|

시장보고서

상품코드

1849869

자동차용 플라스틱 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Automotive Plastics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

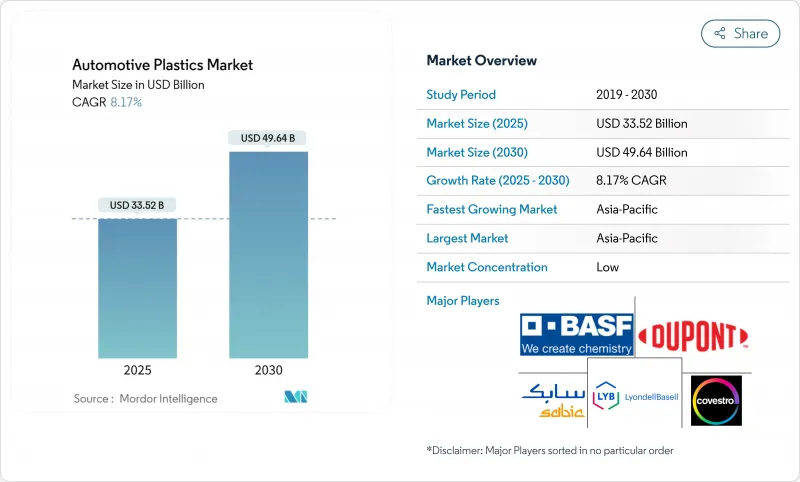

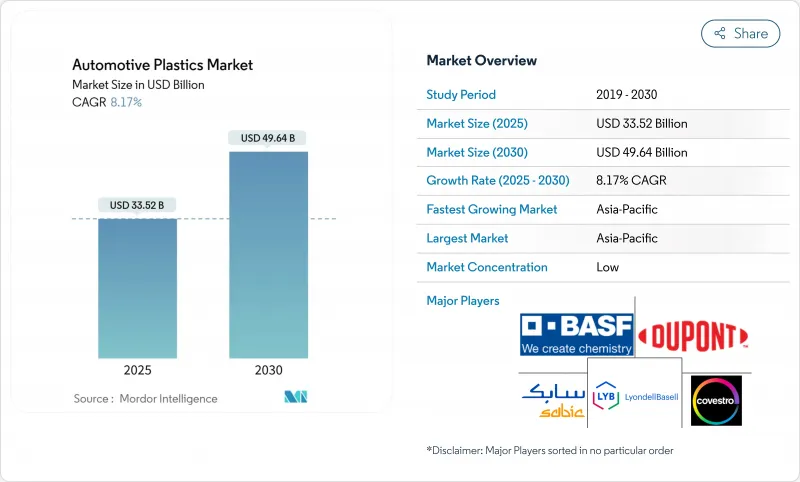

자동차용 플라스틱 시장 규모는 2025년에 335억 2,000만 달러로 추정되고, 예측 기간(2025-2030년) CAGR 8.17%로 성장할 전망이며, 2030년에는 496억 4,000만 달러에 달할 것으로 예측됩니다.

이 꾸준한 성장은 자동차 제조업체가 엄격한 배출 가스 규제와 성능 목표를 양립시키기 위해 경량 소재로 축발을 옮기는 것을 반영합니다. 특히 전기자동차(EV) 플랫폼에서 첨단 폴리머 솔루션의 채용이 가속화되고 있으며, 자동차용 플라스틱 시장은 과거의 속도를 크게 웃돌고 있습니다. 아시아태평양은 세계 수요의 거의 절반을 차지하며, 지역별로는 가장 빠른 페이스로 복합화가 진행되고 있습니다. 한편, 폴리프로필렌(PP)은 주요 자동차 시스템 전반에 걸쳐 비용 대 성능 기준을 계속 설정하고 있습니다.

세계의 자동차용 플라스틱 시장 동향 및 인사이트

전기자동차의 경량 재료에 대한 수요 증가

항속 거리에 대한 불안과 배터리 팩의 비용으로 경량화가 전기자동차 엔지니어링의 중심에 자리잡고 있습니다. PP 컴파운드는 현재 동급 내연 기관차보다 EV 1대당 대량으로 사용되고 있는데, 그 주된 이유는 질량의 감소가 배터리의 크기를 변경하지 않고 항속 거리의 연장으로 직접 변환되기 때문입니다. 계기판과 트림뿐만 아니라 고유전 PP 및 고급 폴리아미드 등급은 구조 하우징과 고전압 버스바에도 사용됩니다. EV 전용 플랫폼을 통해 설계자는 기존의 금속 하드 포인트에서 벗어나 바디 구조 및 열 관리 채널에 플라스틱 통합을 진행합니다.

탄소 배출 규제가 폴리 프로파일렌 범퍼의 채용을 가속

유럽과 북미의 플릿 평균 배출 가스 규제는 CO2 배출량 초과에 대해 많은 벌금을 부과합니다. 따라서 자동차 제조업체는 금속 보강 범퍼에서 완전 PP 범퍼로 전환하는 등 '퀵 윈'을 목표로 시스템 비용을 줄이면서 대폭적인 질량 절감을 실현하고 있습니다. 업계의 라이프사이클 평가는 사용 단계에서의 연료 절약을 고려하여 PP 범퍼가 강철 및 알루미늄 대체품보다 탄소 실적이 작다는 것을 지속적으로 보여줍니다.

냄새와 인화성에 의한 바이오 PA의 OEM 인증 지연

바이오 원료인 폴리아미드는 크래들에서 게이트까지의 배출량을 줄이는 것을 약속하지만, 잔류 냄새와 일관성 없는 발화 거동이 캐빈이나 언더후드의 인가를 복잡하게 하고 있습니다. 셀룰로오스 섬유 강화 바이오 PA의 학술적 연구는 섬유 분산성의 과제로 인한 기계적 특성의 변동이 큰 것으로 확인되었습니다. 업계 단체는 재료 공급업체가 배합을 미세 조정할 수 있도록 보다 긴 검증 사이클을 인정하도록 규제 당국에 청원하고 있습니다.

부문 분석

2024년 자동차용 플라스틱 시장 점유율은 폴리프로필렌이 34.18%를 차지하였고, 비용, 가공성, 물성의 균형이 잡혀 있는 것이 배경에 있습니다. 폴리프로필렌의 주된 용도는 내장재, 도어 트림, 센터 콘솔이지만, 유리 섬유 강화 등급은 반구조의 시트 캐리어나 테일 게이트에도 사용되고 있습니다.

폴리아미드는 고온의 전동 파워트레인이 보다 우수한 단열성과 유전 절연성을 요구하기 때문에 2030년까지 CAGR 8.87%로 상승할 전망입니다. PA66과 부분 방향족 PA6/6T 블렌드는 배터리 콜드 플레이트 어셈블리, 인버터 하우징, 터보 에어 덕트의 금속 브래킷을 대체합니다. 바이오 PA 등급은 아직 주류가 아니지만 냄새와 화염 전파 장애물이 해결되면 Scope-3의 탄소 감소를 요구하는 OEM을 매료시킵니다.

인테리어는 2024년 자동차용 플라스틱 시장 규모의 32.97%를 차지했으며, 소프트 터치 대시보드, 앰비언트 라이트 도어 패널, 디스플레이 클러스터의 일체 성형 유닛에 대한 수요에 지지를 받고 있습니다. 햅틱 코팅 및 레이저 에칭 그래픽은 특수 PP, ABS, PC/PMMA 블렌드에 의존하며 체험형 디자인에서 플라스틱의 역할을 강화하고 있습니다.

보닛 하부품은 절대량이야말로 적은 반면, 연율 8.98%로 성장하고 있습니다. 전자 아키텍처는 더 많은 전자 장비를 탑재하고 복잡한 냉각 채널을 필요로 하기 때문에 열 안정화 PA, PPS, PBT는 전자 모터 냉각 재킷과 고전압 버스 바 커버의 다이 캐스트 알루미늄을 대체합니다.

지역 분석

2024년 자동차용 플라스틱 시장은 아시아태평양이 48.25%의 점유율을 차지하였고, 2030년까지 CAGR 9.82%로 가장 높은 성장이 전망됩니다. 중국에서는 배터리 제조업체와의 제휴와 국가의 장려책에 지지된 대규모 EV 전개가 PP, PA, PBT의 밸류체인 전체에서 폴리머 생산 능력 확대에 박차를 가하고 있습니다. 인도는 승용차의 생산량이 2자리 증가를 기록하고 수입 의존을 억제하기 위해 현지 복합 허브에 투자를 유도합니다. 한국과 일본은 내충격성 외장 패널용 초고분자량 등급을 개량해 기술 혁신과 생산 능력의 선순환을 더욱 정착시킵니다.

북미는 성숙하면서도 독창적인 상황을 나타내고 있습니다. 기업 평균 연비 기준의 강화에 대응하기 위해 OEM은 리프트 게이트, 배터리 팩, 첨단 운전 지원 센서 하우징에 플라스틱을 최대한 활용하는 멀티 머티리얼 아키텍처를 추진하고 있습니다. 또한 미국에서는 수지 공급업체와 Tier1 성형 제조업체와의 폐쇄형 루프 재활용 파트너십의 선구적인 노력을 추진하고 있으며, 지역 서큘러 이코노미 목표를 지원하고 있습니다.

유럽은 고급 자동차 부문과 적극적인 규제 프레임워크을 통해 대규모 수요를 유지하고 있습니다. 승용차의 재활용 함량 25%의 기준안은 포스트 컨슈머 수지의 성능을 향상시키는 상용화제 첨가제나 탈취 시스템에 관한 연구 개발을 촉진합니다. 독일은 섬유 강화 PA 크로스 멤버의 기술 전개를 선도하고 프랑스와 영국은 바이오폴리머의 파일럿 라인에 공적 자금을 투입하고 있습니다. 그럼에도 불구하고, 이 지역은 에너지 비용의 변동으로 인한 마진 압력에 직면하고 있으며, 재료의 효율화가 전략적 급선무가 되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 전기자동차의 경량 소재 수요 증가

- 탄소 배출 페널티에 의해 폴리프로필렌 범퍼의 채용 가속

- 사출 성형 하이브리드에 의한 모듈러 프론트 엔드 캐리어(MEC)로의 이행

- 자동차 업계에서 유연하고 비용 효율적인 설계 재료 수요 증가

- 세계 자동차 산업의 꾸준한 확대

- 시장 성장 억제요인

- 냄새와 가연성에 의해 바이오 PA의 OEM 인정 지연

- 높은 재료비 및 가공비

- 자동차 업계의 대체 소재와의 경쟁 격화

- 밸류체인 분석

- Porter's Five Forces

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 규모 및 성장 예측

- 재료별

- 폴리프로필렌(PP)

- 폴리우레탄(PU)

- 폴리염화비닐(PVC)

- 폴리에틸렌(PE)

- 아크릴로니트릴부타디엔스티렌(ABS)

- 폴리아미드(PA)

- 폴리카보네이트(PC)

- 기타 재료

- 용도별

- 외관

- 인테리어

- 보닛 아래

- 기타 용도

- 차량 유형별

- 기존 차량

- 전기자동차

- 원료별

- 버진 플라스틱

- 재활용 플라스틱

- 바이오 기반 플라스틱

- 지역별

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율(%) 및 랭킹 분석

- 기업 프로파일

- Arkema

- Asahi Kasei Advance Corporation

- BASF SE

- Borealis AG

- Braskem

- Celanese Corporation

- Covestro AG

- Daicel Corporation

- Dow

- dsm-firmenich

- DuPont

- Evonik Industries AG

- Exxon Mobil Corporation

- INEOS

- LANXESS

- LG Chem

- LyondellBasell Industries Holdings BV

- Mitsui Chemicals Inc.

- SABIC

- TEIJIN LIMITED

제7장 시장 기회 및 향후 전망

AJY 25.11.12The Automotive Plastics Market size is estimated at USD 33.52 billion in 2025, and is expected to reach USD 49.64 billion by 2030, at a CAGR of 8.17% during the forecast period (2025-2030).

The steady uptick reflects automakers' pivot toward lighter materials to reconcile strict emission rules with performance targets. Accelerated adoption of advanced polymer solutions, especially in electric-vehicle (EV) platforms, is pushing the automotive plastics market well ahead of its historical pace. Asia-Pacific commands almost half of global demand and is compounding at the fastest regional rate, while polypropylene (PP) continues to set the benchmark for cost-to-performance across major vehicle systems.

Global Automotive Plastics Market Trends and Insights

Increasing demand for lightweight materials in electric vehicles

Range anxiety and battery-pack cost keep lightweighting at the center of EV engineering. PP compounds now appear in larger volumes per EV than in comparable internal-combustion cars, largely because lower mass converts directly into added driving range without resizing the battery. Beyond instrument panels and trims, high-dielectric PP and advanced polyamide grades are entering structural housings and high-voltage busbars. Dedicated EV platforms free designers from legacy metal hard-points, allowing more plastic integration into body structures and thermal-management channels.

Carbon-emission penalties accelerating polypropylene bumper adoption

Fleet-average emissions standards in Europe and North America impose significant financial penalties for excess CO2. Automakers therefore target "quick wins" such as switching from metal-reinforced to fully PP bumpers, achieving meaningful mass savings at lower system cost. Industry life-cycle assessments consistently show PP bumpers delivering a smaller carbon footprint than steel or aluminum alternatives once use-phase fuel savings are incorporated.

OEM qualification delays for Bio-PA due to odor & flammability

Bio-sourced polyamides promise lower cradle-to-gate emissions, yet residual odor and inconsistent ignition behavior complicate cabin and under-hood approvals. Academic work on cellulosic-fiber-reinforced Bio-PA confirms wide variability in mechanical properties stemming from fiber dispersion challenges. Industry groups have petitioned regulators to allow longer validation cycles so material suppliers can fine-tune formulations.

Other drivers and restraints analyzed in the detailed report include:

- Shift to Modular Front-End Carriers (MECs) via injection-molded hybrids

- Growing demand for flexible and cost-efficient design materials

- High materials and processing cost

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Polypropylene held a commanding 34.18% automotive plastics market share in 2024 on the back of balanced cost, processability and property retention. Interior fascia, door trims and center consoles dominate PP usage, but glass-fiber-reinforced grades now extend into semi-structural seat carriers and tailgates.

Polyamides are climbing an 8.87% CAGR trajectory through 2030 as high-temperature electrified powertrains demand better thermal and dielectric insulation. PA66 and partially aromatic PA6/6T blends displace metal brackets in battery-cold-plate assemblies, inverter housings and turbo-air ducts. Bio-based PA grades, while not yet mainstream, attract OEMs seeking Scope-3 carbon reductions once odor and flame-spread hurdles are cleared.

Interior accounted for 32.97% of the automotive plastics market size in 2024, buoyed by demand for soft-touch dashboards, ambient-lit door panels, and integrating display clusters into single multi-shot molded units. Haptic coatings and laser-etch graphics depend on specialty PP, ABS, and PC/PMMA blends, reinforcing plastics' role in experiential design.

Under-bonnet components, though smaller in absolute volume, are growing at 8.98% per year. Electrified architectures pack more electronics and require intricate cooling channels; thus, heat-stabilized PA, PPS, and PBT replace die-cast aluminum for e-motor cooling jackets and high-voltage busbar covers.

The Automotive Plastics Market Report Segments the Industry by Material (Polypropylene (PP), Polyurethane (PU), Polyvinyl Chloride (PVC), and More), Application (Exterior, Interior, and More), Vehicle Type (Conventional/Traditional Vehicles, and Electric Vehicles), Source (Virgin Plastic, Recycled Plastic, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa).

Geography Analysis

Asia-Pacific dominated the automotive plastics market with a 48.25% stake in 2024 and mirrors the highest regional CAGR at 9.82% to 2030. China's large-scale EV rollout, supported by battery-maker alliances and state incentives, is spurring polymer capacity expansions across PP, PA and PBT value chains. India records double-digit growth in passenger-car output, triggering investments in local compounding hubs to curb import reliance. South Korea and Japan refine ultra-high-molecular-weight grades for impact-resistant exterior panels, further embedding a virtuous innovation-capacity loop.

North America presents a mature yet inventive landscape. Compliance with tightening Corporate Average Fuel Economy standards pushes OEMs toward multi-material architectures that maximize plastics in liftgates, battery packs and advanced driver-assistance sensor housings. The United States also hosts pioneering work in closed-loop recycling partnerships between resin suppliers and tier-one molders, supporting local circular-economy targets.

Europe maintains sizeable demand anchored by premium vehicle segments and aggressive regulatory frameworks. The proposed 25% recycled-content threshold in passenger cars catalyzes R&D around compatibilizer additives and de-odorizing systems that elevate post-consumer resin performance. Germany leads technology deployments in fiber-reinforced PA cross-members, while France and the United Kingdom channel public funding toward biopolymer pilot lines. The region nevertheless faces margin pressures from energy-cost volatility, making material efficiency a strategic imperative.

- Arkema

- Asahi Kasei Advance Corporation

- BASF SE

- Borealis AG

- Braskem

- Celanese Corporation

- Covestro AG

- Daicel Corporation

- Dow

- dsm-firmenich

- DuPont

- Evonik Industries AG

- Exxon Mobil Corporation

- INEOS

- LANXESS

- LG Chem

- LyondellBasell Industries Holdings B.V.

- Mitsui Chemicals Inc.

- SABIC

- TEIJIN LIMITED

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Demand for Lighweight Materials in Electric Vehicles

- 4.2.2 Carbon Emission Penalties Accelerating Polypropylene Bumper Adoption

- 4.2.3 Shift to Modular Front-End Carriers (MECs) via Injection-Molded Hybrids

- 4.2.4 Growing Demand for Flexible and Cost Efficient Design Materials in Automotive

- 4.2.5 Consistent Expansion of the Global Automotive Sector

- 4.3 Market Restraints

- 4.3.1 OEM Qualification Delays for Bio-PA due to Odor and Flammability

- 4.3.2 High Materials and Processing Cost

- 4.3.3 Incraesing Competion from Alternative Materials in Automotive

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Material

- 5.1.1 Polypropylene (PP)

- 5.1.2 Polyurethane (PU)

- 5.1.3 Polyvinyl Chloride (PVC)

- 5.1.4 Polyethylene (PE)

- 5.1.5 Acrylonitrile Butadiene Styrene (ABS)

- 5.1.6 Polyamides (PA)

- 5.1.7 Polycarbonate (PC)

- 5.1.8 Other Materials

- 5.2 By Application

- 5.2.1 Exterior

- 5.2.2 Interior

- 5.2.3 Under Bonnet

- 5.2.4 Other Applications

- 5.3 Vehicle Type

- 5.3.1 Conventional/Traditional Vehicles

- 5.3.2 Electic Vehicles

- 5.4 Source

- 5.4.1 Virgin Plastic

- 5.4.2 Recycled Plastic

- 5.4.3 Bio-based Plastic

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 Japan

- 5.5.1.3 India

- 5.5.1.4 South Korea

- 5.5.1.5 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle East Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles {(includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)}

- 6.4.1 Arkema

- 6.4.2 Asahi Kasei Advance Corporation

- 6.4.3 BASF SE

- 6.4.4 Borealis AG

- 6.4.5 Braskem

- 6.4.6 Celanese Corporation

- 6.4.7 Covestro AG

- 6.4.8 Daicel Corporation

- 6.4.9 Dow

- 6.4.10 dsm-firmenich

- 6.4.11 DuPont

- 6.4.12 Evonik Industries AG

- 6.4.13 Exxon Mobil Corporation

- 6.4.14 INEOS

- 6.4.15 LANXESS

- 6.4.16 LG Chem

- 6.4.17 LyondellBasell Industries Holdings B.V.

- 6.4.18 Mitsui Chemicals Inc.

- 6.4.19 SABIC

- 6.4.20 TEIJIN LIMITED

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment

- 7.2 Technological Developments in Electric Vehicles