|

시장보고서

상품코드

1851292

APAC 사이버 보안 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)APAC Cybersecurity - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

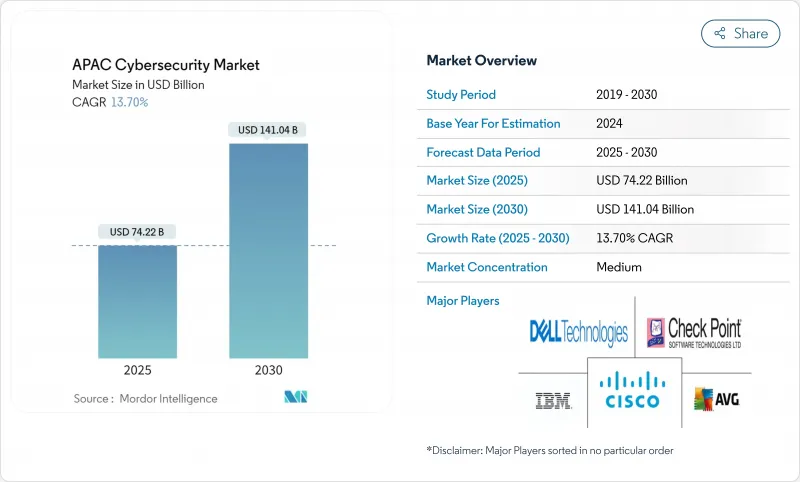

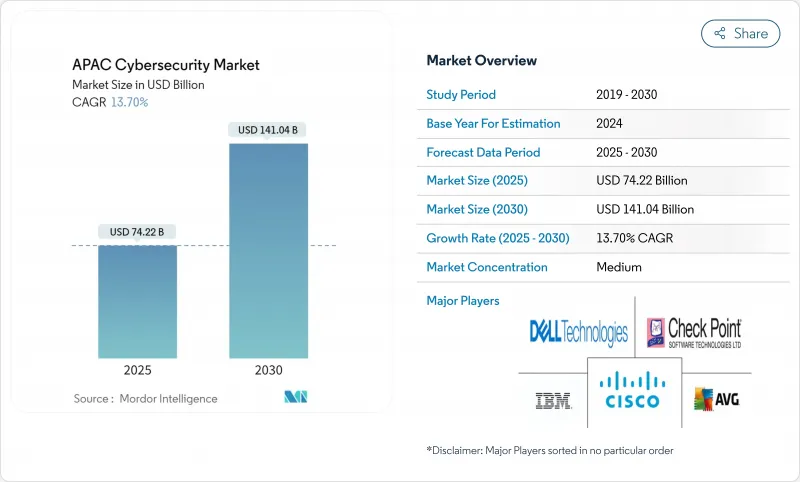

2025년 APAC 사이버 보안 시장 규모는 742억 2,000만 달러에 이르고, 2030년에는 13.7%의 연평균 복합 성장률(CAGR)을 나타내 1,410억 4,000만 달러에 달할 것으로 예상됩니다.

이는 정부가 디지털 주권을 추진하고 기업이 적극적인 사이버 방어 모델로 이동하고 있음을 반영합니다.

국가에 의한 공격의 격화, 5G 전개의 가속, 디지털 결제 사기의 급증, 만성적인 인재 부족에 의해 예산의 우선순위가 변화하고 있습니다. 경쟁은 이제 제품 기능보다 소블린 클라우드 아키텍처, AI 주도의 관리형 감지, 단편화된 규제 환경에서 IT와 OT의 통합 보안을 제공할 수 있는지 여부에 달려 있습니다. 현지화된 위협 인텔리전스와 확장 가능한 관리형 서비스를 결합하는 공급자는 특히 내부 보안 전문가가 충분한 서비스를 제공하지 않는 중견 시장 부문에서 비즈니스 기회를 확장하고 있습니다.

APAC 사이버 보안 시장 동향과 인사이트

정부 데이터 주권 의무화로 APAC 전반에 걸쳐 국내 사이버 보안 지출 가속화

2025년에 시행되는 중국의 네트워크 데이터 보안 관리 규칙은 중국 내에서의 데이터 처리가 의무화되고, 중국 내에서 사업을 전개하는 다국적 기업에는 개별적인 보안 스택이 도입됩니다. 싱가포르의 Cyber Essentials 프로그램은 정부와의 계약과 공급업체의 인증을 맺어 현지 공급자 수요를 환기합니다. 호주 REDSPICE 이니셔티브는 정보기관을 위한 소블린 클라우드에 20억 달러가 할당되어 정책이 사이버 보안 지출에 직접 반영됨을 보여줍니다. 공급업체는 현재 R&D 센터와 SOC를 현지화하여 시장에 대한 접근성을 유지하고 있는 반면, 자국 전문가들은 컴플라이언스 중심의 이점을 얻고 있습니다.

일본, 한국, 인도의 통신 사업자에게 새로운 네트워크 위협의 가능성을 가져오는 5G 롤아웃

높은 처리량의 5G 아키텍처는 기존 경계 도구로 보호할 수 없는 마이크로 슬라이싱 및 엣지 컴퓨팅 노드를 도입합니다. 일본의 액티브 사이버 방어법은 통신 네트워크를 표적으로하는 사이버 위협을 선제적으로 방해할 수 있습니다. 한국에서는 2024년에 공공 네트워크상에서 156만건의 해킹 시도가 기록되어 그 80%가 5G와 IoT의 엔드포인트를 노린 것이었습니다. 인도의 통신사는 침해의 57%가 서비스 저하로 이어졌습니다고 보고했으며, 제로 트러스트와 AI 주도 분석이 시급하다고 강조하고 있습니다. 그 결과 캐리어 환경에 최적화된 SASE(Secure Access Service Edge) 플랫폼과 가상화 방화벽에 대한 수요가 증가하고 있습니다.

심각한 사이버 보안 인력 부족이 신흥 APAC 경제의 서비스 비용을 팽창시킨다.

이 지역에는 280만 명의 미충족 사이버 담당자가 있으며, 관리 서비스의 확장성이 제한되어 중소기업의 예산을 초과하는 급여가 지급되고 있습니다. 필리핀에서는 싱가포르의 3,000명에 대해 공인된 전문가는 단 200명으로 프로젝트 지연을 증폭시키고 있습니다. 베트남은 2025년까지 1,000명의 전문가와 5,000명의 엔지니어를 육성하기 위한 인재 육성 프로그램에 1억 달러를 기록했습니다. 부족은 OT 보안 및 클라우드 아키텍처에서 가장 심각하며, 기업은 기능의 아웃소싱 및 배포를 연기해야 하며 대응 가능한 수요가 줄어들고 있습니다.

부문 분석

2024년 매출은 솔루션이 57.6%를 차지했지만, 2030년까지의 CAGR은 21.4%로, 기업이 인력 부족에 직면하는 가운데, 관리 보안 서비스가 확대될 것으로 예측됩니다. APAC 사이버 보안 시장은 24시간 365일 SOC 모니터링, 위협 조사, 사고 대응을 성과 기반 SLA에 번들로 제공하는 공급자에게 유리합니다. Ensign InfoSecurity는 2024년 세계 MSSP 10위를 차지한 유일한 APAC 기업으로, 이 지역이 관리 서비스의 성숙도에서 상승하고 있음을 보여주었습니다.

사내 분석가의 임금 상승과 침해에 대한 이사회 수준의 책임이 함께 대기업조차도 외부 SOC와 보안 도구를 공동 관리합니다. AI를 활용한 트리어지와 자동화를 통해 MSSP는 중견 시장 고객에게도 수익성 높은 서비스를 제공할 수 있게 되어 도입이 확대되고 있습니다. 그 결과 플랫폼 기반 서비스 제공에 대한 투자가 가속화되고 공급자는 XDR, SOAR, 머신러닝 분석을 통합하여 차별화를 도모하고 있습니다.

2024년 APAC 사이버 보안 시장 점유율은 On-Premise 유형이 62.5%를 차지했습니다. 한편, 클라우드 네이티브 보안은 원격 근무의 의무화와 멀티클라우드 배포에 힘입어 CAGR 23.5%를 나타낼 전망입니다. HashiCorp의 조사에 따르면 지역 기업의 70%가 멀티클라우드를 통해 비즈니스 목표를 달성했으며 90%가 보안을 결정적인 성공 요인으로 평가했습니다.

조직은 CSP 및 에지 노드에 걸친 워크로드를 보호하기 위해 제로 트러스트 네트워킹 및 컨테이너 보안을 채택합니다. 기술 부족은 여전히 역풍이며, 31%는 클라우드 전문 지식이 제한되어 있다고 하지만, 벤더는 로우 코드 정책 오케스트레이션이나 매니지드 SASE로 대항하고 있습니다. 그 결과 클라우드 구축이 그린 필드 프로젝트를 얻는 경우가 늘어나고 있지만 하이브리드 아키텍처는 레거시 시스템의 마이그레이션 경로로 부상하고 있습니다.

APAC 사이버 보안 시장 보고서는 업계를 솔루션, 서비스, 도입 형태(On-Premise, 클라우드), 최종 사용자 업계별(은행, 금융서비스 및 보험(BFSI), 헬스케어, IT 및 통신, 산업·방위, 제조, 소매 및 E-Commerce, 에너지·유틸리티, 제조, 기타), 최종 사용자 기업 규모별(중소기업, 대기업), 국가별로 분류하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 정부의 데이터 주권 의무화로 APAC 전체에서 국내 사이버 보안 투자 가속

- 일본, 한국, 인도의 통신 사업자에게 새로운 네트워크 위협의 가능성을 가져오는 5G 롤아웃

- 디지털 결제와 전자상거래 사기의 급증이 동남아시아의 보안 투자를 촉진

- APAC의 중요 인프라에 대한 국가 주도의 공격의 격화가 OT 보안 도입을 촉진

- 중국과 ASEAN에서 클라우드 워크로드 보호가 필요한 중소기업의 클라우드 이행 촉진

- 국가 사이버 보안 장려 프로그램(예 : SG Cyber Safe, REDSPICE)이 시장 성장을 가속

- 시장 성장 억제요인

- 심각한 사이버 보안 인력 부족이 신흥 APAC 경제권의 서비스 비용 상승 촉진

- 솔루션의 표준화를 막는 지역별 단편적인 컴플라이언스 체제

- APAC 중소기업의 가격 감도 높이가 선진적 솔루션 채용을 제한

- 보안·하드웨어 부품의 수출 규제에 의한 공급망의 혼란

- 중요한 규제 틀의 평가

- 밸류체인 분석

- 기술의 전망

- Porter's Five Forces

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

- 주요 이용 사례와 사례 연구

- 시장의 거시경제 요인에 미치는 영향

- 투자분석

제5장 시장 세분화

- 제공별

- 솔루션

- 애플리케이션 보안

- 클라우드 보안

- 데이터 보안

- 신원 및 접근 관리

- 인프라 보호

- 통합 위험 관리

- 네트워크 보안 기기

- 엔드포인트 보안

- 기타 서비스

- 서비스

- 전문 서비스

- 관리 서비스

- 솔루션

- 배포 모드별

- On-Premise

- 클라우드

- 최종 사용자 업계별

- BFSI

- 헬스케어

- IT 및 통신

- 산업 및 방위

- 제조업

- 소매 및 전자상거래

- 에너지 및 유틸리티

- 제조업

- 기타

- 최종 사용자 기업 규모별

- 중소기업(SME)

- 대기업

- 국가별

- 중국

- 일본

- 인도

- 한국

- 호주 및 뉴질랜드

- 싱가포르

- 기타 아시아태평양

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Cisco Systems, Inc.

- IBM Corporation

- Huawei Technologies Co., Ltd.

- Palo Alto Networks, Inc.

- Check Point Software Technologies Ltd.

- Fortinet, Inc.

- Kaspersky Lab

- Broadcom, Inc.(Symantec Enterprise Division)

- BAE Systems plc

- NEC Corporation

- Infosys Limited

- Tata Consultancy Services Limited

- Darktrace plc

- Zscaler, Inc.

- CrowdStrike Holdings, Inc.

- F5, Inc.

- Sophos Ltd.

- Okta, Inc.

- SentinelOne, Inc.

- Rapid7, Inc.

- Imperva, Inc

제7장 시장 기회와 향후 전망

KTH 25.11.12The APAC cybersecurity market size reached USD 74.22 billion in 2025 and is forecast to expand at a 13.7% CAGR to USD 141.04 billion by 2030, reflecting governments' push for digital sovereignty and enterprises' shift toward proactive cyber-defense models.

Heightened state-sponsored attacks, accelerating 5G roll-outs, surging digital-payment fraud, and chronic talent shortages are reshaping budget priorities, while local data-protection rules are recasting procurement in favor of regionally domiciled vendors. Competition now hinges less on product features and more on the ability to deliver sovereign-cloud architectures, AI-driven managed detection, and integrated IT-OT security across fragmented regulatory environments. Opportunities abound for providers that combine localized threat intelligence with scalable managed services, especially in mid-market segments underserved by in-house security expertise.

APAC Cybersecurity Market Trends and Insights

Government Data-Sovereignty Mandates Accelerating Domestic Cybersecurity Spend Across APAC

China's Network Data Security Management Regulations taking effect in 2025 require in-country data processing and create separate security stacks for multinationals operating inside China. Singapore's refreshed Cyber Essentials program ties government contracts to vendor certification, driving local provider demand. Australia's REDSPICE initiative allocates AUD 2 billion to a sovereign cloud for the intelligence community, illustrating how policy translates directly into cybersecurity outlays. Vendors now localize R&D centers and SOCs to preserve market access, while homegrown specialists gain a compliance-driven edge.

5G Roll-Outs Creating New Network Threat Surfaces for Telcos in Japan, South Korea and India

High-throughput 5G architectures introduce micro-slicing and edge-compute nodes that traditional perimeter tools cannot secure. Japan's Active Cyber Defense law authorizes pre-emptive disruption of cyber threats targeting telecom networks. South Korea logged 1.56 million hacking attempts on public networks in 2024, 80% aimed at 5G and IoT endpoints. India's operators report that 57% of breaches result in service slowdowns, highlighting the urgency for zero-trust and AI-driven analytics. Consequently, demand is rising for secure access service edge (SASE) platforms and virtualized firewalls optimized for carrier environments.

Acute Cybersecurity Talent Shortage Inflating Service Costs in Emerging APAC Economies

The region accounts for 2.8 million unfilled cyber roles, restricting managed-service scalability and pushing salaries beyond SME budgets. The Philippines counts only 200 certified specialists versus Singapore's 3,000, amplifying project delays. Vietnam earmarked USD 100 million for workforce programs to train 1,000 experts and 5,000 engineers by 2025. Scarcity is most severe in OT security and cloud architecture, forcing enterprises to outsource functions or postpone deployments, dampening addressable demand.

Other drivers and restraints analyzed in the detailed report include:

- Surge in Digital-Payment and E-Commerce Fraud Driving Security Investments in Southeast Asia

- Escalating State-Sponsored Attacks on APAC Critical Infrastructure Stimulating OT Security Adoption

- Fragmented Regional Compliance Regimes Complicating Solution Standardization

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solutions retained 57.6% revenue in 2024, yet managed security services are projected to expand 21.4% CAGR through 2030 as enterprises confront staffing gaps. The APAC cybersecurity market favors providers that bundle 24X7 SOC monitoring, threat hunting, and incident response under outcome-based SLAs. Ensign InfoSecurity became the only APAC firm to reach the global top-10 MSSP list in 2024, signaling the region's ascent in managed-service maturity.

Rising wages for in-house analysts, coupled with board-level accountability for breaches, push even large enterprises to co-manage security tools with external SOCs. AI-assisted triage and automation enable MSSPs to serve mid-market clients profitably, widening adoption. As a result, investment in platform-based service delivery is accelerating, with providers embedding XDR, SOAR, and machine-learning analytics to differentiate.

On-premise installations held 62.5% of APAC cybersecurity market share in 2024 because regulated sectors still favor physical control over data. Cloud-native security, however, is growing at 23.5% CAGR, propelled by remote-work mandates and multi-cloud adoption. A HashiCorp survey showed 70% of regional firms hit business targets via multi-cloud, with 90% rating security the defining success factor.

Organizations are embracing zero-trust networking and container security to protect workloads that span CSPs and edge nodes. Skills shortages remain a headwind-31% cite limited cloud expertise-but vendors counter with low-code policy orchestration and managed SASE offerings. Consequently, cloud deployments increasingly win green-field projects, while hybrid architectures emerge as a transition path for legacy systems.

The APAC Cybersecurity Market Report Segments the Industry Into by Offering (Solutions, and Services), Deployment Mode (On-Premise, and Cloud), End-User Vertical (BFSI, Healthcare, IT and Telecom, Industrial and Defense, Manufacturing, Retail and E-Commerce, Energy and Utilities, Manufacturing, and Others), and End-User Enterprise Size (Small and Medium Enterprises (SMEs), and Large Enterprises), and Country.

List of Companies Covered in this Report:

- Cisco Systems, Inc.

- IBM Corporation

- Huawei Technologies Co., Ltd.

- Palo Alto Networks, Inc.

- Check Point Software Technologies Ltd.

- Fortinet, Inc.

- Kaspersky Lab

- Broadcom, Inc. (Symantec Enterprise Division)

- BAE Systems plc

- NEC Corporation

- Infosys Limited

- Tata Consultancy Services Limited

- Darktrace plc

- Zscaler, Inc.

- CrowdStrike Holdings, Inc.

- F5, Inc.

- Sophos Ltd.

- Okta, Inc.

- SentinelOne, Inc.

- Rapid7, Inc.

- Imperva, Inc

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government Data-Sovereignty Mandates Accelerating Domestic Cybersecurity Spend Across APAC

- 4.2.2 5G Roll-Outs Creating New Network Threat Surfaces for Telcos in Japan, South Korea and India

- 4.2.3 Surge in Digital Payments and E-commerce Fraud Driving Security Investments in Southeast Asia

- 4.2.4 Escalating State-Sponsored Attacks on APAC Critical Infrastructure Stimulating OT Security Adoption

- 4.2.5 SME Cloud Migration Wave Necessitating Cloud Workload Protection in China and ASEAN

- 4.2.6 National Cybersecurity Incentive Programs (e.g., SG Cyber Safe, REDSPICE) Catalyzing Market Growth

- 4.3 Market Restraints

- 4.3.1 Acute Cybersecurity Talent Shortage Inflating Service Costs in Emerging APAC Economies

- 4.3.2 Fragmented Regional Compliance Regimes Complicating Solution Standardization

- 4.3.3 High Price Sensitivity Among APAC SMEs Limiting Adoption of Advanced Solutions

- 4.3.4 Supply-Chain Disruptions from Export Controls on Security Hardware Components

- 4.4 Evaluation of Critical Regulatory Framework

- 4.5 Value Chain Analysis

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Key Use Cases and Case Studies

- 4.9 Impact on Macroeconomic Factors of the Market

- 4.10 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 By Offering

- 5.1.1 Solutions

- 5.1.1.1 Application Security

- 5.1.1.2 Cloud Security

- 5.1.1.3 Data Security

- 5.1.1.4 Identity and Access Management

- 5.1.1.5 Infrastructure Protection

- 5.1.1.6 Integrated Risk Management

- 5.1.1.7 Network Security Equipment

- 5.1.1.8 Endpoint Security

- 5.1.1.9 Other Services

- 5.1.2 Services

- 5.1.2.1 Professional Services

- 5.1.2.2 Managed Services

- 5.1.1 Solutions

- 5.2 By Deployment Mode

- 5.2.1 On-Premise

- 5.2.2 Cloud

- 5.3 By End-User Vertical

- 5.3.1 BFSI

- 5.3.2 Healthcare

- 5.3.3 IT and Telecom

- 5.3.4 Industrial and Defense

- 5.3.5 Manufacturing

- 5.3.6 Retail and E-commerce

- 5.3.7 Energy and Utilities

- 5.3.8 Manufacturing

- 5.3.9 Others

- 5.4 By End-User Enterprise Size

- 5.4.1 Small and Medium Enterprises (SMEs)

- 5.4.2 Large Enterprises

- 5.5 By Country

- 5.5.1 China

- 5.5.2 Japan

- 5.5.3 India

- 5.5.4 South Korea

- 5.5.5 Australia and New Zealand

- 5.5.6 Singapore

- 5.5.7 Rest of Asia Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Cisco Systems, Inc.

- 6.4.2 IBM Corporation

- 6.4.3 Huawei Technologies Co., Ltd.

- 6.4.4 Palo Alto Networks, Inc.

- 6.4.5 Check Point Software Technologies Ltd.

- 6.4.6 Fortinet, Inc.

- 6.4.7 Kaspersky Lab

- 6.4.8 Broadcom, Inc. (Symantec Enterprise Division)

- 6.4.9 BAE Systems plc

- 6.4.10 NEC Corporation

- 6.4.11 Infosys Limited

- 6.4.12 Tata Consultancy Services Limited

- 6.4.13 Darktrace plc

- 6.4.14 Zscaler, Inc.

- 6.4.15 CrowdStrike Holdings, Inc.

- 6.4.16 F5, Inc.

- 6.4.17 Sophos Ltd.

- 6.4.18 Okta, Inc.

- 6.4.19 SentinelOne, Inc.

- 6.4.20 Rapid7, Inc.

- 6.4.21 Imperva, Inc

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment