|

시장보고서

상품코드

1640476

FPSO : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)FPSO - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

■ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송일정은 문의해 주시기 바랍니다.

가격

※ 부가세 별도

한글목차

영문목차

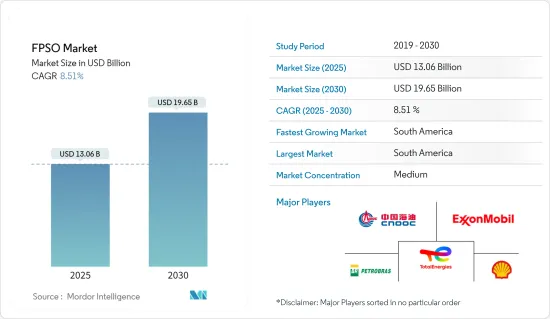

FPSO 시장 규모는 2025년에 130억 6,000만 달러로 추정되며, 예측 기간 중(2025-2030년) CAGR은 8.51%를 나타낼 전망이며, 2030년에는 196억 5,000만 달러에 이를 것으로 예측됩니다.

주요 하이라이트

- 중기적으로는 심해나 초심해 탐사 및 생산 활동 증가가 예측 기간 중 FPSO 시장을 견인할 것으로 보입니다.

- 한편, 높은 초기비용은 예측기간 동안 시장성장을 방해할 것으로 예상됩니다.

- 하지만 FPSO 시스템의 기술적 진보와 혁신은 FPSO 시장에 큰 기회를 가져올 것으로 기대됩니다.

- 남미는 해외 활동 증가로 FPSO 시장의 지배적인 지역이 될 것으로 예상됩니다.

FPSO 시장 동향

계약자 소유 부문이 시장을 독점할 전망

- FPSO의 조달 방법에는 주로 신규 제조, 기존 선박 개조, 기존 유닛 재배치의 세 가지가 있습니다. 이러한 옵션 중에서 FPSO의 재배치는 특정 분야에 맞게 고도로 맞춤화되므로 몇 가지 극복해야 할 과제가 있습니다. 그 결과, 운영자는 주로 신규 제조와 개조식 접근 방식을 선호하게 되었고 지난 20년간 이러한 서비스를 전문 지식을 가진 제3자 계약자에 의존하는 경우가 많았습니다.

- 계약자 소유 FPSO는 운영자 소유 FPSO 및 고정 플랫폼보다 비용면에서 유리합니다. FPSO의 설계, 건설 및 운영을 전문으로 하는 계약자는 규모의 경제를 실현하고 선대 이용률을 최적화하여 운영자의 비용을 절감할 수 있습니다. 따라서 계약자가 소유한 FPSO는 비용 효율적인 솔루션을 요구하는 운영자에게 매력적인 선택입니다.

- 계약자 소유 FPSO는 일반적으로 임대 가능하며 운영자에게 유전 개발의 유연성을 제공합니다. 임대를 통해 운영자는 최소한의 선행 자본 투자로 FPSO를 획득하고 배치할 수 있으므로 소규모 운영자와 생산 프로파일이 불확실한 프로젝트에 유리합니다.

- 해외활동의 활성화에 따라 탐광 및 생산활동에 드는 비용은 증가하고 있으며, FPSO 관련 업무는 계약자에게 위탁되게 되었습니다. 이를 통해 운영자는 FPSO의 운영을 전문가에게 맡기면서 가장 높은 가치를 창출할 수 있는 분야에 자원과 주의를 집중할 수 있습니다.

- 예를 들어 Baker Hughes Rig Count에 따르면 2023년 말의 해양 리그 수는 약 246기로 전년 대비 약 6.4% 증가하였으며 해외에서의 탐광 및 생산 활동 증가로 FPSO 수요가 높아지고 있습니다.

- 2023년 5월, 일본의 FPSO 공급업체인 MODEC은 브라질 오키 캄포스 해협의 BM-C-33 블록에 FPSO 선박을 공급하는 계약을 Equinor로부터 취득했습니다. MODEC은 2027년 완성을 목표로 하는 FPSO 납품에 더해 FPSO의 원유 생산 개시 초년도의 조업 및 보수 서비스를 Equinor에 제공합니다. 그 후 Equinor는 FPSO 운영 책임을 인계할 예정입니다.

