|

시장보고서

상품코드

1640573

북미의 금속 캔 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)North America Metal Cans - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

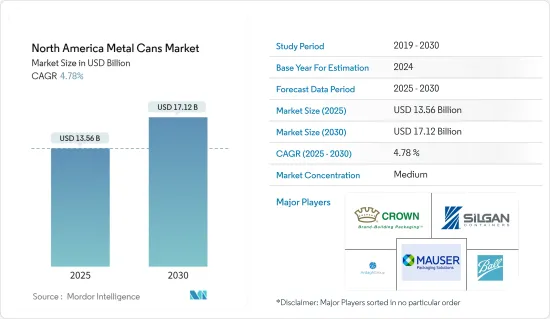

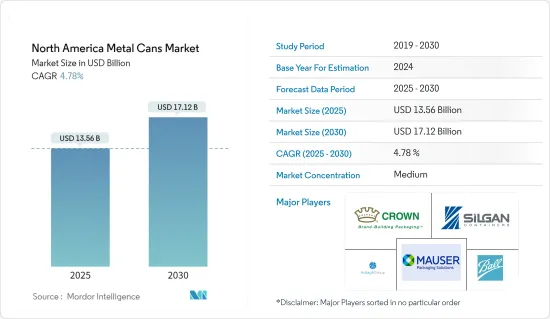

북미의 금속 캔 시장 규모는 2025년에 135억 6,000만 달러로 추정됩니다. 예측 기간(2025-2030년)의 CAGR은 4.78%로, 2030년에는 171억 2,000만 달러에 달할 것으로 예상되고 있습니다.

금속 캔 포장 시장에서 큰 점유율을 차지하는 식음료 업계는 COVID-19 팬데믹 속에서 필수품에 해당하기 때문에 대규모 수요가 나타나고 있습니다. COVID-19 팬데믹을 위해 지역 전체에서 실시된 봉쇄는 소비 습관의 상당한 변화를 사고 있습니다. 포장 식품, 고기, 야채, 과일에 대한 수요가 증가하고 있습니다.

주요 하이라이트

- 금속 캔은 이 지역의 많은 소비자들의 외출이 많은 라이프스타일에 최적인 포장 솔루션의 하나이며, 그 편리성이 가장 큰 장점으로 꼽힙니다. 유리는 깨지기 쉽기 때문에 주로 제한됩니다. 게다가 에너지 음료의 인기가 높아지고, 신제품 소개, 캔 가격과 재활용 가능성이 조사한 시장의 성장을 뒷받침하고 있습니다.

- 많은 브랜드가 새로운 에너지 음료를 출시합니다. 예를 들어, 북미 코카콜라는 2020년 코크 브랜드 최초의 에너지 음료 '코카콜라 에너지 체리'(미국 한정판)를 발표했습니다. 칼로리 제로의 것은 12 온스의 슬리크캔으로 전미에서 판매될 예정입니다.

- 게다가 알루미늄 협회와 제캔 협회(CMI)의 2020년 보고에 따르면 미국에서 알루미늄 캔의 업계 재활용률은 55.9%, 소비자의 재활용률은 46.1%입니다. 또한 재료의 가치는 1,210달러/톤을 차지합니다.

- 이 지역의 화장품 분야도 많은 화장품 및 퍼스널케어 제조업체가 자사 제품의 금속 캔 포장을 선호하기 때문에 금속 캔 시장의 성장을 견인하고 있습니다. 예를 들어, 해피 매거진에 따르면 2020년 미국 Unilever, Procter, and Gamble, Colgate Palmolive 등 주요 탈취제 공급업체의 판매량은 각각 3억 2,704만 달러, 2억 1,979만 달러, 3,849만 달러를 차지하고 있습니다.

- 금속 캔 포장 시장에서 큰 점유율을 차지하는 식음료 업계는 COVID-19가 대유행하는 가운데 필수품에 해당하기 때문에 엄청난 수요를 목격하고 있습니다. Store Brands가 발표한 2020년 조사에 따르면 미국에서는 COVID-19의 대유행으로 통조림 소비량이 96% 증가했습니다. 또한 냉동 저녁 식사 소비도 71% 증가했습니다.

북미의 금속 캔 시장 동향

음료가 큰 시장 점유율을 차지할 전망

- 금속 캔은 음료용으로 가장 널리 사용됩니다. 와인, 칵테일, 하드 음료, 청량 음료 통조림은 북미에서 휴대성의 필요성으로 금속 캔이 주류가되고 있습니다. 음료 산업에서 금속 캔의 용도는 음료의 특성에 따라 알코올 음료와 비 알코올 음료로 크게 나뉩니다. 맥주와 같은 주류는 역사적으로 금속 캔을 사용해 왔으며, 전통적으로 유리병에 담겨 제공되던 와인 같은 다른 종류의 주류도 점점 더 금속 캔을 채택하고 있습니다.

- 또한, 음료 캔 제조 업체는 캔 제조에 필요한 용량을 줄임으로써 경량화를 실현하고 있습니다. 금속 캔은 소다 포장에 필요한 탄산 가스 압력을 지원할 수 있습니다. 금속 캔은 또한 평방인치 당 90 파운드까지의 힘을 견딜 수 있습니다. 이 요인으로 인해 캔은 음료 산업에서 포장에 적합한 옵션이되었습니다.

- 금속 캔 제조 업체는 금속 캔의 부족으로 직면하는 공급망의 혼란을 해결하기 위해 북미에서 생산 능력을 강화하고 있습니다. 볼 사의 회장은 2023년까지 수요가 공급을 상회할 것으로 예측했습니다. 음료 산업에서 금속 캔의 적극적인 수요와 성장은 조사 대상 지역에서 이 부문에 대한 여러 투자에 불을 붙였습니다.

- 예를 들어, 2021년 9월, 포장 회사인 Ball Corporation은 라스베가스의 새로운 알루미늄 음료 포장 공장에 여러 해에 걸쳐 2억 9,000만 달러를 투자할 것이라고 발표했습니다. 이 공장에서는 다양한 크기의 캔을 생산할 예정입니다. 이 공장은 2022년 후반에 생산을 시작할 예정이며, 완전 가동 시에는 180명의 제조업 고용을 창출합니다.

- 또한 아더 그룹은 2020년 10월 미시시피의 생산 시설에 새로운 2개의 고속 음료 제조 라인을 설치할 수 있다고 발표했습니다. 이 회사는 이 투자가 하드셀러, 맥주, 에너지 음료 및 차를 포함한 다양한 음료에 대한 특허를 받은 정교한 디자인 라인의 생산에 대응하기 위한 것이라고 발표했습니다.

미국이 가장 큰 점유율을 차지

- 이 시장에서는 유통에 의한 캔 부족 문제로 인해 많은 기업들이 기존 공장에 새로운 라인을 추가하여 생산성 향상을 도모하고 있습니다. 예를 들어, Ball Corporation은 2020년 9월, 유통에 의해 가정에서의 소비가 확대되는 북미 시장에 대응하기 위해, 2021년 중반까지 펜실베니아주 핏스톤에 알루미늄 음료 포장 공장을 개설한다고 발표했습니다. 이 회사는 처음에는 2021년까지 60억 캔의 생산 확대를 계획했습니다. 볼사는 2021년 말까지 2개의 새로운 공장을 개설하고 미국 시설에 2개의 생산 라인을 추가하는 것을 목표로 하고 있습니다.

- 팬데믹으로 인해 많은 레스토랑과 바가 휴업했고, 캔 알코올 음료의 판매가 크게 증가했습니다. 또, 많은 음료 제조업체가 제품을 캔으로 변경했기 때문에 알루미늄캔 공급 체인에 부담이 걸렸습니다. 캔 수요에 대응하기 위해, 많은 제조업체가 계속 증가하는 수요에 대응하는 시설을 개설하고 있습니다.

- 예를 들어, 2021년 1월, 크라운 홀딩스는 버지니아주 헨리 국가와 브라질 남동부 미나스제라이스 주에 두 개의 음료통 공장을 신설하기 위해 투자했습니다. 버지니아의 공장은 스파클링 워터, 에너지 음료, 탄산 청량 음료, 차, 기능성 음료, 하드 셀 처, 맥주, 칵테일 등 다양한 카테고리에 해당하는 음료 캔을 공급합니다. 이 회사는 이 공장을 통해 북미 공급망을 확대하고 확대하는 표준 및 특수 음료 캔 시장에 대응합니다.

- 게다가 크라운 홀딩은 2021년 4월 미국에서 세 번째 음료 캔 생산 시설의 설립을 발표했습니다. 이 공장은 스파클링 워터, 에너지 음료, 탄산 청량 음료, 기능성 음료, 맥주 등의 캔을 생산합니다.

- 캔 제조업체 협회(CMI)의 음료 캔 제조업체와 알루미늄 캔 시트 제조업체 회원들은 2030년까지 재활용률 70% 등 미국의 야심적인 리사이클율 목표 달성을 위해 노력하고 있습니다. 이러한 새로운 목표는 음료용 알루미늄 캔의 순환성을 향상시키는 동시에 음료용 알루미늄 캔이 시장에서 가장 지속 가능한 포장이 되기 위한 업계의 헌신을 음료 제조업체와 소비자에게 보여주는 것입니다.

북미의 금속 캔 산업 개요

북미의 금속 캔 시장 경쟁은 중간 정도입니다. 시장에서 큰 점유율을 가진 대기업은 다양한 지역에서 고객 기반을 확대하고 있습니다. 또한 많은 기업들이 시장 점유율과 수익성을 높이기 위해 여러 기업과 전략적 및 협력적 이니셔티브를 형성하고 있습니다. 시장의 최근 동향을 몇 가지 소개합니다 :

- 2021년 3월 - Ball Corporation은 스페인의 주요 음료 기업인 Damm사와 제휴하여 북미에서 맥주 저장·포장용 알루미늄캔 ASI's(The aluminum stewardship initiative)를 도입했습니다. 이로 인해 회사의 판매 실적 증가가 기대됩니다.

- 2021년 2월 - 아다시 그룹은 금속 포장 사업을 고어즈 홀딩스 V사와 합병하여 상장 회사를 설립하는 것으로 합의했습니다. 이 합의는 독특한 목적의 인수 회사인 고어즈 홀딩스 V가 아다그의 금속 포장 부문과 합병하여 새롭게 아다그 메탈을 설립합니다. 아다그는 AMP의 주식 80%를 보유하고 거래 완료 시 최대 34억 달러의 현금을 받습니다. 이 거래에는 고어스 홀딩스 V의 최대 5억 2,500만 달러의 현금과 투자자가 주도하는 6억 달러의 제3자 할당 증자와 AMP가 조달하는 약 23억 달러의 신규 부채가 포함됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

- 시장 개요

- 업계의 매력도 - Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 진입업자의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

- 업계 밸류체인 분석

- 시장에 대한 COVID-19의 영향 평가

제5장 시장 역학

- 시장 성장 촉진요인

- 금속 포장의 높은 재활용률

- 캔 음식이 제공하는 편리성과 저렴한 가격

- 시장 성장 억제요인

- 대체 포장 솔루션의 존재

제6장 시장 세분화

- 재료 유형별

- 알루미늄

- 스틸

- 업계별

- 식품

- 음료

- 의약품

- 화장품 및 퍼스널케어

- 기타 업계별

- 국가별

- 미국

- 캐나다

제7장 경쟁 구도

- 기업 프로파일

- Crown Holdings Inc.

- Ball Corporation

- Silgan Containers LLC

- Mauser Packaging Solutions

- Ardagh Group SA

- DS Containers Inc.

- CCL Container Inc.

- Independent Can Company

- Technocap Group

- Can-Pack SA

- Allstate Can Corporation

- Envases Group

제8장 투자 분석

제9장 시장 전망

KTH 25.02.19The North America Metal Cans Market size is estimated at USD 13.56 billion in 2025, and is expected to reach USD 17.12 billion by 2030, at a CAGR of 4.78% during the forecast period (2025-2030).

With a significant share in the metal can packaging market, the food and beverage industry is witnessing massive demand amidst the COVID-19 pandemic, as the industry falls under the essential commodity. The lockdown enforced across the region due to the COVID-19 pandemic has bought a significant change in consumption habits. There has been an increasing demand for packaged food products, meat, vegetables, and fruits.

Key Highlights

- Metal cans are one of the perfect packaging solutions for the on-the-go lifestyle of many consumers in the region, and their convenience is topping the benefits list. These can be easily transported or carried to festivals, beaches, and outdoor and sporting events, whereas glass is mainly restricted due to its breakability. In addition, the increasing popularity of energy drinks, the introduction of new products, and the price and recyclability of cans augment the studied market growth.

- Many brands are introducing new energy drinks. For instance, in 2020, Coca-Cola North America unveiled the first-ever energy drink under the Coke brand Coca-Cola Energy Cherry a flavor available exclusively in the United States. Their zero-calorie counterparts will be available nationwide in 12-oz. sleek cans.

- Furthermore, according to the Aluminum Association and Can Manufacturers Institute (CMI), 2020 report, the industry recycling rate of aluminum can account for 55.9% in the United States, and the Consumer recycling rate of aluminum can account for 46.1%. In addition, the value of material accounted for USD 1,210/tons.

- The cosmetic segment in the region is also driving the growth of the metal cans market in the area as many cosmetic and personal care manufacturers prefer metal cans packaging for their products. For instance, according to Happi Magazine, the unit sales of leading deodorant vendors such as Unilever, Procter, and Gamble, Colgate Palmolive in the United States in 2020 accounted for USD 327.04 million, USD 219.79 million, and USD 38.49 million, respectively.

- The food and beverage industry, with a major share in the metal, can packaging market, has witnessed huge demand amidst the COVID-19 pandemic, as the industry falls under the essential commodity. According to a 2020 survey published by Store Brands, the consumption of canned food due to the Covid-19 pandemic increased by 96% in the United States. Also, frozen dinners consumption also increased by 71%.

North America Metal Cans Market Trends

Beverage is Expected to Account For Significant Market Share

- Metal cans are most widely used for beverages. The most notable trend of canned wine, cocktails, hard drinks, and soft drinks is packaged in metal, driven by the need for portability in North America. The usage of metal cans in the beverage industry can be widely classified into alcoholic drinks and non-alcoholic drinks based on the nature of the beverage. Alcoholic beverages, such as beer, have historically used metal cans, while other kinds of liquor, like wine, traditionally served in glass bottles, are increasingly adopting metal cans.

- Moreover, beverage can manufacturers have reduced the weight by reducing the gauge required to fabricate the cans. Metal cans can support the carbonation pressure that is needed to package soda. Metal cans also resist forces up to 90 pounds per square inch. This factor makes the cans the favored choice for packaging in the beverage industry.

- Metal can manufacturers are increasing the production capacity in North America to address the supply chain disruption faced due to the shortage in metal cans. The President of the Ball Corporation has identified the demand to outstrip the supply until 2023. The aggressive demand and growth of metal cans in the beverage industry sparked multiple investments in the sector in the studied region.

- For instance, in September 2021, Packaging company Ball Corporation announced an investment of USD 290 million over the course of multiple years into a new aluminum beverage packaging plant in Las Vegas. The plant is expected to create a range of can sizes. The facility is scheduled to begin production in late 2022 and will create 180 manufacturing jobs when it is fully operational.

- Further, Ardagh Group announced in October 2020 that the two new high-speed beverages could manufacture lines in its production facility in Mississippi. The company announced that the investment is aimed to cater to the production of its patented sleek design line for various beverages, including hard seltzers, beer, energy drinks, and tea.

United States Accounts for the Largest Share

- Many companies in the market are adding new lines to existing plants and are making productivity enhancements because of the can shortage issues due to the pandemic. For instance, in September 2020, Ball Corporation announced that it would open an aluminum beverage packaging plant in Pittston, Pennsylvania, by mid-2021 to serve the North American market as the at-home consumption grows due to the pandemic. The company initially planned a 6 billion can output expansion by 2021. Ball Corporation is looking forward to opening two new plants and adding two production lines to the United States facilities by the end of 2021.

- Many restaurants and bars were closed with the pandemic, due to which canned alcoholic beverages witnessed a significant increase in sales. Also, many beverage manufacturers shifted their products into cans, which has put a strain on the aluminum can supply chain. To cater to the demand for cans, many manufacturers have been opening facilities to meet this ever-growing demand.

- For instance, in January 2021, Crown Holdings invested in the two new beverage can plant in Henry Country, Virginia, and Minas Gerais State, Southeast Brazil. The plant in Virginia will be supplying beverage cans to serve various categories, including sparkling water, energy drinks, carbonated soft drinks, tea, functional beverages, hard seltzers, beer, and cocktails. The company expands its North American supply network with the plant to address the growing standard and specialty beverage cans market.

- Additionally, in April 2021, Crown Holding unveiled its plan to build its third new beverage can production facility in the United States. The plant will produce cans for sparkling waters, energy drinks, carbonated soft drinks, functional beverages, beers, among other beverages.

- Can Manufacturers Institute (CMI) beverage can manufacturer and aluminum can sheet producer members are committing to achieving ambitious U.S. recycling rate targets, including a 70% recycling rate by 2030. These new targets will improve the circularity of the aluminum beverage can while demonstrating to beverage companies and consumers the industry's dedication to ensuring the aluminum beverage can remain the most sustainable package on the market.

North America Metal Cans Industry Overview

The North America Metal Cans market is moderately competitive. The major players with a significant share in the market are expanding their customer base across various regions. In addition, many companies are forming strategic and collaborative initiatives with multiple companies to increase their market share and profitability. Some of the recent developments in the market are:

- March 2021 - Ball Corporation, along with the partnered company Damm, one of the leading beverage companies in Spain, introduced ASI's(The aluminum stewardship initiative) aluminum cans for storage and packaging of beer in North America. This is expected to increase the sales performance of the company.

- February 2021 - Ardagh Group agreed to merge its metal packaging business with Gores Holdings V, creating a publicly listed company. The agreement will see Gores Holdings V, a unique purpose acquisition company, merge with Ardagh's metal packaging division to form the newly created Ardagh Metal. Ardagh will retain an 80% stake in AMP and receive up to USD 3.4 billion in cash when the transaction completes. The deal includes up to USD 525 million in cash from Gores Holdings V and USD 600 million in a private placement led by investors, along with approximately USD 2.3 billion of new debt raised by AMP.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of COVID -19 Impact on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 High Recyclability Rates of Metal Packaging

- 5.1.2 Convenience and Lower Price Offered by Canned Food

- 5.2 Market Restraints

- 5.2.1 Presence of Alternate Packaging Solutions

6 MARKET SEGMENTATION

- 6.1 By Material Type

- 6.1.1 Aluminum

- 6.1.2 Steel

- 6.2 By End-user Vertical

- 6.2.1 Food

- 6.2.2 Beverage

- 6.2.3 Pharmaceuticals

- 6.2.4 Cosmetic and Personal Care

- 6.2.5 Other End-user Verticals

- 6.3 By Country

- 6.3.1 United States

- 6.3.2 Canada

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Crown Holdings Inc.

- 7.1.2 Ball Corporation

- 7.1.3 Silgan Containers LLC

- 7.1.4 Mauser Packaging Solutions

- 7.1.5 Ardagh Group S.A.

- 7.1.6 DS Containers Inc.

- 7.1.7 CCL Container Inc.

- 7.1.8 Independent Can Company

- 7.1.9 Technocap Group

- 7.1.10 Can-Pack SA

- 7.1.11 Allstate Can Corporation

- 7.1.12 Envases Group