|

시장보고서

상품코드

1639366

중동과 아프리카의 유리병 및 유리용기: 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Middle East & Africa Glass Bottles And Containers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

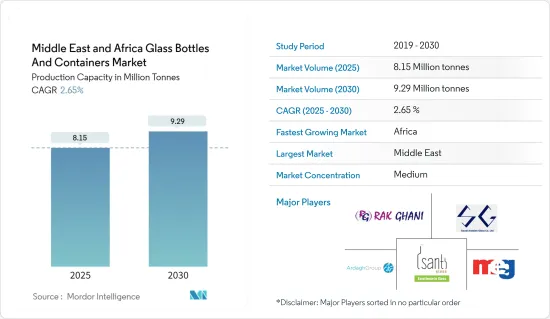

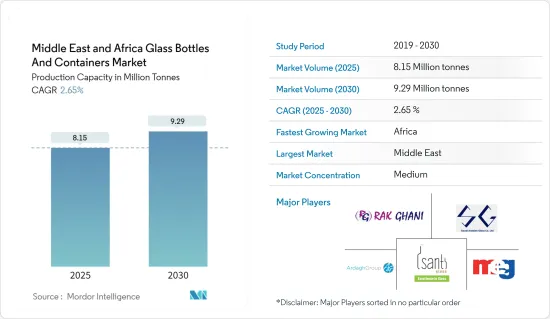

중동과 아프리카의 유리병 및 유리용기 시장 규모는 생산능력 기준으로 2025년 815만톤에서 2030년에는 929만톤으로 확대되며 예측기간(2025-2030년)의 CAGR은 2.65%가 될 전망입니다.

유리용기는 투명하고 소비자가 제품을 확인할 수있는 반면 관능적이고 영양가 높은 품질을 보호할 수 있습니다. 이 특성은 음료 및 의약품 포장에 이 지역에서 선호되는 선택권으로서의 입지를 확고하게 합니다.

주요 하이라이트

- 중동과 아프리카에서는 사우디아라비아와 남아프리카에서 음료 소비가 증가함에 따라 유리용기 수요가 급증하고 있습니다. 이러한 음료 소비 증가는 관광 산업의 활황, 가처분 소득 증가, 소비자의 기호의 진화에 기인하고 있습니다.

- 소비자들 사이에서 환경 문제와 지속가능성에 대한 의식이 높아지고 플라스틱보다 유리 포장을 선호하는 경향에 박차가 걸리고 있습니다. 이 변화는 주로 유리가 재활용 가능하기 때문에 환경 친화적인 선택으로 인식되기 때문입니다.

- 이 지역의 국가들은 강력한 경제 성장과 국내 소비 증가에 힘입어 음식 및 식품 산업의 번영을 목격하고 있습니다. 미국 농무부(USDA)의 보고에 따르면 아랍에미리트(UAE)에는 2,000개가 넘는 음식 및 음료 제조 기업이 있으며, 총 76억 3,000만 달러의 연간 수익을 올리고 있습니다.

- 소비자가 더 안전하고 건강한 포장을 추구함에 따라 유리 포장은 다양한 카테고리에서 성장하고 있습니다. 엠보싱, 성형, 예술적 마감과 같은 혁신적인 기술은 최종 사용자들 사이에서 유리 포장의 매력을 향상시킵니다. 또한, 유행 후 시장의 부활은 환경 친화적 인 제품에 대한 수요가 증가하고 음식 부문의 관심이 높아지기 때문입니다.

- 유리산업용 출판사인 Glass Online의 조사에 의하면 현재 세계 인구의 약 16%를 보유하고 있으며, 2030년에는 20%를 나타낼 것으로 예상되는 아프리카는 유리 제조업체에게 큰 비즈니스 기회입니다. 이 대륙은 소비자의 선택이 제한된 미개척 시장을 자랑합니다. 아프리카 대륙의 제2 경제대국인 남아프리카는 유리용기 생산의 선진국입니다. 연간 100만톤 이상의 생산 능력을 가진 남아프리카는 아프리카의 선진적인 유리용기 생산국 중 하나가 되고 있습니다.

- 그러나 시장은 문제에 직면하고 있습니다. 비용 효율이 높고 유리보다 가벼운 것으로 평가되고 플라스틱 포장에 대한 선호도가 높아지는 것이 큰 장애물이되었습니다. 또한 플라스틱과는 달리 유리는 깨지기 쉽기 때문에 운송 비용이 높아져 운송 중에 파손될 위험이 있으며 중동과 아프리카 시장 성장을 방해할 수 있습니다.

중동과 아프리카 유리병 시장 동향

의약품 부문이 가장 높은 시장 점유율을 기록할 전망

- 중동과 아프리카에서는 의료 산업이 약물 전달 제품에 대한 규제를 강화하고 있으며, 생명 공학 및 비용 중심의 의약품의 중요성이 커지고 있습니다. 제약 유리 제조업체는 제품 보존 기간 연장을 목적으로 하는 포장 솔루션에 대한 투자를 늘리고 있습니다.

- 이 지역 정부는 의료 인프라와 서비스를 강화하기 위해 민간 협력을 추진하고 있습니다. 주요 제약 회사는 중동, 특히 사우디아라비아(KSA), 아랍에미리트(UAE) 및 남아프리카에서 사업 거점을 확대하고 시장 성장을 견인하고 있습니다. 재무 권고사인 알펜 캐피탈은 아랍에미리트(UAE)의 의료 지출은 2020년에 197억 달러로, 2025년에는 269억 달러에 이를 것으로 예측하고 있다고 보고했습니다. 이러한 의료 지출 증가는 이 부문의 유리용기에 기회를 가져올 수 있습니다.

- 세계경제포럼이 2023년 3월에 지적한 바와 같이, 백신의 불균등한 분배나 수입 약품에의 의존과 같은 과제에 직면해 온 아프리카 국가들은 강력한 국내 제약산업을 발전시키는 것의 중요성을 인식하고 있습니다. 아프리카 대륙 자유 무역 지역(AfCFTA) 협정이 현재 효과적이기 때문에 아프리카의 의약품 무역은 주로 아프리카 역내 무역에 의해 크게 밀어올릴 수 있습니다.

- 게다가 많은 기업들이 중동 국가로의 진출을 검토하고 있으며, 중요한 의약품의 현지 생산을 늘림으로써 유리용기 수요를 높이고 있습니다. 2024년 9월, AstraZeneca Egypt는 의약품 생산에 5,000만 달러의 투자를 발표했습니다. 현재 연간 9억정을 생산하고 있는 AstraZeneca는 생산량을 12억 9,000만정으로 늘리는 것을 목표로 하고 있으며, 이 지역의 유리용기에 대한 수요를 높이고 있습니다.

- 게다가 사우디아라비아 식품의약국(SFDA)의 데이터는 임상검사의 진보와 제조에 있어서의 인공지능의 도입이 사우디아라비아의 의약품 시장 확대의 주요 촉매가 되고 있음을 강조하고 있습니다. 이 시장 규모는 인구 증가와 만성 질환 치료 수요가 증가함에 따라 2021년 54억 달러에서 2023년에는 85억 달러로 급증합니다.

남아프리카는 크게 성장할 것으로 예상

- 알코올 음료와 비알코올 음료 모두에 대한 수요가 증가함에 따라 유리 포장의 요구도 커지고 있습니다. 유리는 맛과 신선도를 유지하는 능력이 우수하기 때문에 종종 선호됩니다. 지속가능성이 중요해지면서 소비자는 친환경 포장 솔루션에 매료되고 있습니다. 유리는 재활용 가능하며 플라스틱보다 환경 친화적이기 때문에 많은 기업들이 유리 포장으로 전환하고 있습니다.

- 남아프리카의 유리용기 산업에서는 두 회사가 지배적인 지위를 차지합니다. Consol Glass는 국내 시장의 약 75-80%라는 압도적인 점유율을 자랑합니다. 한편, Nampak Glass는 국내 유리용기 수요의 20-25%를 확보하고 있습니다.(참조 소스: Glass Online).

- 2023년 11월, Ardagh Glass Packaging-Africa(AGP-Africa)는 남아프리카의 하우텐주 나이겔에 있는 생산 시설의 N3로에 점화했습니다. 15억 레알(8,000만 달러)의 거대한 프로젝트를 승인으로부터 불과 1년여로 예정대로 예산 내에서 완성시킨 것은 모든 이해관계자에게 칭찬할만한 위업입니다. 나이젤 3(N3) 확대의 선물은 같은 부지에서 N2 확대 프로젝트의 가동 개시에 이어졌습니다. 이 새로운 퍼니스는 4개의 생산 라인과 함께 시설 생산량을 50% 증가시켰습니다. 그 결과 나이젤은 아프리카 최대의 유리용기 생산 거점이 되어 세계에서 가장 광범위하고 효율적인 시설 중 하나로 꼽히게 되었습니다.

- 게다가 남아프리카공화국에서 알코올 음료 소비 증가는 이 수요를 촉진하는데 중요한 역할을 합니다. 런던에 본사를 둔 정보 서비스 회사 IWSR의 데이터는 2023년 남아프리카에서 맥주 소비량이 9% 급증한다는 점을 강조하고 있습니다. 이 증가는 급속한 도시 확대와 젊은층이 대도시로 이주하여 알코올 음료에 대한 접근성이 향상된 것과 관련이 있습니다.

- 또한 남아프리카 통계국에 따르면 알코올 음료와 담배 소비자 물가 지수(CPI)는 2023년 9월 111.1에서 2024년 7월 115.7로 상승했습니다. 이러한 음료 가격의 상승은 전국적인 평균 수요와 함께 용기들이 들어 있는 유리에 대한 수요 증가를 뒷받침하고 있습니다.

- 남아프리카의 레스토랑과 카페에서 소비 지출 증가는 병과 그릇을 포함한 유리용기 제품 수요에 박차를 가하고 있습니다. 남아프리카 통계국에 따르면 레스토랑과 다방의 식품 매출이 증가하고 있으며, 2024년 1월 1억 4,387만 달러에서 2024년 3월에는 1억 5,604만 달러로 급증하고 있습니다.

중동과 아프리카의 유리병 및 유리용기 시장의 주요 기업

중동과 아프리카의 유리병 및 유리용기 시장은 치열한 경쟁과 적당한 통합이 특징입니다. 국내외 무대에서 경쟁하고있는 주요 기업들은 RAK Ghani Glass LLC, Isanti Glass, Ardagh Group SA, East Glass Manufacturing Company 등이 있습니다. 이들 기업은 신제품 개발, 사업 확대, M&A 등의 전략을 추진하고 제품의 기능성을 높이고 중동 국가의 지리적 존재를 확대하고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

- 시장 개요

- 유리용기의 수출입 무역 데이터

- PESTLE 분석

- 포장용 유리용기의 산업 표준과 규제

- 용기 포장의 지속가능성 동향

- 중동과 아프리카의 유리용기 용량과 입지

제5장 시장 역학

- 시장 성장 촉진요인

- 이 지역의 다양한 음식과 음식의 소비 증가

- 제약 산업에서 유리용기 수요 증가

- 시장 성장 억제요인

- 유리용기보다 플라스틱 용기 수요가 시장 성장의 방해가 될 가능성

- 무역개황 : 중동의 유리용기산업의 수출입 패러다임의 역사와 현황 분석

제6장 시장 세분화

- 최종 사용자 산업별

- 음료

- 알코올 음료(정성 분석 제공 예정)

- 와인과 증류주

- 맥주 사이다

- 기타 알코올 음료

- 비알코올 음료(정성 분석 제공 예정)

- 탄산음료

- 주스류

- 물

- 우유음료

- 향료 음료

- 기타 무알코올 음료

- 식품

- 화장품

- 의약품(바이알·앰풀 제외)

- 기타

- 음료

- 국가별

- 아랍에미리트(UAE)

- 사우디아라비아

- 이집트

- 남아프리카

- 나이지리아

- 쿠웨이트

제7장 경쟁 구도

- 기업 프로파일

- RAK Ghani Glass LLC

- Isanti Glass

- Ardagh Group SA

- Saudi Arabian Glass Company Ltd

- Middle East Glass Manufacturing Company

- Altajir Glass Industries

- Nafis Glass

- Mahmood Saeed Glass Industry Co.

제8장 보충 자료 : 지역 내 주요 컨테이너 유리 공장에 대한 주요 용광로 공급업체 분석

제9장 시장 전망

KTH 25.02.07The Middle East & Africa Glass Bottles And Containers Market size in terms of production capacity is expected to grow from 8.15 million tonnes in 2025 to 9.29 million tonnes by 2030, at a CAGR of 2.65% during the forecast period (2025-2030).

Glass containers offer transparency, enabling consumers to see the product while safeguarding its sensory and nutritional qualities. This attribute has solidified their status as the region's preferred choice for packaging beverages and pharmaceuticals.

Key Highlights

- The demand for glass containers surges in the Middle East and Africa, driven by increasing beverage consumption in Saudi Arabia and South Africa. This uptick in beverage consumption is witnessed owing to a booming tourism industry, rising disposable incomes, and evolving consumer preferences.

- Heightened awareness of environmental issues and sustainability among consumers has spurred a preference for glass packaging over plastic. This shift is mainly because glass is perceived as a more environmentally friendly option, thanks to its recyclability.

- Countries in the region are witnessing a thriving food and beverage industry fueled by strong economic growth and heightened domestic consumption. Highlighting this growth, the US Department of Agriculture (USDA) reports that the United Arab Emirates is home to more than 2,000 food and beverage manufacturing companies, collectively raking in an impressive USD 7.63 billion in annual revenue.

- As consumers increasingly demand safer and healthier packaging, glass packaging is witnessing growth across various categories. Innovative technologies, such as embossing, shaping, and artistic finishes, enhance the appeal of glass packaging among end-users. Additionally, the post-pandemic resurgence of the market can be attributed to the rising demand for eco-friendly products and heightened interest from the food and beverage sector.

- Accordiung to a study by Glass Online, a publisher for the glass industry, Africa, currently home to about 16% of the global population and projected to reach 20% by 2030, presents a significant opportunity for glass producers. The continent boasts untapped markets where consumers face limited choices. South Africa, the continent's second-largest economy, is a leading nation in container glass production. With a production capacity surpassing 1 million tons annually, South Africa has become one of Africa's advanced container glass producers.

- However, the market faces challenges. The rising preference for plastic packaging, lauded for its cost-effectiveness and lighter weight than glass, poses a significant hurdle. Furthermore, glass' fragility, in contrast to plastic, results in higher freight costs and risks of breakage during transit, potentially hindering market growth in the Middle East and Africa.

Middle East and Africa Glass Bottles Market Trends

Pharmaceuticals Segment is Expected to Register the Highest Market Share

- In the MENA region, the healthcare industry has tightened regulations on drug delivery products, highlighting the growing importance of biotech and cost-sensitive medications. Pharmaceutical glass manufacturers are increasingly investing in packaging solutions aimed at extending product shelf life.

- Governments in the region are promoting public-private partnerships to enhance healthcare infrastructure and services. Key pharmaceutical companies are expanding their footprint in the Middle East, particularly in Saudi Arabia (KSA), the United Arab Emirates (UAE), and South Africa, driving market growth. Alpen Capital, a financial advisory firm, reported that healthcare spending in the UAE was USD 19.7 billion in 2020 and is projected to hit USD 26.9 billion by 2025. This uptick in healthcare spending could present opportunities for container glass in the sector.

- As noted by the World Economic Forum in March 2023, African countries, which have faced challenges like unequal vaccine distribution and a dependence on imported medicines, recognize the importance of developing a strong domestic pharmaceutical industry. With the African Continental Free Trade Area (AfCFTA) agreement now active, there's potential for a significant boost in Africa's pharmaceutical trade, largely driven by intra-African commerce.

- Additionally, many companies are looking to expand in Middle Eastern countries to increase local production of vital medications, thereby heightening the demand for container glass. In September 2024, AstraZeneca Egypt announced a USD 50 million investment in pharmaceutical production. Currently producing 900 million tablets yearly, AstraZeneca has set its sights on increasing output to 1.29 billion, subsequently driving up the demand for glass containers in the area.

- Moreover, data from the Saudi Food & Drug Authority (SFDA) highlights that advancements in clinical trials and the adoption of artificial intelligence in manufacturing are key catalysts for Saudi Arabia's expanding pharmaceutical market. The market's value jumped from USD 5.4 billion in 2021 to USD 8.5 billion in 2023, driven by a growing population and rising demand for chronic disease treatments.

South Africa is Expected to Experience Significant Growth

- As the demand for both alcoholic and non-alcoholic beverages rises, so does the need for glass packaging. Glass is often preferred for its superior ability to preserve flavor and freshness. With a growing emphasis on sustainability, consumers are gravitating towards eco-friendly packaging solutions. Given that glass is recyclable and considered more environmentally friendly than plastics, many companies are making the switch to glass packaging.

- In South Africa's container glass industry, two dominant players hold sway. Consol Glass, the more prominent of the duo, boasts a commanding share of approximately 75-80% of the domestic market. In contrast, Nampak Glass secures 20-25% of the nation's container glass demand. (Source: Glass Online).

- In November 2023, Ardagh Glass Packaging-Africa (AGP-Africa) ignited the N3 furnace at its production facility located in Nigel, Gauteng, South Africa. Completing a significant R 1.5 billion (USD 0.08 billion) mega-project on schedule and within budget, just over a year post-approval, is a commendable feat for all stakeholders. The unveiling of the Nigel 3 (N3) expansion followed the operational commencement of the N2 expansion project at the same site. This new furnace, coupled with four production lines, amplifies the facility's output by 50%. As a result, Nigel now stands as Africa's largest glass container production site and ranks among the world's most extensive and efficient facilities.

- Additionally, the rising consumption of alcoholic beverages in South Africa plays a crucial role in driving this demand. Data from IWSR, a London-based information services firm, highlighted a 9% surge in beer consumption in South Africa for 2023. This increase is linked to rapid urban expansion and younger populations migrating to major cities, enhancing accessibility to alcoholic beverages.

- Moreover, Statistics South Africa indicates that the Consumer Price Index (CPI) for alcoholic beverages and tobacco rose from 111.1 in September 2023 to 115.7 in July 2024. This uptick in beverage prices, coupled with average demand across the nation, underscores the growing appetite for container glass.

- Increased consumer spending in South African restaurants and cafes has spurred demand for container glass products, including bottles and bowls. Statistics South Africa notes a rise in food sales from restaurants and coffee shops, jumping from USD 143.87 million in January 2024 to USD 156.04 million in March 2024.

Middle East and Africa Glass Bottles Market Leaders

The container glass market is characterized by intense competition and moderate consolidation in the Middle East and Africa. Key players compete in domestic and international arenas to capture a larger market share, including RAK Ghani Glass LLC, Isanti Glass, Ardagh Group SA, and East Glass Manufacturing Company. These companies are pursuing strategies such as new product development, expansion, and mergers and acquisitions to enhance product functionality and broaden their geographic presence in Middle Eastern nations.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Import Export Trade Data of Container Glass

- 4.3 PESTLE Analysis

- 4.4 Industry Standards and Regulations for Container Glass Use for Packaging

- 4.5 Sustainability Trends for Packaging

- 4.6 Container Glass Furnace Capacity and Location In Middle East & Africa

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rising Consumption of Variety of Food and Beverages in the Region

- 5.1.2 Growing Demand of Glass Containers in the Pharmaceutical Industry

- 5.2 Market Restraint

- 5.2.1 Demand of Plastic Packaging Over Glass Can Hamper Market Growth

- 5.3 Trade Scenerio: Analysis of the Historical and Current Export Import Paradigm for Container Glass Industry in Middle East

6 MARKET SEGMENTATION

- 6.1 By End-user Industry

- 6.1.1 Beverages

- 6.1.1.1 Alcoholic Beverages (Qualitative Analysis to be Provided)

- 6.1.1.1.1 Wins and Spirits

- 6.1.1.1.2 Beer and Cider

- 6.1.1.1.3 Other Alcoholic-Beverages

- 6.1.1.2 Non-alcoholic Beverages (Qualitative Analysis to be Provided)

- 6.1.1.2.1 Carbonated Drinks

- 6.1.1.2.2 Juices

- 6.1.1.2.3 Water

- 6.1.1.2.4 Dairy-Based

- 6.1.1.2.5 Flavored Drinks

- 6.1.1.2.6 Other Non-Alcoholic Drinks

- 6.1.2 Food

- 6.1.3 Cosmetics

- 6.1.4 Pharmaceutical (Excluding Vials and Ampoules)

- 6.1.5 Other End-user Industries

- 6.1.1 Beverages

- 6.2 By Country

- 6.2.1 United Arab Emirates

- 6.2.2 Saudi Arabia

- 6.2.3 Egypt

- 6.2.4 South Africa

- 6.2.5 Nigeria

- 6.2.6 Kuwait

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 RAK Ghani Glass LLC

- 7.1.2 Isanti Glass

- 7.1.3 Ardagh Group SA

- 7.1.4 Saudi Arabian Glass Company Ltd

- 7.1.5 Middle East Glass Manufacturing Company

- 7.1.6 Altajir Glass Industries

- 7.1.7 Nafis Glass

- 7.1.8 Mahmood Saeed Glass Industry Co.