|

시장보고서

상품코드

1630439

유럽의 항공 연료 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Europe Aviation Fuel - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

■ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송일정은 문의해 주시기 바랍니다.

가격

※ 부가세 별도

한글목차

영문목차

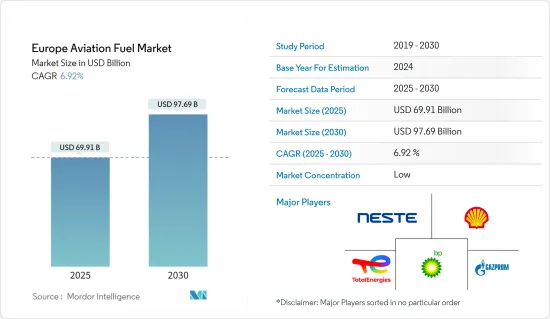

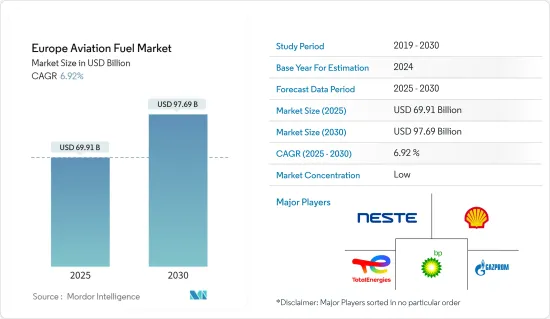

유럽의 항공 연료 시장 규모는 2025년 699억 1,000만 달러로 추정되며, 예측 기간(2025-2030년) 동안 6.92%의 CAGR로 2030년에는 976억 9,000만 달러에 달할 것으로 예상됩니다.

주요 하이라이트

- 중기적으로 몇 가지 요인이 유럽의 제트연료 수요를 견인하고 있습니다. 최근 항공 운임 인하와 항공 노선 확대로 인한 항공 승객 증가 등이 그것입니다.

- 그러나 전기 항공기와 하이브리드 항공기의 도입이 진행되고 있다는 점이 이 시장의 성장에 도전이 되고 있습니다.

- 이러한 어려움에도 불구하고, 유럽위원회는 온실가스 배출을 억제하기 위해 지속가능한 항공 연료(SAF) 의무화 확대를 추진하고 있습니다. 이러한 노력은 항공 연료 시장에 큰 비즈니스 기회를 창출할 수 있습니다.

- 유럽은 영국을 필두로 가장 큰 항공 연료 시장 규모를 자랑합니다. 현재의 주도권을 감안할 때, 영국은 앞으로도 그 우위를 유지할 것으로 보입니다.

유럽의 항공 연료 시장 동향

민간 부문이 시장을 독식

- 민간항공은 정기편과 부정기편 항공기 운항을 포함하며, 여객 또는 화물의 상업용 항공 운송을 포함합니다. 민간 부문은 항공 연료의 최대 소비자 중 하나이며, 항공사의 총 운항 지출의 4분의 1을 차지합니다.

- 2023년에는 민간 항공이 하늘을 지배하여 전체 항공편의 91.9%를 차지하여 유럽 항공 여행에서 중요한 역할을 반영할 것입니다. 일반 항공은 6.5%를 차지하며 틈새 시장과 개인 여행의 수요를 충족시킵니다. 국방 항공은 전체 항공편의 1.6%를 차지하며 미미하지만 여전히 중요한 역할을 하고 있습니다.

- 유럽의 민간 항공 연료 시장은 항공 여행의 부활과 지속가능한 항공 솔루션에 대한 관심에 힘입어 강력한 성장세를 보이고 있습니다. 스페인, 영국, 프랑스 등 유럽 주요 국가에서는 관광 붐이 일어나고 있으며, 상업 부문은 승객 수 증가에 힘입어 성장세를 보이고 있습니다.

- COVID-19 이후 세계 여행과 관광은 저렴한 항공료와 경제 상황의 개선으로 회복되어 항공 수요가 급증하고 있습니다. 이러한 항공 수요 증가는 결국 민간 항공 부문의 연료 소비를 증가시켰습니다.

- Eurostat의 데이터에 따르면 2024년 1분기에 EU 항공사가 수송 한 승객 수는 1억 9,800만 명으로 2023년 1분기 대비 11.5% 증가했으며, 2024년 2 월은 특히 두드러졌으며, 승객 수는 전염병 이후 처음으로 2019년 2월 수치를 넘어 1.0% 증가하여 2024년 2월에 1.0% 증가했습니다. 2024년 1분기 EU 역외 국제선 여객은 EU 역내 전체 여객의 50.1%를 차지했습니다. 전국적으로 관광객이 급증함에 따라 이 지역의 항공 연료 수요는 향후 몇 년 동안 크게 증가할 것으로 예상됩니다.

- 또한, 특히 이탈리아와 스페인과 같은 핫스팟에서 유럽 관광객의 증가는 연료 수요의 지속적인 성장 궤도를 시사하고 있습니다. 항공 부문이 회복되고 새로운 비행 노선이 등장하면 이러한 성장은 가속화될 것으로 보입니다.

- 2024년 9월, 델타항공은 유럽 7개 노선을 추가하여 2025년 여름 대서양 횡단 스케줄을 확대한다고 발표했습니다. 이번 확장에는 보스턴-바르셀로나, 디트로이트-더블린, 애틀랜타-브뤼셀 노선에 더해 이탈리아로 향하는 4개의 신규 노선이 포함됩니다. 이러한 관광 및 항공 네트워크 확대에 따라 항공 연료 수요도 증가할 것으로 예상됩니다.

- 따라서, 위의 점으로 미루어 볼 때, 민간 부문이 시장을 독점할 것으로 예상됩니다.

시장을 독점하고 있는 영국

- 영국의 항공 부문은 경제의 핵심이며 유럽에서 가장 큰 규모를 자랑합니다. 공항 인프라에 대한 막대한 투자와 강력한 관광 산업이 영국 항공 시장을 뒷받침하고 있으며, 이는 영국 항공 시장의 견조한 실적에 기여하고 있습니다.

- 2023년 영국은 하루 평균 5290편으로 가장 많은 항공편을 운항하며 2022년 대비 13% 증가했습니다. 스페인은 9% 증가한 4616편으로 두 번째로 많았고, 독일은 7% 증가한 4532편으로 그 뒤를 이었습니다. 이 때문에 영국의 항공 연료 수요는 유럽 항공 연료 시장의 성장을 주도하고 있습니다.

- 이 나라의 항공 연료 시장은 주로 관광객 증가, 세계 지정학적 상황, 국내 항공 운송량, 주로 정부 정책에 따라 예측 기간 동안 크게 성장할 것으로 예상됩니다.

- 예를 들어, 영국 정부는 2024년 4월, 2030년까지 모든 제트 연료의 10%를 지속가능한 자원에서 조달해야 한다고 발표했습니다. 이 조치는 온실가스 배출을 줄이고 지속가능한 항공 연료(SAF) 산업을 촉진하기 위한 것으로, 18억 파운드 이상의 경제 효과를 가져오고 1만 개 이상의 일자리를 창출할 수 있습니다.

- 또한 영국 정부는 첨단 연료 기금을 통해 1억 3,500 만 파운드를 할당하여 전국적으로 13 개의 획기적인 SAF 프로젝트를 지원했습니다. 이 기금은 지속가능한 항공 연료의 개발 및 생산을 가속화하는 것을 목표로 합니다.

- 따라서 위의 요인으로 인해 예측 기간 동안 항공 연료 부문에서 영국이 시장을 독점 할 것으로 예상됩니다.

유럽의 항공 연료 산업 개요

유럽의 항공 연료 시장은 반분할되어 있습니다. 주요 기업으로는 PJSC Gazprom, BP PLC, Shell PLC, TotalEnergies SE, Neste Oyj 등이 있습니다.

기타 혜택

- 엑셀 형식의 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

목차

제1장 소개

- 조사 범위

- 시장 정의

- 조사 가정

제2장 조사 방법

제3장 주요 요약

제4장 시장 개요

- 소개

- 2029년까지 시장 규모와 수요 예측(단위 : 10억 달러)

- 최근 동향과 개발

- 정부 규제와 시책

- 시장 역학

- 성장 촉진요인

- 항공 여객 운송량 증가

- 지속가능한 항공 연료(SAF) 의무화

- 성장 억제요인

- 연료 비용 급등

- 성장 촉진요인

- 공급망 분석

- Porter's Five Forces 분석

- 공급 기업의 교섭력

- 소비자의 협상력

- 신규 참여업체의 위협

- 대체품의 위협

- 경쟁 기업 간의 경쟁 강도

- 투자 분석

제5장 시장 세분화

- 연료 유형

- 에어 터빈 연료(ATF)

- 항공 바이오연료

- 항공 가스

- 용도

- 상업용

- 방위

- 일반 항공

- 지역

- 영국

- 독일

- 이탈리아

- 프랑스

- 스페인

- 북유럽

- 터키

- 러시아

- 기타 유럽

제6장 경쟁 구도

- M&A, 합작투자, 제휴, 협정

- 주요 기업의 전략

- 기업 개요

- Repsol SA

- BP PLC

- Royal Dutch Shell PLC

- Total SA

- Exxon Mobil Corporation

- Gazprom Neft PJSC

- Neste Oyj

- 기타 주요 국가 리스트

- 시장 순위 분석

제7장 시장 기회와 향후 동향

- 온실가스 배출량 절감을 위한 지속가능한 항공 연료(SAF) 이용 확대를 목표로 한다

The Europe Aviation Fuel Market size is estimated at USD 69.91 billion in 2025, and is expected to reach USD 97.69 billion by 2030, at a CAGR of 6.92% during the forecast period (2025-2030).

Key Highlights

- In the medium term, several factors are driving the demand for jet fuel in Europe. These include a rise in air passengers due to recent reductions in airfare and the expansion of flight routes.

- However, the growing adoption of electric and hybrid aircraft poses a challenge to this market growth.

- Despite these challenges, the European Commission is pushing for increased mandates on sustainable aviation fuel (SAF) to curb greenhouse gas emissions. Such initiatives are poised to unlock substantial opportunities in the aviation fuel market.

- Europe boasts the largest market size for aviation fuel, with the United Kingdom at the forefront. Given its current leadership, the UK is set to maintain its dominance in the coming years.

Europe Aviation Fuel Market Trends

Commercial Sector to Dominate the Market

- Commercial aviation includes operating scheduled and non-scheduled aircraft, which involves commercial air transportation of passengers or cargo. The commercial segment is one of the largest consumers of aviation fuel, accounting for a quarter of an airline operator's total operating expenditure.

- In 2023, commercial aviation dominated the skies, accounting for 91.9 percent of total flights, reflecting its critical role in European air travel. General aviation contributed 6.5 percent, serving niche markets and private travel needs. While minor, defense aviation still played a vital role, with 1.6 percent of total flights.

- The European commercial aviation fuel market is witnessing robust growth, fueled by a resurgence in air travel and a strong emphasis on sustainable aviation solutions. Major European countries, including Spain, the United Kingdom, and France, are witnessing a tourism boom, leading the commercial sector to capitalize on rising passenger numbers.

- Post-COVID-19, global travel and tourism have rebounded, driven by affordable airfares and improved economic conditions, leading to a surge in air travel demand. This uptick in flight demand has, in turn, increased fuel consumption in the commercial aviation sector.

- Eurostat Data highlights that in Q1 2024, EU air carriers transported 198 million passengers, an 11.5% increase from Q1 2023. February 2024 was particularly notable, with passenger numbers exceeding February 2019 figures for the first time since the pandemic, marking a 1.0% uptick. In Q1 2024, international extra-EU transport made up 50.1% of all passengers within the EU. Given the nationwide tourism surge, the region's aviation fuel demand is poised for significant growth in the coming years.

- Moreover, Europe's tourism upswing, especially in hotspots like Italy and Spain, signals a sustained growth trajectory for fuel demand. As the aviation sector rebounds and new flight routes emerge, this growth is set to accelerate.

- In September 2024, Delta Air Lines announced the addition of seven new European routes, expanding its transatlantic schedule for summer 2025. This expansion includes four new services to Italy, alongside routes from Boston to Barcelona, Detroit to Dublin, and Atlanta to Brussels. With such an expansion in tourism and aviation networks, the demand for aviation fuels is anticipated to rise.

- Therefore, based on the above mentioned points, the commercial sector is expected to dominate the market.

The United Kingdom to Dominate the Market

- The United Kingdom's aviation sector is a cornerstone of its economy, ranking among the largest in Europe. Substantial investments in airport infrastructure and a strong tourism industry support the aviation market in the United Kingdom, contributing to its robust performance.

- In 2023, the United Kingdom had the highest average number of daily flights, at 5290, a 13 percent increase from 2022. Spain was the second busiest, with 4616 flights per day, up 9 percent, followed by Germany, with 4532 flights per day, up 7 percent. Due to this, the demand for aviation fuel in the UK is substantial, driving growth in the European aviation fuel market.

- The country's aviation fuel market is expected to grow significantly during the forecast period, mainly driven by increasing tourism, global geopolitical conditions, domestic air traffic, and mainly by government policies.

- For instance, in April 2024, the United Kingdom government announced that by 2030, 10 percent of all jet fuel must come from sustainable sources. This move aims to cut greenhouse gas emissions and boost the sustainable aviation fuel (SAF) industry, potentially adding over 1.8 billion British Pounds to the economy and creating more than 10,000 jobs.

- Furthermore, the United Kingdom government allocated 135 million British Pounds through the Advanced Fuels Fund to support 13 groundbreaking SAF projects nationwide. This funding aims to accelerate the development and production of sustainable aviation fuels.

- Therefore, due to the factors above, the United Kingdom is expected to dominate the market in the aviation fuel sector during the forecast period.

Europe Aviation Fuel Industry Overview

The Europe aviation fuel market is semi-fragmented. Some of the major companies (in no particular order)include PJSC Gazprom, BP PLC, Shell PLC, TotalEnergies SE, Neste Oyj, and others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD billion, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Rising Air Passenger Traffic

- 4.5.1.2 Sustainable Aviation Fuel (SAF) Mandates

- 4.5.2 Restraints

- 4.5.2.1 High Volatile Fuel Costs

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products and Services

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Fuel Type

- 5.1.1 Air Turbine Fuel (ATF)

- 5.1.2 Aviation Biofuel

- 5.1.3 Avgas

- 5.2 Application

- 5.2.1 Commercial

- 5.2.2 Defense

- 5.2.3 General Aviation

- 5.3 Geography

- 5.3.1 United Kingdom

- 5.3.2 Germany

- 5.3.3 Italy

- 5.3.4 France

- 5.3.5 Spain

- 5.3.6 Nordic

- 5.3.7 Turkey

- 5.3.8 Russia

- 5.3.9 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Repsol SA

- 6.3.2 BP PLC

- 6.3.3 Royal Dutch Shell PLC

- 6.3.4 Total SA

- 6.3.5 Exxon Mobil Corporation

- 6.3.6 Gazprom Neft PJSC

- 6.3.7 Neste Oyj

- 6.4 List of Other Prominent Countries

- 6.5 Market Ranking Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Aim to increase sustainable aviation fuel (SAF) use to reduce greenhouse gas emissions