|

시장보고서

상품코드

1636215

데이터 센터 물류 시장 전망 : 시장 점유율 분석, 산업 동향과 통계, 성장 예측(2025-2030년)Data Center Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

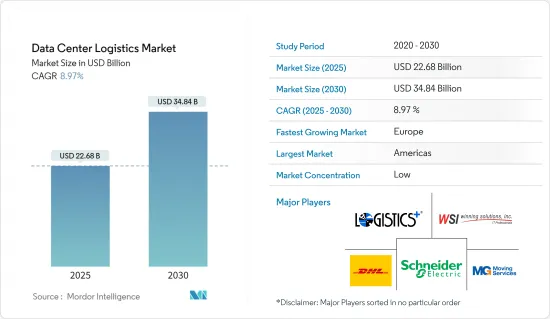

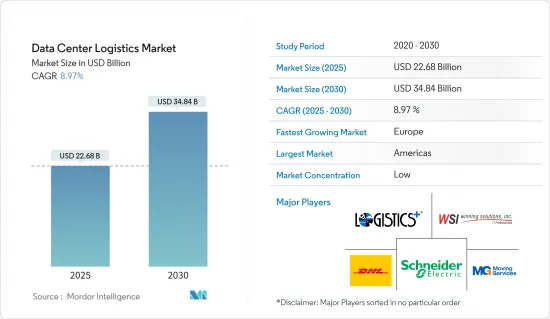

데이터 센터 물류 시장 규모는 2025년에 226억 8,000만 달러로 추정되며, 예측 기간(2025-2030년)의 연평균 성장율(CAGR)은 8.97%로, 2030년에는 348억 4,000만 달러에 이를 것으로 예측됩니다.

데이터 센터 물류 시장은 강력한 데이터 관리 인프라 및 서비스에 대한 전 세계적인 수요 증가에 힘입어 상당한 성장세를 보이고 있습니다. 이러한 성장을 뒷받침하는 몇 가지 중요한 요인이 있습니다. 산업 전반에서 클라우드 컴퓨팅, 빅데이터 분석, 디지털 서비스에 대한 의존도가 높아지면서 대량의 데이터를 안전하고 효율적으로 처리할 수 있는 첨단 데이터센터에 대한 필요성이 커지고 있습니다..

또한 디지털화와 IoT(사물 인터넷)의 확대로 인한 인터넷 트래픽의 급증은 데이터센터 시설에 대한 수요를 더욱 촉진하고 있습니다. 데이터 처리를 최적화하고 지연 시간을 줄이기 위해 하이브리드 클라우드 솔루션과 엣지 컴퓨팅을 도입하는 기업이 늘어나면서 이러한 복잡한 인프라를 지원하기 위한 민첩하고 확장 가능한 물류 솔루션이 필요합니다.

데이터 센터 물류 시장, 특히 민감한 장비의 안전한 운송, 온도 제어 스토리지 솔루션, 데이터 센터 시설의 신속한 구축 및 확장을 위한 효율적인 공급망 관리와 같은 전문 서비스에서 기회가 넘쳐나고 있습니다. 데이터 센터가 점점 더 대형화되고 지리적 이중화를 위해 분산됨에 따라 물류 제공업체는 데이터 관리의 복원력과 안정성을 보장하는 맞춤형 솔루션을 제공함으로써 이점을 활용할 수 있습니다.

또한 친환경 데이터센터와 지속 가능한 관행의 혁신은 새로운 성장의 길을 제시합니다. 환경적 지속 가능성에 대한 중요성이 점점 더 강조됨에 따라 물류업체는 데이터 센터 운영에서 탄소 배출량을 줄이고 에너지 효율성을 최적화하는 친환경 솔루션을 제공함으로써 차별화 할 수 있습니다.

