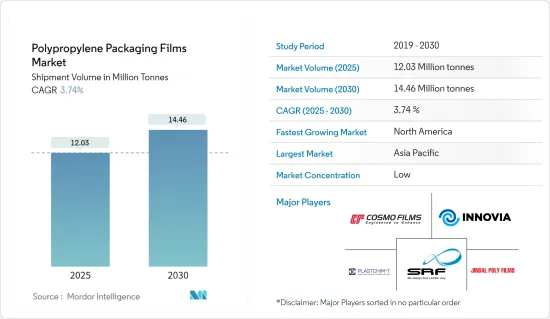

출하량 기준 폴리프로필렌 포장 필름 시장 규모는 예측 기간(2025-2030년) 동안 연평균 3.74%의 CAGR로 2025년 1,203만 톤에서 2030년 1,446만 톤으로 성장할 것으로 예상됩니다.

연질 플라스틱 포장은 폴리프로필렌 포장 필름 시장에서 크게 성장하고 있는 분야 중 하나입니다. 플라스틱의 최고의 품질을 결합하고 적은 재료로 광범위한 보호 특성을 제공하는 포장 필름은 식품 및 기타 비식품 관련 제품의 부가가치와 시장성을 높입니다.

포장 산업은 변화하는 소비자 요구에 부응하기 위해 끊임없이 적응하고 있습니다. 가처분 소득의 증가와 중산층의 급격한 증가와 같은 주요 요인으로 인해 소비재, 식품, 음료, 산업 제품 등 다양한 분야에서 폴리프로필렌 포장 필름에 대한 수요가 증가하고 있습니다.

또한, 지속가능성에 대한 관심이 높아지면서 전통적인 경질 포장 솔루션이 혁신적이고 친환경적인 연질 플라스틱 포장으로 대체되고 있습니다. 이러한 변화는 사용자 친화적인 포장과 제품 보호 강화에 대한 욕구 증가와 함께 폴리프로필렌 포장 필름에 대한 수요를 증가시킬 것으로 예상됩니다.

폴리프로필렌은 PE보다 융점이 높고 다양한 용도에 사용할 수 있어 연질 포장 부문에서 견인차 역할을 하고 있습니다. 또한, 전 세계적으로 재사용 가능한 포장재에서 일회용 포장재로의 전환은 폴리프로필렌 필름에 대한 수요를 강화할 것으로 예상됩니다.

제품의 유통기한을 연장하는 필름에 대한 수요가 증가하면서 폴리프로필렌 포장 필름 시장의 성장을 견인하고 있습니다. 또한, 환경 친화적인 대체 포장재를 쉽게 구할 수 있게 되면서 폴리프로필렌 필름의 용도가 다양해져 시장 확대에 더욱 박차를 가하고 있습니다.

2024년 4월, 앰코와 킴벌리 클라크는 협력하여 페루에서 30% 재활용 소재를 사용한 에코 프로텍트 기저귀의 새로운 포장을 출시했습니다. Amcor는 Kimberly Clark을 위해 이 혁신적인 포장의 설계 및 제조를 주도하여 순환 경제에 대한 약속을 강조했으며, 이 저자극성 기저귀 포장은 식물성 섬유로 만들어지고 재활용 재료를 함유하고 있어 지속가능성을 촉진합니다.

그러나 시장은 팬데믹의 영향으로 공급망과 제조 시설의 큰 혼란에 시달리고 있습니다. 또한, 에너지 위기로 인한 원자재 가격 상승은 시장 성장에 잠재적인 위협이 되고 있습니다.

폴리프로필렌 포장 필름 시장 동향

BOPP 필름은 큰 성장을 이루다

- BOPP 필름은 기계적 및 수동 연신 공정을 통해 교차 방향으로 연신됩니다. 공 압출 구조가 특징인 이 필름은 투명, 불투명, 금속화가 가능하며, BOPP 필름의 다양성과 장점은 포장 산업에서 금속 캔과 카톤을 대체할 수 있는 잠재력을 가지고 있으며, BOPP 필름은 높은 인장 강도, 낮은 연신율, 우수한 가스 차단성, 향상된 강성, 낮은 헤이즈 감소를 제공합니다. 높은 인장강도, 낮은 연신율, 우수한 가스 차단성, 강성 향상, 헤이즈 감소를 실현합니다.

- 실용적인 솔루션과 편리한 운송에 대한 소비자의 수요에 힘 입어 BOPP 필름에 대한 수요가 급증하고 있습니다. 식품 포장의 엄격한 요구 사항을 고려할 때 BOPP 필름은 수요가 증가할 준비가 되어 있습니다.

- BOPP 단층 웹 및 라미네이트는 비누 및 칫솔과 같은 제품을 포장하기 위해 퍼스널케어 및 홈케어 산업에서 일반적으로 사용됩니다. 그 외에도 이 필름은 뛰어난 내화학성, 평평한 표면적, 자외선 차단 기능을 자랑합니다. 재활용이 가능하고 무해하기 때문에 인기와 수요가 증가하고 있습니다. 또한, 수증기, 오일, 그리스에 대한 견고한 장벽을 제공합니다.

- BOPP 필름은 밀봉 능력과 산소 차단 역할로 인해 제약 및 화장품 산업에서 점점 더 선호되고 있습니다. 이러한 추세는 2023년 세계 화장품 시장에서 북미가 29%의 점유율을 차지할 것이라는 전망에서 알 수 있습니다.

- 특히 BOPP 필름은 다른 플라스틱 필름보다 환경 발자국이 적고, 녹는 정도가 낮기 때문에 가공 시 에너지 소비가 적고, 폴리에틸렌과의 라미네이션이 용이하며, 광범위한 폴리올레핀 화학 그룹의 일원으로서 광범위한 재활용이 가능합니다. BOPP 필름은 낮은 융점으로 인해 가공시 에너지 소비가 적고, 폴리에틸렌과 쉽게 적층 할 수 있으며, 광범위한 폴리올레핀 화학 그룹의 일원으로서 광범위한 재활용성을 유지합니다.

- 폴리프로필렌 포장 필름 시장의 주요 기업들이 BOPP 필름 생산을 강화하고 있습니다. 예를 들어, Toppan은 2024년 3월 인도에서 친환경적이고 혁신적인 배리어 필름 "GL-SP"를 출시 할 것이라고 발표했습니다. 인도의 TOPPAN Speciality Films(TSF)와 공동으로 개발한 이 제품은 이축연신 폴리프로필렌(BOPP)을 기반으로 합니다.

아시아태평양이 가장 큰 시장 점유율을 차지

- 아시아태평양에서 플라스틱 재료에 대한 편리한 접근성은 폴리 프로필렌 포장 필름의 성장을 크게 촉진하고 있습니다. 인도 브랜드 에쿼티 재단의 2024년 7월 보고서에 따르면 인도 상공부는 인도 서부의 플라스틱 소비가 47%를 차지하며, 북부가 23%, 남부가 21%를 차지한다고 강조하고 있습니다. 이 소비를 주도하는 주요 산업은 자동차, 포장, 가전제품 등입니다. 중국은 플라스틱 포장의 매우 중요한 시장으로 부상하고 있지만, 성장을 저해할 수 있는 규제 금지라는 도전에 직면해 있습니다.

- 포장 식품 및 조리 식품에 대한 수요 증가와 E-Commerce의 급속한 확장으로 폴리 프로필렌 포장 필름에 대한 수요가 증가하고 있습니다. 식음료, 제약, 퍼스널케어 및 기타 산업에서 연질 포장 솔루션에 대한 선호도가 점점 더 높아지고 있습니다. 폴리프로필렌 필름의 매력은 우수한 차단성, 내구성 및 시각적 매력으로 인해 다양한 포장 용도에 이상적입니다.

- 급증하는 중산층과 조직화된 소매업의 부상은 연포장 산업의 성장에 중요한 촉매제입니다. 특정 세계 포장 요구 사항을 수반하는 수출 급증은 포장 산업에 더욱 활력을 불어넣고 있습니다. 아시아태평양의 포장 환경을 지배하고 있는 플라스틱 연포장은 전통적인 경질 포장 사용자들 사이에서도 변화를 확인했습니다. 폴리프로필렌 포장 필름의 확장의 두드러진 원동력은 편리한 포장과 합리적인 적층량으로 제공되는 제품에 대한 소비자의 선호도입니다.

- 식품 가공 산업에 대한 투자 확대와 농작물 폐기물을 최소화하기 위한 노력으로 포장된 식품과 채소에 대한 수요가 증가하면서 폴리프로필렌 포장 필름에 대한 수요가 증가하고 있습니다.

- 캐나다 농업 식품부의 보고서에 따르면, 즉석면을 포함한 중국의 포장 식품 매출은 2026년까지 약 166억 6,000만 달러에 달할 것으로 예상됩니다. 이 데이터는 중국의 가공 포장 식품 시장이 지속적으로 상승세를 보이고 있음을 보여줍니다. 이러한 추세는 앞으로도 지속될 것으로 예상되며, 폴리프로필렌 포장 필름의 수요에 긍정적인 영향을 미칠 것으로 예상됩니다.

폴리프로필렌 포장 필름 산업 개요

폴리프로필렌 포장 필름 시장은 국내외 많은 기업들이 진출하여 경쟁이 치열합니다. Jindal Poly Films Ltd, CCL Industries(Innovia Films), Cosmo Films Ltd, SRF Limited, Plastchim-T 등 폴리프로필렌 포장 필름 시장의 주요 기업들은 잠재적인 혼란에 대응하고 장기적으로 지속가능한 성장을 보장하기 위해 신제품 개발 및 민첩한 비즈니스 모델 채택에 주력하고 있습니다. 에 대응하고 장기적으로 지속가능한 성장을 보장하기 위해 신제품 개발과 민첩한 비즈니스 모델 채택에 주력하고 있습니다. 몇 가지 주요 시장 발전을 발표합니다.

2024년 5월 Plastchim-T는 Manucor SpA를 인수하여 BOPP 생산량과 연질 포장에 대한 전문성을 크게 확보했습니다. 이번 인수로 연간 20만 톤의 생산능력을 갖추게 되었으며, 유럽 내 운송 및 배송 네트워크가 강화되었습니다.

2024년 3월: 플라스틱 제조업체인 인테플라스트 그룹(Inteplast Group)은 사우스 캐롤라이나 주 그레이 코트, 텍사스 주 롤리타, 테네시 주 모리스타운에 위치한 BOPP 필름 공장 3곳이 ISCC PLUS 인증을 획득했습니다. 이번 인증으로 인테플라스트는 북미에서 최초로 ISCC PLUS 인증을 획득한 BOPP 필름 제조업체 중 하나가 되었습니다.

기타 혜택

- 엑셀 형식의 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 소개

- 조사 가정과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

- 시장 개요

- 산업 밸류체인 분석

- 산업의 매력 - Porter's Five Forces 분석

- 공급 기업의 교섭력

- 소비자의 협상력

- 신규 참여업체의 위협

- 대체품의 위협

- 경쟁 기업 간의 경쟁 관계

제5장 시장 역학

- 시장 성장 촉진요인

- 비용 효율적 포장 형태에 대한 수요 상승

- 연질 포장 요건에 길을 여는 환경 규제

- 포장 식품 시장 성장

- 시장 성장 억제요인

- 원료 가격 변동

제6장 COVID-19의 시장에 대한 영향

제7장 시장 세분화

- 유형별

- BOPP

- CPP

- 용도별

- 식품

- 음료

- 의약품·의료

- 산업용

- 기타

- 지역별

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 아시아

- 중국

- 인도

- 일본

- 호주·뉴질랜드

- 라틴아메리카

- 중동 및 아프리카

- 북미

제8장 경쟁 구도

- 기업 개요

- Plastchim-T

- Jindal Poly Films Ltd

- CCL Industries(Innovia Films)

- SRF Limited

- Cosmo Films Ltd

- Amcor PLC

- UFlex Limited

- Taghleef Industries LLC

- Berry Global Inc.

- Polyplex Corporation Limited

- ProAmpac LLC

- Inteplast Group

- Toray Plastics(America) Inc.

- Profol GmbH

- Napco National

- Oben Holding Group

제9장 투자 분석

제10장 향후 동향

ksm 25.01.23The Polypropylene Packaging Films Market size in terms of shipment volume is expected to grow from 12.03 million tonnes in 2025 to 14.46 million tonnes by 2030, at a CAGR of 3.74% during the forecast period (2025-2030).

Flexible plastic packaging is one of the significant growing segments of the polypropylene packaging film market. Packaging films, which combine the best qualities of plastics to give a wide range of protective characteristics while using little material, are an added value and marketability for foodstuffs and other products not related to food.

The packaging industry continually adapts to meet the changing demands of consumers. Key drivers, such as rising disposable incomes and a burgeoning middle-class population, fuel the demand for polypropylene packaging films across various sectors, including consumer goods, food and beverages, and industrial products.

Moreover, with an increasing emphasis on sustainability, traditional rigid packaging solutions are being replaced by innovative, eco-friendly, flexible plastic packaging. This shift, combined with a growing appetite for user-friendly packaging and enhanced product protection, is set to elevate the demand for polypropylene packaging films.

Polypropylene has gained traction in the flexible packaging domain, primarily due to its higher melting point than PE, making it versatile for numerous applications. Additionally, the global shift from reusable to disposable packaging is anticipated to bolster the demand for polypropylene films.

The rising demand for films that extend product shelf life is propelling the growth of the polypropylene packaging film market. Also, the easy availability of eco-friendly packaging alternatives is broadening the applications of polypropylene films, further fueling market expansion.

In April 2024, Amcor and Kimberly Clark teamed up to launch a new packaging for their Eco Protect diapers in Peru, featuring 30% recycled materials. This hypoallergenic diaper packaging is made from plant-based fibers and includes recycled materials, promoting sustainability. Amcor took the lead in designing and producing this innovative packaging for Kimberly Clark, underscoring the commitment to a circular economy.

However, the market grapples with significant disruptions in its supply chain and manufacturing facilities, a fallout from the pandemic. Additionally, soaring raw material costs due to the energy crisis pose a potential threat to market growth.

Polypropylene Packaging Films Market Trends

BOPP Films to Witness Major Growth

- BOPP films undergo mechanical and manual stretching through a cross-direction process. These films, featuring coextruded structures, can be transparent, opaque, or metalized. The versatility and benefits of BOPP films position them as potential replacements for metal cans and cartons in the packaging industry. BOPP films are excellent alternatives to waxed paper and aluminum foil, offering higher tensile strength, lower elongation, superior gas barriers, increased stiffness, and reduced haze.

- Driven by consumer demand for practical solutions and convenient transport, BOPP films are witnessing a surge in demand. Given the stringent requirements in food packaging, BOPP films are poised for increased demand, mainly because they help preserve food's nutritional properties until consumption.

- Commonly used in the personal and household care industry, BOPP monolayer webs and laminates wrap items like soap and toothbrushes. Beyond this, the film boasts exceptional chemical resistance, a flat surface area, and UV protection. Its recyclability and non-toxic emissions have fueled its rising popularity and demand. Moreover, it offers robust barriers against water vapor, oil, and grease.

- Due to their sealing capabilities and role as an oxygen barrier, BOPP films are increasingly favored in the pharmaceutical and cosmetic industries. This trend is underscored by North America's 29% share of the global cosmetic market in 2023.

- Notably, BOPP films present a smaller environmental footprint than other plastic films. Their low melting point translates to reduced energy consumption during transformation. BOPP films easily laminate with polyethylene and maintain wide recyclability as part of the broader polyolefin chemical group.

- Key players in the polypropylene packaging films market are ramping up BOPP film production. For example, in March 2024, Toppan announced the upcoming launch of "GL-SP", an innovative eco-friendly barrier film, in India. Developed in collaboration with India's TOPPAN Speciality Films (TSF), this product is based on biaxially oriented polypropylene (BOPP).

Asia-Pacific Holds the Largest Market Share

- Convenient access to plastic materials in Asia-Pacific significantly fuels the growth of polypropylene packaging films. The region sees a rising trend in plastic packaging usage. According to a July 2024 report by the India Brand Equity Foundation, the Ministry of Commerce and Industry highlights that Western India accounts for 47% of plastic consumption, followed by Northern India at 23% and Southern India at 21%. The key industries driving this consumption include automotive, packaging, and electronic appliances. While China stands out as a pivotal market for plastic packaging, it faces challenges from legislative bans that could hinder its growth.

- Rising demand for packaged and ready-to-eat foods, coupled with the rapid expansion of e-commerce, propels the demand for polypropylene packaging films. Industries such as food and beverages, pharmaceuticals, and personal care increasingly lean toward flexible packaging solutions. The appeal of polypropylene films lies in their superior barrier qualities, durability, and visual allure, making them ideal for various packaging applications.

- The burgeoning middle class and the rise of organized retailing are significant catalysts for the growth of the flexible packaging industry. The export surge, which comes with specific global packaging requirements, has further invigorated the packaging industry. Dominating the Asia-Pacific packaging landscape, plastic flexible packaging is witnessing a shift even among traditional rigid packaging users. A notable driver for the expansion of polypropylene packaging films is the consumer preference for convenient packaging and products offered in reasonable laminate quantities.

- With growing investments in the food processing industry and initiatives to minimize agricultural crop waste, the demand for packaged food and vegetables is set to rise, subsequently boosting the need for polypropylene packaging films.

- As reported by Agriculture and Agri-Food Canada, sales of packaged foods in China, including instant noodles, are projected to reach around USD 16.66 billion by 2026. The data shows a consistent upward trend in the country's processed and packaged food market. This trend is expected to continue, positively impacting the demand for polypropylene packaging films in the coming years.

Polypropylene Packaging Films Industry Overview

The polypropylene packaging films market is competitive because of the presence of many players running their businesses within national and international boundaries. The market is fragmented. The major companies in the polypropylene packaging films market, such as Jindal Poly Films Ltd, CCL Industries (Innovia Films), Cosmo Films Ltd, SRF Limited, and Plastchim-T, are focusing on developing new products and adopting agile business models to address potential disruptions and ensure sustained long-term growth. Some of the key developments in the market are:

May 2024: Plastchim-T acquired Manucor SpA, gaining significant BOPP volume and expertise in flexible packaging. This acquisition boosts the production capacity to 200,000 tons annually and strengthens Europe's transportation and delivery network.

March 2024: Inteplast Group, a plastics manufacturer, secured ISCC PLUS verification for its three BOPP film facilities located in Gray Court, South Carolina; Lolita, Texas; and Morristown, Tennessee. This certification positions Inteplast as one of the first North American BOPP film producers to achieve ISCC PLUS recognition.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rising Demand of Cost-effective Packaging Formats

- 5.1.2 Environmental Regulation Paving Way for Flexible Packaging Requirements

- 5.1.3 Growth in Packaged Food Markets

- 5.2 Market Restraints

- 5.2.1 Fluctuation in Raw Material Prices

6 IMPACT OF COVID-19 ON THE MARKET

7 MARKET SEGMENTATION

- 7.1 By Type

- 7.1.1 BOPP

- 7.1.2 CPP

- 7.2 By Application

- 7.2.1 Food

- 7.2.2 Beverage

- 7.2.3 Pharmaceutical and Healthcare

- 7.2.4 Industrial

- 7.2.5 Other Applications

- 7.3 By Geography

- 7.3.1 North America

- 7.3.1.1 United States

- 7.3.1.2 Canada

- 7.3.2 Europe

- 7.3.2.1 United Kingdom

- 7.3.2.2 Germany

- 7.3.2.3 France

- 7.3.3 Asia

- 7.3.3.1 China

- 7.3.3.2 India

- 7.3.3.3 Japan

- 7.3.4 Australia and New Zealand

- 7.3.5 Latin America

- 7.3.6 Middle East and Africa

- 7.3.1 North America

8 COMPETITIVE LANDSCAPE

- 8.1 Company Profiles

- 8.1.1 Plastchim-T

- 8.1.2 Jindal Poly Films Ltd

- 8.1.3 CCL Industries ( Innovia Films)

- 8.1.4 SRF Limited

- 8.1.5 Cosmo Films Ltd

- 8.1.6 Amcor PLC

- 8.1.7 UFlex Limited

- 8.1.8 Taghleef Industries LLC

- 8.1.9 Berry Global Inc.

- 8.1.10 Polyplex Corporation Limited

- 8.1.11 ProAmpac LLC

- 8.1.12 Inteplast Group

- 8.1.13 Toray Plastics (America) Inc.

- 8.1.14 Profol GmbH

- 8.1.15 Napco National

- 8.1.16 Oben Holding Group