|

시장보고서

상품코드

1641957

디지털 프로세스 자동화 : 시장 점유율 분석, 산업 동향, 성장 예측(2025-2030년)Digital Process Automation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

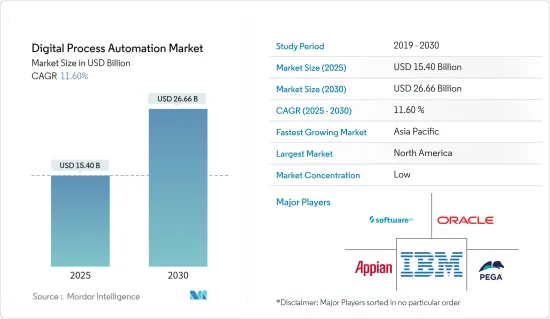

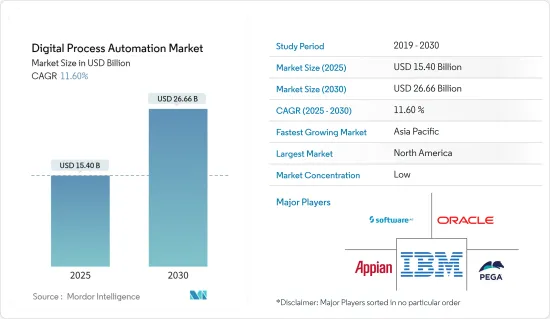

디지털 프로세스 자동화 시장 규모는 2025년에 154억 달러로 추정되며, 예측 기간(2025-2030년)의 CAGR은 11.6%로, 2030년까지 266억 6,000만 달러에 달할 것으로 예측됩니다.

신기술의 동향과 가속에 따라, 가상세계와 물리세계의 융합이 새로운 비즈니스 모델을 창출하고 있습니다. 제조업체 각 회사는 디지털 트윈과 같은 디지털 서비스와 제품을 판매하는 새로운 비즈니스 모델을 도입하고 있습니다.

주요 하이라이트

- 비즈니스 효율성을 개선하고 비즈니스 프로세스를 간소화하는 것은 모든 산업 조직에 최우선 과제입니다. 추론에 따르면, 이 효율성의 중요성은 DPA 솔루션 수요를 촉진하고 있습니다. 수작업과 반복 작업을 자동화하고 최적화함으로써 기업은 실수를 줄이고 병목 현상을 제거하고 공정 효율을 높일 수 있습니다. 기업은 워크플로우를 자동화하고 프로세스를 표준화함으로써 납기 단축, 생산성 향상, 비용 절감을 실현할 수 있습니다. 고객 경험 향상, 운영 우수성 추진, 변화하는 시장 경쟁 유지를 목표로 하는 기업의 경우 DPA 솔루션의 필요성이 높아질 것으로 예상됩니다.

- DPA 솔루션의 또 다른 중요한 시장 성장 촉진요인은 기업이 지속적으로 디지털 변환을 진행하고 있다는 것입니다. 추론에 따르면 기업은 업무 변화, 소비자 경험 향상, 경쟁 우위 획득을 목표로 디지털 기술 도입을 가속화하고 있습니다. 조직의 기본 비즈니스 활동을 디지털화하고 자동화할 수 있는 DPA는 이러한 변화에 매우 중요한 역할을 합니다. DPA 솔루션은 수작업을 자동화하고, 시스템과 용도을 통합하고, 프로세스 성능을 실시간으로 시각화함으로써 엔드 투 엔드 프로세스 자동화와 민첩성을 제공합니다. DPA의 요구는 디지털 기술을 활용하고 운영의 디지털 성숙도를 달성하고자 하는 조직의 요구에 부응하고 있습니다.

- 레거시 시스템과 복잡한 IT 환경은 DPA 솔루션을 채택하는 데 큰 부담을 줄 수 있습니다. 추론에 따르면 많은 조직은 기존 시스템, 용도 및 기술을 도입하고 있지만, 이들은 DPA 플랫폼과 쉽게 통합할 수 있도록 설계되지 않았습니다. 이러한 레거시 시스템에는 DPA 솔루션과 원활하게 연결하는 데 필요한 API(Application Programming Interface) 및 최신 아키텍처가 없으므로 통합이 어려워 시간이 오래 걸릴 수 있습니다. 또한 일부 조직에서는 사용자 지정 및 고유한 소프트웨어가 많아 시중에서 판매되는 DPA 도구와 호환되지 않을 수 있습니다.

- 팬데믹은 많은 섹터에서 DPA 솔루션 도입 확대를 촉구했으나 예산 제약과 우선순위 변동을 초래한 조직도 있었습니다. 추론에 따르면, 유행의 영향을 크게 받은 기업은 비용 절감책이나 필수적인 업무에 집중하는 등 당면 과제를 해결하기 위해 자원을 활용했을 가능성이 있습니다. 그 결과 DPA 솔루션의 배포가 지연되거나 계획 중인 프로젝트가 지연될 수 있습니다. 게다가 재정난에 처한 조직에서는 DPA를 포함한 신기술에 투자하는 예산이 제한될 수 있습니다. 또한 러시아 우크라이나 전쟁이 포장 생태계 전체에 미친 영향도 있었습니다.

디지털 프로세스 자동화 시장 동향

비즈니스 프로세스 관리(BPM) 채택 확대로 소기업의 성장 속도가 높아질 전망

- BPM 솔루션을 채택하면 조직이 기존 비즈니스 프로세스를 더 잘 이해하고 개선해야 할 영역을 파악할 수 있습니다. 추론에 따르면 조직은 BPM 이니셔티브를 도입함에 따라 프로세스 자동화와 최적화의 이점을 더욱 강력하게 인식하게 됩니다. 이러한 의식은 효율성, 생산성 및 민첩성 향상을 달성하기 위해 프로세스를 자동화할 필요성을 조직이 인식함에 따라 DPA 솔루션에 대한 수요를 창출합니다.

- BPM 솔루션은 디지털 전환 이니셔티브의 초석 역할을 하며 기업이 많은 부서와 플랫폼에 걸쳐 업무를 통합하고 간소화하는 데 도움이 됩니다. 추론에 따르면 기업이 BPM을 통합하면 완전한 프로세스 오케스트레이션과 자동화의 이점을 더욱 강력하게 인식하게 됩니다. 이 통찰을 통해 BPM 플랫폼과 쉽게 연결할 수 있는 DPA 시스템에 대한 수요가 증가하고 자동화 기능이 확대되고 기업은 자동화 생태계 전체에 액세스할 수 있습니다.

- BPM 이니셔티브는 종종 변화하는 소규모 비즈니스 요구와 시장 역학에 대응하기 위해 프로세스의 확장과 적응을 수반합니다. 추론에 따르면 기업은 BPM 이니셔티브를 지원하는 확장 가능하고 유연한 자동화 솔루션의 중요성을 인식하고 있습니다. DPA 솔루션은 단순한 것부터 복잡한 것까지 다양한 프로세스를 자동화하는 데 필요한 확장성과 유연성을 제공하고 진화하는 비즈니스 요구 사항을 충족합니다. BPM의 도입에 의해 조직의 자동화 요구의 증대에 대응할 수 있는 확대성과 적응성을 갖춘 DPA 솔루션 수요가 높아지고 있다

- BPM은 지속적인 프로세스 개선 문화를 조성하고 조직이 정기적으로 프로세스를 평가하고 강화하도록 촉구합니다. 추론에 따르면 조직은 BPM을 채택함에 따라 지속적인 개선 노력을 지원하는 자동화 솔루션을 추구할 것입니다. DPA 솔루션은 자동화된 프로세스를 모니터링, 분석 및 최적화할 수 있어 효율성 향상과 장기적인 성능 개선을 촉진합니다. BPM의 채택은 지속적인 프로세스 개선을 촉진하고 데이터 중심의 의사 결정을 위한 분석과 통찰력을 제공하는 DPA 솔루션 수요를 촉진합니다.

- 코로나바이러스(COVID-19)의 유행 중, 전시회 기업은 2020년과 2021년에 세계적으로 일부의 대면식 이벤트를 중지해, 디지털 형식의 모색을 우선했습니다. 2021년 6월에 실시된 조사에 따르면 세계 전시장의 80%가 기존 전시를 보완하기 위해 디지털 서비스와 제품을 도입했습니다. 한편, 서비스 제공업체의 45%는 사내 절차와 워크플로우를 디지털 프로세스로 변환하는 데 의문을 제기합니다.

북미가 시장에서 큰 점유율을 차지

- 이 지역에는 대규모 디지털 프로세스 자동화 벤더가 존재하기 때문에 북미는 시장 확대에 크게 기여할 것으로 예상됩니다. 이 지역의 디지털 프로세스 자동화 시장의 성장을 초래하는 주요 동향은 첨단 감지 기술 수요를 높이는 다양한 포장을 포함하며, 이는 자동화 제품 증가에 직접적인 영향을 미칩니다.

- 미국은 기술 향상과 세계 공급망/물류의 간소화로 현저하게 성장하고 있습니다. 이러한 국제 물류 네트워크의 출현은 미국 제조업체가 완제품과 원료를 세계 어디에서나 효율적이고 효과적으로 배송할 수 있게 되었습니다는 것을 의미합니다.

- 이 지역에서는 이러한 가능성을 활용하기 위해 제휴, 합병, 인수가 급증하고 있습니다. 이러한 투자의 기본 원동력은 새로운 기술과 배포 옵션의 지속적인 성장입니다.

- 2022년 8월, 디지털화, 판매 성장, 시스템 통합, 비즈니스 프로세스 자동화에 대한 고객의 비전을 이끄는 기술 컨설팅 및 소프트웨어 개발 회사인 Sigma Solve는 북미 전역의 기업 손에 통합 디지털 기능과 혁신을 제공하는 기능이 풍부한 플랫폼을 제공하는 Liferay DXP와 전략적 파트너십을 맺었습니다. Sigma Solve의 디지털 변환 방식은 Liferay의 DXP 플랫폼과 완벽하게 통합됩니다.

- 이 추세는 미국 제조업체와 국제 경쟁자의 경제적 기회를 크게 증가시켰습니다. Robotic Process Automation(RPA)은 기업이 모든 비즈니스 부문에서 빠르게 변화하는 속도에 대응할 수 있도록 하는 중요한 기술 중 하나입니다. RPA는 복잡한 작업의 작업, 프로세스 및 워크플로를 자동화하는 가상 에이전트를 설명합니다.

디지털 공정 자동화 산업 개요

디지털 공정 자동화 시장은 세분화되어 있습니다. 신제품 출시와 지속적인 혁신에 대한 주력은 주요 기업이 채택하는 전략의 일부입니다. 주요 진출기업은 IBM Corporation, Pegasystems Inc., Appian Corporation, Oracle Corporation 등입니다. 최근 시장 개척 동향은 다음과 같습니다.

- 2023년 3월 - 이집트의 주요 네트워크 제공업체인 Telecom Egypt(TE)은 IBM과 협력하여 지능형 자동화 기술을 통합하고 모바일, 고정, 코어 네트워크에 걸친 모든 운영 지원 시스템(OSS)에 통합 솔루션을 제공한다고 발표했습니다. RedHat OpenShift에서 실행되는 IBM Cloud Pak for Watson AIOps를 사용하고 TE를 통한 IBM Robotic Process Automation(RPA) 솔루션의 구현을 계획하고 있습니다. 이 솔루션은 TE가 전체 IT 인프라의 전반적인 모습을 파악하고 신속한 혁신, 운영 비용 절감, 네트워크 관련 이벤트 문제 해결 및 해결에 소요되는 시간을 단축하는 데 도움이 됩니다.

- 2022년 2월 - 산업을 선도하는 4/5G 프라이빗 무선 네트워킹 솔루션과 관련 디지털 서비스를 기업에 제공하고 최첨단의 새로운 서비스를 공동으로 개발하기 위해 Nokia와 Atos의 세계 협력 관계가 발족. 새로운 작업 방법을 촉진함으로써 양사의 협력은 기업의 업무 효율성 향상을 지원합니다. Atos 또는 Nokia 서버에서 호스팅되는 이 통합 제품은 에지 컴퓨팅과 클라우드 컴퓨팅 산업 리더인 두 회사의 강점을 융합하여 4.0 산업 혁명으로 전환하는 기업을 지원합니다. 이 파트너십은 최근에 Atos가 AI의 선구자인 Ipsotek과 비교할 수 없는 IP 및 소프트웨어 능력을 인수함으로써 강화된 Atos AI 컴퓨터 비전 플랫폼과 산업 등급 사설 무선 연결 및 용도 플랫폼 Nokia Digital Automation Cloud(DAC)를 활용하는 것입니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 시장 개요

- 산업의 매력 - Porter's Five Forces 분석

- 신규 진입업자의 위협

- 소비자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

- 시장에 대한 COVID-19의 영향 평가

- 시장 성장 촉진요인

- 효율적인 백엔드 프로세스를 위한 비즈니스 프로세스의 자동화 수요 증가

- 접근성 향상을 위한 저코드 자동화 채용 증가

- 시장 성장 억제요인

- 숙련 노동자의 부족

제5장 시장 세분화

- 컴포넌트별

- 솔루션

- 서비스별

- 전개별

- 온디맨드

- 온프레미스

- 조직 규모별

- 중소기업

- 대기업

- 최종 사용자별

- 은행 및 금융 서비스 보험(BFSI)

- 제조업

- IT 및 통신

- 항공우주 및 방위

- 의료

- 소매 및 소비재

- 기타

- 지역

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

제6장 경쟁 구도

- 기업 프로파일

- IBM Corporation

- Bizagi Group Limited

- Pegasystems Inc.

- Appian Corporation

- Oracle Corporation

- Software AG

- DST Systems Inc.

- OpenText Corporation

- Newgen Software Technologies Ltd.

- TIBCO Software Inc.

제7장 투자 분석

제8장 시장의 미래

SHW 25.02.19The Digital Process Automation Market size is estimated at USD 15.40 billion in 2025, and is expected to reach USD 26.66 billion by 2030, at a CAGR of 11.6% during the forecast period (2025-2030).

As new technologies are trending and accelerating, merging the virtual and physical worlds creates new business models. Manufacturers are introducing new business models under which they sell digital services and products, such as digital twins.

Key Highlights

- Improving operational effectiveness and simplifying business processes are top priorities for organizations across all industries. According to inference, this emphasis on efficiency drives the demand for DPA solutions. By automating and optimizing manual and repetitive tasks, firms may lower errors, get rid of bottlenecks, and boost process efficiency. Organizations can achieve faster turn-around times, increased productivity, and cost savings by automating workflows and standardizing processes. The need for DPA solutions is anticipated to increase as companies look to enhance client experiences, drive operational excellence, and maintain their competitiveness in a changing market.

- Another significant market driver for DPA solutions is organizations' continual digital transformation path. According to inference, businesses are embracing digital technology at a faster rate to revolutionize their operations, improve consumer experiences, and gain a competitive advantage. By enabling organizations to digitize and automate their fundamental business activities, DPA plays a crucial part in this shift. DPA solutions enable organizations to achieve end-to-end process automation and agility by automating manual operations, linking systems and applications, and offering real-time visibility into process performance. The need for DPA is fueled by organizations' need to utilize digital technology and attain operational digital maturity.

- Legacy systems and complex IT environments can pose a significant restraint on the adoption of DPA solutions. Inference suggests that many organizations have existing systems, applications, and technologies in place that are not designed to easily integrate with DPA platforms. These legacy systems may lack the necessary APIs (Application Programming Interfaces) or modern architecture to seamlessly connect with DPA solutions, making integration challenging and time-consuming. Additionally, organizations may have heavily customized or proprietary software that is not easily compatible with off-the-shelf DPA tools.

- While the pandemic drove increased adoption of DPA solutions in many sectors, it also introduced budget constraints and shifting priorities for some organizations. Inference suggests that businesses heavily impacted by the pandemic may have diverted resources to address immediate challenges, such as cost-cutting measures or focusing on essential operations. This could have slowed down the adoption of DPA solutions or led to delays in planned projects. In addition, organizations that experienced financial difficulties may have limited budgets for investing in new technologies, including DPA. There has also been an impact of the Russia-Ukraine war on the overall packaging ecosystem.

Digital Process Automation Market Trends

Small Enterprises are expected to grow at a higher pace on back of growing adoption of Business Process Management (BPM)

- The adoption of BPM solutions helps organizations gain a better understanding of their existing business processes and identifies areas for improvement. Inference suggests that as organizations implement BPM initiatives, they become more aware of the benefits of process automation and optimization. This awareness creates a demand for DPA solutions as organizations recognize the need to automate their processes to achieve greater efficiency, productivity, and agility.

- BPM solutions frequently act as the cornerstone for digital transformation initiatives, helping businesses to integrate and streamline their operations across many divisions and platforms. Inference implies that when businesses embrace BPM, they become more aware of the benefits of complete process orchestration and automation. This insight increases demand for DPA systems that can easily link with BPM platforms, extending automation capabilities and giving businesses access to a whole automation ecosystem.

- BPM initiatives often involve scaling and adapting processes to meet changing small business needs and market dynamics. Inference suggests that organizations recognize the importance of scalable and flexible automation solutions to support their BPM efforts. DPA solutions offer the scalability and flexibility required to automate a wide range of processes, from simple to complex, and accommodate evolving business requirements. The adoption of BPM drives the demand for DPA solutions that can scale and adapt to support the organization's growing automation needs.

- BPM fosters a culture of continuous process improvement, encouraging organizations to regularly evaluate and enhance their processes. Inference suggests that as organizations embrace BPM, they seek automation solutions that support their continuous improvement efforts. DPA solutions enable organizations to monitor, analyze, and optimize their automated processes, driving efficiency gains and performance improvements over time. The adoption of BPM fuels the demand for DPA solutions that facilitate ongoing process improvement and provide analytics and insights for data-driven decision-making.

- During the coronavirus (COVID-19) epidemic, exhibition companies globally stopped some in-person events in 2020 and 2021 in favor of exploring digital formats. According to research conducted in June 2021, 80 percent of global exhibition venues incorporated digital services or products to complement their existing displays. Meanwhile, 45 percent of service provider organizations questioned converting internal procedures and workflows into digital processes.

North America to Account for a Significant Market Share in the Market

- Due to the region's large digital process automation vendors, North America is expected to contribute significantly to market expansion. The major trends responsible for the growth of the digital process automation market in the region include the diverse packaging that increases demand for advanced sensing technology, which will directly impact the increase of automated products.

- The United States is significantly growing due to improved technology and streamlined global supply chains/logistics. This emergence of international logistics networks means that United States manufacturers can now efficiently and effectively deliver the finished products and raw materials anywhere around the world.

- The region has witnessed a surge of partnerships, mergers, and acquisitions to capitalize on these possibilities. The fundamental driver of these investments has been the continued growth of new technologies and deployment options.

- In August 2022, Sigma Solve, a technology consulting and software development company that guides clients' visions for digitization, sales growth, system integration, and business process automation, has formed a strategic partnership with Liferay DXP, which will provide a feature-rich platform that puts integrated digital capabilities and innovation in the hands of businesses across North America. Sigma Solve's digital transformation approach integrates perfectly with Liferay's DXP platform.

- This trend has massively increased the economic opportunities of US manufacturers and international competitors. Robotic process automation (RPA) is one key technology enabling companies to address the fast pace of change across all business areas. RPA provides virtual agents to automate tasks, processes, and workflows for complex work.

Digital Process Automation Industry Overview

The digital process automation market is fragmented. New product launches and focuses on continuous technology innovations are some strategies adopted by the major players. Key players are IBM Corporation, Pegasystems Inc., Appian Corporation, Oracle Corporation, etc. Recent developments in the market are

- March 2023 - Leading network provider in Egypt, Telecom Egypt (TE), announced that it is collaborating with IBM to integrate intelligent automation technologies to provide a unified solution for all of its operations support systems (OSS) across mobile, fixed, and core networks. The use of IBM Cloud Pak for Watson AIOps running on RedHat OpenShift and the implementation of IBM Robotic Process Automation (RPA) solutions by TE are both planned. The solution will be created to give TE a complete picture of its whole IT infrastructure and to assist them in fast innovating, lowering operational costs, and reducing the amount of time needed to troubleshoot and resolve network-related events.

- February 2022 - A global cooperation between Nokia and Atos was launched to offer enterprises industry-leading 4/5G private wireless networking solutions, along with related digital services, and to collaborate on the creation of new, cutting-edge services. By facilitating new working methods, our cooperation will assist businesses in achieving increased operational efficiency. The combined product, which is hosted on servers from Atos or Nokia, combines the strengths of the two industry leaders in edge and cloud computing to support businesses as they transition to the 4.0 industrial revolution. The partnership makes use of the Atos AI computer vision platform, which has recently been strengthened by Atos' acquisition of the AI pioneer Ipsotek and its unmatched IP and software capabilities, as well as the industrial-grade private wireless connectivity and application platform Nokia Digital Automation Cloud (DAC).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Assessment of the Impact of COVID-19 on the Market

- 4.4 Market Drivers

- 4.4.1 Increase Demand of Automating Business Process for Efficient Back-end process

- 4.4.2 Increase Adoption of Low Code Automation for Greater Accessibility

- 4.5 Market Restraints

- 4.5.1 Lack of Skilled Workforce

5 MARKET SEGMENTATION

- 5.1 By Component

- 5.1.1 Solution

- 5.1.2 Service

- 5.2 By Deployment

- 5.2.1 On-demand

- 5.2.2 On-premise

- 5.3 By Organization Size

- 5.3.1 Small- and Medium-sized Enterprises

- 5.3.2 Large Enterprises

- 5.4 By End User

- 5.4.1 Banking, Financial Services, and Insurance (BFSI)

- 5.4.2 Manufacturing

- 5.4.3 IT and Telecommunication

- 5.4.4 Aerospace and Defense

- 5.4.5 Healthcare

- 5.4.6 Retail and Consumer Goods

- 5.4.7 Other End Users

- 5.5 Geography

- 5.5.1 North America

- 5.5.2 Europe

- 5.5.3 Asia Pacific

- 5.5.4 Latin America

- 5.5.5 Middle East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 IBM Corporation

- 6.1.2 Bizagi Group Limited

- 6.1.3 Pegasystems Inc.

- 6.1.4 Appian Corporation

- 6.1.5 Oracle Corporation

- 6.1.6 Software AG

- 6.1.7 DST Systems Inc.

- 6.1.8 OpenText Corporation

- 6.1.9 Newgen Software Technologies Ltd.

- 6.1.10 TIBCO Software Inc.