|

시장보고서

상품코드

1683202

지붕용 멤브레인 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Roofing Membranes - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

■ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송일정은 문의해 주시기 바랍니다.

가격

※ 부가세 별도

한글목차

영문목차

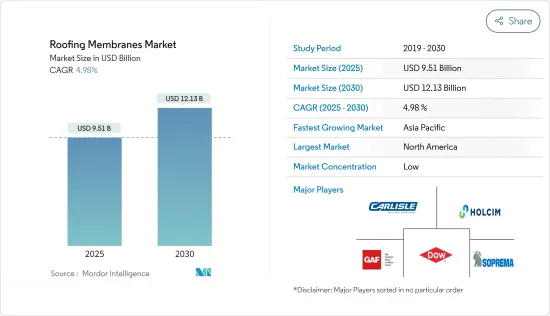

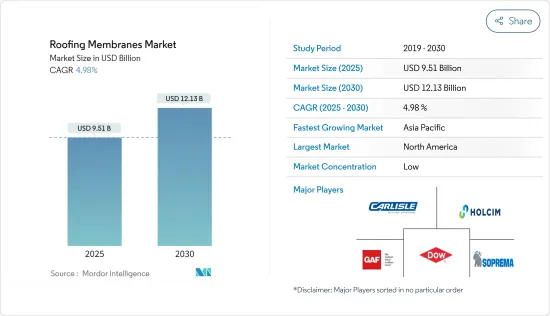

지붕용 멤브레인 시장 규모는 2025년에 95억 1,000만 달러로 추정되고, 예측 기간 2025년부터 2030년까지 CAGR은 4.98%로 전망되며, 2030년에는 121억 3,000만 달러에 달할 것으로 예측됩니다.

주요 하이라이트

- 건설 프로젝트에서 경량 재료의 채용 증가와 건설 활동의 활성화는 지붕용 멤브레인 시장의 성장을 가속하는 주요 요인입니다.

- 그러나 원료 가격의 변동이나 엄격한 규제 및 기준이 시장의 성장을 저해할 가능성이 높습니다.

- 에너지 효율적인 지붕용 멤브레인에 대한 수요 증가와 기술 발전은 예측 기간 동안 시장에 유리한 성장 기회를 가져올 가능성이 높습니다.

- 북미는 건설활동의 활성화로 지붕용 멤브레인 시장을 독점하고 있습니다.

지붕용 멤브레인 시장 동향

시장을 독점하는 것은 상업 부문

- 지붕용 멤브레인은 업무용으로 널리 이용되고 있으며, 그 수요는 세계 상업 건축의 급증에 의해 크게 뒷받침되고 있습니다. 이 멤브레인은 상업용 건물에서 중요한 방수 장벽 역할을 하며 환경 요소로부터 건물을 보호하며 지붕 시스템의 무결성을 유지합니다.

- 강도, 내구성 및 물에 대한 불침투성으로 인해 이러한 멤브레인은 상업시설의 지붕 적용에 선호되는 옵션이 되었습니다.

- 이 막은 공장, 기차역, 공항, 본사, 쇼핑 센터, 극장, 학교, 병원 등의 상업 지역에서 사용됩니다.

- 아시아태평양은 상업 건축 분야에서 압도적인 힘을 자랑합니다. 이 지역에서는 최근, 특히 인도와 중국에서 정부의 적극적인 개발 이니셔티브에 힘입어 사무실 공간 수요가 급증하고 있습니다.

- 중국 국가 통계국의 데이터에 따르면 2022년 중국 상업시설의 연간 착공 면적은 약 8,155만 평방미터로 전년 1억 4,105만 평방미터에서 감소했습니다. 게다가 2023년 말 분양상업 빌딩의 바닥면적은 6억 7,295만 평방미터로 전년대비 19% 증가했습니다.

- 인도에서는 바닥면적 76만 1,804㎡의 오피스 캠퍼스 확대를 포함한 인포시스 포처람 오피스 캠퍼스의 건설이 2023년 3분기에 시작되어 2027년 3분기 말까지 완성될 전망입니다.

- 중동에서는 사우디아라비아 비전 2030과 아부다비 경제 비전 2030과 같은 상업 부문의 개발을 강화하기 위한 몇몇 정부 이니셔티브이 지붕용 멤브레인의 소비를 크게 촉진할 것으로 보입니다.

- 다양한 호텔 건설 프로젝트가 지붕용 멤브레인 수요를 더욱 높일 것으로 예상됩니다. 예를 들어 관광산업이 회복됨에 따라 Marriott International Inc.는 하노이, 호치민시, 다낭, 푸꾸옥 섬 등 베트남의 주요 관광지 전역에서 20개의 고급 호텔과 리조트를 발표할 예정입니다.

- Anantara Hotels, Resorts 및 Spas는 2025년 데뷔 예정인 브라질의 새로운 리조트 계획을 밝혔습니다. Anantara Mamucabo는 116개의 객실, 스위트, 풀 빌라를 보유하고 있습니다.

- 상업시설의 건설이 증가하고 있기 때문에 상업시설 지붕용 멤브레인 수요는 향후 수년간 확대될 전망입니다.

북미가 시장을 독점할 전망

- 북미는 세계 시장에서 가장 큰 점유율을 차지합니다. 미국, 캐나다, 멕시코 등 국가에서는 가볍고 신속한 건설 기술의 채택이 지붕용 멤브레인 수요를 급증시키고 있습니다.

- 미국은 세계 최대급의 건설 산업을 자랑합니다. 미국 인구조사국에 따르면 2023년 건설 총액은 19조 7,800억 달러에 달했고, 2022년부터 7% 증가했습니다. 2024년 2월까지 건축 허가를 받은 민간 주택 호수는 151만 8,000호에 달했으며, 2023년 동시기부터 2.4% 증가했습니다.

- 미국에서는 몇 가지 새로운 상업 건축 프로젝트가 건설 중이며 지붕용 멤브레인 수요는 더욱 증가할 것으로 보입니다. 예를 들어, 2024년 1월, 인디애나 주 정부와 Meta Platforms Inc.는 푸저 주에 8억 달러의 새로운 데이터센터 캠퍼스를 건설하기 위해 제휴했습니다. 이 프로젝트는 2026년까지 완성될 전망이며, 리버 리지 커머스 센터에 70만 평방 피트의 시설을 건설합니다.

- 캐나다 통계국에 따르면 건축물 건설 투자 총액은 1.7% 증가했으며 2023년 10월 19조 4,460억 달러에서 2023년 11월 19조 7,670억 달러로 증가했습니다. 같은 기간 주택건설 투자는 2.2% 증가한 137억 달러, 비주택건설 투자는 0.6% 증가한 60억 달러였습니다.

- 2023년 국제무역청이 보고한 멕시코 건설 산업은 현저한 가치 상승을 보였습니다. 산업 전체의 가치는 2022년 1,028억 8,000만 달러에서 1,205억 8,000만 달러로 상승했습니다. 특히 인프라 부문은 2022년 388억 3,000만 달러에서 2023년에는 약 461억 달러로 급증했습니다. 건설 및 인프라의 두 부문에서 이러한 상승 기조는 향후 몇 년동안 멕시코에서 조사 된 시장 수요를 촉진할 계획입니다.

- 따라서 이러한 건설 시장의 호재 및 경량 재료의 채용 확대로 예측기간 동안 북미에서는 지붕용 멤브레인 수요가 증가할 것으로 예측됩니다.

지붕용 멤브레인 산업 개요

지붕용 멤브레인 시장은 세분화되어 있습니다. 주요 진출기업(순부동)으로는 Carlisle SynTec Systems, Sika AG, HOLCIM, GAF Inc., Saint-Gobain 등이 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사 전제조건

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 시장 성장 촉진요인

- 건설 프로젝트에서 경량 재료 채용 증가

- 건설 활동 증가

- 기타 촉진요인

- 시장 성장 억제요인

- 원료 가격의 변동

- 엄격한 규제 및 기준

- 기타 억제요인

- 산업 밸류체인 분석

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 세분화(금액 베이스 시장 규모)

- 제품 유형별

- 열가소성 폴리올레핀(TPO)

- 에틸렌 프로파일렌 디엔 단량체(EPDM)

- 폴리염화비닐(PVC)

- 개질 역청(모드 비트)

- 기타

- 설치 유형별

- 기계적 접착

- 완전 접착

- 밸러스트

- 기타 설치 유형

- 용도별

- 주택용

- 상업시설

- 시설

- 인프라

- 지역별

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 말레이시아

- 태국

- 인도네시아

- 베트남

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 북유럽 국가

- 터키

- 러시아

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 콜롬비아

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 카타르

- 아랍에미리트(UAE)

- 나이지리아

- 이집트

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- M&A, 합작사업, 제휴 및 협정

- 시장 점유율(%)** 및 랭킹 분석

- 주요 기업의 전략

- 기업 프로파일

- Carlisle SynTec Systems

- Dow

- GAF Inc.

- Henry Company

- HOLCIM

- IB Roof Systems

- IKO Polymeric

- Johns Manville

- Kingspan Group

- Owens Corning

- Polygomma

- Sika AG

- Siplast Inc.

- SOPREMA

제7장 시장 기회 및 향후 동향

- 에너지 효율이 높은 지붕용 멤브레인에 대한 수요 증가

- 기술의 진보

- 기타 기회

The Roofing Membranes Market size is estimated at USD 9.51 billion in 2025, and is expected to reach USD 12.13 billion by 2030, at a CAGR of 4.98% during the forecast period (2025-2030).

Key Highlights

- The rising adoption of lightweight materials in construction projects and increasing construction activities are the major factors driving the growth of the roofing membranes market.

- However, fluctuating raw material prices and stringent regulations and standards are likely to hinder the growth of the market.

- Nevertheless, the increasing demand for energy-efficient roofing membranes and advancements in technology are likely to create lucrative growth opportunities for the market during the forecast period.

- North America dominates the roofing membranes market owing to the growing construction activities in the region.

Roofing Membranes Market Trends

Commercial Segment to Dominate the Market

- Roofing membranes are widely utilized in commercial applications, and their demand is largely fueled by a surge in global commercial construction. These membranes serve as a vital waterproof barrier in commercial buildings, shielding them from environmental elements and upholding the roofing system's integrity.

- Due to their strength, durability, and impermeability to water, these membranes have become the preferred choice for commercial roofing applications.

- These membranes are used in commercial areas, such as factories, railway stations, airports, company headquarters, shopping centers, theaters, schools, and hospitals.

- Asia-Pacific is a dominant player in the commercial construction arena. The region recently witnessed a boom in office space demand, particularly in India and China, driven by proactive government development initiatives.

- As per the data from the National Bureau of Statistics of China, in 2022, the annual starting construction of commercial properties in China amounted to around 81.55 million square meters, down from 141.05 million square meters from the previous year. Furthermore, at the end of 2023, the floor space of commercial buildings for sale was 672.95 million square meters, up by 19% over the previous year.

- In India, the construction of Infosys Pocharam Office Campus, which includes the expansion of an office campus with a floor area of 761,804 square meters, was initiated in the third quarter of 2023, and it is likely to be completed by the end of Q3 2027.

- In the Middle East, several government initiatives to bolster the development of the commercial sector, such as Saudi Arabia Vision 2030 and Abu Dhabi Economic Vision 2030, are likely to substantially drive the consumption of roofing membranes.

- Various hotel construction projects are expected to further propel the demand for roofing membranes. For instance, as the tourism industry rebounds, Marriott International Inc. is set to unveil 20 luxury hotels and resorts across Vietnam's prime tourist spots, including Hanoi, Ho Chi Minh City, Da Nang, and Phu Quoc Island.

- Anantara Hotels, Resorts, and Spas revealed plans for a new resort in Brazil, slated to debut in 2025. Anantara Mamucabo will feature 116 guest rooms, suites, and pool villas.

- Given the growth in commercial construction activities, the demand for roofing membranes in commercial applications is poised for growth in the coming years.

North America Expected to Dominate the Market

- North America holds the largest share of the global market. Countries like the United States, Canada, and Mexico have seen a surge in demand for roofing membranes, driven by the adoption of lightweight and swift construction techniques.

- The United States boasts one of the world's largest construction industries. According to the United States Census Bureau, in 2023, the nation's construction value hit USD 19.78 trillion, marking a robust 7% increase from 2022. By February 2024, the number of privately owned housing units authorized by building permits reached 1,518,000, showing a 2.4% uptick from the same period in 2023.

- Several new commercial construction projects are under construction in the United States, which are likely to increase the demand for roofing membranes further. For instance, in January 2024, the government of Indiana and Meta Platforms Inc. partnered to construct a new USD 800 million data center campus in Hoosier State. The project, which is likely to be completed by the year 2026, is a 700,000-square-foot facility at the River Ridge Commerce Center.

- Statistics Canada reported a 1.7% increase in total investment in building construction, climbing from USD 19,446 billion in October 2023 to USD 19,767 billion in November 2023. In the same period, residential spending saw a 2.2% growth, hitting USD 13.7 billion, while non-residential spending rose by 0.6% to USD 6.0 billion.

- In 2023, Mexico's construction industry, as reported by the International Trade Administration, saw a notable uptick in value. The industry's overall worth climbed to USD 120.58 billion, up from USD 102.88 billion in 2022. Specifically, the infrastructure segment surged to about USD 46.10 billion in 2023, a significant rise from USD 38.83 billion in 2022. These upward trajectories in both the construction and infrastructure sectors are poised to fuel the demand for the market studied in Mexico in the coming years.

- Hence, due to such positive factors in the construction market and the growing adoption of lightweight materials, the demand for roofing membranes is projected to increase in North America during the forecast period.

Roofing Membranes Industry Overview

The roofing membrane market is fragmented in nature. The major players (not in any particular order) include Carlisle SynTec Systems, Sika AG, HOLCIM, GAF Inc., and Saint-Gobain.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Rising Adoption of Lightweight Materials in Construction Projects

- 4.1.2 Increasing Construction Activities

- 4.1.3 Other Drivers

- 4.2 Market Restraints

- 4.2.1 Fluctuating Raw Materials Prices

- 4.2.2 Stringent Regulations and Standards

- 4.2.3 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size by Value)

- 5.1 By Product Type

- 5.1.1 Thermoplastic Polyolefin (TPO)

- 5.1.2 Ethylene Propylene Diene Monomer (EPDM)

- 5.1.3 Poly Vinyl Chloride (PVC)

- 5.1.4 Modified Bitumen (Mod-Bit)

- 5.1.5 Other Product Type

- 5.2 By Installation Type

- 5.2.1 Mechanically Attached

- 5.2.2 Fully Adhered

- 5.2.3 Ballasted

- 5.2.4 Other Installation Types

- 5.3 By Application

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.3.3 Institutional

- 5.3.4 Infrastructural

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Malaysia

- 5.4.1.6 Thailand

- 5.4.1.7 Indonesia

- 5.4.1.8 Vietnam

- 5.4.1.9 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 NORDIC Countries

- 5.4.3.7 Turkey

- 5.4.3.8 Russia

- 5.4.3.9 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 Qatar

- 5.4.5.3 United Arab Emirates

- 5.4.5.4 Nigeria

- 5.4.5.5 Egypt

- 5.4.5.6 South Africa

- 5.4.5.7 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/ Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Carlisle SynTec Systems

- 6.4.2 Dow

- 6.4.3 GAF Inc.

- 6.4.4 Henry Company

- 6.4.5 HOLCIM

- 6.4.6 IB Roof Systems

- 6.4.7 IKO Polymeric

- 6.4.8 Johns Manville

- 6.4.9 Kingspan Group

- 6.4.10 Owens Corning

- 6.4.11 Polygomma

- 6.4.12 Sika AG

- 6.4.13 Siplast Inc.

- 6.4.14 SOPREMA

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Demand for Energy-efficient Roofing Membranes

- 7.2 Advancements in Technology

- 7.3 Other Opportunities