|

시장보고서

상품코드

1684036

독일의 적층 세라믹 커패시터(MLCC) 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Germany MLCC - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

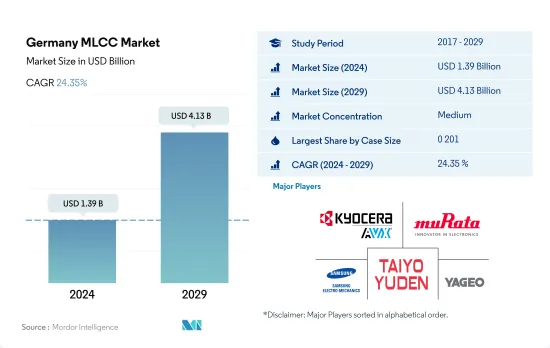

독일의 적층 세라믹 커패시터(MLCC) 시장 규모는 2024년에 13억 9,000만 달러로 평가되었고, 2029년에는 41억 3,000만 달러에 이를 전망이며, 시장 추계 및 예측 기간인 2024-2029년 CAGR은 24.35%를 나타낼 것으로 예측됩니다.

웨어러블 의료기기 이용 증가, PC나 5G 대응 스마트폰 등 소비자 전자기기의 보급이 적층 세라믹 커패시터(MLCC) 수요 견인

- 2022년 수량 기준으로 0 201 케이스 크기 부문이 최고 러너로 부상하여 36.64%의 최대 시장 점유율을 획득하였고, 이어서 0 402 케이스 크기 부문이 14.94%, 0 603 케이스 크기 부문이 13.84%의 점유율을 획득했습니다.

- 케이스 크기 0 402는 가장 컴팩트하며 회로 보드의 부품 밀도를 높일 수 있습니다. 독일 소비자들은 건강과 웰빙에 대한 관심 증가로 피트니스 트래커와 스마트 워치와 같은 웨어러블 의료기기의 사용을 늘리고 있습니다. 예를 들어 독일에서는 2021년에 74,485명이 만성 허혈성 심장 질환으로 사망했습니다. 100uF 미만의 낮은 커패시턴스를 가진 X7R 유전체 0 402 적층 세라믹 커패시터(MLCC)의 요구는 심장 박동기와 제세동기와 같은 심장혈관계 장비에서 안정적이고 효율적인 전력 성능을 유지하는 데 필수적인 역할을 하기 때문에 의료 장비 증가가 예상됩니다.

- 0 603 소형 적층 세라믹 커패시터(MLCC)는 스마트폰, 태블릿, 노트북, 디지털 카메라, 게임기 등 소비자용 전자기기 산업에서 널리 사용되고 있습니다. 컴팩트한 크기와 높은 커패시턴스, 부드러운 통합으로 인기가 높습니다. 0 603 적층 세라믹 커패시터(MLCC) 수요를 견인하는 것은 독일의 가전 산업입니다. PC, 노트북, 에어컨, 냉장고와 같은 가전제품에는 100uF의 낮은 커패시턴스를 가진 0603 적층 세라믹 커패시터(MLCC)와 같은 소형화 부품이 필요합니다.

독일의 적층 세라믹 커패시터(MLCC) 시장 동향

전동 소형 상용차가 시장에 호영향을 미칠 전망

- 소형 상용차는 독일 상용차 시장의 중요한 부분을 차지합니다. 2019년 당시 이 나라에서는 약 2만 8,350대의 소형 상용차가 제조되었습니다.

- COVID-19의 대유행으로 인해 소형 상용차 업계에서는 이전에 없었던 공급망 문제를 일으키는 봉쇄 및 기타 제한이 발생했습니다. 팬데믹은 국내에서 전례가 없는 수준과 유형의 이동 및 여행 제한을 일으켰습니다. 인프라, 운송, 물류 등 물자를 운송하는 최종 사용자 산업은 완전히 작동을 멈추고 제조업과 화물업계에 새로운 과제를 부과했습니다.

- 도시 교통의 중심적인 존재인 소형 상용차(eLCV)는 교통 관련 배출 가스에 대항하는 독일 대처의 다음 단계입니다. 2018년 독일에서 신규 등록된 LCV 중 전 전기차는 2% 미만이었습니다. 디젤 엔진은 여전히 이 시장을 독점하고 있습니다.

- 정부는 향후 몇 년동안 전기자동차의 보급을 가속화하기 위해 배터리, 자동차, 충전소, 디지털 이동성 앱, ICT, 스마트 이동성 및 에너지 서비스 개발을 선호하고 있습니다. 소형 상용차 수요는 전자상거래 및 물류활동의 성장에 따라 증가할 것으로 예상됩니다.

ADAS 채용 증가로 승용차 수요 촉진

- 독일은 유럽에서 두 번째로 인구가 많으며 이 지역에서 가장 큰 경제대국입니다. 승용차 생산량은 2019년부터 2022년까지 감소했습니다. 2019년 생산량 460만 대는 2022년에는 348만 대로 감소합니다. 4년간의 CAGR이 약 -7.06%였던 것은 유럽 자동차 산업이 만난 어려운 시장 환경 및 혼란을 반영하고 있습니다.

- 팬데믹(세계적 유행병)으로 인한 봉쇄 기간 동안 일부 거점에서 생산이 중단되었지만, 이는 이미 기업이 디젤 차량이나 가솔린 차량에서 '환경 친화적인' 전기자동차로의 이동에 어려움을 겪었을 때 일어났습니다. 이는 독일 수출형 경제의 주역인 자동차 산업에 타격을 주었습니다.

- 독일 정부의 장기 목표 중 하나는 화석 연료에서의 철수 및 전기자동차 증가입니다. 독일의 전기자동차 판매량은 2022년까지 매년 증가했습니다. 자동차 자체의 가격이나 국내 물가 상승이 이 숫자의 요인인 것은 틀림없지만, 또 하나는 전기자동차를 충전하기 위한 인프라가 아직 개발 도상이라는 것입니다. 플러그인 하이브리드 자동차에 대한 보조금 중단도 전기자동차 시장을 감속시키고 있습니다.

- AI와 IoT의 진화와 의존도가 높아짐에 따라 자동차 수요는 더 이상 전기자동차에만 머물지 않습니다. ADAS 소프트웨어가 미래의 승용차를 견인하는 요인이 되어 적층 세라믹 커패시터(MLCC) 수요가 증가합니다. 여러 기업이 조인트 벤처와 파트너십을 맺고 경쟁사보다 우위를 차지하기 때문에 새로운 제품을 출시하고 있습니다. 2022년 1월 보쉬와 폭스바겐의 자회사인 카리아드는 자율주행차와 선진운전 지원 시스템의 신기술을 개발하기 위해 제휴를 맺었습니다.

독일의 적층 세라믹 커패시터(MLCC) 산업 개요

독일의 적층 세라믹 커패시터(MLCC) 시장은 적당히 통합되어 상위 5개사에서 43.45%를 차지하고 있습니다. 이 시장 주요 기업은 다음과 같습니다. Kyocera AVX Components Corporation(Kyocera Corporation), Murata Manufacturing, Samsung Electro-Mechanics, Taiyo Yuden 및 Yageo Corporation.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 주요 요약 및 주요 조사 결과

제2장 보고서 제안

제3장 서문

- 조사 전제조건 및 시장 정의

- 조사 범위

- 조사 방법

제4장 주요 산업 동향

- 가전 판매

- 에어컨 판매 대수

- 데스크톱 PC 판매 대수

- 게임기 판매 대수

- 노트북 PC 판매 대수

- 냉장고 판매 대수

- 스마트폰 판매 대수

- 수납 기기 판매 대수

- 태블릿 판매 대수

- TV 판매 대수

- 자동차 생산

- 소형 상용차 생산

- 승용차 생산

- 자동차 생산

- 전기자동차 생산

- BEV(배터리 전기자동차)의 생산

- PHEV(플러그인 하이브리드차) 생산

- 산업용 자동화 매출액

- 산업용 로봇 판매

- 서비스 로봇 판매

- 규제 프레임워크

- 밸류체인 및 유통채널 분석

제5장 시장 세분화

- 유전체 유형별

- 클래스 1

- 클래스 2

- 케이스 사이즈별

- 0 201

- 0 402

- 0 603

- 1 005

- 1 210

- 기타

- 전압별

- 500V-1000V

- 500V 미만

- 1000V 이상

- 정전 용량별

- 100uF-1,000uF

- 100uF 미만

- 1,000uF 이상

- 적층 세라믹 커패시터(MLCC) 실장 유형별

- 금속 캡

- 레이디얼 리드

- 표면 실장

- 최종 사용자별

- 항공우주 및 방위

- 자동차

- 소비자용 전자기기

- 산업기기

- 의료기기

- 전력 및 유틸리티

- 통신 기기

- 기타

제6장 경쟁 구도

- 주요 전략 동향

- 시장 점유율 분석

- 기업 상황

- 기업 프로파일

- Kyocera AVX Components Corporation(Kyocera Corporation)

- Maruwa Co ltd

- Murata Manufacturing Co., Ltd

- Nippon Chemi-Con Corporation

- Samsung Electro-Mechanics

- Samwha Capacitor Group

- Taiyo Yuden Co., Ltd

- TDK Corporation

- Vishay Intertechnology Inc.

- Walsin Technology Corporation

- Wurth Elektronik GmbH & Co. KG

- Yageo Corporation

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

- 세계 개요

- 개요

- Porter's Five Forces 분석 프레임워크

- 세계 밸류체인 분석

- 시장 역학(DROs)

- 정보원 및 참고문헌

- 도표 일람

- 주요 인사이트

- 데이터 팩

- 용어집

The Germany MLCC Market size is estimated at 1.39 billion USD in 2024, and is expected to reach 4.13 billion USD by 2029, growing at a CAGR of 24.35% during the forecast period (2024-2029).

The increasing utilization of wearable medical devices and the rising adoption of consumer electronics like PCs and 5G-enabled smartphones driving MLCC demand

- The 0 201 case size segment emerged as the frontrunner, capturing the largest market share of 36.64%, followed by the 0 402 case size segment, with a 14.94% share, and the 0 603 case size segment, with 13.84%, in terms of volume in 2022.

- The case size of 0 402 is among the most compact available, thus increasing the component density of the circuit board. German consumers are increasingly using wearable medical devices like fitness trackers and smartwatches due to increased interest in health and wellbeing. For instance, in Germany, 74,485 passed away due to chronic ischaemic heart disease in 2021. The need for 0 402 MLCCs with X7R dielectric with low capacitance of less than 100uF is expected to grow in medical devices in cardiovascular devices like pacemakers and defibrillators due to their essential role in sustaining dependable and efficient power performance.

- 0 603 compact MLCCs are widely used in consumer electronic industries such as smartphones, tablets, laptop computers, digital cameras, and gaming consoles. They are popular due to their compact size and high capacitance, as well as their smooth integration. The demand for 0 603 MLCCs is being driven by Germany's consumer electronics industry. Consumer electronics like PCs, laptops, air conditioners, and refrigerators require miniaturized components like 0 603 MLCCs with low capacitance of 100uF.

Germany MLCC Market Trends

Electric light commercial vehicles are expected to have a positive impact on the market

- Light commercial vehicles represent an important part of the commercial vehicle market in Germany. As of 2019, roughly 28.35 thousand light commercial vehicles were manufactured in the country.

- The COVID-19 pandemic resulted in lockdowns and other restrictions that caused supply chain issues in the light commercial vehicle industry that had never been seen before. The pandemic caused unprecedented levels and types of mobility and travel limitations in the country. End-user industries that transport goods, such as infrastructure, transportation, and logistics, were completely shut down, posing new challenges for the manufacturing and freight industries.

- Electric light commercial vehicles (eLCVs), the centerpiece of urban transport, are the next step in Germany's endeavors to combat traffic-related emissions. eLCVs have struggled to build significant market demand so far. In 2018, less than 2% of all newly registered LCVs in Germany were all-electric vehicles. Diesel engines still dominate this market.

- The government has prioritized the development of batteries, cars, charging stations, digital mobility apps, ICT, smart mobility, and energy services in order to speed up the adoption of electric vehicles in the next years. The demand for electric light commercial vehicles is anticipated to increase due to the growth of e-commerce and logistical activities.

Increased adoption of ADAS is propelling the demand for passenger vehicles

- Germany is the second most populous country in Europe and has the largest economy in the region. The production of passenger vehicles witnessed a decline from 2019 to 2022. The production volume of 4.6 million units in 2019 decreased to 3.48 million units in 2022. The observed CAGR of approximately -7.06% over the four-year period mirrors the difficult market conditions and disruptions encountered by the European automotive industry.

- During the pandemic-resultant lockdown, production was stopped at some sites, which happened when companies were already struggling to shift from diesel- and gasoline-powered cars toward "green" electric vehicles. This hit the car industry, the main driver of Germany's export-based economy.

- One of the long-term targets of the German government is a fossil fuel exit and an increase in electric vehicles. German electric car sales increased annually until 2022. While the prices of the vehicles themselves and the rising cost of living in the country are undoubtedly contributing factors to these numbers, another is the still-developing infrastructure for charging electric cars. Discontinuation of subsidies for plug-in hybrids is also slowing the electric vehicles market.

- With advancements in AI and IoT and ever-growing dependence, the demand for automobiles is no longer limited to electric vehicles. ADAS software will become the driving factor for the future of passenger vehicles, thereby increasing the demand for MLCCs. Several companies are entering joint ventures and partnerships to launch newer products to have an edge over their competitors. In January 2022, Bosch and Cariad, Volkswagen's subsidiary, formed a partnership to develop new technology for automated vehicles and advanced driver-aid systems.

Germany MLCC Industry Overview

The Germany MLCC Market is moderately consolidated, with the top five companies occupying 43.45%. The major players in this market are Kyocera AVX Components Corporation (Kyocera Corporation), Murata Manufacturing Co., Ltd, Samsung Electro-Mechanics, Taiyo Yuden Co., Ltd and Yageo Corporation (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Consumer Electronics Sales

- 4.1.1 Air Conditioner Sales

- 4.1.2 Desktop PC's Sales

- 4.1.3 Gaming Console Sales

- 4.1.4 Laptops Sales

- 4.1.5 Refrigerator Sales

- 4.1.6 Smartphones Sales

- 4.1.7 Storage Unit Sales

- 4.1.8 Tablets Sales

- 4.1.9 Television Sales

- 4.2 Automotive Production

- 4.2.1 Light Commercial Vehicles Production

- 4.2.2 Passenger Vehicles Production

- 4.2.3 Total Motor Production

- 4.3 Ev Production

- 4.3.1 BEV (Battery Electric Vehicle) Production

- 4.3.2 PHEV (Plug-in Hybrid Electric Vehicle) Production

- 4.4 Industrial Automation Sales

- 4.4.1 Industrial Robots Sales

- 4.4.2 Service Robots Sales

- 4.5 Regulatory Framework

- 4.6 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

- 5.1 Dielectric Type

- 5.1.1 Class 1

- 5.1.2 Class 2

- 5.2 Case Size

- 5.2.1 0 201

- 5.2.2 0 402

- 5.2.3 0 603

- 5.2.4 1 005

- 5.2.5 1 210

- 5.2.6 Others

- 5.3 Voltage

- 5.3.1 500V to 1000V

- 5.3.2 Less than 500V

- 5.3.3 More than 1000V

- 5.4 Capacitance

- 5.4.1 100µF to 1000µF

- 5.4.2 Less than 100µF

- 5.4.3 More than 1000µF

- 5.5 Mlcc Mounting Type

- 5.5.1 Metal Cap

- 5.5.2 Radial Lead

- 5.5.3 Surface Mount

- 5.6 End User

- 5.6.1 Aerospace and Defence

- 5.6.2 Automotive

- 5.6.3 Consumer Electronics

- 5.6.4 Industrial

- 5.6.5 Medical Devices

- 5.6.6 Power and Utilities

- 5.6.7 Telecommunication

- 5.6.8 Others

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Kyocera AVX Components Corporation (Kyocera Corporation)

- 6.4.2 Maruwa Co ltd

- 6.4.3 Murata Manufacturing Co., Ltd

- 6.4.4 Nippon Chemi-Con Corporation

- 6.4.5 Samsung Electro-Mechanics

- 6.4.6 Samwha Capacitor Group

- 6.4.7 Taiyo Yuden Co., Ltd

- 6.4.8 TDK Corporation

- 6.4.9 Vishay Intertechnology Inc.

- 6.4.10 Walsin Technology Corporation

- 6.4.11 Wurth Elektronik GmbH & Co. KG

- 6.4.12 Yageo Corporation

7 KEY STRATEGIC QUESTIONS FOR MLCC CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms