|

시장보고서

상품코드

1639490

인도의 석유 및 가스 - 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)India Oil And Gas - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

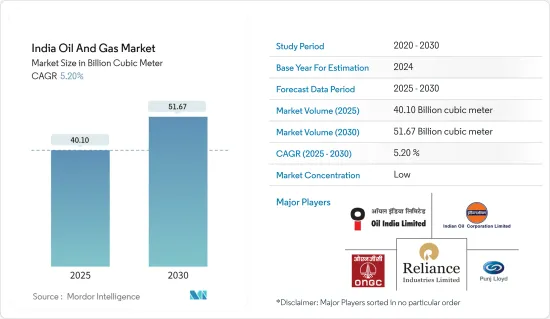

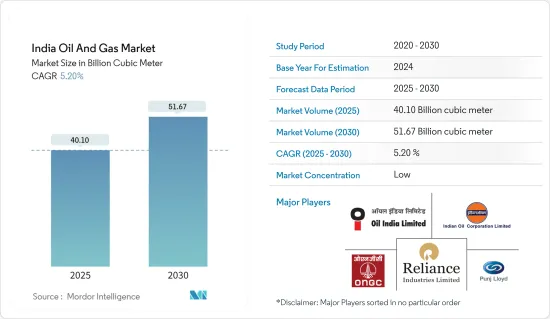

인도의 석유 및 가스 시장 규모는 2025년 401억 입방미터로 추정되며, 예측 기간(2025-2030년) 동안 5.2%의 CAGR로 2030년에는 516억 7,000만 입방미터에 달할 것으로 예상됩니다.

COVID-19 발생으로 인한 지역적 가동 중단과 정유 제품 수요 감소로 인해 시장은 부정적인 영향을 받았습니다. 현재 시장은 전염병 발생 이전 수준으로 회복되고 있습니다.

주요 하이라이트

- 천연가스 파이프라인 용량 증가와 석유 제품 수요 증가 등의 요인이 예측 기간 동안 인도 석유 및 가스 시장을 견인할 것으로 예상됩니다. 또한, 석유 및 천연가스 시장은 에너지 시장의 주요 산업이며, 세계 주요 연료로서 세계 경제에 영향력 있는 역할을 하고 있습니다. 석유 및 가스 생산 및 유통과 관련된 프로세스와 시스템은 매우 복잡하고 자본 집약적이며 최첨단 기술을 필요로 합니다.

- 그러나 국내 수요를 충족시키기 위해 원유 및 천연가스 수입에 크게 의존하고 있다는 점과 원유 가격의 변동성이 크다는 점이 인도 석유 및 가스 시장의 성장을 저해할 것으로 예상됩니다.

- KG 분지에서는 가스하이드레이트가 대량으로 발견되고 있습니다. 경제적으로 채굴 가능한 가스하이드레이트는 기업들에게 큰 비즈니스 기회가 될 수 있으며, 천연가스 생산량 증가로 이어질 수 있습니다.

인도의 석유 및 가스 시장 동향

다운스트림 부문이 크게 성장할 것으로 예상

- 인도의 에너지 수요는 향후 20년간 50% 성장할 것으로 예상됩니다. 이러한 수요 증가는 세계 인구의 증가와 개발도상국의 생활수준 향상에 기인합니다. 신에너지와 재생에너지가 전 세계적으로 보급되고 있지만, 석유 연료는 여전히 전 세계적으로 주요 에너지원으로 남아 있습니다. 이러한 추세는 향후 수십 년 동안 지속될 것으로 예상되며, 석유 및 가스 다운스트림 시장의 성장에 유리하게 작용하고 있습니다.

- 국내 곳곳에 새로운 정유소 설립이 결정되었습니다. 예를 들어, 2023년 2월 Hindustan Petroleum Corp(HPCL)은 2024년 1월까지 라자스탄 주에 연간 생산량 900만 톤 규모의 발마르 정유공장 및 석유화학 프로젝트를 가동할 예정이라고 발표했습니다.

- 2021-2022년(2021-2022년)의 정유 처리량은 2억 4,922만 톤으로 2017년의 약 2억 3,397만 톤에 비해 증가했습니다. 이 수치의 증가는 휘발유 및 디젤과 같은 수송용 연료에 대한 높은 수요와 시장의 주거 부문에서 LPG에 대한 지속적인 높은 수요에 기인합니다.

- 높은 정제 능력이 요구되는 또 다른 큰 요인은 국내, 특히 크리슈나 고다발리 분지와 라자스탄 주 발마르 지역의 유전이 증가하고 있다는 점입니다. 이들 유전의 천연가스 생산량이 많기 때문에 국내 정유소와 석유화학 콤비네이션의 용량이 확대되고 있습니다.

- 향후 예정된 여러 대형 프로젝트들로 인해 다운스트림 부문은 예측 기간 동안 큰 성장을 이룰 것으로 예상됩니다.

미드스티림부문에 대한 투자 증가가 시장을 견인할 것으로 보입니다.

- 파이프라인은 천연가스, 원유, 석유제품을 장거리로 운송하는 가장 경제적인 방법입니다. 향후 몇 년 동안 인도 석유 및 가스 시장에서 미드스티림 부문이 상당한 점유율을 차지할 것으로 예상됩니다.

- 2022년 3월 현재 인도에는 약 10,419km의 원유 파이프라인(육상: 9,825km, 해상: 594km), 17,389km의 천연가스 파이프라인(육상: 1,7,365km, 해상: 24km), 1,4,729km의 정유 제품 파이프라인이 있으며, IOCL, BORL, Cairn India, Oil, HMEL, OIL, ONGC에 의해 운영되고 있습니다. BORL, Cairn India, OIL, HMEL, ONGC에 의해 운영되고 있습니다. 파이프라인 외에도 인도에는 2022년 3월 현재 5개의 LNG 기지가 있습니다.

- 2022년 2월, 인도 정부는 국내 생산량을 늘리기 위해 석유 및 가스 탐사 면적을 2025년까지 50만 평방킬로미터, 2030년까지 100만 평방킬로미터로 두 배로 늘릴 것이라고 발표했습니다.

- 2022년 6월 30일 기준, Gas Authority of India Ltd(GAIL)는 3만 3,815km의 천연가스 파이프라인 네트워크에서 가장 큰 점유율을 차지하고 있습니다.

- 2022년 현재 인도 원유 파이프라인망의 50.88%(1,5,113km)를 Indian Oil Corporation이 점유하고 있습니다. 인도 정부는 국내 가스 파이프라인망 확충을 위해 99억 7,000만 달러를 투자할 예정으로 시장 성장에 박차를 가하고 있습니다.

- 2022년 3월, 중국석유공사(IOC)는 9개 지역의 도시가스 배급(CGD) 네트워크 개발에 9억 3,260만 달러를 투자하는 것을 승인했습니다.

- 따라서 미드스티림 부문에 대한 투자 증가가 인도 석유 및 가스 시장을 주도하고 있습니다. 파이프라인 커버리지는 예측 기간 동안 크게 증가할 것으로 예상되며, 석유 제품 파이프라인은 이 부문에서 가장 많이 증가할 것으로 예상됩니다.

인도의 석유 및 가스 산업 개요

인도의 석유 및 가스 시장은 단편적입니다. 주요 진출 기업(순서는 무관)으로는 Oil and Natural Gas Corporation(ONGC), Oil India Limited(OIL), Reliance Industries, Indian Oil Corporation Limited(IOCL), Punj. Lloyd Limited 등이 있습니다.

기타 혜택

- 엑셀 형식의 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

목차

제1장 소개

- 조사 범위

- 시장 정의

- 조사 가정

제2장 조사 방법

제3장 주요 요약

제4장 시장 개요

- 소개

- 2028년까지 천연가스 생산량 예측(단위 : 1억 입방미터)

- 2028년까지 원유 생산량 예측(단위 : 1억 입방미터)

- 2028년까지 정유소 설치 용량과 예측(단위 : 1,000배럴/일)

- 2028년까지 LNG 터미널 설치 용량(MTPA)과 예측

- 최근 동향과 개발

- 정부 정책 및 규정

- 시장 역학

- 성장 촉진요인

- 성장 억제요인

- 공급망 분석

- PESTLE 분석

제5장 시장 세분화

- 부문

- 업스트림

- 전개 장소

- 온쇼어

- 오프쇼어

- 다운스트림

- 정유소

- 석유화학 플랜트

- 미드스트림

- 운송

- 저장

- LNG 터미널

- 업스트림

제6장 경쟁 구도

- M&A, 합작투자, 제휴, 협정

- 주요 기업의 전략

- 시장 점유율 분석

- 기업 개요

- Oil and Natural Gas Corporation

- Oil India Limited

- Reliance Industries

- Indian Oil Corporation Limited

- Punj Lloyd Limited

- Bharat Petroleum Corporation Limited

- GAIL(India) Limited

- Hindustan Petroleum Corporation Limited

- Cairn India

제7장 시장 기회와 향후 동향

ksm 25.02.10The India Oil And Gas Market size is estimated at 40.10 billion cubic meter in 2025, and is expected to reach 51.67 billion cubic meter by 2030, at a CAGR of 5.2% during the forecast period (2025-2030).

The market was negatively impacted by the outbreak of COVID-19 due to regional lockdowns and a decline in demand for refined petroleum products. Currently, the market has rebounded to pre-pandemic levels.

Key Highlights

- Factors such as the increasing natural gas pipeline capacity and the increasing demand for petroleum products are expected to drive the Indian oil and gas market during the forecast period. Also, the oil and natural gas market is a major industry in the energy market and plays an influential role in the global economy as the world's primary fuel source. The processes and systems involved in producing and distributing oil and gas are highly complex, capital-intensive, and require state-of-the-art technology.

- However, a huge dependence on imports of crude oil and natural gas to satisfy domestic demand and the high volatility of crude oil prices are expected to hinder the growth of the Indian oil and gas market.

- There have been significant gas hydrate discoveries in the KG Basin. Economically feasible extraction of the gas hydrates may create immense opportunities for the companies, which may lead to a boom in natural gas production.

India Oil and Gas Market Trends

The Downstream Sector is Expected to Witness Significant Growth

- Indian energy demand is anticipated to grow by 50% in the next two decades. This growth in demand can be attributed to the growing world population and an improvement in living standards in developing countries. Even though new and renewable energy sources are gaining popularity around the world, petroleum fuel remains a major energy source globally. This trend is expected to continue for the next few decades and favors the growth of the oil and gas downstream market.

- New refineries were set to be established in various parts of the country. For instance, in February 2023, Hindustan Petroleum Corp (HPCL) announced that the company plans to start its 9 million tonne-a-year Barmer refinery and petrochemical project in Rajasthan state by January 2024.

- The country's oil refinery throughput in the fiscal year (2021-2022) was 249.22 million metric tons, a growth from the 2017 figures, which were around 233.97 million metric tons. The increased value is the conclusion of the high demand for transport fuels like motor gasoline and diesel and the constantly high demand for LPG in the market's residential segment.

- The other major factor that has led to the requirement of high refining capacity is the increasing number of fields in the country, especially in the Krishna-Godavari Basin and Barmer Region of Rajasthan State. The high natural gas production from these fields has led to an expansion in the capacity of refineries and petrochemical complexes in the country.

- Owing to several major upcoming projects, the downstream sector is expected to witness significant growth during the forecast period.

Increasing Investment in the Midstream Sector May Drive the Market

- The pipeline is the most economical way of transporting natural gas, crude oil, and petroleum products over a long distance due to increasing investments in upcoming pipelines in the country. The midstream segment is expected to contribute a decent share in the Indian oil and gas market in the coming years.

- As of March 2022, the country had around 10,419 km of crude oil pipelines (onshore: 9,825 km and offshore: 594 km), 17,389 km of natural gas pipelines (onshore: 17,365 km and offshore: 24 km), and 14,729 km of refined products pipelines, being operated by IOCL, BORL, Cairn India, OIL, HMEL, and ONGC. In addition to the pipelines, India had 5 LNG terminals in March 2022.

- In February 2022, the government of India announced to double its exploration area of oil and gas to 0.5 million sq. km. by 2025 and to 1 million sq. km. by 2030 with a view to increasing domestic output.

- As of June 30, 2022, the Gas Authority of India Ltd (GAIL) had the largest share of the country's natural gas pipeline network, i.e., 33,815 km.

- As of 2022, Indian Oil Corporation accounted for 50.88% (15113 km) of India's crude pipeline network. The Indian government is set to invest USD 9.97 billion to expand the gas pipeline network across the country, culminating in the growth of the market.

- In March 2022, Indian Oil Corporation (IOC) Limited approved to invest USD 932.6 million for the development of City Gas Distribution (CGD) network in 9 geographical areas.

- Hence, increasing investments in the midstream sector have driven the India oil and gas market. Pipeline coverage is expected to increase substantially during the forecast period, with the petroleum product pipeline expected to increase the most in the segment.

India Oil and Gas Industry Overview

The India oil and gas market is fragmanted. Some of the key players (in no particular order) include Oil and Natural Gas Corporation (ONGC), Oil India Limited (OIL), Reliance Industries, Indian Oil Corporation Limited (IOCL), and Punj Lloyd Limited., among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Natural Gas Production Forecast in billion cubic meters, till 2028

- 4.3 Crude Oil Production Forecast in billion cubic meters, till 2028

- 4.4 Refinery Installed Capacity and Forecast in thousand barrels per day, till 2028

- 4.5 LNG Terminals Installed Capacity and Forecast in MTPA, till 2028

- 4.6 Recent Trends and Developments

- 4.7 Government Policies and Regulations

- 4.8 Market Dynamics

- 4.8.1 Drivers

- 4.8.2 Restraints

- 4.9 Supply Chain Analysis

- 4.10 PESTLE Analysis

5 MARKET SEGMENTATION

- 5.1 Sector

- 5.1.1 Upstream

- 5.1.1.1 Location of Deployment

- 5.1.1.1.1 Onshore

- 5.1.1.1.2 Offshore

- 5.1.2 Downstream

- 5.1.2.1 Refineries

- 5.1.2.2 Petrochemical Plants

- 5.1.3 Midstream

- 5.1.3.1 Transportation

- 5.1.3.2 Storage

- 5.1.3.3 LNG Terminals

- 5.1.1 Upstream

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Market Share Analysis

- 6.4 Company Profiles

- 6.4.1 Oil and Natural Gas Corporation

- 6.4.2 Oil India Limited

- 6.4.3 Reliance Industries

- 6.4.4 Indian Oil Corporation Limited

- 6.4.5 Punj Lloyd Limited

- 6.4.6 Bharat Petroleum Corporation Limited

- 6.4.7 GAIL (India) Limited

- 6.4.8 Hindustan Petroleum Corporation Limited

- 6.4.9 Cairn India