- 세계에는 아직 발견되지 않았거나 탐사 단계에 있는 미개발 해양 매장이 여러 군데 존재합니다. 석유 및 가스 회사는 앞으로 이러한 미개발 석유 및 가스 매장량의 발견에 주력하기 때문에 FPSO 수요는 증가할 것으로 예상됩니다.

- FPSO에 대한 수요 증가와 다른 유형의 FPSO에 대한 이점으로 인해 계약자 소유의 FPSO가 예측 기간 동안 시장을 독점할 것으로 예상됩니다.

남미가 시장을 독점할 전망

- 남미는 세계 FPSO 시장에 가장 큰 영향을 미칠 것으로 예상됩니다. 특히 브라질과 가이아나가 해당 시장의 주요 국가로 부상하고 있어 최근 FPSO 수요가 크게 급증하고 있습니다.

- 남미는 특히 브라질과 가이아나에 해양석유 및 가스 매장량이 많습니다. 매장량은 심해와 초심해에 위치하고 있으며 효율적인 생산, 저장, 하역을 위해 FPSO가 필요합니다. 조사 지역에서는 대규모 발견과 생산이 이루어질 수 있기 때문에 FPSO에 대한 수요가 증가하고 있습니다.

- 예를 들어, 2024년 1월, Offshore Frontier Solution Pte Ltd는 남미 Uaru 유전에 배치될 ExxonMobil 부유식 원유생산 저장 하역 설비(FPSO)의 전기 시스템 및 관련 디지털 솔루션을 제공했으며 해당 시설은 가이아나 앞바다 약 200km에서 운영됩니다.

- 또한 남미에는 특히 브라질 산토스 분지와 캄포스 분지에 광대한 암염하층이 매장되어 있습니다. 매장층은 두꺼운 소금층 아래에 있어 탐사와 생산에 기술적 노력이 필요합니다. FPSO는 심해에서 안전하게 운영할 수 있으며 암염하층 유전의 복잡한 요구 사항을 처리할 수 있으므로 이러한 까다로운 환경에 적합합니다. 따라서 앞으로 조사 지역에서 심해와 초심해의 석유 및 가스 프로젝트가 탐사 및 생산됨에 따라 FPSO 수요는 늘어날 것으로 예상됩니다.

- 위 요인에 의해 예측기간 동안 남미가 FPSO 시장을 독점할 것으로 예상됩니다.

FPSO 산업 개요

FPSO 시장은 적당히 통합되어 있습니다. 시장 주요 기업으로는 Petroleo Brasileiro SA(Petroblas), CNOOC Ltd, TotalEnergies SE, Exxon Mobil Corp., Shell PLC 등이 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

목차

제1장 서론

- 조사 범위

- 시장의 정의

- 조사의 전제

제2장 조사 방법

제3장 주요 요약

제4장 시장 개요

- 소개

- 2029년까지 시장 규모 및 수요 예측(단위 : 달러)

- FPSO 가동 상황(지역별 및 오퍼레이터별) : 2023년

- 최근 동향과 개발

- 정부의 규제와 정책

- 시장 역학

- 촉진요인

- 해양석유, 가스탐사 및 생산활동 증가

- 에너지 수요 증가

- 억제요인

- 높은 초기 비용

- 촉진요인

- 공급망 분석

- Porter's Five Forces 분석

- 공급기업의 협상력

- 소비자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 세분화

- 소유별

- 사업자 소유

- 운영자 소유

- 수심별

- 천해

- 심해

- 초심해

- 지역별 시장 분석 {2028년까지 시장 규모 및 수요 예측(지역별)}

- 북미

- 미국

- 캐나다

- 멕시코

- 기타 북미

- 유럽

- 노르웨이

- 영국

- 러시아

- 네덜란드

- 프랑스

- 이탈리아

- 노르딕

- 독일

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 호주

- 인도네시아

- 말레이시아

- 태국

- 일본

- 베트남

- 기타 아시아태평양

- 남미

- 브라질

- 아르헨티나

- 베네수엘라

- 콜롬비아

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 나이지리아

- 알제리

- 카타르

- 남아프리카

- 이집트

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- M&A, 합작사업, 제휴, 협정

- 주요 기업의 전략

- 기업 프로파일

- FPSO 계약자

- Modec Inc.

- SBM Offshore NV

- BW Offshore Limited

- Teekay Offshore Partners LP

- Bluewater Holding BV

- Saipem SpA

- Petrofac Limited

- FPSO 운영자

- Petroleo Brasileiro SA(Petrobras)

- CNOOC Ltd

- TotalEnergies SE

- ExxonMobil Corp.

- Chevron Corporation

- Shell PLC

- BP PLC

- 시장 순위/점유율(%) 분석

- FPSO 계약자

제7장 시장 기회와 앞으로의 동향

- 기술의 진보와 혁신

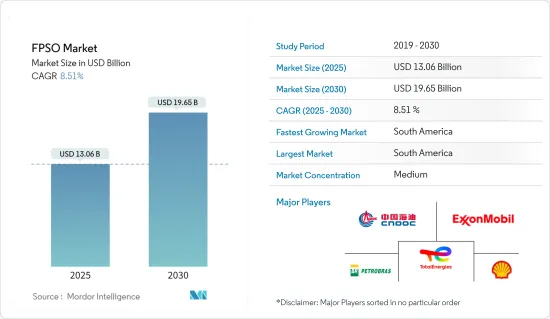

The FPSO Market size is estimated at USD 13.06 billion in 2025, and is expected to reach USD 19.65 billion by 2030, at a CAGR of 8.51% during the forecast period (2025-2030).

Key Highlights

- In the medium term, the increasing exploration and production activities in deep and ultradeep water depths are expected to drive the FPSO market during the forecast period.

- On the other hand, the high upfront cost is expected to hinder the market's growth during the forecast period.

- Nevertheless, the technological advancements and innovation in FPSO systems are expected to create huge opportunities for the FPSO market.

- South America is expected to be a dominant region for the FPSO market due to increasing offshore activities in the region.

FPSO Market Trends

The Contractor-owned Segment is Expected to Dominate the Market

- There are three primary methods for procuring FPSOs: new build, conversion of an existing vessel, and redeployment of an existing unit. Among these options, redeployment poses several challenges due to the highly customized nature of the FPSO for a specific field. As a result, operators have predominantly favored the new build and conversion approaches, often relying on third-party contractors with specialized expertise for these services over the past two decades.

- Contractor-owned FPSOs offer cost advantages over operator-owned FPSOs or fixed platforms. Contractors specializing in designing, constructing, and operating FPSOs can achieve economies of scale and optimize their fleet utilization, reducing operator costs. This makes contractor-owned FPSOs an attractive option for operators seeking cost-effective solutions.

- Contractor-owned FPSOs are typically available for lease, providing operators greater flexibility in field development. Leasing allows operators to access and deploy FPSOs with minimal upfront capital investments, benefiting smaller operators or projects with uncertain production profiles.

- With increasing offshore activities, the cost of exploration and production activities is increasing, and FPSO-related activities are being outsourced to contractors. This allows operators to allocate their resources and attention to areas where they can create the most value, leaving the FPSO operations to specialized contractors.

- For instance, according to Baker Hughes Rig Count, at the end of 2023, there were around 246 offshore rigs, which witnessed about 6.4% compared to the previous year, signifying an increase in offshore exploration and production activities, consequently driving the demand for FPSOs.

- In May 2023, MODEC, a Japanese FPSO supplier, secured a contract from Equinor to supply an FPSO vessel for the BM-C-33 block in the Campos Basin offshore Brazil. In addition to delivering the FPSO, which is expected to be completed by 2027, MODEC will provide Equinor with operations and maintenance services for the first year of the FPSO's oil production. Subsequently, Equinor plans to take over the operational responsibilities of the FPSO.

- There are several untapped offshore reserves globally that have not been discovered yet or are in the process of exploration. As oil and gas companies are focusing on discovering these untapped oil and gas reserves in the future, the demand for FPSO is expected to increase.

- With increasing demand for FPSO and its advantages over other types of FPSO, the Contractor-owned FPSO is expected to dominate the market during the forecast period.

South America is Expected to Dominate the Market

- South America is anticipated to exert the highest influence on the global FPSO market. Particularly, Brazil and Guyana have emerged as key players in this market, experiencing a significant surge in demand for FPSOs in recent years.

- South America has significant offshore oil and gas reserves, particularly in Brazil and Guyana. These reserves are located in deepwater and ultra-deepwater areas, requiring FPSOs for efficient production, storage, and offloading. The potential for large-scale discoveries and production in these regions drives the demand for FPSOs.

- For instance, in January 2024, Offshore Frontier Solution Pte Ltd awarded a contract for an electrical system and associated digital solutions on an ExxonMobil floating production storage and offloading (FPSO) vessel for the South American Uaru oil field. The unit will perform operations approximately 200 kilometers off the coast of Guyana.

- Moreover, South America has extensive pre-salt reserves, especially in Brazil's Santos and Campos Basins. These reserves are located beneath thick layers of salt, presenting technical challenges for exploration and production. FPSOs are well-suited for these challenging environments, as they can safely operate in deepwater and handle the complex processing requirements of pre-salt fields. Thus, in the future, with the upcoming deep and ultra-deep oil and gas projects' exploration and production in the region, demand for the FPSO is expected to grow.

- Therefore, as per the above points, South America is expected to dominate the FPSO market during the forecast period.

FPSO Industry Overview

The FPSO market is moderately consolidated. Some of the major players in the market are Petroleo Brasileiro SA (Petrobras), CNOOC Ltd, TotalEnergies SE, Exxon Mobil Corp., and Shell PLC.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 FPSOs in Operation, by Region and Operator, 2023

- 4.4 Recent Trends and Developments

- 4.5 Government Policies and Regulations

- 4.6 Market Dynamics

- 4.6.1 Drivers

- 4.6.1.1 Increasing Offshore Oil and Gas Exploration and Production Activities

- 4.6.1.2 Increasing Demand for Energy

- 4.6.2 Restraints

- 4.6.2.1 High Upfront Costs

- 4.6.1 Drivers

- 4.7 Supply Chain Analysis

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Consumers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitute Products and Services

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Ownership

- 5.1.1 Operator-owned

- 5.1.2 Contractor-owned

- 5.2 Water Depth

- 5.2.1 Shallow Water

- 5.2.2 Deep Water

- 5.2.3 Ultra-deep Water

- 5.3 Geography Regional Market Analysis {Market Size and Demand Forecast till 2028 (for regions only)}

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.1.4 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Norway

- 5.3.2.2 United Kingdom

- 5.3.2.3 Russia

- 5.3.2.4 Netherland

- 5.3.2.5 France

- 5.3.2.6 Italy

- 5.3.2.7 NORDIC

- 5.3.2.8 Germany

- 5.3.2.9 Spain

- 5.3.2.10 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Australia

- 5.3.3.4 Indonesia

- 5.3.3.5 Malaysia

- 5.3.3.6 Thailand

- 5.3.3.7 Japan

- 5.3.3.8 Vietnam

- 5.3.3.9 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Venezuela

- 5.3.4.4 Colombia

- 5.3.4.5 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 Nigeria

- 5.3.5.4 Algeria

- 5.3.5.5 Qatar

- 5.3.5.6 South Africa

- 5.3.5.7 Egypt

- 5.3.5.8 Rest of Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 FPSO Contractors

- 6.3.1.1 Modec Inc.

- 6.3.1.2 SBM Offshore NV

- 6.3.1.3 BW Offshore Limited

- 6.3.1.4 Teekay Offshore Partners LP

- 6.3.1.5 Bluewater Holding BV

- 6.3.1.6 Saipem SpA

- 6.3.1.7 Petrofac Limited

- 6.3.2 FPSO Operators

- 6.3.2.1 Petroleo Brasileiro SA (Petrobras)

- 6.3.2.2 CNOOC Ltd

- 6.3.2.3 TotalEnergies SE

- 6.3.2.4 ExxonMobil Corp.

- 6.3.2.5 Chevron Corporation

- 6.3.2.6 Shell PLC

- 6.3.2.7 BP PLC

- 6.3.3 Market Ranking/Share (%) Analysis

- 6.3.1 FPSO Contractors

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Technological Advancements and Innovations