|

시장보고서

상품코드

1636516

중국의 전기자동차용 VRLA 전지 : 시장 점유율 분석, 산업 동향과 통계, 성장 예측(2025-2030년)China Electric Vehicle Vrla Batteries - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

■ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송일정은 문의해 주시기 바랍니다.

가격

※ 부가세 별도

한글목차

영문목차

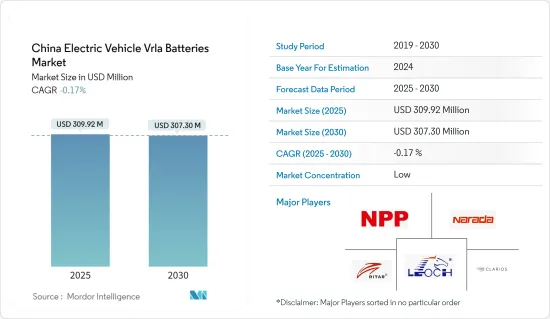

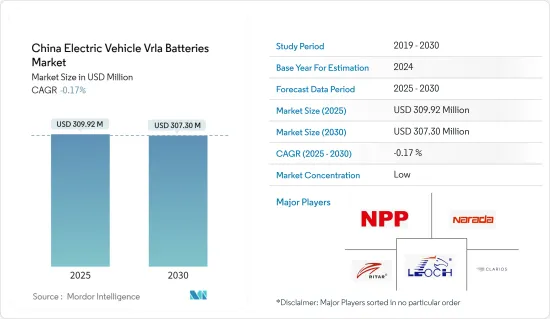

중국의 전기자동차용 VRLA 전지 시장 규모는 2025년 3억992만 달러로 추정되고, 2030년에는 3억730만 달러로 감소할 것으로 예측됩니다.

주요 하이라이트

- 향후 몇 년동안 전기자동차용 VRLA 전지 수요가 증가할 것으로 예상됩니다. 이는 리튬 이온 전지에 비해 비용 효과가 높고 전국적으로 전기 스쿠터와 전기 이륜차의 인기가 급상승하고 있는 것이 요인입니다.

- 반대로 고성능 EV의 표준이 되고 있는 첨단 리튬 이온 전지로의 신속한 전환은 전기자동차용 VRLA 전지 시장의 성장을 제한하고 있습니다.

- 그러나 VRLA 전지는 특히 에너지 밀도보다 신뢰성을 선호하는 시나리오에서 전기자동차의 보조 전원 또는 백업으로 여전히 가치를 유지하고 있습니다. 이 틈새 시장은 가까운 미래에 전기자동차용 VRLA 전지 시장에 큰 성장 가능성을 제공합니다.

중국 전기자동차용 VRLA 전지 시장 동향

AGM 전지가 크게 성장

- VRLA 전지, 특히 AGM 전지는 비용 효율성, 신뢰성 및 유지 보수가 필요없는 특성으로 인해 중국의 전기자동차 산업에서 자주 사용됩니다. AGM 전지는 리튬 이온 전지보다 저렴한 가격으로 전기자동차에 매력적인 선택입니다.

- VRLA 전지의 일종인 AGM(Absorbed Glass Mat) 전지는 기존의 납축전지를 능가하는 성능으로 주목을 받고 있습니다. 전해액을 흡수하기 위해 유리 섬유 매트 분리막을 사용함으로써 AGM 전지는 명확한 이점을 제공하며 특정 EV 응용 분야, 특히 저비용 전기 이동성에 적합합니다.

- 중국에서 이륜차와 삼륜차의 전기차가 보급됨에 따라 이 부문의 AGM 전지 수요가 급증하고 있습니다. 그러나 이륜차와 삼륜차 판매가 최근 둔화되어 AGM 전지 부문은 위협을 받고 있습니다. 국제에너지기구(IEA)의 데이터에 따르면 중국의 전동이륜차 판매량은 감소하여 2021년 1,020만대에서 590만대로 급감하고 있습니다. 앞으로는 리튬 이온을 필두로 하는 대체 전지 기술의 대두가 AGM 시장에 과제를 제시하게 됩니다.

- 중국의 전기자동차 전지 시장은 주로 신에너지 자동차(NEV) 보급에 의해 추진되고 있으며, 그 기세는 정부의 의무화에 의해 더욱 가속화되고 있습니다. 예를 들어 재무부는 2023년 6월에 2024년과 2025년에 구입한 NEV에 대해 1대당 3만 위안(미화 4,170달러)의 소비세 면제를 발표했습니다. 이 면세 정책은 2026-2027년에 걸친 구매에 대해서는 1만 5,000 위안으로 축소됩니다. 또한 EV 판매를 더욱 자극하기 위해 2020년 4월에 시작된 중국의 국가 신에너지차 보조금 제도는 당초 2020년 말 종료될 예정이었지만 COVID-19의 유행으로 2022년까지 연장 되었습니다.

- EV 부문, 특히 비용에 민감한 지역에서 AGM 전지의 중요성이 증가하는 것은 VRLA 기술의 지속적인 중요성을 강조합니다. 또한 정부의 합의와 이니셔티브는 EV의 보급을 촉진하고 지역의 EV 인프라를 강화할 것을 강조합니다.

- 그 결과 이러한 이니셔티브는 동지역의 EV 생산을 뒷받침할 뿐만 아니라 향후 수년간 EV용 VRLA 전지 수요를 높일 것입니다.

신에너지 차량용 충전 인프라를 대상으로 한 중국 시책

- 중국의 전기자동차 충전 인프라 추진 연맹(EVCIPA)에 따르면, 2023년 8월 현재 중국은 720만 8,000기의 충전 인프라(공공 및 민간)를 가지고 있습니다. 이 중 227만 2,000대가 공공 충전소로, 493만 6,000대가 자가용으로 지정되어 있습니다.

- 2024년 말 예측에서 중국의 EV 충전기 수는 958만 대로 급증하여 약 84%의 대폭적인 성장을 보입니다. 이 상승 궤도는 EV 충전기 시장에 엄청난 잠재력과 기회가 있음을 보여줍니다.

- 중국은 EV 충전 시장을 강화하기 위해 다음과 같은 주요 일정으로 일련의 세부 정책을 도입했습니다.

- 2023년 6월(시책 문서 : 고품질 충전 인프라 시스템의 추가 구축에 관한 지도 의견) : 이 시책은 도시, 고속도로, 농촌에 걸쳐 통일된 충전 네트워크를 확립하는 것을 목표로 합니다. 표준화, 규제, 시장 모니터링의 필요성을 강조하고, 2030년까지 세계의 충전 기술을 지배한다는 비전을 내걸고 있습니다.

- 2023년 5월(시책 문서 : 신에너지 자동차의 지방 보급과 지방 활성화를 보다 잘 지원하기 위한 충전 인프라 개발 가속화) : 이 이니셔티브는 현 레벨에서의 공공 충전 네트워크의 설치에 있어서 지방 자치체를 지원하고 상업용 건물, 교통 기지, 고속도로 주차장에 충전 지점의 설치를 촉진합니다.

- 2023년 1월(시책 문서 : 에너지 일렉트로닉스 산업의 개발 촉진에 관한 지도 의견) : 5G 기지국이나 신에너지 자동차 충전소 등, 신흥 설비에 있어서의 에너지 일렉트로닉스 제품 응용을 촉진하는 것에 중점을 둡니다.

- 2022년 12월(시책 문서 : 제14차 5개년 계획에 있어서의 내수 확대 실시 계획) : 주차장, 충전소, 전지 교환 스테이션, 수소 충전소 등의 지원 시설의 강화를 강조.

- 예를 들어 14차 5개년 계획에 따른 베이징시 도시관리개발계획은 2025년까지 누계 70만대의 전기자동차 충전기를 목표로 하고 있습니다.

- 이러한 정부의 이니셔티브는 단순한 수치가 아니라 충전 설비의 안전성, 인텔리전스, 연결성을 높이는 데 중점을 둡니다. 이러한 발전은 EV 산업을 전진시켜 향후 수년간 전지 시장을 강화시킬 수 있습니다.

중국 전기자동차용 VRLA 전지 산업 개요

중국의 전기자동차용 VRLA 전지 시장은 적정 수준으로 세분화되어 있습니다. 주요 기업(순서부동)으로는 NPP 파워그룹, 비전전지그룹, Zhejiang Narada Power Source, LEOCH Battery Corporation 등이 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사 범위

- 시장의 정의

- 전제조건

제2장 주요 요약

제3장 조사 방법

제4장 시장 개요

- 서문

- 2029년까지 시장 규모와 수요 예측(단위 : 달러)

- 최근 동향과 개발

- 정부의 규제와 시책

- 시장 역학

- 촉진요인

- VRLA 전지의 비용효과

- 전동 스쿠터와 전동 이륜차의 성장

- 억제요인

- 대체 전지 기술의 이용 가능성

- 촉진요인

- 공급망 분석

- 산업의 매력-PESTLE 분석

- 투자분석

제5장 시장 세분화

- 유형별

- AGM 전지

- 겔 전지

- 차종별

- 이륜차

- 저속 EV

- 산업용 EV

제6장 경쟁 구도

- M&A, 합작사업, 제휴, 협정

- 주요 기업의 전략

- 기업 개요

- LEOCH Battery Corporation

- Zhejiang Narada Power Source Co., Ltd.

- NPP Power Group

- C&D Technologies

- Shenzhen Ritar Power Co Ltd

- Clarious LLC

- Ritar Power

- GS Yuasa Battery Ltd.

- JYC Battery Manufacturer Co. Ltd.

- Chilwee Battery

- 기타 유력 기업 목록

- 시장 순위/점유율 분석

제7장 시장 기회와 앞으로의 동향

- 백업 및 보조 용도

The China Electric Vehicle Vrla Batteries Market size is estimated at USD 309.92 million in 2025, and is expected to decline to USD 307.30 million by 2030.

Key Highlights

- In the coming years, the demand for electric vehicle VRLA batteries is projected to rise, driven by their cost-effectiveness compared to lithium-ion batteries and the surging popularity of electric scooters and bikes nationwide.

- Conversely, the swift transition to advanced lithium-ion batteries, which are becoming the standard for high-performance EVs, poses a challenge to the growth of the electric vehicle VRLA batteries market.

- However, VRLA batteries still hold value as auxiliary power sources or backups in electric vehicles, especially in scenarios prioritizing reliability over energy density. This niche presents substantial growth potential for the electric vehicle VRLA batteries market in the near future.

China Electric Vehicle Vrla Batteries Market Trends

Absorbed Glass Mat Battery Witness Significant Growth

- Due to their cost-effectiveness, reliability, and maintenance-free nature, VRLA batteries, particularly Absorbed Glass Mat (AGM) types, are frequently utilized in China's EV industry. AGM batteries, being more affordable than lithium-ion counterparts, present an attractive option for electric vehicles.

- AGM (Absorbed Glass Mat) batteries, a subset of VRLA batteries, have garnered attention for outperforming traditional lead-acid variants. By utilizing a glass mat separator to absorb the electrolyte, AGM batteries offer distinct advantages, making them particularly suited for certain EV applications, especially in budget-friendly electric mobility.

- As two and three-wheeler electric vehicles gain traction in China, the demand for AGM batteries in this segment has surged. Yet, with a recent downturn in two and three-wheeler sales, the AGM battery sector is feeling the pinch. Data from the International Energy Agency (IEA) reveals a drop in electric two-wheeler sales in China, plummeting from 10.2 million in 2021 to 5.9 million. Looking ahead, the rise of alternative battery technologies, notably lithium-ion, poses a challenge to the AGM market.

- China's electric vehicle battery market is primarily propelled by the uptake of new energy vehicles (NEVs), a momentum further fueled by government mandates. For example, in June 2023, The Ministry of Finance announced a sales tax exemption of CNY 30,000 (USD 4,170) per vehicle for NEVs purchased in 2024 and 2025. This exemption will taper to CNY 15,000 for purchases made between 2026 and 2027. Additionally, China's national New Energy Vehicle Subsidy Program, initiated in April 2020 to further stimulate EV sales, was originally set to conclude at the end of 2020 but received an extension until 2022 due to the COVID-19 pandemic.

- The growing prominence of AGM batteries in the EV domain, especially in cost-sensitive regions, underscores the sustained significance of VRLA technology. Furthermore, government agreements and initiatives underscore a commitment to bolster EV adoption and enhance the region's EV infrastructure.

- Consequently, these initiatives are poised to not only boost EV production in the region but also elevate the demand for EV VRLA batteries in the coming years.

Chinese Policies Targeting Charging Infrastructure for New Energy Vehicles

- As of August 2023, China boasted 7,208,000 charging infrastructure units (both public and private), according to the China Electric Vehicle Charging Infrastructure Promotion Alliance (EVCIPA). Out of these, 2,272,000 were public charging stands, while 4,936,000 were designated for private use.

- Projections for the end of 2024 suggest that the number of EV chargers in China will surge to 9.58 million units, representing a substantial growth rate of approximately 84 percent. This upward trajectory underscores the immense potential and opportunities within the EV charging market.

- China has introduced a series of targeted policies to strengthen its EV charging market, with the following key dates:

- June 2023 (Policy Document: Guiding Opinions on Further Constructing a High-Quality Charging Infrastructure System): The policy aims to establish a unified charging network across urban, highway, and rural areas. It emphasizes the need for standardization, regulation, and market oversight, with a vision to dominate global charging technologies by 2030.

- May 2023 (Policy Document: Accelerating the Development of Charging Infrastructure to Better Support the Deployment of New Energy Vehicles in Rural Areas and Rural Revitalization): This initiative supports local governments in setting up public charging networks at the county level and facilitates the installation of charging points in commercial buildings, traffic hubs, and highway parking areas.

- January 2023 (Policy Document: Guiding Opinions on Promoting the Development of Energy Electronics Industry): Focuses on boosting the application of energy electronic products in emerging facilities, including 5G base stations and new energy vehicle charging stations.

- December 2022 (Policy Document: Implementation Plan for Expanding Domestic Demand in the 14th Five-Year Plan): Emphasizes the enhancement of supporting facilities like parking lots, charging stations, battery swapping stations, and hydrogen refueling stations.

- For example, the Beijing Urban Management Development Plan, aligned with the 14th Five-Year Plan, targets a cumulative total of 700,000 electric vehicle chargers by 2025.

- These governmental efforts are not just about numbers; they focus on elevating the safety, intelligence, and connectivity of charging facilities. Such advancements are poised to propel the EV industry forward, potentially bolstering the battery market in the coming years.

China Electric Vehicle Vrla Batteries Industry Overview

The China Electric Vehicle VRLA Batteries market is moderately fragmented. Some of the key players (not in particular order) are NPP Power Group., Vision Battery Group, Zhejiang Narada Power Source Co., Ltd., and LEOCH Battery Corporation, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Cost-Effectiveness of VRLA batteries

- 4.5.1.2 Growth in Electric Scooters and Bikes

- 4.5.2 Restraints

- 4.5.2.1 Availability of Alternate Battery Technology

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Industry Attractiveness - PESTLE Analysis

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 By Type

- 5.1.1 Absorbed Glass Mat Battery

- 5.1.2 Gel Battery

- 5.2 By Vehicle Type

- 5.2.1 Two-Wheelers

- 5.2.2 Low-Speed EVs

- 5.2.3 Industrial Evs

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 LEOCH Battery Corporation

- 6.3.2 Zhejiang Narada Power Source Co., Ltd.

- 6.3.3 NPP Power Group

- 6.3.4 C&D Technologies

- 6.3.5 Shenzhen Ritar Power Co Ltd

- 6.3.6 Clarious LLC

- 6.3.7 Ritar Power

- 6.3.8 GS Yuasa Battery Ltd.

- 6.3.9 JYC Battery Manufacturer Co. Ltd.

- 6.3.10 Chilwee Battery

- 6.4 List of Other Prominent Companies

- 6.5 Market Ranking/ Share Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Backup and Auxiliary Applications