|

시장보고서

상품코드

1639423

유럽의 데이터센터 냉각 시장 전망 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Europe Data Center Cooling - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

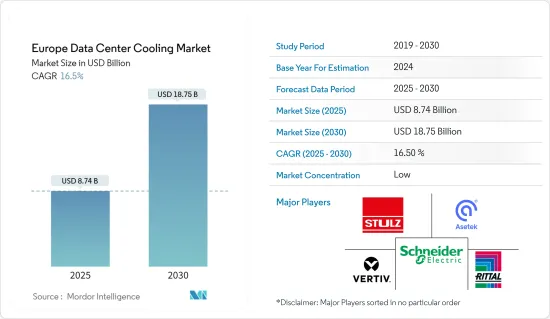

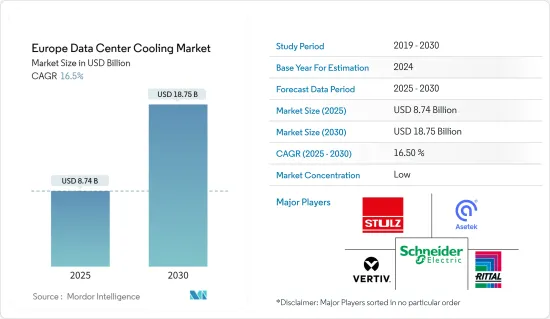

유럽의 데이터센터 냉각 시장 규모는 2025년에 87억 4,000만 달러로 추정되며, 예측 기간(2025-2030년)의 연평균 성장율(CAGR)은 16.5%로, 2030년에는 187억 5,000만 달러에 달할 것으로 예측됩니다.

중소기업의 클라우드 컴퓨팅 도입 증가, 현지 데이터 보안에 대한 정부 규제, 국내 기업의 투자 증가는 이 지역의 데이터 센터 냉각 수요를 견인하는 주요 요인 중 일부입니다.

주요 하이라이트

- 냉각 기술은 일반적으로 데이터센터의 지리적 위치에 따라 선택됩니다. 기업들이 정기적으로 비용 절감을 모색함에 따라 에너지 효율적인 냉각 방법이 기존 냉각 방법의 잠재적 대안으로 고려되고 있습니다. 또한 엣지 컴퓨팅 도입과 IoT 디바이스의 증가로 인해 시장의 성장이 촉진되고 있습니다.

- 헝가리, 그리스, 폴란드, 터키와 같은 신흥 유럽 국가의 IT 인프라 개발로 50MW 이상의 전력 용량을 갖춘 하이퍼스케일 데이터센터 시설의 건설이 증가할 것으로 예상됩니다. 영국, 독일, 프랑스는 유럽 전역에서 가장 많은 데이터 센터를 보유하고 있으며, 시장 참여자들은 이들 국가를 타깃으로 새로운 기술에 투자할 수 있습니다. 또한 향후 데이터 센터 조직과 파트너십을 맺어 경쟁력 있는 가격으로 시장 요구 사항을 충족하여 예측 기간 동안 유럽 데이터 센터 냉각 시장의 성장을 지원할 수 있습니다.

- 냉각 시스템은 데이터센터 전력 소비의 거의 40%를 차지합니다. 기업들은 친환경 데이터 센터를 구축하여 이 문제를 해결하려고 노력하고 있습니다. 정보를 저장, 관리, 배포하기 위해 친환경 데이터센터를 구축하는 추세가 증가함에 따라 많은 소프트웨어 기업이 에너지 소비와 총 에너지 비용을 절감하는 데 도움이 되었습니다. 예를 들어, AI와 결합된 Immersion4과 같은 친환경 기술은 효율적인 에너지 사용과 낮은 탄소 배출로 데이터센터의 운영 방식을 변화시켜 지속 가능성을 높이고 있습니다. 이러한 친환경 데이터센터의 등장은 이 지역의 냉각 장치에 대한 수요를 증가시키고 있습니다.

- 데이터센터 냉각 시스템은 설치에 많은 초기 투자가 필요하기 때문에 시장을 제한할 수 있습니다. 그러나 많은 현지 공급업체와 시장 참여자들이 기존 데이터 센터를 저렴한 비용으로 개조하여 새로운 장치를 설치하는 비용을 절감하는 혁신적인 솔루션을 개발하고 있습니다. 또한 정전 시 탄소 배출량 감소와 냉각 문제도 시장 성장을 저해할 수 있습니다.

- COVID-19 팬데믹은 봉쇄, 기기 부족, 공급망 중단으로 인해 신규 데이터센터 설립과 기존 데이터센터 업데이트에 차질을 빚으며 시장에 영향을 미쳤습니다. 반면에 유럽 국가에서는 데이터 양과 모바일 데이터 사용량이 크게 증가하여 유럽 전역의 데이터센터 설치가 증가할 것으로 예상됩니다. 이는 예측 기간 동안 시장 성장을 촉진할 것입니다. 또한 정부 지원은 예측 기간 동안 데이터 센터 냉각 시장의 발전을 촉진 할 것으로 예상됩니다.

유럽 데이터센터 냉각 시장 동향

소매 부문이 큰 시장 점유율을 차지할 전망

- 소매 부문에서는 전자 상거래 및 온라인 지출의 사용자 수가 증가함에 따라 엄청난 양의 빅 데이터가 생성되고 있으며, 이는 데이터 저장, 보안 및 지연 시간 단축에 대한 필요성을 촉진 할 것으로 예상됩니다. 이로 인해 이 지역의 지출과 데이터 센터 수가 증가하고 있습니다. 소매 부문의 급속한 발전과 4차 산업혁명 트렌드도 데이터 센터의 증가에 영향을 미치며 냉각 장치의 필요성을 높이고 있습니다.

- 온라인 사용자 수가 증가함에 따라 해외 리테일 기업들은 유럽 국가에 정기적으로 투자하여 스토리지 용량을 확장하고 인터넷 트래픽과 데이터 센터의 부하를 증가시키고 있습니다. 예를 들어, 중국의 거대 이커머스 기업인 JD.com은 최근 유럽 리테일 영역에 전략적으로 진출하기로 확정했습니다. 이 지역의 엄격한 규제로 인해 이 지역에 투자하는 외국 기업은 데이터 보호법과 관련하여 원활한 전환을 위해 데이터를 현지에 저장할 수 있습니다. 그 결과 데이터 센터 냉각 시스템의 사용이 증가하여 예측 기간 동안이 지역의 시장 성장을 촉진 할 것으로 예상됩니다.

- 특히 전자상거래 재단에 따르면, 유럽 지역의 높은 인터넷 보급률로 인해 유럽 B2C 전자상거래 매출은 약 13% 증가하여 6,210억 달러에 달할 것으로 예상됩니다. 이는 빅데이터의 양을 증가시켜 이 지역에 더 많은 데이터 센터와 냉각 시스템으로 이어질 수 있습니다.

- Eurostat에 따르면 이탈리아와 폴란드는 이커머스 사용자의 엄청난 성장을 목격했습니다. 이로 인해 방대한 양의 데이터가 생성되어 스토리지 요구 사항이 강화되었습니다. 그 결과 유럽 데이터 센터 냉각 시장은 예측 기간 동안 성장할 것으로 예상됩니다.

최대 시장 점유율을 차지하는 영국

- 영국의 기업들은 새로운 데이터 센터에 적극적으로 투자하고 있으며, 이는 예측 기간 동안 이 지역의 시장 성장에 긍정적인 영향을 미칠 것으로 예상됩니다. 예를 들어, 유럽의 코로케이션 및 네트워킹 회사인 Interxion은 런던에 세 번째 데이터 센터를 착공하여 소비자를 위한 통신사 및 CDN을 확장했습니다. 이러한 발전은 냉각 시스템 활용을 촉진하고 시장 성장을 촉진할 것으로 예상됩니다.

- 스웨덴의 패션 리테일러인 H&M은 스톡홀름의 새로운 데이터 센터에 냉각 및 열 회수 시스템을 통합할 계획입니다. 데이터 센터에서 발생하는 여분의 열은 에너지 회사인 Fortum Varme에서 도시 전역의 고객(최대 부하 시 2,500개의 현대식 주거용 아파트)에게 분배하여 재사용합니다.

- 영국은 유럽 전역에서 가장 많은 데이터 센터를 보유하고 있습니다. 시장 참여자들은 이러한 국가를 타깃으로 새로운 기술에 투자할 수 있습니다. 또한 향후 데이터 센터 조직과 파트너십을 맺어 경쟁력 있는 가격으로 요구 사항을 충족할 수 있으며, 이는 예측 기간 동안 유럽 데이터 센터 냉각 시장의 성장에 도움이 될 수 있습니다.

- 친환경 전기, 물 재생, 제로 수냉 시스템, 재활용 및 폐기물 관리와 같은 친환경 및 재생 가능 솔루션은 가장 지속 가능한 데이터 센터를 구축하는 데 사용되고 있습니다. 영국을 비롯한 유럽 국가들의 빅데이터 양이 증가함에 따라 저지연 및 고용량 데이터센터의 필요성이 증가하여 냉각 시스템 활용도가 높아질 것으로 예상됩니다. Science Direct에 따르면 데이터센터 에너지 사용량은 예측 기간 동안 전 세계 전력 공급의 2.13%를 차지할 것으로 예상됩니다.

- 기업들은 정기적으로 업종 전반에 걸쳐 운영 비용을 절감하기 위해 노력하고 있으며, 국내 데이터센터 냉각 시스템에 사용되는 AI 기술을 늘리고 있습니다. 예를 들어, 지멘스는 데이터센터의 냉각 시스템을 개선하기 위해 비질런트 AI 제품을 활용하는 AI 기반 열 최적화를 도입했습니다.

유럽의 데이터센터 냉각 산업 개요

유럽의 데이터 센터 냉각 시장은 세분화되어 있으며, 데이터 센터에 대한 효율 규제를 통해 기술 및 정부의 지원이 데이터 센터 냉각 시장의 성장에 도움이 될 것으로 예상됩니다. 주요 시장 기업으로는 IBM Corporation, 후지쯔 주식회사, 주식회사 히타치 제작소, 휴렛 팩커드 엔터프라이즈, 슈나이더 일렉트릭 SE 등을 들 수 있습니다. 기존 시장에서 주요 업체들의 강력한 입지를 바탕으로 시장 침투가 증가하고 있습니다. 혁신에 대한 관심이 높아짐에 따라 새로운 기술에 대한 수요가 증가하고 있으며, 이에 따라 추가 개발을 위한 투자가 증가하고 있습니다.

- 2024년 5월 : 리탈은 여러 하이퍼스케일 데이터센터 운영업체와 협력하여 모듈형 냉각 시스템을 개발했습니다. 이 솔루션은 직접 수냉식 냉각을 통해 1MW가 넘는 냉각 용량을 자랑합니다. 이 솔루션은 특히 AI 애플리케이션의 높은 전력 밀도를 충족하도록 맞춤 제작되었습니다.

- 2024년 1월 : 전 세계 하이퍼스케일 및 엔터프라이즈 고객을 위해 지속 가능하고 혁신적이며 적응형 규모의 데이터센터와 빌드 투 스케일 솔루션을 제공하는 기술 인프라 기업인 Aligned Data Centers는 인공지능, 머신러닝, 슈퍼컴퓨터를 비롯한 차세대 애플리케이션과 고성능 컴퓨팅의 고밀도 컴퓨팅 요구사항을 지원하기 위해 특허 출원 중인 솔루션인 DeltaFlow 액체 냉각 기술을 도입했습니다. DeltaFlow는 Aligned의 주문형 확장 기능을 확장하여 고객에게 변화하는 컴퓨팅 환경을 지원하기 위해 원활하게 확장하고 전환할 수 있는 유연성을 제공합니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

- 시장 개요(대상 범위 : 데이터센터 냉각과 관련된 현재 지역 동향의 상세한 분석 포함)

- 냉각에 관한 주요 비용의 고찰

- DC 냉각을 염두에두고 DC 운영과 관련된 주요 비용 오버 헤드 분석

- 데이터센터 냉각의 주요 기술 혁신과 발전

- 데이터센터에서 채택되고 있는 주된 에너지 효율 관행

제5장 시장 역학

- 시장 성장 촉진요인(에너지 소비에 대한 강조 증가, 친환경 솔루션으로의 이동과 같은 주요 요인은 향후 5-7년 동안 상대적인 영향을 기반으로 매핑)

- 시장 역학(규제의 역동적인 성질, 고객 요구의 진화 등의 주요인을, 향후 5-7년간의 상대적 영향에 근거해 매핑)

- 시장 기회

- 격리가있는 바닥과 격리가없는 바닥의 비교

- 산업 생태계 분석

제6장 지역별 데이터센터의 실적의 현황 분석

- 데이터센터의 IT 부하 용량과 면적 실적의 지역 분석(2017-2030년 기간)

- 유럽에서 확립된 DC 시장과 신흥 DC 핫스팟의 지역 분석

- DC 냉각에 관한 규제 틀의 지역 분석

제7장 데이터센터 냉각 시장 세분화

- 냉각 기술별(주요 동향, 2022-2029년 시장 규모 추계 및 예측, 전망)

- 공기 기반 냉각

- CRAH

- 냉각기와 이코노마이저

- 냉각탑(직접 냉각, 간접 냉각, 2단계 냉각을 포함)

- 기타

- 액체 기반 냉각

- 침수 냉각

- 직접 칩 냉각

- 후면 도어 열교환기

- 공기 기반 냉각

- 업계별

- IT 및 통신

- 소매 및 소비재

- 헬스케어

- 미디어, 엔터테인먼트

- 연방정부기관

- 기타 최종 사용자

- 국가별

- 영국

- 독일

- 러시아

- 덴마크

- 노르웨이

- 네덜란드

- 스페인

- 폴란드

- 스위스

- 오스트리아

- 벨기에

- 프랑스

- 이탈리아

- 아일랜드

- 스웨덴

제8장 경쟁 구도

- 기업 프로파일

- Vertiv Group Corp.

- Stulz GmbH

- Schneider Electric SE

- Rittal GmbH & Co. KG

- Asetek A/S

- Alfa Laval AB

- Iceotope Technologies Limited

- Green Revolution Cooling Inc.

- Chilldyne Inc.

- Airedale International Air Conditioning Ltd

제9장 투자 분석

제10장 시장 기회와 앞으로의 동향

HBR 25.02.17The Europe Data Center Cooling Market size is estimated at USD 8.74 billion in 2025, and is expected to reach USD 18.75 billion by 2030, at a CAGR of 16.5% during the forecast period (2025-2030).

The growing adoption of cloud computing among SMEs, government regulations for local data security, and growing investment by domestic players are some of the major factors driving the demand for data center cooling in the region.

Key Highlights

- Cooling technologies are usually selected based on the data centers' geographical location. As companies regularly seek to mitigate costs, energy-efficient cooling methods are being considered the potential alternatives to traditional cooling methods. The market's growth is also fueled by edge computing adoption and the increase in IoT devices.

- Developments in IT Infrastructure in emerging European countries such as Hungary, Greece, Poland, and Turkey are expected to increase the construction of hyperscale data center facilities with over 50 MW power capacity. The United Kingdom, Germany, and France had the highest number of data centers across Europe, and market players can target these countries to invest in their new technologies. Also, they can form partnerships with upcoming data center organizations to cater to market requirements at a competitive price, aiding the growth of the European data center cooling market over the forecast period.

- The cooling systems are responsible for almost 40% of the data center power consumption. Companies are trying to tackle this issue by setting up green data centers. The growing trends toward deploying green data centers for storing, managing, and distributing information have helped many software companies reduce energy consumption and total energy costs. For example, green technologies, such as Immersion4 in combination with AI, are changing how data centers operate to make them more sustainable with efficient energy usage and low carbon footprint. Such green data centers' emergence drives the demand for cooling units in the region.

- Data center cooling systems require a high initial investment to set up, which could restrain the market. However, many local vendors and market players are developing innovative solutions by modifying the existing data centers at a low cost to reduce the cost of setting up a new unit. Additionally, reduced carbon emission and cooling issues during power outages could hamper the growth of the market.

- The COVID-19 pandemic impacted the market owing to lockdowns, shortage of devices, and supply chain disruptions to set up new data centers and update the existing data centers. On the other hand, there is a massive rise in data volume and mobile data usage in European countries, which is anticipated to boost the setup of data centers across Europe. This will propel the market growth over the forecast period. Also, government support is projected to boost the development of the data center cooling market over the forecast period.

Europe Data Center Cooling Market Trends

The Retail Segment is Expected to Hold a Significant Market Share

- In the retail segment, the increasing number of users in e-commerce and online spending is creating an enormous volume of Big Data, which is expected to propel the need for data storage, security, and reduced latency. This boosts the region's expenditure and the number of data centers. Rapid development in the retail sector and Industry 4.0 trends are also responsible for the rise of data centers, enhancing the need for cooling devices.

- Due to the increasing number of online users, foreign retail companies regularly invest in European countries to expand their storage capacity, increasing internet traffic and the load on data centers. For instance, JD.com, a Chinese e-commerce giant, recently confirmed a strategic entry into the European retail sphere. Due to stringent regulations in the region, foreign companies investing in the area may store their data locally for smooth transitions regarding the data protection law. As a result, the usage of data center cooling systems is expected to increase, thereby boosting the market growth in the region over the forecast period.

- Notably, according to the E-commerce Foundation, the European B2C e-commerce turnover is expected to expand by approximately 13% to reach USD 621 billion due to the high internet penetration in the region. It may increase the Big Data volume, leading to more data centers and cooling systems in the area.

- According to Eurostat, Italy and Poland witnessed tremendous growth in e-commerce users. It led to the generation of a vast amount of data, thereby strengthening storage requirements. As a result, the European data center cooling market is expected to grow over the forecast period.

The United Kingdom Accounts For the Largest Market Share

- Companies in the UK are rigorously investing in new data centers, and this is expected to positively impact the market growth in the region over the forecast period. For instance, Interxion, a European colocation and networking company, commenced its third data center in London, expanding carriers and CDNs for consumers. This development is expected to propel cooling system utilization and foster market growth.

- H&M, a fashion retailer in the country, plans to integrate a cooling and heat recovery system in its new data center in Stockholm. The excess heat generated from the data center is reused by Fortum Varme, an energy company, by distributing it to customers (2,500 modern residential apartments at full load) throughout the city.

- The UK recorded the highest number of data centers across Europe. Market players can target these countries to invest in their new technologies. Also, they can form partnerships with upcoming data center organizations to cater to their requirements at a competitive price, which may aid the growth of the European data center cooling market over the forecast period.

- Green and renewable solutions, such as green electricity, water reclamation, zero water cooling systems, recycling, and waste management, are being used to build the most sustainable data centers. Growth in Big Data volume across European countries, including the United Kingdom, is expected to increase the need for low-latency and high-capacity data centers, thereby boosting cooling system utilization. According to Science Direct, data center energy use might account for 2.13% of worldwide electricity supply over the forecast period.

- Companies are regularly trying to reduce their operational cost across their verticals, increasing the AI technology used in data center cooling systems in the country. For instance, Siemens introduced AI-based thermal optimization, wherein the company utilizes Vigilant AI products to enhance cooling systems in data centers.

Europe Data Center Cooling Industry Overview

The European data center cooling market is fragmented as the benefits offered by the technology and support from the government by imposing efficiency regulations on data centers are expected to help the growth of the data center cooling market. Some major market players are IBM Corporation, Fujitsu Ltd, Hitachi Ltd, Hewlett-Packard Enterprise, and Schneider Electric SE. Market penetration is growing with a strong presence of major players in established markets. With the increasing focus on innovation, the demand for new technologies is growing, which, in turn, is driving investments for further developments.

- May 2024: Rittal, in collaboration with multiple hyperscale data center operators, developed a modular cooling system. This solution boasts a cooling capacity exceeding 1 MW, achieved through direct water cooling. It is specifically tailored to cater to the high-power densities of AI applications.

- January 2024: Aligned Data Centers, the technology infrastructure company providing sustainable, innovative, and adaptive scale data centers and build-to-scale solutions for global hyperscale and enterprise customers, introduced its DeltaFlow liquid cooling technology, a patent-pending solution built to support the high-density compute requirements of next-generation applications and high-performance computing, including artificial intelligence, machine learning, and supercomputers. DeltaFlow extended Aligned's ExpandOnDemand capabilities, providing customers the flexibility to seamlessly scale and pivot to support shifting computing environments.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview (Coverage: A detailed analysis of the current regional trends related to Data Center Cooling are included in this section)

- 4.2 Key cost considerations for Cooling

- 4.2.1 Analysis of the key cost overheads related to DC operations with an eye on DC Cooling

- 4.2.2 Key innovations and developments in Data Center Cooling

- 4.2.3 Key energy efficiency practices adopted in Data Centers

5 MARKET DYNAMICS

- 5.1 Market Drivers (Key factors such as the increased emphasis on energy consumption, move towards green solutions are mapped based on their relative impact over the next 5-7 years)

- 5.2 Market Challenges (Key factors such as the dynamic nature of regulations, evolving customer needs are mapped based on their relative impact over the next 5-7 years)

- 5.3 Market Opportunities

- 5.4 Comparison of raised floor with containment & raised floor without commitment

- 5.5 Industry Ecosystem Analysis

6 ANALYSIS OF THE CURRENT REGIONAL DATA CENTER FOOTPRINT

- 6.1 Regional Analysis of IT Load Capacity & Area Footprint of Data Centers (for the period of 2017-2030)

- 6.2 Regional Analysis of the Established DC Markets and Emerging DC Hotspots in Europe region (we will include coverage by highlighting major established and emerging DC markets)

- 6.3 Regional Analysis of Regulatory Framework On DC Cooling

7 DATA CENTER COOLING MARKET SEGMENTATION

- 7.1 By Cooling Technology (Key trends, market size estimates & projections for the period of 2022-2029 and future outlook)

- 7.1.1 Air-based Cooling

- 7.1.1.1 CRAH

- 7.1.1.2 Chiller and Economizer

- 7.1.1.3 Cooling Tower (covers direct, indirect & two-stage cooling)

- 7.1.1.4 Others

- 7.1.2 Liquid-based Cooling

- 7.1.2.1 Immersion Cooling

- 7.1.2.2 Direct-to-Chip Cooling

- 7.1.2.3 Rear-Door Heat Exchanger

- 7.1.1 Air-based Cooling

- 7.2 By End-user Vertical

- 7.2.1 IT & Telecom

- 7.2.2 Retail & Consumer Goods

- 7.2.3 Healthcare

- 7.2.4 Media & Entertainment

- 7.2.5 Federal & Institutional agencies

- 7.2.6 Other End Users

- 7.3 By Country

- 7.3.1 United Kingdom

- 7.3.2 Germany

- 7.3.3 Russia

- 7.3.4 Denmark

- 7.3.5 Norway

- 7.3.6 Netherlands

- 7.3.7 Spain

- 7.3.8 Poland

- 7.3.9 Switzerland

- 7.3.10 Austria

- 7.3.11 Belgium

- 7.3.12 France

- 7.3.13 Italy

- 7.3.14 Ireland

- 7.3.15 Sweden

8 COMPETITIVE LANDSCAPE

- 8.1 Company Profiles

- 8.1.1 Vertiv Group Corp.

- 8.1.2 Stulz GmbH

- 8.1.3 Schneider Electric SE

- 8.1.4 Rittal GmbH & Co. KG

- 8.1.5 Asetek A/S

- 8.1.6 Alfa Laval AB

- 8.1.7 Iceotope Technologies Limited

- 8.1.8 Green Revolution Cooling Inc.

- 8.1.9 Chilldyne Inc.

- 8.1.10 Airedale International Air Conditioning Ltd