|

시장보고서

상품코드

1940712

유럽의 코워킹 스페이스 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Europe Coworking Spaces - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

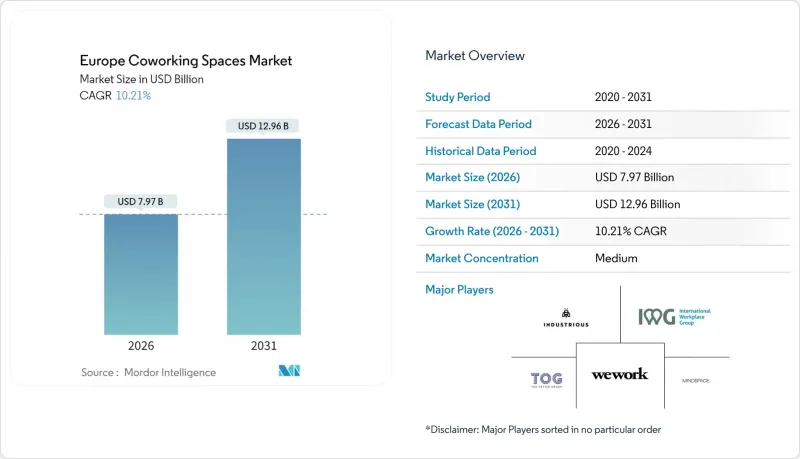

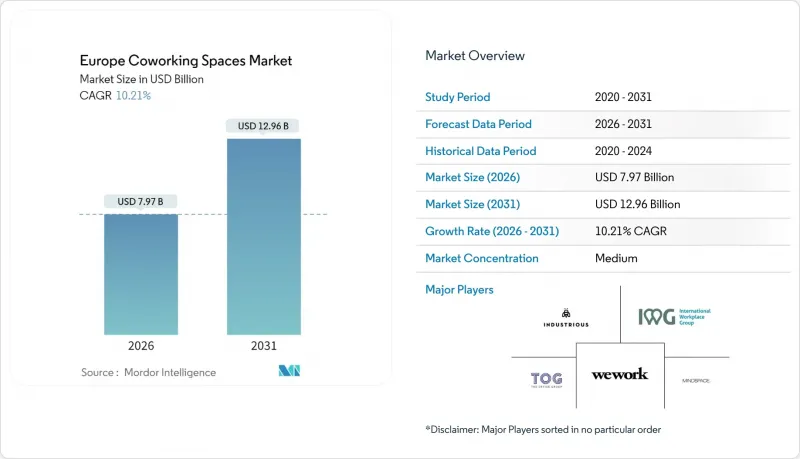

유럽의 코워킹 스페이스 시장은 2025년에 72억 3,000만 달러로 평가되었으며, 2026년 79억 7,000만 달러에서 2031년까지 129억 6,000만 달러에 달할 것으로 예측됩니다.

예측 기간(2026-2031년) 동안 CAGR은 10.21%로 예상됩니다.

하이브리드 업무로의 구조적 전환, 기업 부동산 포트폴리오 최적화에 대한 압력 증가, 초기 비용 절감에 대한 지자체 인센티브 등이 유연한 업무공간 솔루션에 대한 지속적인 수요를 견인하고 있습니다. 기업은 자본 보존을 위해 자산 경량형 관리 계약을 채택하는 반면, 중간 규모의 시설은 사업자가 이용률과 서비스 품질의 균형을 맞추기 위해 필요한 밀도를 제공합니다. 대기업 고객들이 전용 협업존을 갖춘 전체 층을 제공하고자 하는 가운데, 대규모 사이트가 가장 빠르게 성장하고 있습니다. 또한, AI가 탑재된 가동률 플랫폼은 동적 가격 책정을 지원하는 실시간 점유율 데이터를 제공함으로써 운영 사업자의 수익률 향상에 기여하고 있습니다. 한편, 주요 도시의 잉여 그레이리스 재고와 노후화된 오피스 재고에 대한 ESG 리노베이션 비용 상승은 단기적으로 가격 결정력을 억제하고 있습니다. 기술적 차별화와 복합용도 입지 전략을 결합한 운영자는 유럽 코워킹 스페이스 시장의 다음 성장 단계를 포착할 수 있는 좋은 위치에 있습니다.

유럽 코워킹 스페이스 시장 동향과 인사이트

유연한 공간을 통한 기업 부동산 포트폴리오 최적화

상업용 부채 시장에서 재융자 리스크가 다시 부각되면서 기업들은 유연한 공간으로의 전환을 가속화했습니다. 현재 자산 경량형 거래가 주류를 이루고 있습니다: IWG가 2024년까지 개설한 624개 지점 중 95%가 관리형 파트너십으로 구축되어 기업 임차인에게 턴키 오피스 환경을 제공하면서 설비투자를 집주인에게 전가하는 방식으로 운영되고 있습니다. 다국적 기업들은 고정 임대 계약 수를 줄이면서 인력을 재배치하는 네트워크형 부동산 전략의 일환으로 플렉서블 허브를 활용하고 있습니다. 이를 통해 부동산 담당자는 직원 1인당 법정 면적 기준을 준수하면서 좌석 밀도 20% 감소 목표를 달성할 수 있습니다. 공간 예약 API는 기업의 인사 시스템과 연동하여 직원들이 사무실 근무일에 프로젝트 팀 근처의 책상을 예약할 수 있도록 합니다. 이를 통해 기업은 2019년 기준치 대비 직원 1인당 바닥 면적을 35% 줄일 수 있습니다. 이러한 경향은 런던과 뮌헨에서 가장 두드러지게 나타나고 있으며, 금융기관의 추정에 따르면 2025년부터 2027년까지 발생하는 929억 달러의 부채 자금 조달 격차 중 44%를 오피스 관련 분야가 차지할 것으로 예상됩니다. 유연한 공간은 어려운 노동 시장에서 중요한 인재 유치 지표를 유지하면서 임대 부채를 줄일 수 있습니다.

EU 노동법의 하이브리드 근무 정책 가속화

재택근무 권리에 관한 EU 차원의 지침이 2024년부터 2025년까지 각국 법에 반영되어 원격근무 스케줄 설정과 인체공학적으로 안전한 위성 사무실 이용권이 법적으로 명문화되었습니다. 고용주는 통근권 내에 '적절한 시설'을 제공하거나 코워킹 스페이스 이용료를 보전하는 수당을 지급할 의무가 생겼습니다. 이 의무로 인해 건물 인증 추적 체계가 갖추어지지 않은 기업에 컴플라이언스 비용이 전가되고, 조달 부문은 작업환경 일체를 전문 사업자에게 아웃소싱하는 움직임이 가속화되고 있습니다. 그 결과, 2025년에는 직원들이 매일 근무지를 선택할 수 있는 멀티 사이트 패스(구독 모델)의 기업용 계약 건수가 전년 대비 32% 증가했습니다. 이에 운영사는 ISO 45001 보건안전 기준을 충족하도록 기존 시설을 개조하고, 노동 감사에 대응할 수 있는 방음시설과 공기질 센서를 설치했습니다. 하이브리드 근무 정책은 팀 단위의 작업 공간과 회의 중심의 플로어 레이아웃과 같은 설계 변경을 촉진하고, 기업들은 밀도 제한을 준수하면서 협업에 집중할 수 있는 '앵커 데이'를 조정할 수 있습니다.

노후화된 오피스 재고의 ESG 리노베이션 비용 상승

유럽의 2030 에너지 성능 규정에 따라 상업용 바닥 면적은 EPC B 또는 이와 동등한 기준을 달성해야 하며, 노후 자산에 대한 자본 지출이 급증하고 있습니다. 1970년대 건축물의 평균 개보수 비용은 전기식 공조설비, LED 조명, 외벽 단열재 등을 포함하면 평방피트당 190달러가 넘습니다. 임대계약이 아닌 관리계약을 체결하는 코워킹 사업자는 직접적인 설비투자를 피할 수 있지만, 임대인으로부터 전가되는 서비스 이용료의 증가는 여전히 직면하게 됩니다. 규제산업 임차인들은 다년 계약 체결 전에 BREEAM 'Very Good' 또는 LEED 'Gold' 인증을 요구하는 경향이 강해지고 있으며, 비준수 공간은 사실상 임대할 수 없게 되었습니다. 2차 시장에서는 변동금리 벤치마크에 기반한 은행부채에 의존하는 자본구조로 인해 자금조달의 문턱이 높아지고 있습니다. 리노베이션 일정을 예측하고 친환경 인증의 설비투자 분담 조항을 협상하는 사업자는 비용 우위를 확보할 수 있지만, 대응이 늦어지는 사업자는 자산의 노후화 위험에 직면하여 유럽 코워킹 스페이스 시장에서의 네트워크 확장이 정체될 수 있습니다.

부문 분석

2025년 기준, 중규모 시설(20,000-40,000평방피트)이 유럽 코워킹 스페이스 시장의 52.80%를 차지했습니다. 이는 300-500 데스크 규모의 네트워크를 유지하면서도 커뮤니티 참여를 저해하지 않는 능력을 반영합니다. 운영사는 모듈식 파티션을 활용하여 48시간 이내에 레이아웃을 변경함으로써 변화하는 기업 니즈에 대응하고 있습니다. 대규모 시설은 기업들이 층 전체를 임대하여 방송 스튜디오, 5G 지원 몰입형 룸 등 프리미엄 시설을 찾는 추세로 인해 2031년까지 CAGR 11.74%로 확대될 것으로 예상됩니다. 운영사는 행사 개최일에 좌석 밀도를 18% 향상시키는 AI 기반 공간 활용 툴을 도입하여 대규모 시설의 고정비 증가를 상쇄하고, 수익의 계절적 변동성을 완화하고 있습니다. 소규모 시설은 통근권에서 번창하고 허브 앤 스포크 모델에서 스포크 역할을 하며, 회원들이 집에서 20분 이내에 좌석을 확보할 수 있도록 보장합니다.

관리 계약의 급증(2024년 전체 IWG 신규 오픈의 95%)은 임대인이 현금흐름을 안정화시키면서 대출 계약상의 가동률 요건을 충족하는 파트너십 모델을 선호한다는 것을 보여줍니다. 대규모 시설의 경우, 기업용 스위트룸이 전체 임대면적의 42%(2년 전 26%)를 차지해 프리랜서 중심에서 기업 지향적인 레이아웃으로 전환되고 있음을 알 수 있습니다. 계약 기간 지표도 이러한 변화를 반영하여 2023년부터 2025년까지 기업용 계약의 평균 기간이 9개월에서 14개월로 연장되었습니다. 이러한 추세는 유럽 코워킹 스페이스 시장의 성장을 가속화하는 데 있어 중대형 시설의 핵심적인 역할을 확고히 하고 있습니다.

기타 특전:

- 엑셀 형식의 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 소개

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측(금액, 단위 : 10억 달러)

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KSM 26.03.10The Europe Co-Working Spaces Market was valued at USD 7.23 billion in 2025 and estimated to grow from USD 7.97 billion in 2026 to reach USD 12.96 billion by 2031, at a CAGR of 10.21% during the forecast period (2026-2031).

Structural shifts toward hybrid work, mounting pressure to optimize corporate real-estate portfolios, and municipal incentives that lower set-up costs are driving sustained demand for flexible workspace solutions. Corporations are embracing asset-light managed agreements to conserve capital, while medium facilities provide the density operators need to balance utilization and service quality. Large sites are scaling fastest as enterprise clients ask for entire floors equipped with private collaboration zones, and AI-enabled utilization platforms are boosting operator margins by providing real-time occupancy data that supports dynamic pricing. At the same time, surplus grey-lease inventory in Tier-1 cities and rising ESG retrofitting costs on aging office stock temper near-term pricing power. Operators that combine technology differentiation with mixed-use location strategies are positioned to capitalize on the next growth phase of the Europe co-working spaces market.

Europe Coworking Spaces Market Trends and Insights

Corporate Real-Estate Portfolio Optimization via Flex Space

Enterprises accelerated their migration to flexible space once refinancing risk resurfaced in the commercial debt market. Asset-light deals now dominate: 95% of IWG's 624 openings in 2024 were structured as managed partnerships that shift cap-ex to landlords while delivering turnkey office ecosystems to corporate tenants. Multinationals treat flexible hubs as part of a networked real-estate stack that reallocates headcount across fewer fixed leases, helping real-estate directors hit 20% seat-density targets without breaching labor-code mandates on square footage per employee. Space-booking APIs integrate with company HR systems so staff reserve desks near project teams on in-office days, enabling firms to reduce square footage per employee by 35% relative to 2019 benchmarks. The most pronounced uptake is in London and Munich, where lenders estimate offices make up 44% of the USD 92.9 billion debt-funding gap due 2025-2027. Flexible space mitigates lease liabilities while sustaining talent-attraction metrics that matter in tight labor markets.

Acceleration of Hybrid Work Policies in EU Labor Codes

EU-level guidance on home-office rights filtered into national statutes during 2024-2025, codifying employee entitlements to remote scheduling and ergonomically safe satellite offices. Employers must now provide "suitable facilities" within commuting distance or grant allowances that cover co-working subscriptions. The mandate shifts compliance costs to companies ill-equipped to track building certifications, prompting procurement teams to outsource the entire workplace bundle to specialized operators. As a result, subscription models, multi-site passes that let staff choose locations daily, gained 32% more corporate seats during 2025 than the prior year. Operators respond by rehabbing legacy inventory to meet ISO 45001 health-and-safety standards, embedding acoustic dampening and air-quality sensors that satisfy labor-inspection audits. Hybrid policies also drive design changes such as team-based neighborhoods and meeting-heavy floorplates so firms can orchestrate anchor days that concentrate collaboration while respecting density caps.

Rising ESG Retrofitting Costs for Aging Office Stock

Europe's 2030 energy-performance mandate requires commercial floor space to achieve EPC B or equivalent, pushing capital expenditure on dated assets skyward. Average retrofit costs for 1970s-era buildings exceed USD 190 per square foot when factoring in electrified HVAC, LED lighting, and facade insulation. Co-working operators that hold management contracts rather than leases avoid direct cap-ex yet still confront service-charge increases passed through by landlords. Tenants from regulated industries now demand BREEAM Very Good or LEED Gold ratings before signing multi-year agreements, effectively rendering non-compliant space unlettable. Financing hurdles intensify in secondary markets where capital-stack structures rely on bank debt priced off floating-rate benchmarks. Operators that anticipate retrofit schedules and negotiate green-certification cap-ex sharing clauses secure a cost advantage, while laggards face stranded-asset risk that can stall network expansion within the Europe co-working spaces market.

Other drivers and restraints analyzed in the detailed report include:

- Booming Startup Ecosystem Seeking Cost-Efficient, Flexible Leases

- National & Municipal Incentives for Revitalizing Post-Pandemic CBDs

- Surplus Grey-Lease Inventory Depressing Desk Rates in Tier-1 Cities

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Medium facilities, 20,000 to 40,000 square feet, held 52.80% of Europe's co-working spaces market share in 2025, reflecting their ability to support 300-to-500 desk networks without diluting community engagement. Operators use modular partitions to pivot layouts within 48 hours, meeting fluctuating corporate requirements. Large facilities are projected to grow at an 11.74% CAGR through 2031 as enterprises commit to entire floors and demand premium amenities such as broadcast studios and 5G-enabled immersive rooms. Operators balance the higher fixed costs of large footprints by integrating AI-driven space-utilization tools that lift seat density by 18% on event days, smoothing revenue seasonality. Small facilities thrive in commuter belts, acting as spokes in hub-and-spoke models that guarantee members a seat within 20 minutes of home.

