|

시장보고서

상품코드

1640438

스킨 포장 : 시장 점유율 분석, 산업 동향, 성장 예측(2025-2030년)Skin Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

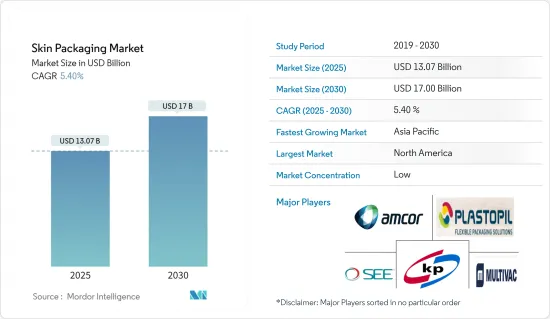

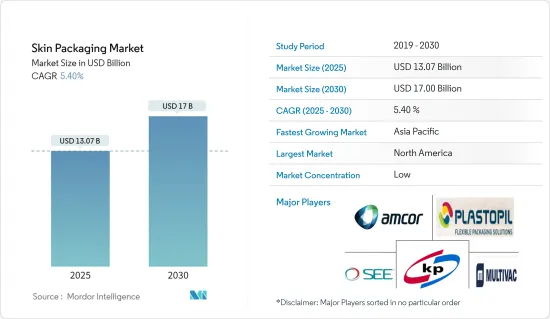

스킨 포장 시장 규모는 2025년에 130억 7,000만 달러로 추정되며, 예측 기간(2025-2030년)의 CAGR은 5.4%로, 2030년에는 170억 달러에 달할 것으로 예측됩니다.

주요 하이라이트

- 스킨 포장은 열성형 트레이와 제조된 플라스틱 용기 위에 얇은 플라스틱 필름을 씌우는 최첨단 기술입니다. 이 플라스틱 필름은 고객이 오염의 위험 없이 제품을 볼 수 있게 하고 제품을 손상시키거나 부패시킬 수 있는 공기 및 습기에 대해 투명한 보호층을 제공합니다.

- 식품을 보호하고, 유통기한을 연장하며, 폐기물을 줄이고, 시인성을 향상시키는 요구가 높아짐에 따라 스킨 포장은 내구성이 있는 트레이로 신뢰성 등의 이점을 제공해 출하, 보관 및 진열시에 제품 형태를 유지하고 보호하기 위해 식품 산업에서의 수요가 높아지고 있습니다.

- 치즈, 콜드 컷, 다양한 형태의 쇠고기 등 다양한 육류와 유제품 보존에 대한 수요 증가가 스킨 포장 시장을 견인하고 있습니다. 진공 스킨 포장은 더 나은 내구성을 제공하기 때문에 기존의 포장 기술은 최근 다양한 식품 산업 응용 분야에서 사라지고 있습니다. 또한 기존 포장 솔루션에 비해 식품을 보호하는 층을 추가로 제공하여 채택이 증가하고 이는 시장 성장을 지원합니다.

- 재활용과 바이오플라스틱의 장점에 대한 이해가 넓어지면서 스킨 포장 수요는 세계적으로 증가하고 있습니다. 주요 촉진요인으로 풍부한 원료와 스킨 포장 시장의 빠른 기술 개발을 들 수 있습니다.

- 인도 포장 산업 협회(PIAI)에 따르면 인도의 스킨 포장 시장은 2025년 말까지 2,048억 1,000만 달러 이상의 규모가 된다고 합니다. 1인당 소비 지출이 증가하고 가볍고 내구성이 있으며 오염으로부터 보호할 수 있는 연질 플라스틱 포장의 우수한 제품에 대한 수요가 높아지고 있기 때문에 시장은 예측 기간을 통해 발전을 계속할 것으로 보입니다.

- 소비자가 더 긴 유통 기한과 제품의 더 나은 시인성을 원한다는 점도 시장을 견인하고 있습니다. 스킨 포장은 더 나은 제품 보호를 제공하고 제품의 무결성과 신선도를 유지합니다. 또한 상품의 가시성이 향상되므로 소비자는 실제 상품과 그 특성을 볼 수 있어 구매 의욕이 높아질 수 있습니다.

- 전자 제품과 부품은 물에 약하기 때문에 보호 포장이 필요하며 따라서 내수성이 있는 스킨 포장 수요는 높습니다. 또한 전기 제품을 손상이나 긁힘으로부터 본체를 보호할 수 있습니다. 게다가 공구나 자동차 부품 등의 공업 제품은 본체가 손상되기 쉽고 다양한 기상 조건에 노출되기 때문에 다양한 공업 제품의 포장 용도로 스킨 포장의 요구가 높아지고 있습니다.

- 지속가능한 포장은 포장 산업의 미래이며 환경친화적인 대안 탐구는 식품 산업의 최우선 과제입니다. 기존의 플라스틱으로 만들어진 생고기 포장이 기피되면서 산업이 친환경 솔루션으로 이동하고 있습니다. 2023년 4월, Stora Enso의 신제품 Trayforma BarrPeel(진공 스킨 포장용 배리어 코트 판지)은 신선식품을 재활용 가능한 판지 트레이로 포장할 수 있게 함으로써 포장 전체의 플라스틱 함량을 10% 이하로 줄이고 있습니다.

- 원료가격 변동과 식품포장용 플라스틱 사용에 관하여 정부가 부과하는 엄격한 규제가 시장의 성장을 억제할 가능성이 높습니다. 환경 친화적인 대체품을 이용할 수 있고 환경에 대한 우려가 높아지고 있다는 점도 시장 성장을 방해할 것으로 예상됩니다.

스킨 포장 시장 동향

식품 중에서도 고기 하위 부문이 주요 시장 점유율을 차지할 전망

- 스킨 포장은 기존의 진공 포장에서 파생된 최신 식육 보존 방법입니다. 이 방법에서는 생고기를 플라스틱 트레이에 놓고 고기가 놓여있는 동안 가열되는 열성형 플라스틱 필름으로 덮습니다. 이 공정은 포장이 수축하면서 정확하게 성형되므로 기포 발생을 방지하고 눈에 보이는 유출 가능성을 줄이며 제품의 보존성을 높일 수 있습니다.

- 이 기술은 소매점에서 구입할 수 있는 소량의 생고기, 다진 고기, 육류 가공품을 상품화하기 위해 고안되었습니다. 플라스틱 필름을 제품에 밀착시켜 소비자가 느끼는 모든 감각을 향상시킬 수 있습니다.

- 유엔의 지속가능한 개발 목표(SDGs)에 대한 의식이 증가함에 따라 유통 기한을 연장하고 식품 손실을 최소화하기 위해 슈퍼마켓 및 기타 소매점에서 스킨 포장이 점점 보편화되고 있습니다. 덩어리 고기는 구입할 때까지 오랫동안 선반에 비치되는 경향이 있기 때문에 스킨 포장 방식은 주로 가정에서 소비되는 슬라이스 고기 등이 아닌 덩어리 고기에 사용됩니다.

- 뼈에 찔리지 않고 유통 기한을 연장하며 상품을 확실히 고정하고 유통시에 육류를 보호할 수 있다는 점, 그리고 소비자가 상품을 확인할 수 있는 투명성이 스킨 필름의 주요 특징입니다. 머천다이징이나 유통기한에 대한 장점 외에도 스킨 포장 씰의 사이즈는 식육의 폐기나 반품을 줄입니다. 특히 식육 산업에서는 액 누출이나 씰 불량에 의한 소매점에서의 반품이 많습니다.

- 식육 및 절단 고기 포장 수요는 E-Commerce 붐에 의해 급속히 증가하고 있어 예측 기간 중에도 일정할 것으로 예상됩니다. 경제협력개발기구의 데이터에 따르면 세계 닭고기 소비량은 2022년 135.62킬로톤에서 증가하고 2028년에는 147.47킬로톤에 이를 것으로 예상됩니다. 이처럼 식육제품의 소비가 증가하고 있기 때문에 스킨 포장의 요구는 지속되고 있습니다.

아시아태평양이 시장에서 큰 점유율을 차지할 전망

- 조직화되는 소매업 및 전자상거래 부문이 확대되고 원료를 쉽게 입수할 수 있게 되면서 아시아태평양은 시장 진출 기업에게 유망한 성장 가능성을 가져올 것으로 예상됩니다. 중국, 인도, 인도네시아에서는 소비자의 구매력이 높아짐에 따라 포장 식품 수요가 증가할 것으로 예상되며 이는 시장 확대를 뒷받침할 것으로 예상됩니다.

- 중국의 스킨 포장 산업은 내수 호경기, 급속한 도시화, 생활 수준의 향상으로 성장하고 있습니다. 소비자는 보다 안전하고, 실용적이며, 개성적이고, 환경 친화적인 포장을 선호합니다. 중국 국가통계국에 따르면 중국 총 인구의 약 63.9%가 도시 지역에 살고 있습니다. 중국은 지난 수십년동안 도시화율이 꾸준히 상승하고 있습니다.

- 아시아태평양이 계속 발전함에 따라 기업은 아시아태평양에서의 존재감을 높이고 있습니다. 예를 들어 지속가능한 포장 솔루션의 선두주자인 Amcor는 중국의 혜주에 최첨단 생산 시설을 설립했습니다. 1억 달러 이상을 들여 건설된 59만 평방피트의 공장은 생산능력에서 중국 최대의 연질 포장시설로 아시아태평양 전역에서 높아지는 고객 수요를 충족하면서 Amcor의 능력을 높이고 있습니다.

- 인구 증가, 소득 수준 향상, 라이프 스타일 변화로 소비자 지출이 증가하면서 인도의 스킨 포장 제품 수요가 증가할 것으로 예상됩니다. 게다가 인터넷이나 텔레비전을 통한 미디어의 보급이 진행되어 농촌로부터의 포장 상품 수요도 높아지고 있습니다.

- 수요가 증가하고 식품 산업에서 신규 사업이 출현함에 따라 인도에서는 음식 및 식품에 사용되는 포장이 급증했습니다. Zomato와 Swiggy와 같은 식품 택배 서비스의 출시와 급속한 확대로 식품 및 음료 포장의 사용이 증가하고 있습니다. 스킨 포장으로 식품의 품질과 수준을 유지하면서 브랜드 인지를 강조하는 식품 포장이 상당히 선진화하고 있습니다.

- 인구가 증가하고 도시화됨에 따라 중국의 육류 수요는 현저하게 증가하고 있으며, 이는 육류의 신선도와 부드러움을 길게 유지하기 위한 다양한 유형의 스킨 포장 수요에 영향을 미치고 있습니다. 경제협력개발기구(OECD)에 따르면 중국의 1인당 식육 소비량은 증가하는 경향이 있습니다. 2021년에는 45.17킬로그램이었으나 2023년에는 48.28킬로그램으로 증가했으며 2029년에는 52.84킬로그램에 이를 것으로 예상됩니다.

- 보존성을 높이기 위해 고기, 치즈, 생선, 돼지고기, 해산물, 야채 등 대부분에 스킨 포장을 적용하고 있다는 점이 이 시장을 견인하고 있으며 이는 중국 고객의 기호 향상에 기인합니다. 중국 고객은 신선한 해산물을 점점 더 쉽게 구입하고 있습니다.

스킨 포장 산업 개요

스킨 포장 시장 경쟁 구도는 세분화되고 있으며, Amcor Group GmbH, Sealed Air Corporation, Clondalkin Flexible Packaging Orlando Inc., Plastopil Hazorea Co. 등 시장 진출 기업에 의한 R&D 비용 증가는 경쟁 우위를 확보하는 전략인 제품 차별화로 이어지고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

- 시장 개요

- 산업의 매력 - Porter's Five Forces 분석

- 공급기업의 협상력

- 소비자의 협상력

- 신규 진입업자의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

- 산업 가치사슬 분석

제5장 시장 역학

- 촉진요인

- Ready To Eat 포장 식품에 대한 수요 증가

- 풍미를 유지하는 포장에 대한 수요 증가

- 억제요인

- 환경에 대한 우려 증가와 플라스틱 사용에 관한 정부의 엄격한 규제

- 기술 스냅샷

- 스킨 포장 기계

- 최근의 스킨 포장 기술의 동향

제6장 시장 세분화

- 용도별

- 식품

- 육류

- 해산물

- 가공식품

- 치즈

- 공업 제품(전자 및 전기 부품 포함)

- 의료기기

- 내구 소비재

- 식품

- 지역별

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 프랑스

- 독일

- 아시아

- 중국

- 일본

- 인도

- 호주 및 뉴질랜드

- 라틴아메리카

- 브라질

- 멕시코

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 남아프리카

- 북미

제7장 경쟁 구도

- 기업 프로파일

- Plastopil Hazorea Co. Ltd

- Sealed Air Corporation

- Amcor Group GmbH

- MULTIVAC Sepp Haggenmller SE & Co. KG

- Klckner Pentaplast Ltd

- Flexopack SA

- Winpak LTD

- SUDPACK Holding GmbH

- Taghleef Industries Group

- KM Packaging Services Ltd

제8장 투자 분석

제9장 시장의 미래

CSM 25.02.13The Skin Packaging Market size is estimated at USD 13.07 billion in 2025, and is expected to reach USD 17.00 billion by 2030, at a CAGR of 5.4% during the forecast period (2025-2030).

Key Highlights

- Skin packaging is a state-of-the-art technique consisting of thin layers of plastic film over a thermoforming tray or manufactured plastic container. In addition to allowing customers to look at the product without any risk of contamination, this plastic film provides a very transparent layer of protection against air and moisture that may degrade products or cause them to spoil.

- The growing need to protect food, increase shelf life, reduce waste, and increase visibility is raising the demand for skin packaging from the food industry since it offers benefits, such as reliability, with durable trays, which support and protect products during shipping, storage, and display.

- The growing demand for the preservation of various meat and dairy products, such as cheese, cold cuts, and various forms of beef, is driving the skin packaging market. As vacuum skin packaging provides better durability, traditional packaging techniques have been phased out in various food industry applications in recent years. Moreover, it provides an additional layer that protects the food compared to conventional packaging solutions, increasing its adoption and supporting market growth.

- The demand for skin packaging has increased globally due to the growing understanding of the advantages of recycling and bioplastics. Key market drivers include the abundance of raw materials and the quickening pace of technical developments in the skin packaging market.

- According to the Packaging Industry Association of India (PIAI), the Indian skin packaging market will be worth more than USD 204.81 billion by the end of 2025. The market will continue to develop throughout the forecast period due to rising per capita spending and growing demand for superior products with flexible plastic packaging that is light and durable and can provide protection against contamination.

- In part, the market is driven by consumers wanting longer shelf life and better visibility of products. Skin packaging offers better product protection, preserving the integrity and freshness of the goods. It also gives the goods better visibility so that consumers can see the actual product and its characteristics, which may motivate purchases.

- Since electronic products and components are sensitive to water, they require protective armor. Hence, the demand for skin packaging is high due to its water-resistant properties. It also helps protect the body from damage and scratches in electrical products. Furthermore, industrial goods, such as tools and automotive parts, are prone to body damage and are exposed to dynamic weather conditions, increasing the need for skin packaging in different industrial goods packaging applications.

- Sustainable packaging is the future, and the quest for eco-friendly alternatives is a top priority in the food industry. Fresh meat packaging made from conventional plastic is facing pressure; hence, the industry is shifting toward eco-friendly solutions. In April 2023, Stora Enso's new Trayforma BarrPeel (barrier-coated paperboard for vacuum skin packaging) aimed to enable perishable products to be packaged in recyclable paperboard trays, reducing the overall plastic content of packaging to less than 10%.

- The fluctuating prices of raw materials and stringent regulations imposed by the government on the application of plastic for food packaging are likely to restrain market growth. The availability of environmentally friendly alternatives and rising environmental concerns are further expected to hamper market growth.

Skin Packaging Market Trends

The Meat Sub-segment Under Food is Expected to Hold a Major Market Share

- Skin packaging is a recent method of meat storage derived from traditional vacuum packaging. This method involves placing raw meats on a plastic tray and then covering them with a thermoformed plastic film that is heated simultaneously while the meat is being positioned. This process ensures that the upper skin is precisely shaped by shrinking it, thus preventing the formation of air and reducing the likelihood of visible exudation, increasing the product's shelf-life.

- This technique was created to commercialize small amounts of raw, minced, or meat preparations that can be bought in a retail store. The close fixation of the plastic film on the product also has the finality to enhance all sensory aspects perceived by the consumer since this technique is mainly used for self-service purchases.

- Skin packaging is becoming increasingly common in supermarkets and other retail outlets to extend expiration dates and minimize food loss, supported by the increased awareness of the UN Sustainable Development Goals (SDGs). As meat blocks tend to remain on the shelves long before being purchased, the skin packaging method is primarily used for blocks of meat rather than sliced meat for household consumption and other products.

- The ability to resist bone punctures and increase shelf life, hold the product in place, and protect the meat during distribution, as well as the clarity of the film that allows consumers to see the product, are the main characteristics of skin films. Aside from its advantages for merchandising and shelf life, the skin packaging seal's size reduces meat waste and returns. There can be many returns from retailers due to leaks or packages with poor seals, especially in the meat industry.

- The demand for meat and cut meat packaging is rapidly increasing due to the e-commerce boom, and it is expected to be constant during the forecast period. According to the Organisation for Economic Co-operation and Development data, poultry meat consumption worldwide is expected to reach 147.47 metric kilotons in 2028, an increase from 135.62 metric kilotons in 2022. Thus, due to the increasing consumption of meat products, there is a constant need for skin packaging.

Asia-Pacific is Expected to Hold Significant Share of the Market

- Due to the expanding organized retail and e-commerce sectors and the simplicity with which raw materials can be obtained, Asia-Pacific is anticipated to present prospective growth possibilities for market players. The demand for packaged food goods is expected to increase due to the rising consumer buying power in China, India, and Indonesia, which would boost market expansion.

- China's skin packaging industry is growing due to the country's booming economy, rapid urbanization, and rising standard of living. Consumers gravitate toward more secure, practical, distinctive, and environmentally responsible packaging. According to the National Bureau of Statistics of China, approximately 63.9% of China's total population resides in cities. China has experienced a steady increase in its urbanization rate over the past few decades.

- Companies are extending their presence in Asia-Pacific as the region continues to develop. For instance, Amcor, a leader in responsible packaging solutions, opened its brand-new, cutting-edge production facility in Huizhou, China. The 590,000 square foot factory, which cost over USD 100 million to build, is China's largest flexible packaging facility in terms of production capacity, enhancing Amcor's capabilities to fulfill rising client demand throughout Asia-Pacific.

- The rising population, rising income levels, and changing lifestyles are expected to increase consumer spending, raising the demand for skin packaging products in India. Moreover, the increased media penetration via the Internet and television is boosting the demand from the rural sector for packaged goods.

- With increased demand and the emergence of new businesses in the food and beverage industry, India witnessed a surge in the packaging used for food and beverages. Food and beverage packaging use has increased due to the launch and rapid expansion of food delivery services like Zomato and Swiggy. There have been considerable advancements in food packaging that emphasize brand recognition while upholding the caliber and level of the food product with contain skin packs.

- With the growing population and urbanization, the demand for meat in China is growing significantly, which impacts the demand for different types of skin packaging for meat to keep it fresh and tender for a longer duration. According to the Organisation for Economic Co-operation and Development, per capita meat consumption in China showed a growing trend. It was 45.17 kilograms in 2021, which increased to 48.28 kilograms in 2023; it is expected to reach 52.84 kilograms by 2029.

- The market is driven by the growing preference of Chinese customers for meat, cheese items, fish, pork, seafood, vegetables, and others that are mostly skin-packed to make them shelf-stable. Customers in the nation are becoming increasingly accustomed to purchasing fresh fish and seafood.

Skin Packaging Industry Overview

The competitive landscape of the skin packaging market is fragmented, consisting of several players like Amcor Group GmbH, Sealed Air Corporation, Clondalkin Flexible Packaging Orlando Inc., and Plastopil Hazorea Co. Increased R&D spending by market participants leads to product differentiation, which is a strategy to secure a competitive advantage.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rise in Demand for Ready-to-Consume Packaged Food Products

- 5.1.2 Growing Demand for Flavor Retaining Packaging

- 5.2 Market Restraint

- 5.2.1 Rising Concerns About the Environment and Stringent Government Regulations Regarding the Use of Plastic

- 5.3 Technology Snapshot

- 5.3.1 Skin Packaging Machinery

- 5.3.2 Recent Developments in Skin Packaging Technology

6 MARKET SEGMENTATION

- 6.1 By Application

- 6.1.1 Food

- 6.1.1.1 Meat

- 6.1.1.2 Fish and Seafood

- 6.1.1.3 Processed Food

- 6.1.1.4 Cheese

- 6.1.2 Industrial Goods (Including Electronic and Electrical Components)

- 6.1.3 Medical Devices

- 6.1.4 Durable Consumer Goods

- 6.1.1 Food

- 6.2 By Geography

- 6.2.1 North America

- 6.2.1.1 United States

- 6.2.1.2 Canada

- 6.2.2 Europe

- 6.2.2.1 United kingdom

- 6.2.2.2 France

- 6.2.2.3 Germany

- 6.2.3 Asia

- 6.2.3.1 China

- 6.2.3.2 Japan

- 6.2.3.3 India

- 6.2.3.4 Australia and New Zealand

- 6.2.4 Latin America

- 6.2.4.1 Brazil

- 6.2.4.2 Mexico

- 6.2.5 Middle East And Africa

- 6.2.5.1 Saudi Arabia

- 6.2.5.2 United Arab Emirates

- 6.2.5.3 South Africa

- 6.2.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Plastopil Hazorea Co. Ltd

- 7.1.2 Sealed Air Corporation

- 7.1.3 Amcor Group GmbH

- 7.1.4 MULTIVAC Sepp Haggenmller SE & Co. KG

- 7.1.5 Klckner Pentaplast Ltd

- 7.1.6 Flexopack SA

- 7.1.7 Winpak LTD

- 7.1.8 SUDPACK Holding GmbH

- 7.1.9 Taghleef Industries Group

- 7.1.10 KM Packaging Services Ltd