|

시장보고서

상품코드

1639526

건설용 접착제 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Construction Adhesives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

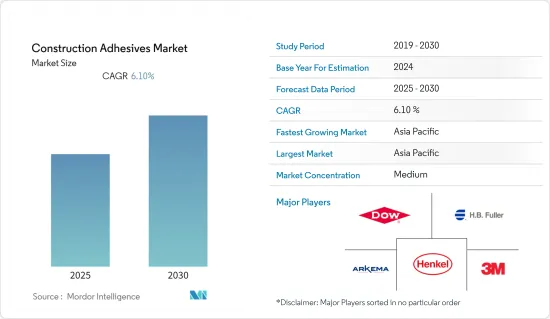

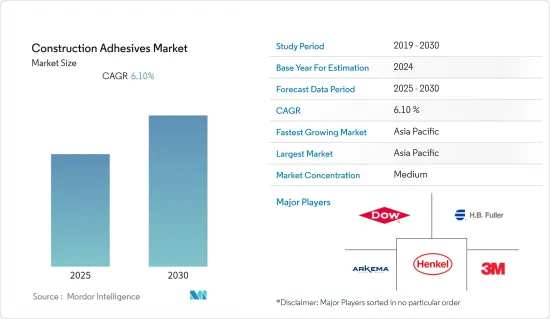

건설용 접착제 시장은 예측 기간 동안 6.1%의 CAGR을 기록할 것으로 예상됩니다.

COVID-19의 발생은 건설 산업에 단기 및 장기적으로 여러 가지 영향을 미치고 건설용 접착제 및 실란트 수요에 영향을 미칠 가능성이 높습니다. 미국종합건설협회(AGC)에 따르면, 작업 중단 및 프로젝트 중단이 있을 수 있으며, 사무실, 엔터테인먼트 및 스포츠 시설과 같은 "비본질적" 프로젝트에서 수요가 감소할 수 있다고 합니다. 이러한 프로젝트 및 기타 건설 활동의 중단으로 인해 건설용 접착제에 대한 수요가 감소하는 경향이 있습니다.

주요 하이라이트

- 단기적으로는 신흥국의 주택 및 건설 프로젝트 증가와 건설 산업에 대한 투자 증가가 시장을 이끄는 주요 요인으로 작용하고 있습니다.

- 그러나 배출가스에 대한 엄격한 환경 규제가 시장 성장을 억제할 가능성이 높습니다.

- 건설 부문에서 바이오 기반 및 하이브리드 접착제에 대한 수요 증가와 녹색 건설에 대한 접착제의 기여는 향후 시장에서 기회를 창출할 가능성이 높습니다.

건설용 접착제 시장 동향

시장을 독점하는 주택 부문

- 주택 건설에서 접착제는 카펫 깔기, 카운터 라미네이트, 바닥재 설치, 벽지 붙이기 등 여러 가지 응용 분야가 있습니다. 접착제를 사용하면 나사 사용을 줄이고 주택의 내후성을 높일 수 있습니다.

- 전 세계 주택 건설은 인구 증가, 농촌에서 서비스 산업 클러스터로의 전환, 핵가족화 추세 등의 요인으로 인해 지난 몇 년 동안 큰 폭의 성장세를 보이고 있습니다. 또한, 인구 대비 토지 비율의 감소와 고층 주택 및 타운십 건설의 증가 추세는 전 세계 주택 건설 부문에서 접착제의 적용을 촉진하고 있습니다.

- 전 세계적으로 주택 수요를 충족시킬 수 있는 공급이 크게 부족합니다. 이는 개발을 진행하기 위해 대체 공법이나 새로운 파트너십을 채택하는 투자자와 개발자들에게 큰 기회가 되었습니다.

- Oxford Economics의 추정에 따르면 2020년 세계 건설 생산액은 10조 7,000억 달러로 2020-2030년 사이에 42% 증가한 4조 5,000억 달러, 15조 2,000억 달러에 달할 것으로 예상됩니다. 예를 들어

- 미국에서는 World Construction Today에 따르면, 미국종합건설협회(AGC)가 연방정부 데이터를 평가한 결과, 많은 유형의 상업용 건설에 대한 수요가 당분간 견조할 것으로 판단했습니다.

- 인터내셔널 컨스트럭션에 따르면, 중국 정부는 전염병으로 인한 지역 경제 회복을 지원하기 위해 2023년부터 대규모 건설 인프라 프로젝트에 대한 지출을 전년 대비 1조 8,000억 달러 증가시킬 계획입니다.

- 캐나다에서는 Affordable Housing Initiative(AHI), New Building Canada Plan(NBCP), Made in Canada 등 다양한 정부 프로젝트가 이 부문의 확장을 지원하고 있습니다.

- 유로 통계에 따르면 2023년 2월 건설 생산은 2023년 1월 대비 유로존(EA20)에서 2.3%, EU-27에서 2.1% 증가했습니다.

- 위와 같은 요인으로 인해 세계 건설 산업이 성장할 것으로 예상되기 때문에 건설용 접착제의 수요도 증가할 것으로 예상됩니다.

아시아태평양 시장을 장악

- 아시아태평양은 인도, 중국, 동남아시아 각국의 건설 시장의 막대한 수요로 인해 건설용 접착제의 가장 큰 시장을 차지하고 있습니다.

- 이 지역의 상업용 사무실과 건물의 수는 주요 경제 비즈니스 중심지의 성장과 매력적인 외관과 지속가능하고 경제적인 건설을 추구하는 건설업체 간의 경쟁으로 인해 지난 10년간 증가했습니다.

- 중국의 건설산업이 빠르게 발전한 것은 중앙정부가 경제성장을 유지하기 위한 수단으로 건설산업에 대한 투자를 추진했기 때문입니다.

- 중국 국가통계국에 따르면, 중국 건설 산업은 2022년 약 8조 3,000억 위안(1조 1,800억 달러)의 부가가치를 창출했습니다.

- 중국 정부는 경제를 서비스 중심으로 재조정하기 위해 노력하고 있음에도 불구하고, 향후 10년간 2억 5,000만 명을 새로운 거대 도시로 이주시키는 등 대규모 건설 계획을 추진했습니다.

- India Brand Equity Foundation(IBEF)에 따르면, 인도의 건설 산업은 2025년까지 약 1조 달러 규모의 세계 3위 시장으로 성장할 것이라고 합니다.

- 일본 국토교통성(일본)에 따르면, 2022년 일본에서 착공된 주택 수는 약 85만 9,500호입니다. 경제연구회에 따르면, 2023년 4월 기준 일본의 건설자재 월간 가격지수는 147.8입니다.

- 이러한 요인들은 아시아태평양의 건설용 접착제 시장을 견인할 것으로 예상됩니다.

건설용 접착제 산업 개요

세계 건설용 접착제 시장은 통합적인 성격을 가지고 있습니다. 주요 참여 기업으로는 Henkel Adhesives Technologies India Private Limited, Dow, H.B. Fuller, Arkema Group, 3M 등이 있습니다.

기타 혜택

- 엑셀 형식의 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

목차

제1장 소개

- 조사 가정

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 성장 촉진요인

- 건설 산업에 대한 투자 확대

- 신흥 국가의 주택·건설 프로젝트 증가

- 기타 촉진요인

- 성장 억제요인

- 엄격한 환경 규제

- 기타 성장 억제요인

- 산업 밸류체인 분석

- Porter's Five Forces 분석

- 공급 기업의 교섭력

- 소비자의 협상력

- 신규 참여업체의 위협

- 대체품의 위협

- 경쟁 정도

제5장 시장 세분화(금액 기준 시장 규모)

- 유형

- 수성

- 용제형

- 핫멜트

- 반응성

- 기타

- 용도

- 주택

- 상업

- 인프라

- 산업·시설

- 지역

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 이탈리아

- 프랑스

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카공화국

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- M&A, 합작투자, 제휴, 협정

- 시장 점유율(%) 분석**/시장 순위 분석

- 주요 기업의 전략

- 기업 개요

- 3M

- Adhesives Technology Corporation(ATC)

- Ashland

- Avery Dennison Corporation

- Bostik

- Don Construction Products Limited

- Dow

- Franklin International

- Gorilla Glue Inc.

- H.B. Fuller Company

- Henkel Adhesives Technologies India Private Limited

- Huntsman International LLC

- MAPEI S.p.A.

- RPM International Inc.

- Sika AG

- Wacker Chemie AG

제7장 시장 기회와 향후 동향

- 건설 산업의 바이오 기반 접착제와 하이브리드 접착제 수요 증가

- 그린 컨스트럭션에 기여하는 접착제

The Construction Adhesives Market is expected to register a CAGR of 6.1% during the forecast period.

The outbreak of COVID-19 brought several short-term and long-term consequences in the construction industry, which is likely to affect the demand for construction adhesives and sealants. According to the Associated General Contractors of America (AGC), there were disruptions to work or canceled projects, and the demand may be potentially less for 'non-essential' projects, like offices, entertainment, and sports facilities. Due to the shutdown of such projects and other construction activities, the demand for construction adhesives tends to constrain.

Key Highlights

- In the short term, major factors driving the market studied are the increase in housing and construction projects in emerging countries and increasing investments in the construction industry.

- However, stringent environmental regulations related to emissions will likely restrain the market's growth.

- Increasing demand for bio-based and hybrid adhesives in the construction sector and adhesive contribution to green construction is likely to create opportunities for the market in the future.

Construction Adhesives Market Trends

Residential Segment to Dominate the Market

- In residential construction, adhesives have several application areas like carpet laying, laminating countertops, installing flooring, wallpapering, etc. The use of adhesives can reduce the usage of screws and help in weatherproofing the house.

- Residential construction across the globe has been witnessing significant growth over the past few years owing to factors like population growth, migration from rural areas to service sector clusters, and the growing trend of nuclear families. Besides, the decreasing land-to-population ratio and the growing trend of constructing high-rise residential buildings and townships have been driving the application of adhesives in the residential construction segment across the globe.

- Globally, there has been a significant undersupply to meet the demand for housing. This presented a major opportunity for the investors and developers to embrace alternative construction methods and new partnerships to bring forward development.

- According to Oxford Economics Estimates, in 2020, the global construction output was USD 10.7 trillion and is expected to grow by 42% or USD 4.5 trillion between 2020 and 2030 to reach USD 15.2 trillion. For instance:

- In the United States, according to World Construction Today, the Associated General Contractors of America's- AGC evaluation of the federal data determined that the demand for numerous kinds of commercial construction will remain strong for the immediate future.

- According to International Construction, the Chinese government is set to increase its spending on large construction and infrastructure projects by USD 1.8 trillion year-on-year starting from 2023 to help regional economies recover from the pandemic.

- Various government projects in Canada, including the Affordable Housing Initiative (AHI), New Building Canada Plan (NBCP), and Made in Canada, have supported the sector's expansion.

- According to Eurostat, in February 2023, construction production increased by 2.3% in the euro area (EA20) and 2.1% in EU-27 compared to January 2023.

- Due to all the factors above, the global construction industry is expected to grow, so the demand for construction adhesives is also expected to increase.

Asia-Pacific Region to Dominate the Market

- Asia-Pacific accounted for the largest market for construction adhesives, owing to huge demand from the construction market in India, China, and various countries in Southeast Asia.

- The number of commercial offices and buildings in the region has increased since the last decade, owing to major economic and business centers' growth and competition among the construction players for attractive looks and sustainable and economical construction.

- China's construction industry developed rapidly due to the central government's push for investment in the construction industry as a means to sustain economic growth.

- China's construction industry generated an added value of around 8.3 trillion yuan (USD 1.18 trillion) in 2022, according to the National Bureau of Statistics of China.

- The Chinese government rolled out massive construction plans, including making provision for the movement of 250 million people to its new megacities over the next ten years, despite efforts to rebalance its economy to a more service-oriented form.

- According to the India Brand Equity Foundation (IBEF), India's construction industry is set to emerge as the third-largest market in the world, with a size of almost USD 1 trillion by 2025.

- According to MLIT (Japan), around 859.5 thousand housing units were initiated in Japan in 2022. According to the Economic Research Association, as of April 2023, Japan's construction materials monthly price index stood at 147.8.

- These factors are expected to drive the construction adhesives market in the Asia-Pacific region.

Construction Adhesives Industry Overview

The global construction adhesive market is consolidated in nature. Some of the major players include Henkel Adhesives Technologies India Private Limited, Dow, H.B. Fuller, Arkema Group, and 3M.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Investments in the Construction Industry

- 4.1.2 Increase in Housing and Construction Projects in Emerging Countries

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Stringent Environmental Regulations

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Type

- 5.1.1 Water-based

- 5.1.2 Solvent-based

- 5.1.3 Hot-melt

- 5.1.4 Reactive

- 5.1.5 Other Types

- 5.2 Application

- 5.2.1 Residential

- 5.2.2 Commercial

- 5.2.3 Infrastructure

- 5.2.4 Industrial and Institutional

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%) Analysis**/Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 3M

- 6.4.2 Adhesives Technology Corporation (ATC)

- 6.4.3 Ashland

- 6.4.4 Avery Dennison Corporation

- 6.4.5 Bostik

- 6.4.6 Don Construction Products Limited

- 6.4.7 Dow

- 6.4.8 Franklin International

- 6.4.9 Gorilla Glue Inc.

- 6.4.10 H.B. Fuller Company

- 6.4.11 Henkel Adhesives Technologies India Private Limited

- 6.4.12 Huntsman International LLC

- 6.4.13 MAPEI S.p.A.

- 6.4.14 RPM International Inc.

- 6.4.15 Sika AG

- 6.4.16 Wacker Chemie AG

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increase In Demand for Bio-based and Hybrid Adhesives in the Construction Industry

- 7.2 Adhesives Contribute to Green Construction