A surge in managed agreements, 95% of IWG openings in 2024, signals that landlords prefer partnership models that stabilize cash flows while enabling them to satisfy lender covenants on occupancy. In large facilities, corporate suites account for 42% of gross leased area versus 26% two years earlier, underscoring the shift from freelancer-centric to enterprise-oriented layouts. Duration metrics mirror this shift: the average enterprise contract length rose from nine to 14 months between 2023 and 2025. These dynamics solidify the central role of medium and large sites in accelerating the Europe co-working spaces market.

The Europe Co-Working Spaces Market Report is Segmented by Size & Scale of Facility (Small, Medium, Large), by Sector (Information Technology, BFSI, Business Consulting & Professional Service, Other Services), by End Use (Freelancers, Enterprises, Start Ups and Others), and by Geography (Germany, United Kingdom, France, Italy, Spain, Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- IWG (Regus & Spaces)

- WeWork

- The Office Group (TOG)

- Mindspace

- Industrious

- Second Home

- Tribes

- Impact Hub

- Fora Space

- Talent Garden

- Huckletree

- Betahaus

- Knotel Europe

- KAPTUR

- BounceSpace

- Mokrin House

- Paper Hub

- Mortimer House

- Sirius Facilities

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Booming startup ecosystem seeking cost-efficient, flexible leases

- 4.2.2 Corporate real-estate (CRE) portfolio optimisation via flex space

- 4.2.3 National & municipal incentives for revitalising post-pandemic CBDs

- 4.2.4 Acceleration of hybrid work policies in EU labour codes (2025+)

- 4.2.5 Venture-capital funding earmarked for "work-near-home" sub-urb hubs

- 4.2.6 AI-enabled space-utilisation platforms boosting operator margins

- 4.3 Market Restraints

- 4.3.1 Surplus grey-lease inventory depressing desk-rates in Tier-1 cities

- 4.3.2 Rising ESG retrofitting costs for ageing office stock

- 4.3.3 Interest-rate volatility constraining REIT financing windows

- 4.3.4 Municipal resistance to zoning conversion in heritage districts

- 4.4 Government Regulations and Initiatives in the Industry

- 4.5 Technological Innovations in the Co-Working Office Space Real Estate Market

- 4.6 Insights into the Key Office Real Estate Industry Metrics (Supply, Rentals, Prices, Occupancy/Vacancy (%))

- 4.7 Impact of Remote Working on Space Demand

- 4.8 Industry Attractiveness - Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers/Consumers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitute Products

- 4.8.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, In USD Billion)

- 5.1 By Size & Scale of Facility

- 5.1.1 Small

- 5.1.2 Medium

- 5.1.3 Large

- 5.2 By Sector

- 5.2.1 Information Technology (IT and ITES)

- 5.2.2 BFSI (Banking, Financial Services and Insurance)

- 5.2.3 Business Consulting & Professional Service

- 5.2.4 Other Services (Retail, Lifesciences, Energy, Legal Services)

- 5.3 By End User

- 5.3.1 Freelancers

- 5.3.2 Enterprises

- 5.3.3 Start Ups and Others

- 5.4 By Geography

- 5.4.1 Germany

- 5.4.2 United Kingdom

- 5.4.3 France

- 5.4.4 Italy

- 5.4.5 Spain

- 5.4.6 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 IWG (Regus & Spaces)

- 6.4.2 WeWork

- 6.4.3 The Office Group (TOG)

- 6.4.4 Mindspace

- 6.4.5 Industrious

- 6.4.6 Second Home

- 6.4.7 Tribes

- 6.4.8 Impact Hub

- 6.4.9 Fora Space

- 6.4.10 Talent Garden

- 6.4.11 Huckletree

- 6.4.12 Betahaus

- 6.4.13 Knotel Europe

- 6.4.14 KAPTUR

- 6.4.15 BounceSpace

- 6.4.16 Mokrin House

- 6.4.17 Paper Hub

- 6.4.18 Mortimer House

- 6.4.19 Sirius Facilities

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment