|

시장보고서

상품코드

1851114

BOPP 필름 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)BOPP Films - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

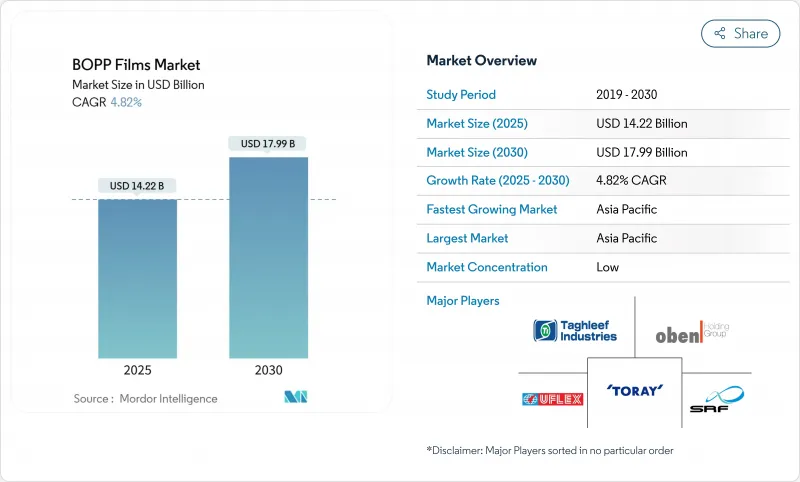

세계의 BOPP 필름 시장 규모는 2025년에 142억 2,000만 달러, 2030년에는 179억 9,000만 달러로 확대되고, 예측 기간의 CAGR은 4.82%를 나타낼 것으로 예측되고 있습니다.

성장의 배경은 규제의 합리화에 의해 식품접촉 승인 사이클이 단축되어, 간식, 의약품, 전자상거래 포장을 위한 신규 2축 연신 폴리프로필렌(BOPP) 배합의 채용이 가속되고 있는 경우가 있습니다. 디지털 소매 증가로 브랜드 소유자는 가볍고 히트 씰이 가능한 메일러 필름을 선호합니다. 한편, 폴리프로필렌 수지의 가격 변동(북미에서는 2025년 초에 1파운드당 4-5센트 상승)은 컨버터의 마진을 계속 압박하고 있어 수직 통합과 헤지 수단을 장려하고 있습니다. 정책면에서는 유럽연합(EU)의 포장·포장 폐기물 규제(PPWR)가 2030년까지 모든 포장재를 재활용 가능하게 할 것을 요구하고 있으며, 세계 공급망 전체에서 단일 소재의 BOPP 구조에 대한 수요를 환기하고 있습니다.

세계의 BOPP 필름 시장 동향과 인사이트

개발도상국의 고밀착성 간식 포장 수요 급증

도시 지역의 식료품 확대와 지역 스낵 브랜드의 프리미엄화가 BOPP 필름 시장을 투명하고 고광택 등급으로 밀어 올리고 있습니다. Haldiram 사와 같은 인도의 스낵 제조업체는 현재 투명 BOPP를 활용하여 유통 기한을 최대 20% 연장하여 현대적인 소매점 진열로 제품의 시인성을 높이고 있습니다. 동남아시아에서도 검사가 용이한 시스루팩을 선호하는 식품안전규칙에 따라 비슷한 변화가 진행되고 있습니다. 이 움직임은 변조 방지 씰로 폐기물을 줄이면서 비용 효율적인 장벽 성능을 실현합니다. PET에 비해 낮은 변환비용에 힘입은 신흥기업은 2030년까지 지속적인 수요를 확보하기 위해 계속해서 주요 채용기업으로 남아 있습니다.

브랜드 소유자가 지속가능성 목표를 위해 PVC 랩에서 BOPP로 전환

할로겐 기재를 제거하는 규제 압력은 PVC 랩에서 BOPP로의 세계적인 축 다리를 가속화하고 있습니다. 유니레버는 2026년까지 PVC를 폐기하겠다는 2024년 헌신을 통해 식품 및 퍼스널케어 제품 라인의 유연한 팩 소재로 BOPP 필름을 선택하게 되었습니다. 네슬레 사는 이러한 전환으로 재활용 물류를 간소화하여 10-15%의 비용 절감을 실현했습니다. 또한 과자류의 랩을 BOPP로 이행함으로써 재활용률은 23%에서 87%로 급상승했습니다. 컨버터는 새로운 씰링 죠와 설비의 리노베이션에 투자하고 있지만, 컴플라이언스 비용의 저하와 브랜드 에퀴티의 향상이 설비 투자의 장애물을 상쇄하고 있습니다.

폴리프로필렌 수지 가격 변동

북미의 폴리프로필렌 가격은 2025년 초에 파운드당 4-5센트 상승하여 2024년부터 비슷한 상승에 호응했습니다. 인도의 BOPP 가격은 1톤당 1,020달러에 달했지만, 20%의 신규 생산 능력에 대해 국내 수요는 11% 증가에 그치고, 업계의 수익성은 10년간에서 최소의 8%가 되었습니다. 컨버터는 현금 흐름의 긴박에 직면하여 규모의 경제를 얻기 위해 M&A를 가속화하고 있습니다.

부문 분석

메탈라이즈드 필름은 2030년까지 연평균 복합 성장률(CAGR) 8.36%를 나타낼 전망입니다. 투명 필름은 2024년 금액 기준으로 BOPP 필름 시장의 51.32%를 차지했으며, 제품의 신선도를 강조하는 스낵과 베이커리 창에 필수적인 것으로 입증되었습니다. 고진공 메탈라이저에 대한 컨버터 투자는 더 가볍고 프리미엄 호일과 동등한 성능을 지원합니다. 이와 병행하여, 블리스터 오버랩을 위한 금속화된 등급과 관련된 BOPP 필름 시장 규모는 엄격한 안정성 요건을 뒷받침하며 2030년까지 30억 달러 이상에 달할 것으로 예상됩니다.

흰색, 불투명, 진주 광택의 각 등급은 라벨 스톡, 테이프, 고급 랩에 사용되며 미적 대비와 UV 불투명도를 제공합니다. 그러나 그 점유율은 범용 클리어 등급에 비해 틈새 시장입니다. AluBond와 AlOx와 같은 특수 코팅은 금속과의 접착성과 광학 투명성을 향상시켜 용도의 폭을 넓혀 규제 대상의 의약품 카톤 중 PVdC 코팅 PVC의 대체품으로 BOPP 필름 시장을 강화하고 있습니다.

45µm 이상의 필름은 기계적 강성이 필요한 산업용 테이프, 비료 봉지 및 스탠드업 파우치 덕분에 CAGR 7.54%를 나타낼 전망입니다. 그래도 15-30µm 분야는 시장 세분화의 36.34%를 차지해, 코스트 밸런스가 있는 스낵 과자용 랩이나 라벨의 주류를 유지하고 있습니다. 순차 이축 연신 기술은 현재 기계 방향 배향도를 12까지 끌어올려, 한때 더 무거운 게이지로 제한된 성능을 더 얇은 필름으로 가져옵니다. 이 기술 변화는 비중요한 포장에서 헤비 게이지의 이점을 점차적으로 침식할 수 있습니다.

15µm 이하의 틈새는 권취 및 펑크 우려에 직면하지만, 폴리머 핵제와 제어된 냉각은 공정 안정성을 향상시킵니다. 미들 웨이트의 30-45µm 필름은 의약품의 오버랩이나 프리미엄 커피 라이너의 스테디셀러이며 계속해서 강성과 배리어 요구의 밸런스를 유지하고 있습니다. 이러한 다양성은 BOPP 필름 시장의 근본적인 다층 성장 프로파일을 보여줍니다.

이 보고서는 BOPP 필름 시장 분석을 커버하고, 필름 유형(투명, 메탈라이즈드, 기타), 두께(15mm 미만, 15-30mm, 기타), 용도(포장, 라벨링, 랩 어라운드, 기타), 최종 사용자 버티컬(식품, 식음료, 기타), 지역(북미, 유럽, 아시아태평양, 남미)으로 구분됩니다.

지역 분석

아시아태평양은 2024년 수익의 45.21%를 차지했고 8.43%라는 가장 빠른 연평균 성장률(CAGR)을 나타내며, 특히 인도에서 2024년부터 2025년까지의 폴리머 소비량의 8.5% 성장이 이를 뒷받침하고 있습니다. 일관된 생산, 낮은 인건비, 간식 및 의약품 수요에 대한 근접성은 구조적 우위를 창출합니다. 그럼에도 불구하고 올레핀공급 과잉과 레거시 자산의 미가동은 마진의 중하가 되어 선택적인 조업 정지와 수출의 리밸런스를 촉진하고 있습니다.

북미에서는 전자상거래가 지방으로의 배송을 확대하고 메일러 필름 소비에 박차를 가하고 있기 때문에 수요는 꾸준히 성장하고 있습니다. 그러나 수지 변동성은 컨버터의 수익성에 어려움을 야기하며 수직 통합 및 재활용 컨텐츠 혁신에 박차를 가하고 있습니다. 유럽에서는 PPWR 규제를 충족시키기 위한 고 배리어성 재활용 대응 라미네이트가 중심이 되어 현지 브랜드 소유자들 사이에서 모노머티리얼 BOPP에 대한 투자가 촉진되고 있습니다.

중동 및 아프리카는 인프라 정비의 혜택을 누리고 있습니다. UFlex의 이집트 공장은 소비자 시장에 가깝고 유럽에 대한 무역 액세스를 활용합니다. 남미에서는 현지 식품 가공업자가 브랜드화한 보존 가능한 스낵 과자를 목표로 하고 있지만, 통화 변동과 수지의 수입 의존이 성장을 억제하고 있습니다. 이 지역별 이야기는 BOPP 필름 시장이 지리적으로 다양한 궤도를 그린다는 것을 뒷받침합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 개발도상국에 있어서 고투명도 스낵 과자 포장에 수요 급증

- 브랜드 소유자가 지속가능성을 목표로 PVC 랩에서 BOPP로 변경

- E-Commerce 붐이 히트 씰 가능한 BOPP 메일러 필름을 견인

- 폴리올레핀 종합 제조업체에 의한 급속한 생산 능력 증강

- 리사이클 대응 모노 머티리얼 적층판의 상품화

- 시장 성장 억제요인

- 폴리프로필렌 수지 가격의 변동

- 세계의 마진을 밀어 내리는 중국 레거시 라인의 미가동

- 프리미엄 틈새 시장에서 바이오베이스 배리어 필름과의 경쟁

- 공급망 분석

- 규제 상황

- 기술 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

- 주요 거시 경제 동향이 시장에 미치는 영향

제5장 시장 규모와 성장 예측

- 필름 유형별

- 투명

- 금속 코팅

- 불투명/흰색

- 진주광택

- 기타 필름 유형

- 두께별

- 15μm 미만

- 15-30µm

- 30-45µm

- 45μm 이상

- 용도별

- 포장

- 라벨링 및 랩어라운드

- 라미네이팅

- 감압 접착 테이프

- 기타 용도

- 최종 사용자 업계별

- 식품

- 음료

- 제약 및 의료

- 퍼스널케어 및 화장품

- 산업

- 기타 최종 사용자 업계별

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- 기타 아시아태평양

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 케냐

- 나이지리아

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Taghleef Industries

- Jindal Poly Films

- Toray Industries

- SRF Limited

- Uflex Ltd

- Cosmo Films

- Polyplex Corp

- Oben Holding Group

- Treofan Group

- Vacmet India

- NAN YA Plastics

- Mitsui Chemicals Tohcello

- Futamura Chemical

- Innovia Films

- Irplast SpA

- Inteplast Group

- Biofilm SA

- Manucor Spa

- Dunmore Corp

- Tatrafan SRO

제7장 시장 기회와 향후 전망

KTH 25.11.20The global BOPP films market size stands at USD 14.22 billion in 2025 and is projected to advance to USD 17.99 billion by 2030, translating into a 4.82% CAGR over the forecast period.

Growth stems from regulatory streamlining that shortens food-contact approval cycles, accelerating adoption of novel biaxially oriented polypropylene (BOPP) formulations for snack, pharmaceutical, and e-commerce packaging. Rising digital retail has pushed brand owners to favor lightweight, heat-sealable mailer films that reduce packaging volume by 23% compared with corrugated formats. Meanwhile, polypropylene resin volatility-prices in North America rose 4-5 cents per pound in early 2025-continues to squeeze converter margins, encouraging vertical integration and hedging instruments. On the policy front, the European Union's Packaging and Packaging Waste Regulation (PPWR) requires all packaging to be recyclable by 2030, catalyzing demand for mono-material BOPP structures across global supply chains.

Global BOPP Films Market Trends and Insights

Surging Demand for High-Clarity Snack Packaging in Developing Economies

Urban grocery expansion and premiumization of regional snack brands are pushing the BOPP films market toward transparent, high-clarity grades. Indian snack producers such as Haldiram's now leverage transparent BOPP to extend shelf life by up to 20%, boosting product visibility in modern retail displays. Similar shifts in Southeast Asia are driven by food-safety rules that favor see-through packs for easy inspection. The move enables cost-effective barrier performance while reducing waste through tamper-evident seals. Emerging players, incentivized by lower conversion costs versus PET, remain key adopters, ensuring sustained demand through 2030.

Brand-Owner Switch from PVC Wrap to BOPP for Sustainability Goals

Regulatory pressure to eliminate halogenated substrates has accelerated the global pivot from PVC wraps to BOPP. Unilever's 2024 commitment to phase out PVC by 2026 frames BOPP films as the material of choice for flexible packs across food and personal care lines. The shift yields 10-15% cost savings at Nestle due to simplified recycling logistics, while recyclability rates jumped from 23% to 87% after migrating confectionery wraps to BOPP. Converters invest in new sealing jaws and equipment retrofits, but lower compliance fees and positive brand equity offset capex hurdles.

Volatility in Polypropylene Resin Prices

North American polypropylene prices climbed 4-5 cents per pound in early 2025, echoing similar hikes from 2024. India's BOPP prices touched USD 1,020 per ton, yet domestic demand rose only 11% against 20% fresh capacity, pushing industry profitability toward a decade-low 8%. Converters face cash-flow strain and accelerate M&A to gain economies of scale.

Other drivers and restraints analyzed in the detailed report include:

- E-Commerce Boom Driving Heat-Sealable BOPP Mailer Films

- Commercialization of Recycle-Ready Mono-Material Laminates

- Under-Utilized Legacy Lines in China Depressing Global Margins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Metallized films secured an 8.36% CAGR outlook through 2030 as pharmaceutical packs demand superior oxygen and moisture barriers. Transparent films held 51.32% of the BOPP films market in 2024 by value, proving indispensable in snack and bakery windows that highlight product freshness. Converter investment in high-vacuum metallizers supports premium foil-equivalent performance at lower weight. In parallel, the BOPP films market size tied to metallized grades for blister over-wraps is projected to top USD 3 billion by 2030, buoyed by stringent stability mandates.

White, opaque, and pearlescent variants serve labelstock, tape, and luxury wraps, providing aesthetic contrast and UV opacity. Yet, their share remains niche compared with commodity clear grades. Specialty coatings such as AluBond and AlOx are widening the application canvas by improving metal adhesion and optical clarity, reinforcing the BOPP films market as a replacement for PVdC-coated PVC within regulated drug cartons.

Films above 45 µm are growing at 7.54% CAGR thanks to industrial tapes, fertilizer bags, and stand-up pouches that need mechanical rigidity. The 15-30 µm segment nonetheless captures 36.34% of the BOPP films market size, maintaining primacy for cost-balanced snack wraps and labels. Sequential biaxial stretching techniques now raise machine-direction orientation to ratios of 12, yielding thinner films with performance once limited to heavier gauges. This engineering shift could gradually erode heavy-gauge dominance in non-critical packaging.

The sub-15 µm niche faces winding and puncture concerns; however, polymer nucleating agents and controlled cooling have improved process stability. Middle-weight 30-45 µm films remain staples for pharmaceutical over-wrap and premium coffee liners, balancing stiffness and barrier demands. Such diversity illustrates the multi-tiered growth profile underlying the BOPP films market.

The Report Covers Biaxially Oriented Polypropylene Films Market Analysis and is Segmented by Film Type ( Transparent, Metallized, and More), Thickness ( Less Than 15 Mm, 15 - 30 Mm, and More), Application (Packaging, Labeling and Wrap-Arounds, and More), End-User Vertical (Food, Beverage, and More) and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa).

Geography Analysis

Asia-Pacific accounted for 45.21% of 2024 revenue and records the fastest 8.43% CAGR, underscored by India's polymer consumption growth of 8.5% in FY 2024-25. Integrated production, low labor costs, and proximity to snack and pharmaceutical demand create structural advantages. Nonetheless, olefin oversupply and under-utilized legacy assets weigh on margins, prompting selective shutdowns and export rebalancing.

North America illustrates steady demand growth as e-commerce expands rural deliveries, fueling mailer film consumption. Resin volatility, however, challenges converter profitability, spurring vertical integration and recycled-content innovations. Europe centers on high-barrier, recycle-ready laminates to meet PPWR mandates, encouraging mono-material BOPP investments among local brand owners.

The Middle East & Africa benefits from infrastructure upgrades; UFlex's Egypt complex positions it near consumer markets while leveraging trade access to Europe. South America advances as local food processors move toward branded, shelf-stable snacks, yet currency volatility and import dependency on resin temper growth. Together, these regional narratives underline the geographically diversified trajectory of the BOPP films market.

- Taghleef Industries

- Jindal Poly Films

- Toray Industries

- SRF Limited

- Uflex Ltd

- Cosmo Films

- Polyplex Corp

- Oben Holding Group

- Treofan Group

- Vacmet India

- NAN YA Plastics

- Mitsui Chemicals Tohcello

- Futamura Chemical

- Innovia Films

- Irplast S.p.A

- Inteplast Group

- Biofilm SA

- Manucor Spa

- Dunmore Corp

- Tatrafan SRO

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging demand for high-clarity snack packaging in developing economies

- 4.2.2 Brand-owner switch from PVC wrap to BOPP for sustainability goals

- 4.2.3 E-commerce boom driving heat-sealable BOPP mailer films

- 4.2.4 Rapid capacity additions by integrated polyolefin producers

- 4.2.5 Commercialization of recycle-ready mono-material laminates

- 4.3 Market Restraints

- 4.3.1 Volatility in polypropylene resin prices

- 4.3.2 Under-utilized legacy lines in China depressing global margins

- 4.3.3 Competition from bio-based barrier films in premium niches

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Impact of Key Macroeconomic Trends on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Film Type

- 5.1.1 Transparent

- 5.1.2 Metallized

- 5.1.3 Opaque / White

- 5.1.4 Pearlescent

- 5.1.5 Other Film Type

- 5.2 By Thickness

- 5.2.1 Less than 15 µm

- 5.2.2 15 - 30 µm

- 5.2.3 30 - 45 µm

- 5.2.4 More than 45 µm

- 5.3 By Application

- 5.3.1 Packaging

- 5.3.2 Labeling and Wrap-Arounds

- 5.3.3 Laminating

- 5.3.4 Pressure-Sensitive Tapes

- 5.3.5 Other Application

- 5.4 By End-user Vertical

- 5.4.1 Food

- 5.4.2 Beverage

- 5.4.3 Pharmaceutical and Medical

- 5.4.4 Personal Care and Cosmetics

- 5.4.5 Industrial

- 5.4.6 Other End-user Vertical

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Russia

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Kenya

- 5.5.5.2.3 Nigeria

- 5.5.5.2.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, Recent Developments)

- 6.4.1 Taghleef Industries

- 6.4.2 Jindal Poly Films

- 6.4.3 Toray Industries

- 6.4.4 SRF Limited

- 6.4.5 Uflex Ltd

- 6.4.6 Cosmo Films

- 6.4.7 Polyplex Corp

- 6.4.8 Oben Holding Group

- 6.4.9 Treofan Group

- 6.4.10 Vacmet India

- 6.4.11 NAN YA Plastics

- 6.4.12 Mitsui Chemicals Tohcello

- 6.4.13 Futamura Chemical

- 6.4.14 Innovia Films

- 6.4.15 Irplast S.p.A

- 6.4.16 Inteplast Group

- 6.4.17 Biofilm SA

- 6.4.18 Manucor Spa

- 6.4.19 Dunmore Corp

- 6.4.20 Tatrafan SRO

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment