|

시장보고서

상품코드

1636269

ASEAN 국가의 플러그인 하이브리드 전기자동차 배터리 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)ASEAN Countries Plug-in Hybrid Electric Vehicle Battery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

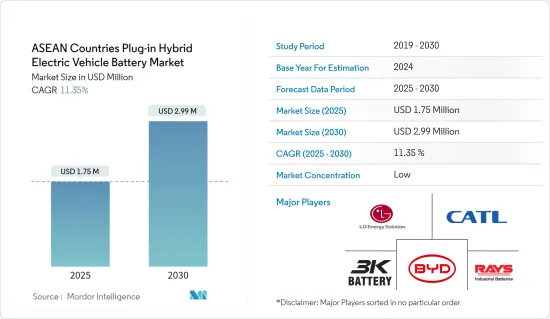

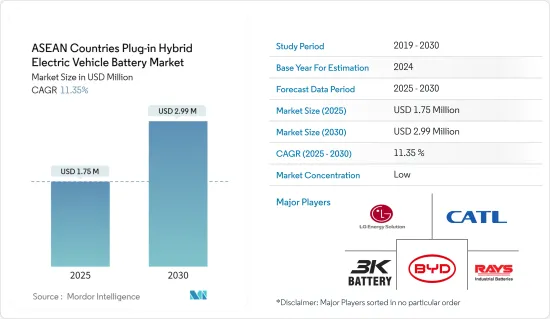

ASEAN 국가의 플러그인 하이브리드 전기자동차 배터리 시장 규모는 2025년에 175만 달러로 추정되며, 예측 기간(2025-2030년) 동안 11.35%의 CAGR로 2030년에는 299만 달러에 달할 것으로 예상됩니다.

주요 하이라이트

- 향후 몇 년 동안 ASEAN 국가의 플러그인 하이브리드 전기자동차 배터리 시장은 전기자동차 판매 급증과 리튬이온 배터리 가격 하락으로 인해 큰 영향을 받을 것으로 예상됩니다.

- 그러나 시장은 특히 플러그인 하이브리드 전기자동차 배터리 교체 비용의 급등이라는 역풍에 직면해 있습니다.

- 그러나 에너지 용량 향상과 항속거리 연장을 목표로 한 배터리 화학의 발전은 계속되고 있으며, 시장에 많은 기회를 가져올 것으로 예상됩니다.

- 향후 몇 년 동안 모든 국가 중 인도네시아가 시장을 독점할 것으로 예상됩니다.

ASEAN 국가의 플러그인 하이브리드 전기자동차 배터리 시장 동향

승용차가 성장을 주도

- 정부 정책, 환경 문제, 기술 발전의 혼합에 힘입어 플러그인 하이브리드 자동차(PHEV) 배터리 시장의 승용차 부문은 아세안(동남아시아국가연합) 국가에서 괄목할 만한 성장세를 보이고 있습니다.

- 급속한 도시화와 중산층의 급증으로 ASEAN 국가의 자동차 수요가 급증하고 있습니다. 도시 혼잡과 오염이 심각해짐에 따라 각국 정부는 엄격한 배기가스 규제와 전기자동차 및 하이브리드 자동차 도입을 촉진하는 인센티브로 대응하고 있습니다.

- ASEAN Automotive Federation의 데이터에 따르면, 2023년 판매량은 인도네시아가 77만 9,326대로 1위, 말레이시아가 71만 9,160대로 그 뒤를 이을 것으로 예상됩니다. 태국은 40만 6,501대, 베트남은 23만 706대, 필리핀은 11만 1,980대입니다. 싱가포르는 3만 2,511대, 미얀마는 2,832대입니다. 이러한 판매량은 해당 지역에서 승용차에 대한 구매 의지가 높아지고 있음을 입증하고 있습니다.

- 보조금, 세금 감면, 충전 인프라 구축 등 아세안 각국 정부의 노력은 아세안 전역에서 플러그인 하이브리드 자동차의 보급을 촉진하고 있습니다. 또한, 지역 간 협력과 R&D 투자는 아세안 자동차 부문에서 플러그인 하이브리드 자동차 배터리 시장의 중요성을 확고히 하고 있습니다.

- 태국 정부는 국내 PHEV용 배터리 생산을 촉진하기 위해 2023년 11월 'EV3.5' 보조금 프로그램을 도입했습니다. 이는 2024-2027년까지 유효하며, 생산된 배터리 1대당 최대 2,760달러의 보조금을 제공합니다.

- 주요 목적은 두 가지로, 외국의 투자를 유치하는 것과 동남아시아의 플러그인 하이브리드 자동차 배터리 제조의 중심지로서 태국의 위상을 확립하는 것입니다. 현재 중국의 플러그인 하이브리드 자동차 브랜드가 우위를 점하고 있고, 유럽 업체들의 관심도 높아지고 있는 상황에서 이러한 전략적 움직임은 빠르게 발전하고 있는 플러그인 하이브리드 자동차 배터리 분야에서 태국의 궤도를 재정의하는 것입니다.

- 배터리 기술의 발전은 아세안의 플러그인 하이브리드 자동차 시장을 결정적으로 형성하고 있습니다. 특히 리튬이온 배터리의 기술 혁신은 에너지 밀도를 높이고, 수명 주기를 연장하고, 급속 충전을 가능하게함으로써 플러그인 하이브리드 자동차의 매력을 높이고 있습니다.

- 이러한 움직임에 비추어 볼 때, 승용차 부문은 향후 몇 년 동안 성장할 가능성이 있습니다.

인도네시아의 시장 독점 전망

- 정부 정책, 경제 성장, 소비자 행동, 기술 발전 등의 요인에 힘입어 아세안 플러그인 하이브리드 자동차(PHEV) 배터리 시장의 인도네시아 부문은 눈에 띄게 변화하고 있습니다. 동남아시아 최대 경제대국인 인도네시아의 급성장하는 자동차 시장은 플러그인 하이브리드 전기자동차 부문에 큰 잠재력을 가지고 있습니다.

- 인도네시아 정부는 다양한 정책과 이니셔티브를 통해 탄소 배출량을 줄이고 지속가능한 교통수단을 장려하기 위해 적극적으로 노력하고 있습니다. 세제 혜택, 보조금, 그리고 중요한 것은 충전 인프라 개발 등 이러한 노력은 일반적으로 플러그인 하이브리드 전기자동차와 관련된 높은 초기 비용을 줄이는 것을 목표로 하고 있습니다.

- 인도네시아 산업부는 전기이륜차를 포함한 전기자동차 및 하이브리드 자동차에 대한 구매 보조금을 지급하고 있습니다. 또한 기존 내연기관 이륜차를 전기이륜차로 개조하기 위한 보조금도 지급할 예정입니다. 배터리 전기자동차 신규 구매 시 5,130달러의 보조금이 지급되며, 기존 하이브리드 차량에는 그 절반의 보조금이 지급됩니다.

- 지난 10년간 배터리 기술 및 제조의 비약적인 발전으로 인도네시아의 하이브리드 전기자동차에 리튬이온 배터리의 채택이 가속화되었습니다. 이러한 발전은 비용 절감뿐만 아니라 성능과 신뢰성을 향상시켜 리튬이온 배터리는 제조업체와 소비자 모두에게 선호되는 선택이 되었습니다.

- 최근 리튬이온 배터리와 셀 팩의 가격은 하락 추세로 최종사용자 산업에 호소하고 있으며, 2022년 소폭 상승 후 2023년 가격 하락이 재개되어 리튬이온 배터리 팩은 139달러/kWh의 역사적 최저치를 기록하여 14% 하락했습니다.

- 또한, 플러그인 하이브리드 전기자동차 배터리의 현지 제조 시설의 부상은 제조 비용을 낮출 수 있는 여건이 조성되고 있습니다. 그 결과, 플러그인 하이브리드 전기자동차는 소비자들에게 더욱 친숙하게 다가갈 수 있을 것으로 보입니다. 정부의 장려책과 기술 발전과 함께 저렴한 가격의 지속가능한 교통수단에 대한 이러한 경제적 기반은 인도네시아의 플러그인 하이브리드 전기자동차 시장이 크게 성장할 수 있는 원동력이 될 것입니다.

- 예를 들어, 2023년 6월 인도네시아는 Hapco Neta, Wuling, Chery, Xiaokang 등 중국 유명 자동차 제조업체 4곳과 중요한 협약을 체결하여 인도네시아를 잠재적인 전기자동차 수출 허브로 자리매김했습니다. 플러그인 하이브리드 전기자동차(PHEV)를 국내에서 생산하기 위한 조사 길을 모색하려는 명확한 의도가 있습니다. 기존 하이브리드 자동차보다 연비가 좋은 플러그인 하이브리드 전기자동차는 이미 중국에서 인기를 끌고 있습니다. 지리자동차는 야심찬 계획을 가지고 있으며, 2030년까지 10만 대의 전기자동차를 보급하는 것을 목표로 하고 있습니다.

- 이러한 신흥국 시장 개척을 감안할 때, 인도네시아는 향후 몇 년 안에 시장을 선도할 수 있는 태세를 갖추고 있습니다.

ASEAN 국가의 플러그인 하이브리드 전기자동차 배터리 산업 개요

ASEAN 국가의 플러그인 하이브리드 전기자동차 배터리 시장은 반분할 구조입니다. 이 시장의 주요 기업으로는 LG Energy Solution, Contemporary Amperex Technology, BYD Company, HDS Global Pte Ltd, 3K Battery 등이 있습니다.

기타 혜택

- 엑셀 형식의 시장 예측(ME) 시트

- 3개월 애널리스트 지원

목차

제1장 소개

- 조사 범위

- 시장 정의

- 조사 가정

제2장 주요 요약

제3장 조사 방법

제4장 시장 개요

- 소개

- 2029년까지 시장 규모와 수요 예측(단위 : 달러)

- 최근 동향과 개발

- 정부 정책 및 규정

- 시장 역학

- 성장 촉진요인

- 전기자동차 판매 성장

- 리튬이온 배터리 가격 하락

- 성장 억제요인

- 높은 전지 교환 비용

- 성장 촉진요인

- 공급망 분석

- 산업의 매력 - Porter's Five Forces 분석

- 공급 기업의 교섭력

- 소비자의 협상력

- 신규 참여업체의 위협

- 대체품의 위협 제품·서비스

- 경쟁 기업 간의 경쟁 관계

- 투자 분석

제5장 시장 세분화

- 배터리 유형

- 리튬이온 배터리

- 납축배터리

- 나트륨 이온 배터리

- 기타

- 차종

- 승용차

- 상용차

- 지역

- 싱가포르

- 필리핀

- 베트남

- 태국

- 말레이시아

- 인도네시아

- 기타 ASEAN 국가

제6장 경쟁 구도

- M&A, 합작투자, 제휴, 협정

- 주요 기업의 전략

- 기업 개요

- LG Energy Solution

- Contemporary Amperex Technology Co Ltd.

- BYD Company

- Panasonic Holdings Corporation

- Toshiba Corporation

- Enersys Sarl

- Exide Industries Ltd

- HDS Global Pte Ltd

- 3K Battery

- Clarios, LLC

- 기타 저명한 기업 리스트

- 시장 순위/점유율(%) 분석

제7장 시장 기회와 향후 동향

- 새로운 배터리 화학의 연구개발 지속

The ASEAN Countries Plug-in Hybrid Electric Vehicle Battery Market size is estimated at USD 1.75 million in 2025, and is expected to reach USD 2.99 million by 2030, at a CAGR of 11.35% during the forecast period (2025-2030).

Key Highlights

- In the coming years, the ASEAN Countries Plug-in Hybrid Electric Vehicle Battery Market is poised to be significantly influenced by surging electric vehicle sales and the plummeting costs of lithium-ion batteries.

- However, the market faces headwinds, notably from the steep replacement costs associated with plug-in hybrid electric vehicle batteries.

- Yet, ongoing advancements in battery chemistries, aimed at enhancing energy capacity and extending driving range, promise to unlock numerous opportunities for the market.

- Among all the countries, Indonesia is expected to dominate the market during the upcoming years.

ASEAN Countries Plug-in Hybrid Electric Vehicle Battery Market Trends

Passenger Vehicles to Witness Growth

- Driven by a mix of government policies, environmental concerns, and technological advancements, the passenger vehicle segment of the plug-in hybrid electric vehicle (PHEV) battery market is experiencing notable growth in ASEAN (Association of Southeast Asian Nations) countries.

- With rapid urbanization and a burgeoning middle class, ASEAN nations are witnessing a surge in vehicle demand. As urban congestion and pollution escalate, governments are responding with stringent emission regulations and incentives to promote electric and hybrid vehicle adoption.

- Data from the ASEAN Automotive Federation highlights Indonesia's lead in 2023 with 779,326 units sold, trailed by Malaysia at 719,160 units. Thailand's market stands robust at 406,501 units, while Vietnam and the Philippines report 230,706 and 111,980 units, respectively. Singapore and Myanmar round out the figures with 32,511 and 2,832 units. Such sales figures underscore the growing appetite for passenger vehicles in the region.

- Government initiatives, including subsidies, tax rebates, and charging infrastructure development, are propelling the adoption of plug-in hybrid vehicles across ASEAN. Furthermore, regional collaborations and R&D investments are solidifying the plug-in hybrid vehicle battery market's significance in the ASEAN automotive arena.

- In a move to boost domestic PHEV battery production, the Thai government, in November 2023, introduced the "EV3.5" subsidy program. This initiative offers a subsidy of up to USD 2,760 per battery produced, valid from 2024 to 2027.

- The primary objective is two fold: to entice foreign investments and cement Thailand's stature as a pivotal player in the Southeast Asian plug-in hybrid vehicle battery manufacturing landscape. Given the current dominance of Chinese plug-in hybrid vehicle brands and the growing interest from European counterparts, this strategic move is poised to redefine Thailand's trajectory in the swiftly evolving plug-in hybrid vehicle battery sector.

- Battery technology advancements are crucially shaping the plug-in hybrid vehicle market in ASEAN. Innovations, especially in lithium-ion batteries, are boosting energy density, extending life cycles, and enabling faster charging, thereby enhancing the allure of plug-in hybrids.

- Given these dynamics, the passenger vehicle segment is poised for growth in the coming years.

Indonesia is Expected to Dominate the Market

- Driven by factors such as government policies, economic growth, consumer behavior, and technological advancements, the Indonesian segment of the ASEAN plug-in hybrid electric vehicle (PHEV) battery market is undergoing a notable transformation. As Southeast Asia's largest economy, Indonesia's burgeoning automotive market holds immense promise for the plug-in hybrid electric vehicle sector.

- Through policies and initiatives, the Indonesian government is actively working to reduce carbon emissions and champion sustainable transportation. These efforts, including tax incentives, subsidies, and crucially, the development of charging infrastructure, aim to alleviate the higher upfront costs typically associated with plug-in hybrid electric vehicles.

- The Indonesian Ministry of Industry has rolled out purchase subsidies for electric and hybrid vehicles, including electric motorbikes. Furthermore, there's a push to subsidize converting traditional combustion-engine motorbikes to electric. New battery-electric vehicle purchases can benefit from a generous subsidy of USD 5,130, while conventional hybrids enjoy a subsidy that's half that amount.

- Over the past decade, breakthroughs in battery technology and manufacturing have accelerated the adoption of lithium-ion batteries in Indonesia's hybrid electric vehicle landscape. These advancements have not only reduced costs but also enhanced performance and reliability, making lithium-ion batteries a favored choice for both manufacturers and consumers.

- Recently, lithium-ion battery and cell pack prices have been on a downward trajectory, appealing to end-user industries. After a minor uptick in 2022, prices resumed their decline in 2023, with lithium-ion battery packs hitting a historic low at USD 139/kWh, marking a 14% decrease.

- Moreover, the rise of local manufacturing facilities for plug-in hybrid electric vehicle batteries is poised to drive down production costs. This, in turn, is set to make plug-in hybrid electric vehicles more accessible to consumers. Coupled with government incentives and technological strides, this economic pivot towards affordable and sustainable transportation is primed to spur substantial growth in Indonesia's plug-in hybrid electric vehicle market.

- For example, in June 2023, Indonesia sealed a significant agreement with four prominent Chinese automakers - Hapco Neta, Wuling, Chery, and Xiaokang - positioning Indonesia as a potential electric vehicle export hub. In talks with Chery Automobile, there's a clear intent to explore research avenues for manufacturing plug-in hybrid electric vehicles (PHEVs) domestically. Given their enhanced fuel efficiency over traditional hybrids, plug-in hybrid electric vehicles are already popular in China. Chery has ambitious plans, targeting a rollout of 100,000 electric vehicles by 2030.

- Given these developments, Indonesia is poised to lead the market in the coming years.

ASEAN Countries Plug-in Hybrid Electric Vehicle Battery Industry Overview

The ASEAN Countries Plug-in Plug-in Hybrid Electric Vehicle Battery Market is semi-fragmented. Some of the key players in this market (in no particular order) are LG Energy Solution, Contemporary Amperex Technology Co Ltd., BYD Company, HDS Global Pte Ltd, and 3K Battery

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Growing Electric Vehicle Sales

- 4.5.1.2 Decreasing Lithium-ion Battery Price

- 4.5.2 Restraints

- 4.5.2.1 High Battery Replacment Costs

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Battery Type

- 5.1.1 Lithium-ion Battery

- 5.1.2 Lead-Acid Battery

- 5.1.3 Sodium-ion Battery

- 5.1.4 Others

- 5.2 Vehicle Type

- 5.2.1 Passenger Cars

- 5.2.2 Commercial Vehicles

- 5.3 Geography

- 5.3.1 Singapore

- 5.3.2 Philippines

- 5.3.3 Vietnam

- 5.3.4 Thailand

- 5.3.5 Malaysia

- 5.3.6 Indonesia

- 5.3.7 Rest of ASEAN Countries

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 LG Energy Solution

- 6.3.2 Contemporary Amperex Technology Co Ltd.

- 6.3.3 BYD Company

- 6.3.4 Panasonic Holdings Corporation

- 6.3.5 Toshiba Corporation

- 6.3.6 Enersys Sarl

- 6.3.7 Exide Industries Ltd

- 6.3.8 HDS Global Pte Ltd

- 6.3.9 3K Battery

- 6.3.10 Clarios, LLC

- 6.4 List of Other Prominent Companies

- 6.5 Market Ranking/Share (%) Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Continued Research and Development In New Battery Chemistries