|

시장보고서

상품코드

1683102

중국의 작물 보호 화학제품 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)China Crop Protection Chemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

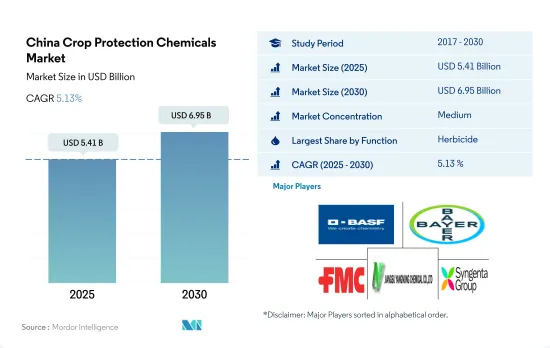

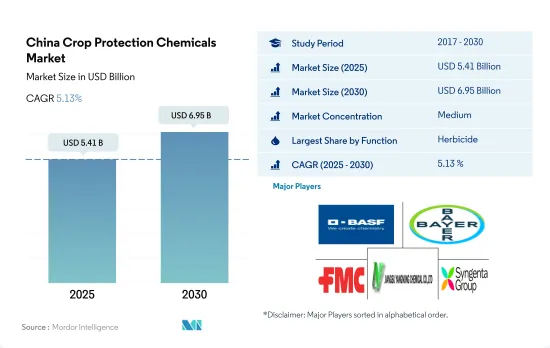

중국의 작물 보호 화학제품 시장 규모는 2025년에 54억 1,000만 달러로 추정되고, 2030년에는 69억 5,000만 달러에 이를 것으로 예측되며, 예측 기간 중 2025년부터 2030년까지 CAGR은 5.13%로 성장할 전망입니다.

제초제가 시장을 석권

- 중국은 많은 국가에서 판매되는 제형화된 작물 보호 화학제품 및 기성품 작물 보호 화학제품의 기초가 되는 활성 성분의 주요 생산국입니다. 이 나라는 작물 보호 화학제품의 세계 최대급 생산국이자 수출국이기도 합니다. 살충제는 작물 보호 화학제품 시장의 중요한 부문을 구성합니다. 시장의 주요 촉진요인은 인구가 많고, 농지의 규모가 제한되어 있고, 식량 안보가 높아지고 있으며, 효율적인 농업 생산이 시급하다는 것입니다. 2022년 아시아태평양 작물 보호 화학제품 시장 전체에서 중국은 금액 기준으로 20.8%로 가장 높은 점유율을 차지했습니다.

- 2022년 중국의 작물 보호 화학제품 시장에서 제초제는 금액 기준으로 38.2%의 최대 점유율을 차지했습니다. 중국에서는 제초제의 사용이 잡초 방제에 도움이 되어 농업 종사자들은 잡초와 경쟁하기 어려운 왜성 벼 품종을 보다 많이 재배하기 쉬워져 수율이 증가하고 있습니다. 농촌 지역에서 산업 지역으로 이주한 전통적인 수작업 노동자의 감소가 컸지만, 제초제 덕분에 농부들은 잡초를 방제할 수 있게 되었습니다.

- 2022년 시장에서는 살충제 부문이 금액 기준으로 30.0%로 큰 점유율을 차지했습니다. 면화에 사용 등록된 작물 보호 화학제품에서 가장 흔한 것은 살충제입니다. 그 중에서도 홉심은 시펠메트린이나 β-시페르메트린 등의 활성 물질의 등록수가 가장 많습니다.

- 병해충의 확산에 대한 우려가 증가하고 국제 수요가 증가함에 따라 기업과 정부는 지속적으로 연구 프로젝트에 투자하고 병해충으로 인한 작물 피해를 예방하기위한 새로운 유효 성분을 개발하고 있습니다. 이 시장은 예측 기간 동안 CAGR 5.4%를 나타낼 것으로 예측되고 있습니다.

중국 작물 보호제 시장 동향

IPM 전략 및 기타 작물 보호 화학제품 삭감 시책이 헥타르당 작물 보호 화학제품 소비량 삭감에 기여

- 지난 몇 년동안 중국의 헥타르 당 작물 보호 화학제품 소비량이 현저히 감소했습니다. 과거에는 작물 보호 화학제품의 사용량이 헥타르 당 약 300g까지 크게 감소했습니다. 2017년 소비량은 1헥타르당 1,700그램이었지만, 2022년에는 1헥타르당 1,400그램으로 감소했습니다.

- 1헥타르당 작물 보호 화학제품 사용량이 크게 감소한 것은 작물 보호 화학제품 소비량의 성장을 0으로 하는 엄격한 시책을 실시한 것이 크게 영향을 미쳤습니다.

- 중국은 다양한 예방 조치, 대체 기술, 신중한 작물 보호 화학제품 살포를 포함한 종합 병해충 관리(IPM) 전략의 채택을 적극적으로 추진해 왔습니다. 이 종합적인 접근의 결과로, 작물 보호 화학제품 사용률은 현저하게 감소했습니다.

- 중국에서는 제초제 사용량이 88.78g으로 크게 감소했지만, 이는 주로 농업 종사자가 윤작 등의 관행을 도입한 것이 원인입니다. 윤작은 성장 패턴과 영양 요구량이 다른 작물을 번갈아 재배함으로써 잡초의 라이프 사이클을 효과적으로 차단하는 것입니다. 중국의 농업 종사자들은 이런 관행을 시행함으로써 잡초의 성장주기를 중단시키는 데 성공했고, 그 결과 잡초의 개체수가 감소하고 제초제에 대한 의존도가 감소하였습니다.

- 헥타르당 작물 보호 화학제품 사용량의 기타 상당한 감소는 특히 살충제 범주에서 관찰되었으며 2017년부터 2022년까지 58.31g 감소했습니다. 이 감소는 주로 유해한 살충제의 금지를 목적으로 하는 정부의 시책과 유전자 변형 작물의 채용에 기인합니다.

- 살충제 사용에 대한 최대 잔류 기준치 설정과 같은 기타 요인들도 국내 1헥타르당 소비량을 감소시켰습니다.

유효 성분의 가격은 국내 날씨, 해충 발생, 에너지 가격, 인건비 등의 요인에 크게 영향을 받습니다.

- 중국은 제형화된 작물 보호 화학제품의 기초가 되는 활성 성분의 주요 생산국 중 하나입니다. 살충제는 살충제 생산의 주요 점유율을 차지합니다.

- 시페르메트린은 피레스로이드계 살충제 중에서 가장 널리 사용되고 있으며, 야채나 과일의 미바에, 붕어벌레, 메리충 등 많은 해충을 구제합니다. 2022년에는 톤당 2만 900달러로 평가되었습니다.

- Atrazine은 다양한 잎이 많은 잡초와 잔디를 방제하는 데 널리 사용되는 제초제입니다. 중국에서는 연간 1만 6,000톤 이상(기술적으로 97%)의 아틀라진이 소비되고 있습니다. 아트라진은 주로 옥수수와 사탕수수 밭의 연간 잡초를 방제하는 데 사용됩니다. 중국은 세계의 아틀라진의 주요 공급국 중 하나입니다. 2022년 가격은 톤당 1만 3,700달러였습니다.

- Mancozeb는 넓은 스펙트럼 접촉 살균제로, 나타네, 양상추, 밀, 사과, 토마토, 테이블 포도, 와인 포도, 전구 양파, 당근, 퍼스닙, 샬롯, 듀럼 밀의 탄저병, 피슘병, 엽반병, 우동병, 병병, 보트리티병 2022년 가격은 톤당 7,700달러였습니다.

- 글리포세이트는 유기인계 광역 스펙트럼 침투성 제초제와 작물 건조제로 2022년 가격은 톤당 1,100달러였습니다. 글리포세이트는 주로 쌀과, 수염과, 활엽수와 같은 잡초의 방제에 사용됩니다. 중국은 세계 최대의 글리포세이트 생산 및 수출국입니다. 2017년 중국은 30만 톤 이상의 글리포세이트 기술을 수출하여 세계 글리포세이트 수요의 절반 이상을 충족했습니다.

- 국내 날씨, 해충 발생, 에너지 가격, 인건비 등의 요인이 유효 성분의 가격에 크게 영향을 미치고 있습니다.

중국의 작물 보호 화학제품 산업 개요

중국의 작물 보호 화학제품 시장은 적당히 통합되어 있으며 상위 5개 기업에서 52.57%를 차지합니다. 이 시장의 주요 진출기업은 BASF SE, Bayer AG, FMC Corporation, Jiangsu Yangnong Chemical, Syngenta Group입니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 주요 요약 및 주요 조사 결과

제2장 보고서 제안

제3장 서문

- 조사 전제조건 및 시장 정의

- 조사 범위

- 조사 방법

제4장 주요 산업 동향

- 1헥타르당 작물 보호 화학제품 소비량

- 유효성분의 가격 분석

- 규제 프레임워크

- 중국

- 밸류체인 및 유통채널 분석

제5장 시장 세분화(시장 규모(단위-달러, 수량), 예측 및 성장 전망 분석 포함)(-2030년)

- 기능별

- 살균제

- 제초제

- 살충제

- 살연체 동물제

- 살선충제

- 적용 모드별

- 약제 살포

- 잎면 살포

- 훈증

- 종자 처리

- 토양처리

- 작물 유형별

- 상업 작물

- 과일 및 야채

- 곡물

- 콩류 및 지방종자

- 잔디 및 관상용

제6장 경쟁 구도

- 주요 전략적 움직임

- 시장 점유율 분석

- 기업 상황

- 기업 프로파일(세계 수준 개요, 시장 수준 개요, 주요 사업 부문, 재무, 직원 수, 주요 정보, 시장 순위, 시장 점유율, 제품 및 서비스, 최근 동향 분석 포함)

- BASF SE

- Bayer AG

- Corteva Agriscience

- FMC Corporation

- Jiangsu Yangnong Chemical Co. Ltd

- Lianyungang Liben Crop Technology Co. Ltd

- Rainbow Agro

- Syngenta Group

- UPL Limited

- Wynca Group(Wynca Chemicals)

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

- 세계 개요

- 개요

- Porter's Five Forces 분석 프레임워크

- 세계의 밸류체인 분석

- 시장 역학(DROs)

- 정보원 및 참고문헌

- 도표 일람

- 주요 인사이트

- 데이터 팩

- 용어집

The China Crop Protection Chemicals Market size is estimated at 5.41 billion USD in 2025, and is expected to reach 6.95 billion USD by 2030, growing at a CAGR of 5.13% during the forecast period (2025-2030).

Herbicides dominate the market

- China is a major producer of active ingredients that serve as the foundation for formulated agrochemicals and ready-made pesticides sold in many countries. The country is one of the world's largest producers and exporters of crop protection chemicals. Insecticides comprise an important segment in the crop protection chemicals market. The key drivers of the market are a high number of people, limited size of farms, rising food security, and an urgent need for efficient agricultural production. China occupied the highest share of 20.8% by value of the overall Asia-Pacific crop protection chemicals market in 2022.

- Herbicides accounted for the largest share of 38.2% by value in the Chinese crop protection chemicals market in 2022. In China, the use of herbicides has helped in weed control and, thus, increased yields by making it easier for farmers to grow more dwarf rice varieties that are less likely to compete with weeds. Even though there has been a large decline in traditional hand laborers who have moved out of rural areas to industrial zones, herbicides have allowed farmers to control weeds.

- In 2022, the insecticide segment held a significant share of 30.0% by value in the market. The most common pesticides registered for use in cotton are insecticides. Among them, phoxim has the highest number of registered active substances, including cypermethrin and beta-cypermethrin.

- With the increasing concern over the infestation of pests and diseases and the rise in international demand, companies and the government are continuously investing in research projects and developing new active ingredients to prevent crop damage from pests. The market is anticipated to register a CAGR of 5.4% during the forecast period.

China Crop Protection Chemicals Market Trends

IPM strategies and other pesticide reduction policies contributed to reduction in per hectare pesticides consumption

- Over the past few years, there has been a notable reduction in pesticide consumption per hectare in the country. During the historical period, there was a significant decline in pesticide usage to approximately 300 grams per hectare. In 2017, the consumption stood at 1,700 grams per hectare; however, by 2022, it had dropped to 1,400 grams per hectare.

- The considerable reduction in pesticide utilization per hectare can be largely attributed to the country's implementation of a stringent policy of zero growth in pesticide consumption.

- China has proactively promoted the adoption of Integrated Pest Management (IPM) strategies, encompassing a range of preventive measures, alternative techniques, and careful pesticide applications. As a result of this holistic approach, there has been a notable reduction in pesticide usage rates.

- China witnessed a significant decline in herbicide usage by 88.78 grams, primarily driven by the adoption of practices such as crop rotation by farmers. Crop rotation involves alternating different crops with varying growth patterns and nutritional requirements, effectively breaking the lifecycle of weeds. By implementing this practice, Chinese farmers have successfully disrupted weed growth cycles, resulting in reduced weed populations and a decreased reliance on herbicides.

- The other substantial decrease in pesticide usage per hectare was observed specifically in the category of insecticides, with a reduction of 58.31 grams from 2017 to 2022. This decline can be primarily attributed to government policies aimed at banning harmful insecticides and the adoption of transgenic crops.

- Other factors like setting limits on the maximum residue levels on the usage of pesticides reduced the per hectare consumption in the country.

The active ingredients' prices are majorly influenced by factors like weather conditions, pest outbreaks, energy prices, and labor costs in the country

- China is one of the major producers of active ingredients that form the base of formulated crop protection chemicals. Insecticides constitute the major share of pesticide production.

- Cypermethrin is the most widely used pyrethroid pesticide to control many pests, such as fruit flies, borers, and mealy bugs in vegetables and fruits in China. It was valued at USD 20.9 thousand per metric ton in 2022.

- Atrazine is a herbicide widely used to control various broadleaved weeds and grasses. China consumes more than 16,000 ton (97% technical) of atrazine annually. Atrazine is mainly used to control annual weeds in corn or sugarcane fields. China is one of the major suppliers of atrazine worldwide. It was priced at USD 13.7 thousand per metric ton in 2022.

- Mancozeb is a broad-spectrum contact fungicide used to control a number of fungal diseases, such as anthracnose, Pythium blight, leaf spot, downy mildew, Botrytis, rust, and scab in oilseed rape, lettuce, wheat, apples, tomatoes, table grapes, wine grapes, bulb onions, carrot, parsnip, shallot, and durum wheat. It was priced at USD 7.7 thousand per metric ton in 2022.

- Glyphosate is an organophosphorus broad-spectrum systemic herbicide and crop desiccant, priced at USD 1.1 thousand per metric ton in 2022. Glyphosate is mainly used to control weeds like grasses, sedges, and broadleaves. China is the largest producer and exporter of glyphosate in the world. In 2017, China exported over 300,000 ton of glyphosate technical, which met more than half of the global glyphosate demand.

- Factors like weather conditions, pest outbreaks, energy prices, and labor costs in the country majorly influence the prices of active ingredients.

China Crop Protection Chemicals Industry Overview

The China Crop Protection Chemicals Market is moderately consolidated, with the top five companies occupying 52.57%. The major players in this market are BASF SE, Bayer AG, FMC Corporation, Jiangsu Yangnong Chemical Co. Ltd and Syngenta Group (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Consumption Of Pesticide Per Hectare

- 4.2 Pricing Analysis For Active Ingredients

- 4.3 Regulatory Framework

- 4.3.1 China

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Function

- 5.1.1 Fungicide

- 5.1.2 Herbicide

- 5.1.3 Insecticide

- 5.1.4 Molluscicide

- 5.1.5 Nematicide

- 5.2 Application Mode

- 5.2.1 Chemigation

- 5.2.2 Foliar

- 5.2.3 Fumigation

- 5.2.4 Seed Treatment

- 5.2.5 Soil Treatment

- 5.3 Crop Type

- 5.3.1 Commercial Crops

- 5.3.2 Fruits & Vegetables

- 5.3.3 Grains & Cereals

- 5.3.4 Pulses & Oilseeds

- 5.3.5 Turf & Ornamental

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 BASF SE

- 6.4.2 Bayer AG

- 6.4.3 Corteva Agriscience

- 6.4.4 FMC Corporation

- 6.4.5 Jiangsu Yangnong Chemical Co. Ltd

- 6.4.6 Lianyungang Liben Crop Technology Co. Ltd

- 6.4.7 Rainbow Agro

- 6.4.8 Syngenta Group

- 6.4.9 UPL Limited

- 6.4.10 Wynca Group (Wynca Chemicals)

7 KEY STRATEGIC QUESTIONS FOR CROP PROTECTION CHEMICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms