|

시장보고서

상품코드

1640491

용사 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Thermal Spray - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

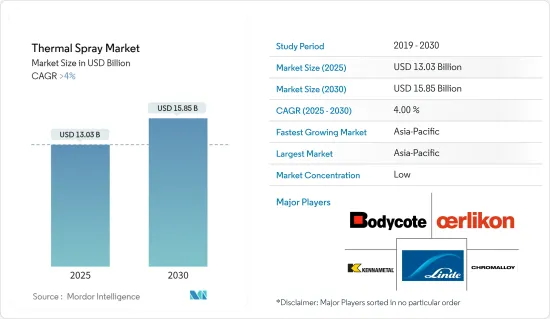

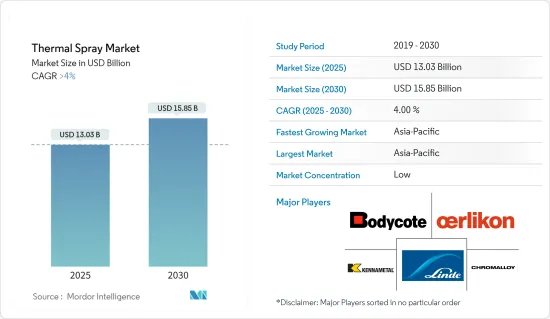

용사 시장 규모는 2025년에 130억 3,000만 달러로 추계되며 예측기간 중(2025-2030년) CAGR은 4%를 넘어 2030년에는 158억 5,000만 달러에 달할 것으로 예측됩니다.

용사 시장은 COVID-19의 유행에 의해 부정적인 영향을 받았으며 초기에는 운영 정지와 공급망의 혼란으로 인해 제조 활동이 둔화되어 용사 코팅 수요가 일시적으로 감소했습니다. 그러나 산업계가 새로운 규범을 채택하고 위생과 보호를 중시하게 되면서 헬스케어, 자동차, 항공우주 등의 산업에서 용사 코팅 수요가 확대되었습니다.

주요 하이라이트

- 세라믹 용사 코팅을 의료기기에 사용함으로써 용사 코팅의 인기가 높아지고 있으며 항공우주 산업 분야 사용 증가와 경질 크롬 코팅을 대체하는 용사 코팅의 특성은 용사 시장 수요를 촉진하는 요인 중 하나입니다.

- 그러나 공정의 신뢰성과 일관성에 대한 과제와 최근 몇 년 사이 경질 3가 크롬 코팅의 출현은 시장 성장을 방해할 가능성이 높습니다.

- 석유 및 가스 산업의 용사 수요 증가, 용사 처리 재료의 재활용, 용사 기술(콜드 스프레이 프로세스)의 진보는 향후 수년간 시장에 유리한 성장 기회를 가져올 것으로 예상됩니다.

- 예측 기간 동안 아시아태평양은 용사 시장을 독점할 것으로 예상됩니다.

용사 시장 동향

항공우주산업이 시장을 독점할 전망

- 항공우주 부품은 고온, 부식성 화학물질, 극단적인 기상 조건 등 가혹한 환경에 노출되는 경우가 많습니다. 용사 코팅은 효과적인 부식 장벽을 제공하여 터빈 블레이드, 엔진 부품, 기체와 같은 중요한 부품의 수명을 연장합니다.

- 용사 코팅은 항공우주 부품에 경량화 솔루션을 제공하여 연비 효율과 전체 항공기 성능 향상에 기여합니다. 특성을 조정한 코팅은 구조적 무결성을 유지하면서 더 무거운 재료를 대체할 수 있습니다.

- 항공우주산업은 빠른 기술 진보와 혁신 속에 있으며 이는 항공기 제조의 호황을 창출하고 있습니다. Boeing Commercial Outlook 2023-2042에 따르면 국제선 이용이 부활하고 국내선 이용이 팬데믹 전 수준으로 회복되고 있기 때문에 Boeing은 2042년까지 48,575기의 새로운 민간 제트기의 세계 시장 수요를 예측했습니다.

- 국제항공여객협회에 따르면 2023년 8월 국내선 민간항공기 여객 수송량은 팬데믹 전보다 9.2% 증가했습니다. 항공 수송량 증가는 민간 항공기 수요를 증가시키고 예측 기간 동안 접착제 수요를 촉진할 수 있습니다.

- 세계 주요 항공기 제조업체인 Airbus는 2023년 735대의 민간항공기를 납품하였고 이는 전년대비 11% 증가한 수치입니다.

- 위의 요인은 예측 기간 동안 항공우주 산업에서 용사 수요를 높일 것으로 예상됩니다.

아시아태평양이 시장을 독점

- 아시아태평양은 특히 중국, 인도, 일본, 한국 등의 국가에서 빠른 산업화가 진행되고 있습니다. 자동차, 항공우주, 일렉트로닉스, 에너지 산업 등 조사 지역의 제조업은 활황을 보이고 있으며, 부품의 성능과 내구성을 향상시키는 용사 코팅 수요가 크게 늘고 있습니다.

- 아시아태평양 정부는 운송, 에너지, 건설 등의 인프라 프로젝트에 많은 투자를 하고 있습니다. 용사 코팅은 중요한 인프라 부품을 부식, 마모, 침식으로부터 보호하여 수명을 연장하고 유지 보수 비용을 절감합니다.

- 중국은 세계 최대의 항공기 제조업체 중 하나이며 중국 민용 항공국의 발표에 따르면 국내선 항공 여객 시장이기도 합니다. 또한 소형 항공기 부품 제조업체가 200개 이상 존재하여 부품 및 조립 산업이 급성장하고 있습니다.

- 중국은 세계 최대의 전자 기기 제조 기지입니다. 스마트폰, TV, 케이블, 모바일 컴퓨터, 게임기, 기타 가전제품 등의 전자제품은 중국에서 활발하게 생산되고 있습니다. CEIC에 따르면 2023년 12월 중국 전자제품의 수출액은 216억 3,000만 달러였습니다.

- 2023년 한국은 해외로부터 총액 188억 달러의 투자를 받았으며 이는 전년 대비 3.4% 증가한 수치입니다. 특히 전자산업은 투자 중 가장 큰 점유율을 차지하며, 세부 산업 중 가장 많은 30억 달러가 할당되었습니다.

- 중국은 세계 최대의 철강 생산국 중 하나입니다. 공식 발표에 따르면 2023년 연초 11개월간의 1차 철강 생산량은 9억 5,214만 톤에 달하고, 전년 동기 대비 1.5% 증가했습니다.

- 인도의 자동차 산업은 기술 발전과 거시 경제 확대에 중요한 역할을 하고 있습니다. 인도자동차공업회(SIAM)에 따르면 2023년 4월부터 2024년 3월까지 자동차 판매량은 2,385만 3,463대에 이르렀으며, 2023년도 같은 시기의 2,120만 4,846대에서 12.5% 증가했습니다.

- 위의 요인들로부터 예측 기간 동안 조사 지역은 시장을 독점할 것으로 예상됩니다.

용사 산업 개요

용사 시장은 세분화되어 있습니다. 주요 기업(순서부동)으로는 OC Oerlikon Management AG, Linde PLC(Praxair ST Technologies Inc.), Chromalloy Gas Turbine LLC, Bodycote, Kennametal Inc. 등이 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 촉진요인

- 의료기기 분야 용사 코팅 용도 확대

- 용사 세라믹 코팅의 인기 상승

- 경질 크롬 피막을 대체하는 특성

- 항공우주산업 분야 용사 코팅 사용 증가

- 억제요인

- 경질 3가 크롬 코팅의 출현

- 프로세스의 신뢰성과 일관성 과제

- 업계 밸류체인 분석

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 진입업자의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 세분화(금액 기준 시장 규모)

- 제품 유형별

- 코팅재료

- 분말

- 세라믹

- 금속

- 폴리머 및 기타 파우더

- 와이어/로드

- 기타 코팅 재료(보조 재료)

- 용사장치

- 용사 시스템

- 집진장치

- 스프레이건과 노즐

- 공급장치

- 예비 부품

- 방음 커버

- 기타 용사 장치

- 용사 코팅과 마무리

- 연소

- 전기 에너지

- 코팅재료

- 최종 사용자 산업별

- 항공우주

- 산업용 가스 터빈

- 자동차

- 일렉트로닉스

- 석유 및 가스

- 의료기기

- 에너지 및 전력

- 제철

- 섬유

- 인쇄 및 제지

- 지역별

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 말레이시아

- 태국

- 인도네시아

- 베트남

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 터키

- 러시아

- 북유럽

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 콜롬비아

- 기타 남미

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 나이지리아

- 이집트

- 카타르

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- M&A, 합작사업, 제휴, 협정

- 시장 점유율(%)**/순위 분석

- 주요 기업의 전략

- 기업 프로파일

- Thermal Spray Material Companies

- Aimtek Inc.

- AISher APM LLC

- AMETEK Inc.

- C&M Technologies GmbH

- CASTOLIN EUTECTIC

- CenterLine(Windsor) Limited(Supersonic Spray Technologies Division)

- CRS Holdings LLC

- Fisher Barton

- Global Tungsten & Powders

- HC Starck Inc.

- HAI Inc

- Hoganas AB

- Hunter Chemical LLC

- Kennametal Inc.

- Linde PLC(Praxair ST Technologies Inc.)

- LSN Diffusion Limited

- Metallisation Limited

- Metallizing Equipment Co. Pvt. Ltd

- OC Oerlikon Management AG

- Polymet

- Powder Alloy Corporation

- Saint-Gobain

- Sandvik AB

- Thermion

- Thermal Spray Coatings Companies

- APS Materials Inc.

- Bodycote

- Chromalloy Gas Turbine LLC

- Curtiss-Wright Corporation(FW Gartner)

- Fisher Barton

- FM Industries

- Hannecard Roller Coatings, Inc(ASB Industries Inc.)

- Lincotek Trento SpA

- Linde PLC(Praxair ST Technologies Inc.)

- OC Oerlikon Management AG

- Thermion

- TOCALO Co. Ltd

- Thermal Spray Equipment Companies

- Air Products and Chemicals Inc.

- Arzell Inc.

- ASB Industries Inc.(Hannecard Roller Coatings Inc.)

- Bay State Surface Technologies Inc.(Aimtek Inc.)

- Camfil Air Pollution Control(APC)

- CASTOLIN EUTECTIC

- Centerline(Windsor) Ltd(SUPERSONIC SPRAY TECHNOLOGIES)

- Donaldson Company Inc.

- Flame Spray Technologies BV

- GTV Verschleibschutz GmbH

- HAI Inc.

- Imperial Systems Inc.

- Kennametal Inc.

- Lincotek Equipment SpA

- Linde PLC(Praxair ST Technologies Inc.)

- Metallisation Limited

- Metallizing Equipment Co. Pvt. Ltd

- OC Oerlikon Management AG

- Plasma Powders

- Powder Feed Dynamics Inc.

- Progressive Surface

- Saint-Gobain

- Thermion

- Thermal Spray Material Companies

제7장 시장 기회와 앞으로의 동향

- 용사 기술의 진보(콜드 스프레이 공정)

- 용사 재료의 재활용

- 석유 및 가스 산업 분야 수요 증가

The Thermal Spray Market size is estimated at USD 13.03 billion in 2025, and is expected to reach USD 15.85 billion by 2030, at a CAGR of greater than 4% during the forecast period (2025-2030).

The thermal spray market was negatively affected by the COVID-19 pandemic. Initially, there was a slowdown in manufacturing activities due to lockdowns and supply chain disruptions, leading to a temporary decrease in demand for thermal spray coatings. However, as industries adopted new norms and increased their emphasis on hygiene and protection, there was a growing demand for thermal spray coatings in industries such as healthcare, automotive, and aerospace.

Key Highlights

- The increasing popularity of thermal spray ceramic coatings due to their usage in medical devices, the rising use of thermal spray coatings in the aerospace industry, and the replacement of hard chrome coatings are some factors driving the demand for the thermal spray market.

- However, issues regarding process reliability and consistency and the emergence of hard trivalent chrome coatings in recent years are likely to hinder the market's growth.

- The increasing demand for thermal spray from the oil and gas industry, recycling of thermal spray processing materials, and advancements in spraying technology (cold spray process) are expected to provide lucrative growth opportunities for the market in the coming years.

- Asia-Pacific is expected to dominate the thermal spray market over the forecast period.

Thermal Spray Market Trends

The Aerospace Industry is Expected to Dominate the Market

- Aerospace components are often exposed to harsh environments, including high temperatures, corrosive chemicals, and extreme weather conditions. Thermal spray coatings provide an effective barrier against corrosion, extending the lifespan of critical components such as turbine blades, engine parts, and airframes.

- Thermal spray coatings offer lightweight solutions for aerospace components, contributing to fuel efficiency and overall aircraft performance. Coatings with tailored properties can replace heavier materials while maintaining structural integrity.

- The aerospace industry is undergoing rapid technological advancements and innovation, creating upswings for aircraft manufacturing. According to the Boeing Commercial Outlook 2023-2042, with a resurgence in international traffic and domestic air travel back to pre-pandemic levels, the company has projected global demand for 48,575 new commercial jets by 2042.

- According to the International Air Travel Association, domestic commercial aircraft passenger traffic increased by 9.2% over the pre-pandemic timeline in August 2023. Increased air traffic may raise the demand for commercial aircraft and propel the demand for adhesives during the forecast period.

- Airbus, a major aircraft manufacturer worldwide, delivered 735 commercial aircraft in 2023, an increase of 11% compared to the previous year.

- The factors mentioned above are expected to boost the demand for thermal spray in the aerospace industry during the forecast period.

Asia-Pacific to Dominate the Market

- Asia-Pacific is experiencing rapid industrialization, particularly in countries like China, India, Japan, and South Korea. The region's booming manufacturing sector, including the automotive, aerospace, electronics, and energy industries, is driving significant demand for thermal spray coatings to enhance component performance and durability.

- Governments in Asia-Pacific are investing heavily in infrastructure projects, including transportation, energy, and construction. Thermal spray coatings protect critical infrastructure components from corrosion, wear, and erosion, thereby extending their lifespan and reducing maintenance costs.

- China is one of the world's biggest aircraft manufacturers and a market for domestic air passengers, as stated by the Chinese Civil Aviation Administration. In addition, with more than 200 small aircraft component manufacturers, there has been rapid growth in the parts and assembly industry.

- China is the largest electronics manufacturing base in the world. Electronic products such as smartphones, televisions, cables, mobile computers, gaming systems, and other consumer electronic equipment are being produced in China on an active basis. According to the CEIC, in December 2023, the export value of Chinese electronics products was USD 21.63 billion.

- In 2023, South Korea received a total of USD 18.8 billion in investments from abroad, marking a 3.4% increase from the previous year. Specifically, the electronics industry saw the largest share of this investment, with USD 3 billion allocated, standing out as the top sub-industry.

- China is one of the largest producers of steel globally. According to official figures, the nation's primary steel production reached 952.14 million tons during the initial 11 months of 2023, marking a 1.5% increase compared to the same period in the previous year.

- The automotive industry in India plays a crucial role in technological advancements and macroeconomic expansion. According to the Society of Indian Automobile Manufacturers (SIAM), the number of vehicles sold from April 2023 to March 2024 reached 23,853,463, marking an increase of 12.5% from the 21,204,846 units sold in the same timeframe during FY 2023.

- Due to the above-mentioned factors, the region is projected to dominate the market during the forecast period.

Thermal Spray Industry Overview

The thermal spray market is fragmented in nature. The major players (not in any particular order) include OC Oerlikon Management AG, Linde PLC (Praxair ST Technologies Inc.), Chromalloy Gas Turbine LLC, Bodycote, and Kennametal Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Usage of Thermal Spray Coatings in Medical Devices

- 4.1.2 Rising Popularity of Thermal Spray Ceramic Coatings

- 4.1.3 Replacement of Hard Chrome Coating

- 4.1.4 Rising Use of Thermal Spray Coatings in the Aerospace Industry

- 4.2 Restraints

- 4.2.1 Emergence of Hard Trivalent Chrome Coatings

- 4.2.2 Issues Regarding Process Reliability and Consistency

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Product Type

- 5.1.1 Coatings Materials

- 5.1.1.1 Powders

- 5.1.1.1.1 Ceramics

- 5.1.1.1.2 Metal

- 5.1.1.1.3 Polymers and Other Powders

- 5.1.1.2 Wires/Rods

- 5.1.1.3 Other Coating Materials (Auxiliary Material)

- 5.1.2 Thermal Spray Equipment

- 5.1.2.1 Thermal Spray Coating System

- 5.1.2.2 Dust Collection Equipment

- 5.1.2.3 Spray Gun and Nozzle

- 5.1.2.4 Feeder Equipment

- 5.1.2.5 Spare Parts

- 5.1.2.6 Noise-reducing Enclosures

- 5.1.2.7 Other Thermal Spray Equipment

- 5.1.1 Coatings Materials

- 5.2 Thermal Spray Coatings and Finishes

- 5.2.1 Combustion

- 5.2.2 Electric Energy

- 5.3 End-user Industry

- 5.3.1 Aerospace

- 5.3.2 Industrial Gas Turbines

- 5.3.3 Automotive

- 5.3.4 Electronics

- 5.3.5 Oil and Gas

- 5.3.6 Medical Devices

- 5.3.7 Energy and Power

- 5.3.8 Steel Making

- 5.3.9 Textile

- 5.3.10 Printing and Paper

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Malaysia

- 5.4.1.6 Thailand

- 5.4.1.7 Indonesia

- 5.4.1.8 Vietnam

- 5.4.1.9 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Turkey

- 5.4.3.7 Russia

- 5.4.3.8 NORDIC

- 5.4.3.9 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 South Africa

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 Nigeria

- 5.4.5.4 Egypt

- 5.4.5.5 Qatar

- 5.4.5.6 United Arab Emirates

- 5.4.5.7 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Thermal Spray Material Companies

- 6.4.1.1 Aimtek Inc.

- 6.4.1.2 AISher APM LLC

- 6.4.1.3 AMETEK Inc.

- 6.4.1.4 C&M Technologies GmbH

- 6.4.1.5 CASTOLIN EUTECTIC

- 6.4.1.6 CenterLine (Windsor) Limited (Supersonic Spray Technologies Division)

- 6.4.1.7 CRS Holdings LLC

- 6.4.1.8 Fisher Barton

- 6.4.1.9 Global Tungsten & Powders

- 6.4.1.10 H.C. Starck Inc.

- 6.4.1.11 HAI Inc

- 6.4.1.12 Hoganas AB

- 6.4.1.13 Hunter Chemical LLC

- 6.4.1.14 Kennametal Inc.

- 6.4.1.15 Linde PLC (Praxair ST Technologies Inc.)

- 6.4.1.16 LSN Diffusion Limited

- 6.4.1.17 Metallisation Limited

- 6.4.1.18 Metallizing Equipment Co. Pvt. Ltd

- 6.4.1.19 OC Oerlikon Management AG

- 6.4.1.20 Polymet

- 6.4.1.21 Powder Alloy Corporation

- 6.4.1.22 Saint-Gobain

- 6.4.1.23 Sandvik AB

- 6.4.1.24 Thermion

- 6.4.2 Thermal Spray Coatings Companies

- 6.4.2.1 APS Materials Inc.

- 6.4.2.2 Bodycote

- 6.4.2.3 Chromalloy Gas Turbine LLC

- 6.4.2.4 Curtiss-Wright Corporation (FW Gartner)

- 6.4.2.5 Fisher Barton

- 6.4.2.6 FM Industries

- 6.4.2.7 Hannecard Roller Coatings, Inc (ASB Industries Inc.)

- 6.4.2.8 Lincotek Trento SpA

- 6.4.2.9 Linde PLC (Praxair ST Technologies Inc.)

- 6.4.2.10 OC Oerlikon Management AG

- 6.4.2.11 Thermion

- 6.4.2.12 TOCALO Co. Ltd

- 6.4.3 Thermal Spray Equipment Companies

- 6.4.3.1 Air Products and Chemicals Inc.

- 6.4.3.2 Arzell Inc.

- 6.4.3.3 ASB Industries Inc. (Hannecard Roller Coatings Inc.)

- 6.4.3.4 Bay State Surface Technologies Inc. (Aimtek Inc.)

- 6.4.3.5 Camfil Air Pollution Control (APC)

- 6.4.3.6 CASTOLIN EUTECTIC

- 6.4.3.7 Centerline (Windsor) Ltd (SUPERSONIC SPRAY TECHNOLOGIES)

- 6.4.3.8 Donaldson Company Inc.

- 6.4.3.9 Flame Spray Technologies BV

- 6.4.3.10 GTV Verschleibschutz GmbH

- 6.4.3.11 HAI Inc.

- 6.4.3.12 Imperial Systems Inc.

- 6.4.3.13 Kennametal Inc.

- 6.4.3.14 Lincotek Equipment SpA

- 6.4.3.15 Linde PLC (Praxair ST Technologies Inc.)

- 6.4.3.16 Metallisation Limited

- 6.4.3.17 Metallizing Equipment Co. Pvt. Ltd

- 6.4.3.18 OC Oerlikon Management AG

- 6.4.3.19 Plasma Powders

- 6.4.3.20 Powder Feed Dynamics Inc.

- 6.4.3.21 Progressive Surface

- 6.4.3.22 Saint-Gobain

- 6.4.3.23 Thermion

- 6.4.1 Thermal Spray Material Companies

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Advancements in Spraying Technology (Cold Spray Process)

- 7.2 Recycling of Thermal Spray Processing Materials

- 7.3 Increasing Demand From The Oil and Gas Industry