|

시장보고서

상품코드

1639413

열 스프레이 재료 시장 전망 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Thermal Spray Materials - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

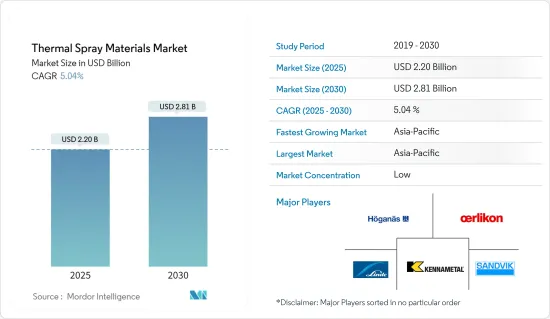

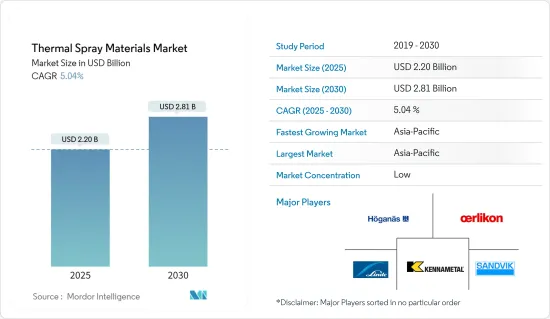

열 스프레이 재료 시장 규모는 2025년에 22억 달러로 추정되며, 예측기간(2025-2030년)의 연평균 성장율(CAGR)은 5.04%로, 2030년에는 28억 1,000만 달러에 달할 것으로 예측됩니다.

COVID-19는 2020년과 2021년 상반기에 시장에 부정적인 영향을 미쳤습니다. 바이러스 확산을 억제하기 위해 모든 제조 및 기타 활동이 보류되면서 시장에 부정적인 영향을 미쳤습니다. 그러나 팬데믹이 진정된 이후에는 제조 활동이 증가하고 최종 사용자 산업이 거의 정상적으로 가동되면서 수요가 회복됨에 따라 시장이 꾸준히 성장할 것으로 예상됩니다.

주요 하이라이트

- 본 시장은 의료 기기 제조에서 열 스프레이 코팅의 사용 증가, 열 스프레이 세라믹 코팅의 인기 상승, 부식 방지 애플리케이션에서의 광범위한 소비, 아시아 태평양 풍력 부문의 발전이 있습니다.

- 반면 대체품의 출현은 시장 성장을 방해할 것으로 예상됩니다.

- 서멧의 용액 전구체 플라즈마 분사, 열 스프레이 가공 재료의 재활용, 환경 차단 코팅(EBC) 열 스프레이 분말의 산업 규모 생산, 석유 및 가스 산업의 성장 전망은 향후 시장을 주도할 것으로 예상되는 중요한 기회입니다.

- 아시아태평양은 중국과 인도와 같은 경제가 크게 성장하고 있기 때문에 예측 기간 동안 시장을 독점할 것으로 예상됩니다.

열 스프레이 재료 시장 동향

시장을 독점하는 항공우주산업

- 열 스프레이 재료는 항공 우주 부문에서 광범위하게 사용됩니다. 항공기 전체의 다양한 부품에 적용되는 코팅을 제조하는 데 사용됩니다. 이러한 코팅은 부품 수명을 늘려 유지보수 비용을 절감하고 연료 효율을 높입니다.

- 산화 지르코늄, 알루미늄 청동, 코발트-몰리브덴과 같은 열 스프레이 재료는 각각 로켓 연소실, 압축기 에어 씰, 고압 노즐의 코팅 용도로 사용됩니다.

- 항공기 엔진에는 마모, 고온 부식, 프레팅, 입자 침식 등으로 인해 다양한 성능 저하 문제가 존재합니다. 이러한 성능 저하는 고온이 수반될 때 가속화됩니다. 열 스프레이 재료는 엔진 부품의 수명을 늘리는 데 필요한 표면 조건을 제공합니다.

- 전 세계 군사 및 항공우주 제조 시장에는 보잉, 록히드, 노스롭 그루먼과 같은 주요 기업이 있습니다. 국제 민간 항공기구에서 발표한 보고서에 따르면, 경제 개방으로 인해 팬데믹 이후 기간 동안 상업 항공사의 수익이 크게 증가했습니다. 2021년에는 최대 4억 7,200만 달러에 달했으며 2022년 말에는 6억 5,800만 달러로 무려 39% 증가할 것으로 예상됩니다.

- 항공우주 인프라 건설 및 신규 프로젝트 시운전에 대한 높은 지출로 인해 항공우주 부문, 특히 신흥 경제국의 민간 항공 분야의 성장이 시장 성장을 견인할 것으로 예상됩니다. 예를 들어, 인도에서는 2021년 3월 정부가 민간항공부의 UDAN-RCS 산하의 우자인 댐에 수상 비행장 프로젝트를 개발하는 제안서를 제출했습니다.

- 따라서 위에서 언급한 장점으로 인해 열 스프레이 재료의 채택이 증가하면 항공 우주 산업에서 수요가 증가할 것으로 예상됩니다.

아시아태평양이 시장을 독점

- 열 스프레이 재료는 항공 우주 산업에서 보호 코팅으로 사용됩니다. 중국은 가장 큰 항공기 제조업체 중 하나이며 국내 항공 승객이 가장 많은 시장 중 하나입니다.

- 큰 시장 규모, 정부 지원 확대, 온라인을 통한 전기 자동차 예약 기능 등의 요인이 중국 내 전기 자동차 수요를 촉진할 것으로 보입니다.

- 중국의 항공 산업은 지난 몇 년간 크게 감소한 후 2022년에 수익성을 회복할 것으로 예상됩니다. 또한 중국민용항공국(CAAC)은 항공 부문이 국내 교통량을 팬데믹 이전 수준의 약 85%까지 회복할 것으로 예상했습니다.

- 또한 중국 항공사들은 향후 20년간 약 1조 2,000억 달러에 달하는 약 7,690대의 신규 항공기 구매를 계획하고 있어 열 스프레이 소재에 대한 수요가 증가할 것으로 예상됩니다. 보잉 상용 전망 2021-2040에 따르면 2040년까지 중국에서 약 8,700대의 신규 납품이 이루어질 것이며, 시장 서비스 가치는 1,800억 달러에 달할 것으로 예상됩니다.

- 2021년 12월, 중국은 향후 15년 동안 4,400억 달러를 투자하여 최소 150기의 신규 원자로를 건설할 계획입니다. 현재 건설 중인 원자로는 19기, 허가 대기 중인 원자로는 43기, 그리고 이미 발표된 원자로는 166기에 달합니다. 이 228개의 원자로를 합치면 총 용량은 246GW입니다.

- 인도 정부는 중공업부 산하 생산연계 인센티브 제도를 통해 자동차 및 자동차 부품 부문에 78억 달러를 지원할 계획입니다. 따라서 자동차 생산량 증가에 따른 자동차 부문의 확장은 예측 기간 동안 시장의 성장을 주도 할 것으로 예상됩니다.

- 이러한 개발은 아시아태평양이 예측 기간 동안 시장을 독점할 것으로 예상됩니다.

열 스프레이 재료 산업 개요

열 스프레이 재료 시장은 그 특성상 부분적으로 단편화됩니다. 시장의 주요 기업(특정한 순서 없음)에는 Hoganas AB, OC Oerlikon Management AG, Kennametal Inc., Sandvik AB, Linde PLC 등이 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 성장 촉진요인

- 의료기기 제조에 있어서의 열 스프레이 코팅의 용도 확대

- 열 스프레이 세라믹 코팅 수요 증가

- 방청 용도로의 광범위한 소비

- 아시아태평양의 풍력 발전 부문의 발전

- 억제요인

- 대체품의 출현

- 산업 밸류체인 분석

- Porter's Five Forces 분석

- 공급기업의 협상력

- 소비자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 세분화

- 제품 유형별

- 코팅재료

- 분말

- 세라믹

- 세라믹 산화물

- 알루미나

- 티타니아

- 지르코니아

- 크로미아 및 기타 세라믹 산화물

- 탄화물(서멧 포함)

- 탄화 크롬

- 텅스텐 카바이드

- 금속

- 순금속 및 합금

- 귀금속

- MCrAlY

- 폴리머 및 기타 코팅재료

- 와이어, 로드

- 기타 코팅재(액체)

- 부자재(보조재료)

- 코팅재료

- 프로세스 유형별

- 연소

- 전기 에너지

- 최종 사용자 산업별

- 항공우주

- 산업용 가스 터빈

- 자동차

- 전자

- 석유 및 가스

- 의료기기

- 에너지 및 전력

- 기타 최종 사용자 산업

- 지역별

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- ASEAN 국가

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- M&A, 합작사업, 제휴, 협정

- 시장 랭킹 분석

- 주요 기업의 전략

- 기업 프로파일

- Aisher APM LLC

- Ametek Inc.

- Aimtek Inc.

- C&M Technologies GmbH

- Castolin Eutectic

- CenterLine(Windsor)Limited

- CRS Holdings Inc.

- Fisher Barton

- Global Tungsten & Powders Corp.

- HAI Inc.

- HC Starck GmbH

- Hoganas AB

- Hunter Chemical LLC

- Kennametal Stellite

- Linde PLC

- LSN Diffusion Ltd

- Metallisation Limited

- Metallizing Equipment Co. Pvt. Ltd

- OC Oerlikon Management AG

- Polymet Corporation

- Powder Alloy Corporation

- Saint-Gobain

- Sandvik AB

- Thermion

제7장 시장 기회와 앞으로의 동향

- 서멧의 용액 전구체 플라즈마 열 스프레이의 현재의 진전

- 열 스프레이재료의 재활용

- 환경 배리어 코팅(EBC) 열 스프레이 분말의 공업규모 생산

- 석유 및 가스 산업의 성장 전망

The Thermal Spray Materials Market size is estimated at USD 2.20 billion in 2025, and is expected to reach USD 2.81 billion by 2030, at a CAGR of 5.04% during the forecast period (2025-2030).

COVID-19 negatively impacted the market in 2020 and the first half of 2021. All the manufacturing and other activities were put on hold to curb the spreading of the virus, thereby negatively affecting the market. However, the market is projected to grow steadily post the retraction of the pandemic, owing to increased manufacturing and reinstating demand from the end-user industries, which have become operational at almost full scale.

Key Highlights

- The studied market's significant factors include the increasing usage of thermal spray coating in medical device manufacturing, the rising popularity of thermal spray ceramic coatings, extensive consumption in anti-corrosion applications, and evolution in the Asia-Pacific wind power sector.

- On the other hand, the emergence of alternate substitutes is expected to hinder the market's growth.

- The ongoing progress in solution precursor plasma spraying of cermets, recycling of thermal spray processing materials, industrial-scale production of environmental barrier coatings (EBC) thermal spray powders, and growth prospects in the oil and gas industry are the significant opportunities expected to drive the market in the future.

- Asia-Pacific region is expected to dominate the market in the forecast period because of vastly growing economies such as China and India.

Thermal Spray Materials Market Trends

Aerospace Industry to Dominate the Market

- Thermal spray materials are extensively used in the aerospace sector. They are used in manufacturing coatings, which are applied to various parts throughout the aircraft. These coatings offer component longevity, thus, reducing maintenance costs and increasing fuel efficiency.

- Thermal spray materials, such as zirconium oxide, aluminum bronze, and cobalt-molybdenum, are used for coating purposes in rocket combustion chambers, compressor air seals, and high-pressure nozzles, respectively.

- Various degradation problems exist in aircraft engines due to wear, hot corrosion, fretting, particle erosion, and many more. This degradation is accelerated when high temperatures are involved. Thermal spray material imparts the surface conditions required to increase engine components' service life.

- The global military and aerospace manufacturing market include dominant players such as Boeing, Lockheed, and Northrop Grumman. As per the report published by International Civil Aviation Organisation, commercial airlines' revenue grew significantly during the post-pandemic period because of the opening up of economies. It reached up to USD 472 million in 2021 and is forecasted to gain a whopping 39% standing at USD 658 million by the end of 2022.

- Growth in the aerospace sector, especially in civil aviation in emerging economies, on account of high expenditure on aerospace infrastructural construction and commissioning new projects, is expected to drive the market's growth. For instance, in India, in March 2021, the government submitted a proposal to develop a water aerodrome project at the Ujjain Dam under the Ministry of Civil Aviation's UDAN-RCS.

- Thus, increasing the adoption of thermal spray material due to its advantages mentioned above is expected to boost its demand in the aerospace industry.

Asia-Pacific to Dominate the Market

- Thermal spray materials are used in the aerospace industry as protective coating. China is one of the largest aircraft manufacturers and one of the largest markets for domestic air passengers.

- Factors such as large market size, increasing government support, and the ability to book electric vehicles online are likely to fuel the demand for electric vehicles in the country.

- China's aerospace industry is projected to return to profitability in 2022 after facing a significant decline in the previous years. In addition, the Civil Aviation Administration of China (CAAC) has estimated the aviation sector to recover domestic traffic to around 85% of pre-pandemic levels.

- Moreover, Chinese airline companies are planning to purchase about 7,690 new aircraft in the next 20 years, valued at approximately USD 1.2 trillion, expected to drive the demand for thermal spray materials. According to the Boeing Commercial Outlook 2021-2040, around 8,700 new deliveries will be made in China by 2040, with a market service value of USD 1,800 billion.

- In December 2021, China planned to build at least 150 new nuclear reactors in the next 15 years with an investment of USD 440 billion. The country has 19 reactors under construction, 43 reactors awaiting permits, and a massive 166 reactors that have been announced. The combined capacity of these 228 reactors is 246GW.

- The Government of India has planned to give USD 7.8 billion to the automobile and auto components sector in production-linked incentive schemes under the Department of Heavy Industries. Thus, the expansion of the automotive sector with the growing production of automobiles is anticipated to drive the market's growth over the forecast period.

- Owing to these developments, Asia-Pacific is expected to dominate the market over the forecast period.

Thermal Spray Materials Industry Overview

The thermal spray materials market is partially fragmented in nature. Some of the major players in the market (in no particular order) include Hoganas AB, OC Oerlikon Management AG, Kennametal Inc., Sandvik AB, and Linde PLC.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Usage of Thermal Spray Coating in Medical Device Manufacturing

- 4.1.2 Rising Demand of Thermal Spray Ceramic Coatings

- 4.1.3 Extensive Consumption in Anti-corrosion Applications

- 4.1.4 Evolution in the Asia-Pacific Wind Power Sector

- 4.2 Restraints

- 4.2.1 Emergence of Alternate Substitutes

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Product Type

- 5.1.1 Coating Materials

- 5.1.1.1 Powders

- 5.1.1.1.1 Ceramics

- 5.1.1.1.1.1 Ceramic Oxides

- 5.1.1.1.1.1.1 Alumina

- 5.1.1.1.1.1.2 Titania

- 5.1.1.1.1.1.3 Zirconia

- 5.1.1.1.1.1.4 Chromia and Other Ceramic Oxides

- 5.1.1.1.1.2 Carbides (including Cermets)

- 5.1.1.1.1.2.1 Chromium Carbides

- 5.1.1.1.1.2.2 Tungsten Carbides

- 5.1.1.1.2 Metals

- 5.1.1.1.2.1 Pure Metal and Alloys

- 5.1.1.1.2.2 Precious Metals

- 5.1.1.1.2.3 MCrAlY

- 5.1.1.1.3 Polymer and Other Coating Materials

- 5.1.1.2 Wires/Rods

- 5.1.1.3 Other Coating Materials (Liquid)

- 5.1.2 Supplementary Materials (Auxiliary Materials)

- 5.1.1 Coating Materials

- 5.2 Process Type

- 5.2.1 Combustion

- 5.2.2 Electric Energy

- 5.3 End-user Industry

- 5.3.1 Aerospace

- 5.3.2 Industrial Gas Turbines

- 5.3.3 Automotive

- 5.3.4 Electronics

- 5.3.5 Oil and Gas

- 5.3.6 Medical Devices

- 5.3.7 Energy and Power

- 5.3.8 Other End-user Industries

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Aisher APM LLC

- 6.4.2 Ametek Inc.

- 6.4.3 Aimtek Inc.

- 6.4.4 C&M Technologies GmbH

- 6.4.5 Castolin Eutectic

- 6.4.6 CenterLine (Windsor) Limited

- 6.4.7 CRS Holdings Inc.

- 6.4.8 Fisher Barton

- 6.4.9 Global Tungsten & Powders Corp.

- 6.4.10 HAI Inc.

- 6.4.11 HC Starck GmbH

- 6.4.12 Hoganas AB

- 6.4.13 Hunter Chemical LLC

- 6.4.14 Kennametal Stellite

- 6.4.15 Linde PLC

- 6.4.16 LSN Diffusion Ltd

- 6.4.17 Metallisation Limited

- 6.4.18 Metallizing Equipment Co. Pvt. Ltd

- 6.4.19 OC Oerlikon Management AG

- 6.4.20 Polymet Corporation

- 6.4.21 Powder Alloy Corporation

- 6.4.22 Saint-Gobain

- 6.4.23 Sandvik AB

- 6.4.24 Thermion

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Current Progress in Solution Precursor Plasma Spraying of Cermets

- 7.2 Recycling of Thermal Spray Processing Materials

- 7.3 Industrial Scale Production of Environmental Barrier Coatings (EBC) Thermal Spray Powders

- 7.4 Growth Prospects in the Oil and Gas Industry