|

시장보고서

상품코드

1630438

북미의 항공 연료 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)North America Aviation Fuel - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

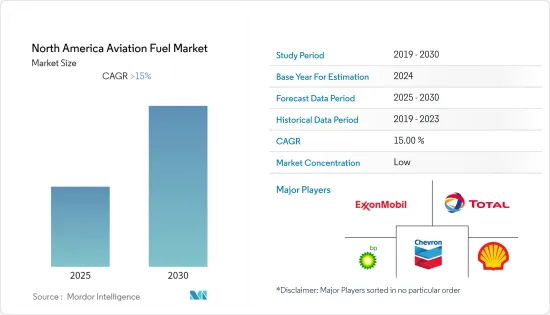

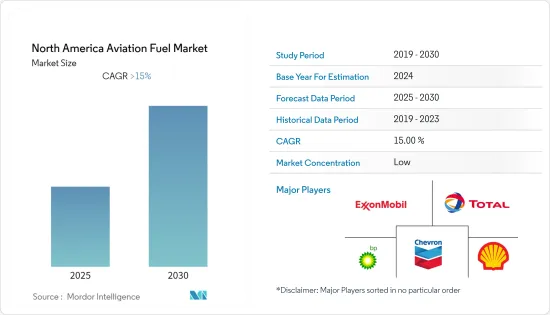

북미의 항공 연료 시장은 예측 기간 동안 15% 이상의 CAGR을 기록할 것으로 예상됩니다.

COVID-19의 발생으로 인해 지역 폐쇄와 비행 제한이 발생하여 시장에 부정적인 영향을 미쳤습니다. 현재 시장은 전염병 이전 수준에 도달했습니다.

주요 하이라이트

- 최근 몇 년 동안 항공 운임의 저평가, 경제 상황의 개선, 가처분 소득의 증가 등을 배경으로 한 항공 승객 수의 증가가 시장의 주요 촉진요인으로 작용하고 있습니다.

- 그러나 항공유 가격의 급등과 변동이 시장을 억제할 것으로 예상됩니다.

- 항공 여객 수는 2037년까지 82억 명에 달할 것으로 예상됩니다. 이 중 북미가 큰 비중을 차지할 것으로 예상되며, 시장 관계자들에게 충분한 기회를 제공하고 있습니다.

- 북미에서는 미국이 시장을 주도하고 있습니다. 예상되는 성장으로 인해 미국은 그 우위를 계속 유지할 가능성이 높습니다.

북미의 항공 연료 시장 동향

민간 부문이 시장을 독식

- 민간 항공은 정기 및 부정기 항공기 운항을 포함하며, 여객 또는 화물의 상업적 항공 운송에 관여합니다. 민간 부문은 항공 연료의 가장 큰 소비자 중 하나이며, 항공사의 총 운항 지출의 4분의 1을 차지합니다.

- 2021년 북미 시장 점유율은 민간 부문이 대부분을 차지할 것으로 예상되며, 일반 항공 부문과 방산 부문이 각각 그 뒤를 이을 것으로 예상됩니다.

- 2021년 현재 항공 연료는 민간 항공사의 총 비용의 20% 이상을 차지합니다. 따라서 민간 항공 항공편의 승객 수가 증가함에 따라 항공 연료에 대한 수요가 증가하여 예측 기간 동안 조사 된 시장을 주도 할 것으로 예상됩니다.

- 2021년 민간 항공사가 수송한 총 여객 수는 약 45억 4,000만 명으로 2020년 대비 5.58% 증가했습니다.

- 2021년 12월, Aemetis는 Delta Air Lines와 21억 달러 규모의 지속가능한 항공 연료 공급 계약을 체결하여 10년간 약 2억 5,000만 갤런을 공급합니다. 미국 외에도 Aemetis는 샌프란시스코 공항에 2억 8,000만 갤런을 공급하기 위한 양해각서를 체결한 바 있습니다.

- 따라서 앞서 언급한 요인으로 인해 예측 기간 동안 상업 부문이 시장을 독점할 것으로 예상됩니다.

시장을 독점하고 있는 미국

- 국방 부문은 대량의 항공 연료를 소비합니다. 예를 들어, 미 공군은 연간 평균 약 48억 갤런의 항공 연료를 소비하는데, 이는 공군 전체 에너지 예산의 약 81%에 해당합니다. 그 중 거의 절반은 공군에, 약 1/3은 해군에 사용됩니다. 따라서 국방부 예산이 증가함에 따라 공군의 보유 기체도 증가하여 항공 연료 시장에 긍정적인 영향을 미칠 것으로 예상됩니다.

- 미 공군은 국내 연료 수요의 절반을 대체 연료로 충당하는 것을 목표로 삼고 있으며, 그 일환으로 군과 민간 항공사는 A-10 지상 공격기에서 알코올 제트(ATJ) 연료를 테스트했습니다. 또한 Honeywell과 같은 회사는 미국 해군과 공군을 위해이 재생 가능한 제트 연료 공정 기술을 사용하고 있습니다.

- 일반 항공기는 2인승 훈련기 및 실용 헬리콥터부터 대륙간 비즈니스 제트기까지 2021년 현재 전 세계에서 운항 중인 총 440,000대의 일반 항공기(GAMA)를 포함하며, 21만 1,000대 이상의 일반 항공기가 미국을 기반으로 하고 있습니다. 독점하고 있습니다.

- Airlines for America(A4A)에 따르면 2021년 미국 항공사는 매일 290만 명의 승객을 전 세계로 운송했으며 이는 미국 항공 역사상 가장 많은 승객을 수송 한 기록입니다.

- 또한 2021년 중국 항공사가 운송한 화물은 하루 58,000톤(A4A)에 달했습니다. 따라서 항공 여객과 화물 물동량의 견조한 성장으로 지난 몇 년 동안 항공 연료에 대한 수요가 증가했습니다.

- Aemetis Inc.는 2022년 3월 콴타스항공(Qantas Airways Limited)과 2025년부터 2,000만 리터의 혼합 항공 연료를 공급하기로 계약했다고 발표했습니다. 이 혼합 연료는 캘리포니아 시설에서 생산되며, 주로 양국 간 운항하는 보잉 및 에어버스 항공기의 연료로 사용될 예정입니다.

- 따라서 앞서 언급한 요인으로 인해 예측 기간 동안 미국이 시장을 독점할 것으로 예상됩니다.

북미의 항공 연료 산업 개요

북미의 항공 연료 시장은 상당히 세분화되어 있습니다. 주요 기업으로는 Exxon Mobil Corporation, BP PLC, Shell PLC, TotalEnergies SE, Chevron Corporation 등이 있습니다.

기타 혜택

- 엑셀 형식의 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 소개

- 조사 범위

- 시장 정의

- 조사 가정

제2장 조사 방법

제3장 주요 요약

제4장 시장 개요

- 소개

- 2028년까지 시장 규모와 수요 예측(단위 : 10억 달러)

- 최근 동향과 개발

- 정부 규제와 시책

- 시장 역학

- 성장 촉진요인

- 성장 억제요인

- 공급망 분석

- Porter's Five Forces 분석

- 공급 기업의 교섭력

- 소비자의 협상력

- 신규 참여업체의 위협

- 대체품의 위협

- 경쟁 기업 간의 경쟁 강도

제5장 시장 세분화

- 연료 유형

- 에어 터빈 연료(ATF)

- 항공 바이오연료

- 항공 가스

- 용도

- 상업용

- 방위

- 일반 항공

- 지역

- 미국

- 캐나다

- 기타 북미

제6장 경쟁 구도

- M&A, 합작투자, 제휴, 협정

- 주요 기업의 전략

- 기업 개요

- BP PLC

- Shell PLC

- TotalEnergies SE

- Pan American Energy S.L.

- Exxon Mobil Corporation

- Allied Aviation Services Inc

- Chevron Corporation

- Honeywell International Inc

- Valero Marketing and Supply

제7장 시장 기회와 향후 동향

ksm 25.01.23The North America Aviation Fuel Market is expected to register a CAGR of greater than 15% during the forecast period.

The market was negatively impacted by the outbreak of COVID-19 due to regional lockdowns and flight restrictions. Currently, the market has reached pre-pandemic levels.

Key Highlights

- The increasing number of air passengers, on account of the cheaper airfare in recent times, stronger economic conditions, and increasing disposable income, are among the major driving factors for the market.

- However, the high and volatile cost of aviation fuel is expected to restrain the market.

- The air passenger number is expected to touch 8.2 billion by 2037. North America is expected to hold a significant share in this, creating ample opportunities for market players.

- The United States is leading the market in the North American region. With forecast growth, the United States is likely to continue its dominance.

North America Aviation Fuel Market Trends

Commercial Sector to Dominate the Market

- Commercial aviation includes operating scheduled and non-scheduled aircraft, which involves commercial air transportation of passengers or cargo. The commercial segment is one of the largest consumers of aviation fuel, and it accounts for a quarter of the total operating expenditure for an airline operator.

- The market share is dominated by the commercial sector in 2021 in North America, followed by general aviation and defense, respectively.

- As of 2021, aviation fuel accounted for more than 20% (IATA) of the total expenses for commercial airlines. Hence, as the number of passengers is increasing on commercial flights, the demand for aviation fuel is expected to increase, in turn driving the market studied during the forecast period.

- In 2021, the total number of passengers carried by commercial airlines rose to around 4.54 billion, which was 5.58% higher than in 2020.

- In December 2021, Aemetis signed a USD 2.1 billion sustainable aviation fuel supply agreement with Delta Air Lines to supply approximately 250 million gallons under a 10-year agreement. In addition to America, Aemetis has also signed memorandums of understanding to supply 280 million gallons for delivery to the San Francisco Airport.

- Therefore, due to the aforementioned factors, the commercial sector is expected to dominate the market during the forecast period.

The United States to Dominate the Market

- The defense sector consumes a large amount of aviation fuel. For instance, on average, the US Air Force consumes approximately 4.8 billion gallons of aviation fuel annually, about 81% of the total Air Force energy budget. Nearly half of that goes to the Air Force and around one-third to the Navy. Therefore, as the budget increases for the defense sector, the air force fleet is expected to increase, positively affecting the aviation fuel market.

- As part of the United States Air Force's goal of achieving half of its domestic fuel needs drawn from alternative sources, the military and commercial airlines tested alcohol-to-jet (ATJ) fuel on A-10 ground attack aircraft. Moreover, companies such as Honeywell use this renewable jet fuel process technology for the US Navy and Air Force.

- General Aviation included a total of 440,000 general aircraft flying worldwide (GAMA) as of 2021, ranging from two-seat training aircraft and utility helicopters to intercontinental business jets. Over 211,000 general planes are based in the United States, which makes the nation dominate the sector.

- According to the Airlines for America (A4A), in 2021, the country's airlines carried 2.9 million passengers worldwide daily, which was an all-time high number of passengers in the country's airline history.

- Moreover, 58,000 metric tons of cargo per day were ferried by the country's airlines in 2021 (A4A). Therefore, the country's robust growth in air travel and cargo volumes has resulted in higher demand for aviation fuel in past years.

- In March 2022, Aemetis Inc announced that it had made an agreement with Qantas Airways Limited to supply 20 million liters of blended aviation fuel from 2025. The blended fuel will be produced at a facility in California and will primarily be used to power Boeing and Airbus planes being operated between the countries.

- Therefore, due to the aforementioned factors, the United States is expected to dominate the market during the forecast period.

North America Aviation Fuel Industry Overview

The North American aviation fuel market is moderately fragmented. Some of the major companies (in no particular order) include Exxon Mobil Corporation, BP PLC, Shell PLC, TotalEnergies SE, Chevron Corporation, and others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD billion, till 2028

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.2 Restraints

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Fuel Type

- 5.1.1 Air Turbine Fuel (ATF)

- 5.1.2 Aviation Biofuel

- 5.1.3 AVGAS

- 5.2 Application

- 5.2.1 Commercial

- 5.2.2 Defense

- 5.2.3 General Aviation

- 5.3 Geography

- 5.3.1 The United States

- 5.3.2 Canada

- 5.3.3 Rest of North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 BP PLC

- 6.3.2 Shell PLC

- 6.3.3 TotalEnergies SE

- 6.3.4 Pan American Energy S.L.

- 6.3.5 Exxon Mobil Corporation

- 6.3.6 Allied Aviation Services Inc

- 6.3.7 Chevron Corporation

- 6.3.8 Honeywell International Inc

- 6.3.9 Valero Marketing and Supply