결론적으로 데이터 센터 물류 시장은 기술 발전과 디지털 경제의 확장에 힘입어 빠르게 진화하고 있습니다. 데이터 센터 운영자의 다양하고 까다로운 요구를 충족시킬 준비가 된 물류 제공업체는 이 역동적인 시장에서 성장과 혁신을 위한 충분한 기회를 찾을 수 있을 것입니다.

데이터 센터 물류 시장 동향

IT 지출 급증과 GenAI 통합이 시장 성장 촉진

데이터 센터 시스템은 향후 수요가 크게 증가할 것으로 예상됩니다. 2023년에 이러한 시스템에 대한 전 세계 지출은 4% 증가했으며, 전문가들은 2024년에는 주로 GenAI의 부상에 힘입어 10%의 상당한 도약을 예상하고 있습니다. 기술 제공업체들은 기업 고객이 파악한 새로운 사용 사례에 맞춰 GenAI 기능을 자사 제품에 선제적으로 통합하고 있습니다.

업계 전문가들은 데이터 센터 물류 산업이 전 세계 IT 지출 추세를 반영하여 괄목할 만한 상승세를 보이고 있다고 강조합니다. 예를 들어, 2012년 1,400억 달러에 불과했던 이 지출은 2023년에는 2,361억 8,000만 달러로 크게 늘어날 것으로 예상됩니다. 이러한 추세는 데이터 스토리지, 고급 처리 및 클라우드 서비스의 영역이 계속 확장되고 있음을 생생하게 보여줍니다.

이 부문의 지출이 가파르게 증가함에 따라 데이터 센터 건설, 확장 및 유지를 위한 효율적인 물류에 대한 관심이 집중되고 있습니다. 이는 온도 제어 운송, 안전한 보관, 정시 인프라 배송을 포함하는 최첨단 솔루션에 대한 수요를 강조합니다. 데이터 센터에 대한 투자가 급증함에 따라 물류 공급업체는 규모를 확장할 뿐만 아니라 복잡성이 높아진 문제를 능숙하게 해결하는 동시에 혁신과 지속 가능성을 옹호하여 시장의 변화하는 요구를 충족해야 합니다.

하이퍼스케일 데이터 센터에서 미국의 우위가 데이터 센터 물류의 성장을 주도

업계 보고서에 따르면 미국은 전 세계 하이퍼스케일 데이터 센터 1,000개 중 500개 이상을 수용하고 있으며, 2024년 상반기에 이 기록을 달성할 것으로 예상했습니다. 2023년 말까지 Amazon, Microsoft, Google과 같은 주요 하이퍼스케일 제공업체가 운영하는 대형 데이터 센터는 992개에 달했습니다.

전문가들에 따르면 2024년에 총 5,381개에 달하는 미국의 데이터 센터 집중은 글로벌 데이터 인프라 환경에서 미국의 지배적인 위치를 강조합니다. 이 엄청난 숫자는 클라우드 컴퓨팅, 빅데이터 분석, 디지털 서비스에 대한 의존도가 높아짐에 따라 고급 데이터 관리 및 처리 기능에 대한 강력한 수요를 반영합니다. 따라서 미국 데이터 센터 물류 시장은 상당한 성장과 진화를 경험하고 있습니다. 이러한 성장에는 민감한 장비의 안전한 운송, 온도 제어 보관, 중요 부품의 적시 배송 등 데이터 센터 건설, 유지보수 및 확장과 관련된 복잡한 공급망을 관리할 수 있는 정교한 물류 솔루션이 필요합니다.

또한 미국에 데이터 센터가 집중되어 있기 때문에 데이터 관리의 복원력과 안정성을 보장하기 위해 지리적 이중화와 현지화된 데이터 스토리지 솔루션에 대한 중요성이 점점 더 커지고 있습니다. 이에 따라 미국의 물류업체들은 데이터센터 운영의 역동적이고 중요한 요구사항을 충족하기 위해 서비스 제공을 혁신하고 확장하고 있습니다. 더 많은 데이터 센터를 향한 추세는 전문 물류 서비스에 대한 강력한 수요를 강조하며 미국이 데이터 센터 물류 발전의 중추적인 시장으로 자리매김하고 있음을 보여줍니다.

데이터 센터 물류 산업 개요

데이터 센터 물류 시장은 전문 물류 기업과 엔드투엔드 공급망 솔루션을 제공하는 주요 공급업체를 아우르는 다양한 경쟁 구도를 특징으로 합니다. 아이언 마운틴, 슈나이더 일렉트릭, 디지털 리얼티를 비롯한 주목할만한 시장 기업은 각각의 전문 지식을 활용하여 데이터센터 운영 특유의 요구에 맞는 맞춤형 물류 서비스를 제공합니다.

이 시장의 확대 전략은 일반적으로 지리적 다양화, 온도 관리 운송 및 안전한 보관과 같은 전문 서비스의 도입, 실시간 추적 및 최적화를 위한 AI 및 IoT와 같은 최첨단 기술의 채택을 중심으로 전개되고 있습니다. 클라우드 컴퓨팅 및 데이터 스토리지 수요가 급증하면서 세계 데이터 센터 건설이 증가하는 가운데 물류 공급업체는 확장성과 지속가능성을 선호하고 더 큰 시장 점유율을 보장하기 위해 서비스 제공의 폭을 넓히고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 성과

- 조사의 전제

- 조사 범위

제2장 조사 방법

- 분석 방법

- 조사 단계

제3장 주요 요약

제4장 시장 인사이트

- 현재의 시장 시나리오

- 기술 동향

- 공급체인, 가치체인 분석에 대한 통찰

- 업계의 정부 규제에 관한 통찰

- 데이터센터의 계층 분류에 관한 통찰

- 업계의 기술 진보에 관한 통찰

- 지정학과 팬데믹이 시장에 미치는 영향

제5장 시장 역학

- 시장 성장 촉진요인

- 데이터 스토리지 및 데이터 처리에 대한 수요 증가

- 그린 데이터센터 중시의 고조

- 시장 성장 억제요인

- 인프라의 제약

- 기기 손상의 위험

- 시장 기회

- IT기업과의 전략적 파트너십

- 필요에 맞는 물류 솔루션 개발

- 업계의 매력 - Porter's Five Forces 분석

- 신규 진입업자의 위협

- 구매자, 소비자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제6장 시장 세분화

- 디바이스별

- 전기 디바이스(UPS 시스템, 기타 전기 인프라)

- 기계 장치(냉각 시스템, 랙 및 기타 기계 인프라)

- 데이터센터 규모별

- 중소규모 데이터센터

- 대규모 데이터센터

- 서비스별

- 수송

- 설치

- 창고 보관

- 부가가치 서비스

- 최종 사용자별

- 은행, 금융서비스, 보험

- IT 및 통신

- 정부 및 방위

- 헬스케어

- 기타 최종 사용자

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제7장 경쟁 구도

- 시장 집중도 개요

- 기업 프로파일

- Winning Solutions lnc

- Schneider Electric

- DHL

- Logistics Plus Inc.

- MG Moving Services

- Iron Mountain Inc.

- JK Moving

- Flexential

- Equinix

- CyrusOne*

- 기타 기업

제8장 시장 기회와 앞으로의 동향

제9장 부록

- 거시경제지표

- 자본 흐름의 통찰(운수, 창고 부문에 대한 투자)

- 대외무역 통계

The Data Center Logistics Market size is estimated at USD 22.68 billion in 2025, and is expected to reach USD 34.84 billion by 2030, at a CAGR of 8.97% during the forecast period (2025-2030).

The data center logistics market is poised for substantial growth, driven by escalating global demand for robust data management infrastructure and services. Several vital factors underpin this growth. The increasing reliance on cloud computing, big data analytics, and digital services across industries fuels the need for advanced data centers capable of handling large volumes of data securely and efficiently.

Additionally, the surge in internet traffic, driven by expanding digitalization and IoT (Internet of Things), further propels the demand for data center facilities. Companies increasingly adopt hybrid cloud solutions and edge computing to optimize data processing and reduce latency, necessitating agile and scalable logistics solutions to support these complex infrastructures.

Opportunities are surplus in the data center logistics market, particularly in specialized services such as secure transportation of sensitive equipment, temperature-controlled storage solutions, and efficient supply chain management for rapid deployment and expansion of data center facilities. As data centers become larger and more dispersed to ensure geographic redundancy, logistics providers can capitalize on offering tailored solutions that ensure resilience and reliability in data management.

Moreover, innovations in green data centers and sustainable practices present new avenues for growth. With increasing emphasis on environmental sustainability, logistics providers can differentiate themselves by offering eco-friendly solutions that reduce carbon footprints and optimize energy efficiency in data center operations.

In conclusion, the data center logistics market is evolving rapidly, driven by technological advancements and the expanding digital economy. Logistics providers poised to meet data center operators' diverse and demanding needs will find ample opportunities for growth and innovation in this dynamic market.

Data Center Logistics Market Trends

The Surge in IT Spending and GenAI Integration Augmenting Market Growth

Data center systems are expected to witness significant growth in demand in the future. In 2023, global expenditure on these systems saw a 4% uptick, and experts are eyeing a substantial 10% leap in 2024, propelled mainly by the rise of generative AI. Technology providers are proactively integrating GenAI features into their offerings, aligning with fresh use cases identified by their corporate clientele.

Industry experts underscore a remarkable upswing in the data center logistics industry, mirroring the global IT spending trends. For instance, from a modest USD 140 billion in 2012, this spending ballooned to a significant USD 236.18 billion by 2023. Such a trajectory vividly illustrates the mounting appetite for data storage, advanced processing, and the ever-expanding realm of cloud services.

With this sector's spending on a steep incline, the spotlight intensifies on efficient logistics for data center construction, expansion, and upkeep. It accentuates the demand for state-of-the-art solutions, encompassing temperature-controlled transit, secure storage, and punctual infrastructure deliveries. As investments in data centers surge, logistics providers must not only scale up but also deftly navigate heightened complexities, all while championing innovation and sustainability to cater to the market's evolving needs.

The Dominance of the United States in Hyperscale Data Centers is Driving Growth in Data Center Logistics

Industry reports indicate that the United States accommodates more than 500 of the 1,000 hyperscale data centers globally, a milestone reached in the first half of 2024. By the end of 2023, 992 large data centers were operated by leading hyperscale providers like Amazon, Microsoft, and Google.

As per experts, the concentration of data centers in the United States, totaling 5,381 units in 2024, highlights the country's dominant position in the global data infrastructure landscape. This substantial number reflects the robust demand for advanced data management and processing capabilities, driven by the increasing reliance on cloud computing, big data analytics, and digital services. Consequently, the US data center logistics market is experiencing significant growth and evolution. This growth necessitates sophisticated logistics solutions to manage the complex supply chains associated with data center construction, maintenance, and expansion, including secure transportation of sensitive equipment, temperature-controlled storage, and just-in-time delivery of critical components.

The high concentration of data centers in the United States also indicates a growing emphasis on geographic redundancy and localized data storage solutions to ensure resilience and reliability in data management. As a result, logistics providers in the United States are innovating and expanding their service offerings to meet the dynamic and critical needs of data center operations. The trend toward more data centers underscores a robust demand for specialized logistics services, positioning the country as a pivotal market for advancements in data center logistics.

Data Center Logistics Industry Overview

The data center logistics market features a diverse competitive landscape, encompassing specialized logistics firms and major providers offering end-to-end supply chain solutions. Notable market players, including Iron Mountain, Schneider Electric, and Digital Realty, leverage their expertise to deliver customized logistics services tailored to the unique needs of data center operations.

Expansion strategies in this market commonly revolve around geographic diversification, the introduction of specialized services like temperature-controlled transportation and secure storage, and the adoption of cutting-edge technologies such as AI and IoT for real-time tracking and optimization. With global data center construction on the rise, propelled by the surging demand for cloud computing and data storage, logistics provider are prioritizing scalability and sustainability and broadening their service offerings to secure a larger market share.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Analysis Methodology

- 2.2 Research Phases

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Current Market Scenario

- 4.2 Technological Trends

- 4.3 Insights on Supply Chain/Value Chain Analysis

- 4.4 Insights into Government Regulations in the Industry

- 4.5 Insights into Tier Classifications of Data Center

- 4.6 Insights into Technological Advancements in the Industry

- 4.7 Impact of Geopolitics and Pandemics on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Demand For Data Storage and Processing

- 5.1.2 Increasing Emphasis On Green Data Centers

- 5.2 Market Restraints

- 5.2.1 Infrastructure Limitations

- 5.2.2 Risk of Equipment Damage

- 5.3 Market Opportunities

- 5.3.1 Forming Strategic Partnerships With IT Companies

- 5.3.2 Developing Tailored Logistics Solutions

- 5.4 Industry Attractiveness - Porter's Five Forces Analysis

- 5.4.1 Threat of New Entrants

- 5.4.2 Bargaining Power of Buyers/Consumers

- 5.4.3 Bargaining Power of Suppliers

- 5.4.4 Threat of Substitute Products

- 5.4.5 Intensity of Competitive Rivalry

6 MARKET SEGMENTATION

- 6.1 By Devices

- 6.1.1 Electrical Devices (UPS Systems, Other Electrical Infrastructure)

- 6.1.2 Mechanical Devices (Cooling Systems, Racks, Other Mechanical Infrastructure)

- 6.2 By Size of Data Center

- 6.2.1 Small and Medium-scale Data Center

- 6.2.2 Large-scale Data Center

- 6.3 By Service

- 6.3.1 Transport

- 6.3.2 Installation

- 6.3.3 Warehousing

- 6.3.4 Value-added Services

- 6.4 By End User

- 6.4.1 Banking, Financial Services, and Insurance

- 6.4.2 IT and Telecommunications

- 6.4.3 Government and Defense

- 6.4.4 Healthcare

- 6.4.5 Other End Users

- 6.5 By Geography

- 6.5.1 North America

- 6.5.1.1 United States

- 6.5.1.2 Canada

- 6.5.1.3 Mexico

- 6.5.2 Europe

- 6.5.2.1 Germany

- 6.5.2.2 United Kingdom

- 6.5.2.3 France

- 6.5.2.4 Italy

- 6.5.2.5 Spain

- 6.5.2.6 Rest of Europe

- 6.5.3 Asia-Pacific

- 6.5.3.1 China

- 6.5.3.2 Japan

- 6.5.3.3 India

- 6.5.3.4 Australia

- 6.5.3.5 South Korea

- 6.5.3.6 Rest of Asia-Pacific

- 6.5.4 Middle East and Africa

- 6.5.4.1 GCC

- 6.5.4.2 South Africa

- 6.5.4.3 Rest of Middle East and Africa

- 6.5.5 South America

- 6.5.5.1 Brazil

- 6.5.5.2 Argentina

- 6.5.5.3 Rest of South America

- 6.5.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Market Concentration Overview

- 7.2 Company Profiles

- 7.2.1 Winning Solutions lnc

- 7.2.2 Schneider Electric

- 7.2.3 DHL

- 7.2.4 Logistics Plus Inc.

- 7.2.5 MG Moving Services

- 7.2.6 Iron Mountain Inc.

- 7.2.7 JK Moving

- 7.2.8 Flexential

- 7.2.9 Equinix

- 7.2.10 CyrusOne*

- 7.3 Other Companies

8 MARKET OPPORTUNITIES AND FUTURE TRENDS

9 APPENDIX

- 9.1 Macroeconomic Indicators

- 9.2 Insight Into Capital Flows (Investments In Transport and Storage Sector)

- 9.3 External Trade Statistics