|

시장보고서

상품코드

1636254

의료기기 및 장비 물류 - 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Medical Devices And Equipment Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

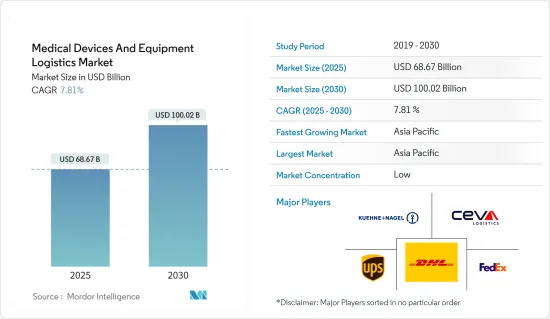

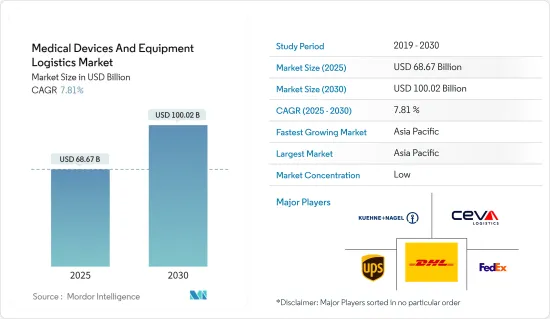

의료기기 및 장비 물류 시장 규모는 2025년에 686억 7,000만 달러로 추정되며, 예측 기간(2025-2030년) 동안 7.81%의 CAGR로 2030년에는 1,000억 2,000만 달러에 달할 것으로 예상됩니다.

의료기기 및 장비 물류 시장은 첨단 의료 서비스에 대한 수요 증가와 의료기기 기술 발전에 힘입어 빠르게 성장하고 있습니다. 제조업체와 의료 서비스 제공업체들은 중요한 장비를 적시에 전 세계로 배송하기 위해 공급망 운영의 효율성을 높이고 있습니다. 이러한 효율화는 자동화, 실시간 추적 시스템, 투명성 향상 및 비용 절감을 위한 첨단 재고 관리 기술을 통해 더욱 강화되고 있습니다.

2024년 2월, GobalMed Logistix(GMLx)는 애틀랜타 캠퍼스를 200% 확장하여 6만 5,000평방피트 규모의 새로운 시설을 도입한다고 발표하여 화제가 되었습니다. 이번 이전은 의료기기 물류 및 제3자 서비스에 대한 수요 증가에 직접적으로 대응하는 것으로, 업계의 물류 역량을 크게 향상시킬 것으로 기대됩니다.

메드트로닉의 드론 배송 검사와 같은 획기적인 노력은 윙과의 협력을 통해 라스트 마일 의료 물류에 혁명을 일으키고 있으며, 보다 신속하고 적응력 있는 공급망 솔루션을 약속하고 있습니다. 또한, 전 세계적으로 의료 인프라가 계속 확장되고 있으며, 특히 신흥국에서는 물류 제공업체들이 탄탄한 물류 네트워크를 구축하여 증가하는 수요에 대응할 수 있는 환경이 조성되고 있습니다.

예를 들어, 영국에 본사를 둔 Apian은 2023년 12월 NHS의 의료 공급 배송을 강화하기 위해 Zipline과 제휴하여 의료 물류의 지속적인 기술 혁신의 물결을 강조하고 있습니다.

의료기기 물류 시장 동향

의료기기 제조업체의 최첨단 물류 솔루션 통합

메드트로닉은 인슐린 펌프, 심박조율기, 당뇨병 치료 등 의료기기 및 치료제를 제조하는 다국적 기업으로, 2022년부터 물류 및 공급망 운영에 대한 대대적인 재검토에 착수하여 2024년에 그 결실을 맺을 예정입니다. 회사는 세계 운영 및 공급망(GOSC), 핵심 기술, 대기업 고객을 대상으로 한 상업 전략의 세 가지 주요 부문에 중점을 두었습니다. 이는 큰 방향 전환을 의미합니다.

2024년 7월, 메드트로닉은 아일랜드에서 최초로 드론 배송 업체인 Wing을 이용해 의료용품과 의료기기를 병원에 배송하는 기업 중 하나가 되었습니다. 양사는 더블린의 블랙록 헬스(Blackrock Health)와 세인트 빈센트(St. Vincent) 사립병원과 협력하여 드론이 의료에 어떻게 활용될 수 있는지를 입증하기 위해 드론 배송을 시범 운영할 예정입니다.

메드트로닉과 윙의 노력은 의료기기 시장에서 최첨단 물류 솔루션을 통합하는 것이 점점 더 중요해지고 있음을 강조하고 있습니다. 경쟁사 및 업계 이해관계자들도 이에 따라 공급망 효율화와 고객 서비스 향상을 위한 혁신적 기술 도입이 가속화될 것으로 보입니다.

영국 의료기기 제조 산업이 물류 산업을 주도하고 있습니다.

2022년 영국 통계청(Office for National Statistics)은 영국의 의료기기 및 치과 용품 제조 산업의 총 부가가치(GVA)가 약 29억 8,000만 파운드(38억 1,000만 달러)로 증가했다고 보고했습니다. 이러한 지속적인 성장은 이 산업의 경제적 중요성을 강조하며, 영국 내 의료기기 생산 및 수요 증가를 반영합니다.

산업이 확장됨에 따라 탄탄한 공급망과 유통 네트워크가 최우선 과제가 되고 있습니다. 이러한 네트워크는 의료 제품의 효율적인 세계 운송에 필수적이며, 의료 시설에 신속하게 도착하고 엄격한 규정을 준수할 수 있도록 보장합니다. 또한, 이 산업의 생산량 증가는 온도 제어 창고, 자동화된 재고 시스템, 특수 운송 솔루션과 같은 최첨단 물류 기술에 대한 투자를 촉진하고 있습니다.

러시아의 우크라이나 침공으로 피해를 입은 민간인들에게 UK-Med를 통해 의약품을 제공한 것과 같은 최근의 인도주의적 시도는 산업계의 의료 지원 역할을 더욱 부각시키고 있습니다.

요컨대, 영국 의료 및 치과용품 제조 산업의 GVA 증가는 물류가 중요한 의료기기의 접근성과 이용 편의성을 국내외로 확대하는 데 있어 물류가 필수적인 역할을 하고 있음을 강조합니다.

의료기기 및 장비 물류 산업 개요

UPS Healthcare, DHL Supply Chain, FedEx Healthcare Solutions, Kuehne Nagel, Ceva Logistics와 같은 물류 대기업이 주도하는 의료기기 및 장비 물류 시장은 세계 물류 강자부터 틈새 서비스 제공업체까지 다양한 업체가 경쟁하고 있습니다. Kuehne Nagel, Ceva Logistics와 같은 물류 대기업이 주도하고 있습니다. 이들은 광범위한 세계 네트워크, 최첨단 기술, 다양한 서비스를 보유하고 있습니다. 반대로 Cardinal Health, Owens & Minor, DB Schenker와 같은 전문적 진입 기업도 존재합니다. 이들 기업은 창고관리, 유통, 재고관리 등을 포함한 헬스케어 산업을 위한 맞춤형 물류 솔루션을 제공함으로써 독자적인 입지를 구축하고 있습니다.

물류 사업자와 의료 이해관계자들의 협업은 시장 침투를 확대하고 서비스 포트폴리오를 강화하기 위해 증가하고 있으며, IoT, AI, 블록체인과 같은 기술의 도입은 물류 체인의 효율성과 투명성을 향상시키기 위해 매우 중요합니다. 또한, 의료기기 물류에 대한 엄격한 모니터링을 고려할 때, 규제 준수와 품질 보증에 대한 확고한 약속은 여전히 가장 중요한 요소입니다.

기타 혜택

- 엑셀 형식의 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

목차

제1장 소개

- 조사 성과

- 조사 가정

- 조사 범위

제2장 조사 방법

- 분석 방법

- 조사 단계

제3장 주요 요약

제4장 시장 인사이트

- 현재 시장 시나리오

- 기술 동향

- 공급망/밸류체인 분석에 관한 인사이트

- 산업 규제에 관한 인사이트

- 산업의 기술적 진보에 관한 인사이트

- 지정학과 팬데믹이 시장에 미치는 영향

제5장 시장 역학

- 시장 성장 촉진요인

- 의료 서비스 세계적 확대

- 기술의 진보

- 시장 성장 억제요인

- 높은 운영 비용

- 규제의 복잡성

- 시장 기회

- 신흥 시장에 대한 진출

- 의료 프로바이더와의 전략적 파트너십과 협업 구축

- 산업의 매력 - Porter's Five Forces 분석

- 신규 참여업체의 위협

- 구매자/소비자의 협상력

- 공급 기업의 교섭력

- 대체품의 위협

- 경쟁 기업 간의 경쟁 강도

제6장 시장 세분화

- 제품 유형별

- 의료기기

- 의료장비

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC 국가

- 남아프리카공화국

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제7장 경쟁 구도

- 시장 집중도 개요

- 기업 개요

- UPS Healthcare

- DHL Supply Chain

- FedEx Healthcare Solutions

- Kuehne+Nagel

- Ceva Logistics

- Cardinal Health

- Owens & Minor

- DB Schenker

- DSV

- World Courier*

- 기타 기업

제8장 시장 기회와 향후 동향

제9장 부록

- 거시경제 지표

- 자본 플로우 인사이트(운송·창고 부문에 대한 투자)

- E-Commerce와 소비 관련 통계

- 대외무역 통계

The Medical Devices And Equipment Logistics Market size is estimated at USD 68.67 billion in 2025, and is expected to reach USD 100.02 billion by 2030, at a CAGR of 7.81% during the forecast period (2025-2030).

The medical devices and equipment logistics market is rapidly expanding, fueled by surging demand for advanced healthcare services and technological advancements in medical devices. Manufacturers and healthcare providers are increasingly streamlining their supply chain operations to ensure the timely global delivery of critical equipment. This efficiency drive is further empowered by automation, real-time tracking systems, and advanced inventory management techniques to boost transparency and cut costs.

In February 2024, GobalMed Logistix (GMLx) made headlines by unveiling a 200% expansion of its Atlanta campus, introducing a new 65,000-sq. ft facility. This move directly responds to the escalating need for medical device logistics and third-party services, marking a significant stride in the industry's logistics capabilities.

In collaboration with Wing, groundbreaking initiatives like Medtronic's drone delivery trials are revolutionizing last-mile healthcare logistics and promising swifter and more adaptable supply chain solutions. Moreover, the ongoing global expansion of healthcare infrastructure, especially in emerging economies, is creating a ripe environment for logistics providers to establish robust distribution networks and cater to mounting demands.

For instance, UK-based Apian partnered with Zipline in December 2023 to enhance NHS medical supply deliveries, underscoring the continuous wave of innovation in healthcare logistics.

Medical Devices and Equipment Logistics Market Trends

Medical Devices Manufacturer Integrate Cutting-edge Logistics Solutions

Medtronic is a multinational producer of medical devices and therapies, such as insulin pumps, pacemakers, and diabetes therapies. Since 2022, Medtronic has embarked on a massive overhaul of its logistics and supply chain operations that will culminate in 2024. The company has focused on three key areas: global operations and supply chain (GOSC), core technology, and commercial strategies targeting large enterprise customers. It represents a significant shift in direction.

In July 2024, Medtronic was among the first companies in Ireland to use the drone delivery company Wing to deliver medical supplies and devices to hospitals. The two companies are teaming up with Blackrock Health and St. Vincent's Private Hospital in Dublin to launch a drone delivery trial to demonstrate how drones can be used in healthcare.

Medtronic's initiative with Wing underscores the growing importance of integrating cutting-edge logistics solutions in the medical devices market. Competitors and industry stakeholders may follow suit, accelerating the adoption of innovative technologies to enhance supply chain efficiency and customer service.

UK Medical Devices Manufacturing Propels the Logistics Industry

In 2022, the Office for National Statistics reported that the UK manufacturing industry for medical and dental instruments and supplies saw its gross value added (GVA) climb to around GBP 2.98 billion (USD 3.81 billion). This consistent growth highlights the industry's economic significance and mirrors the escalating production and demand for medical instruments within the United Kingdom.

With the industry's expansion, robust supply chains and distribution networks become paramount. These networks are vital for the efficient global transportation of medical products, ensuring they reach healthcare facilities promptly and comply with stringent regulations. The industry's heightened manufacturing output also spurs investments in cutting-edge logistics technologies, including temperature-controlled storage, automated inventory systems, and specialized transportation solutions.

Recent humanitarian endeavors, like the country's provision of medical supplies to civilians affected by the Russian invasion of Ukraine through UK-Med, further underscore the industry's global healthcare support role.

In essence, the escalating GVA in the UK medical and dental supplies manufacturing industry accentuates the indispensable role of logistics in broadening the accessibility and availability of crucial healthcare equipment, both domestically and internationally.

Medical Devices and Equipment Logistics Industry Overview

The medical devices and equipment logistics market boasts a competitive landscape, hosting a diverse array of players, from global logistics powerhouses to niche service providers. Logistics giants like UPS Healthcare, DHL Supply Chain, FedEx Healthcare Solutions, Kuehne + Nagel, and Ceva Logistics lead the charge. These industry giants leverage their expansive global networks, cutting-edge technology, and a robust suite of services. Conversely, specialized players such as Cardinal Health, Owens & Minor, and DB Schenker carve their niche by tailoring logistics solutions for the healthcare sector, encompassing warehousing, distribution, and inventory management.

Collaborations between logistics entities and healthcare stakeholders are rising to broaden market penetration and enrich service portfolios. Embracing technologies like IoT, AI, and blockchain is pivotal, as they bolster efficiency and transparency in the logistics chain. Moreover, given the stringent oversight in medical device logistics, a steadfast commitment to regulatory compliance and quality assurance remains paramount.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Analysis Methodology

- 2.2 Research Phases

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Current Market Scenario

- 4.2 Technological Trends

- 4.3 Insights on Supply Chain/Value Chain Analysis

- 4.4 Insights into Governement Regualtions in the Industry

- 4.5 Insights into Technological Advancements in the Industry

- 4.6 Impact of Geopolitics and Pandemics on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Global Expansion of Healthcare Services

- 5.1.2 Technological Advancements

- 5.2 Market Restraints

- 5.2.1 High Operational Costs

- 5.2.2 Regulatory Complexity

- 5.3 Market Opportunities

- 5.3.1 Expansion into Emerging Markets

- 5.3.2 Forging Strategic Partnerships and Collaborations With Healthcare Providers

- 5.4 Industry Attractiveness - Porter's Five Forces Analysis

- 5.4.1 Threat of New Entrants

- 5.4.2 Bargaining Power of Buyers/Consumers

- 5.4.3 Bargaining Power of Suppliers

- 5.4.4 Threat of Substitute Products

- 5.4.5 Intensity of Competitive Rivalry

6 MARKET SEGMENTATION

- 6.1 By Product Type

- 6.1.1 Medical Devices

- 6.1.2 Medical Equipment

- 6.2 By Geography

- 6.2.1 North America

- 6.2.1.1 United States

- 6.2.1.2 Canada

- 6.2.1.3 Mexico

- 6.2.2 Europe

- 6.2.2.1 Germany

- 6.2.2.2 United Kingdom

- 6.2.2.3 France

- 6.2.2.4 Italy

- 6.2.2.5 Spain

- 6.2.2.6 Rest of Europe

- 6.2.3 Asia-Pacific

- 6.2.3.1 China

- 6.2.3.2 Japan

- 6.2.3.3 India

- 6.2.3.4 Australia

- 6.2.3.5 South Korea

- 6.2.3.6 Rest of Asia-Pacific

- 6.2.4 Middle East and Africa

- 6.2.4.1 GCC

- 6.2.4.2 South Africa

- 6.2.4.3 Rest of Middle East and Africa

- 6.2.5 South America

- 6.2.5.1 Brazil

- 6.2.5.2 Argentina

- 6.2.5.3 Rest of South America

- 6.2.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Market Concentration Overview

- 7.2 Company Profiles

- 7.2.1 UPS Healthcare

- 7.2.2 DHL Supply Chain

- 7.2.3 FedEx Healthcare Solutions

- 7.2.4 Kuehne + Nagel

- 7.2.5 Ceva Logistics

- 7.2.6 Cardinal Health

- 7.2.7 Owens & Minor

- 7.2.8 DB Schenker

- 7.2.9 DSV

- 7.2.10 World Courier*

- 7.3 Other Companies

8 MARKET OPPORTUNITIES AND FUTURE TRENDS

9 APPENDIX

- 9.1 Macroeconomic Indicators

- 9.2 Insight Into Capital Flows (Investments In Transport and Storage Sector)

- 9.3 E-commerce and Consumer Spending-related Statistics

- 9.4 External Trade Statistics