|

시장보고서

상품코드

1684037

항공우주 및 방위용 MLCC 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Aerospace and Defence MLCC - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

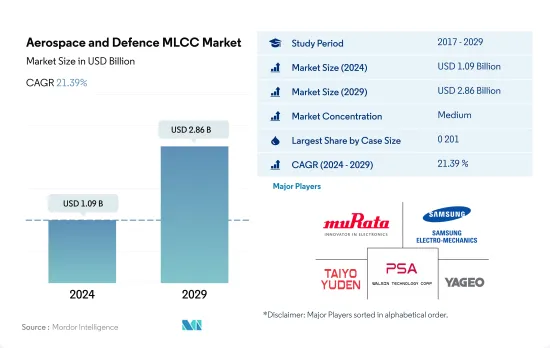

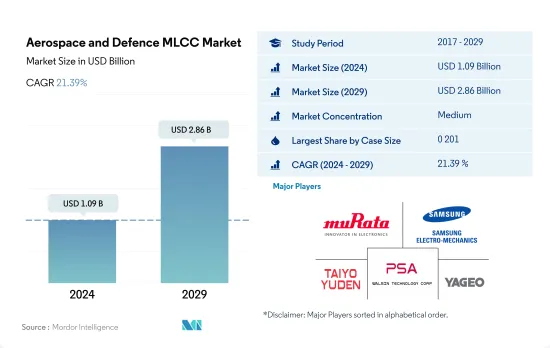

항공우주 및 방위용 MLCC 시장 규모는 2024년에 10억 9,000만 달러로 평가되었고, 2029년에는 28억 6,000만 달러에 이를 것으로 예측되며, 예측 기간인 2024-2029년 CAGR 21.39%로 성장할 전망입니다.

최적화된 아비오닉 MLCC의 선택이 항공우주 및 방위 시스템 강화

- 항공우주 및 방위 산업은 AI, IoT, 5G 통신을 포함한 첨단 어비오닉스 기술의 채용이 진행되고 있는 가운데, 급속한 변모를 이루고 있습니다. 이러한 추세는 항공기의 최첨단 전자 시스템을 지원하기 위해 높은 커패시턴스, 낮은 ESR 및 신뢰성 향상을 갖춘 MLCC의 필요성을 뒷받침합니다. 케이스 크기 0 201 및 0 402의 MLCC는 어비오닉스의 소형 및 경량 전자 회로에 인기가 있습니다. 소형 폼 팩터와 높은 커패시턴스는 UAV 및 기타 소형 항공기에 장착되는 비행 제어 시스템, 내비게이션 시스템, 통신 장비 등의 소형화 디바이스에 이상적입니다. 항공전자기기의 소형화 및 경량화의 동향은 케이스 사이즈 0 201 및 0 402 MLCC 수요를 견인하고 있습니다.

- 케이스 크기 0 603 및 1 005의 MLCC는 소형화와 커패시턴스의 균형을 이루며 다양한 항공 전자기기 용도에서 다재다능한 부품이 되었습니다. 이들은 일반적으로 조종석 디스플레이, 센서 시스템, 유인 및 무인 항공기의 배전 네트워크에 사용됩니다. 최신 항공기에서는 고급 어비오닉스 시스템의 채용이 증가하고 있으며, 케이스 크기 0 603 및 1 005 MLCC에 대한 수요가 증가하고 있습니다.

- 케이스 크기 1 210의 MLCC는 높은 커패시턴스 값을 제공하며 항공 전자기기의 전력 관리, 에너지 저장 및 필터링 용도에 적합합니다. 이 대형 MLCC는 일반적으로 레이더 시스템, 위성 통신 및 고급 어비오닉스 제어 장치와 같은 중요한 어비오닉스 시스템에서 사용됩니다. 보다 강력하고 정교한 바이오닉스 기술에 대한 요구 증가는 케이스 크기 1 210 및 기타 MLCC 수요에 기여합니다. UAV와 MAV에 대한 수요가 증가하고 있으며 MLCC는 안정적이고 효율적인 전자 부품의 작동을 보장하는 중요한 역할을 담당합니다.

방위비 증가와 지정학적 다이나믹스 속에서 항공우주 및 방위용 MLCC 시장은 세계적으로 성장

- 항공우주 및 방위용 MLCC 시장은 세계적으로 견조한 성장을 이루고 있습니다. 중국과 인도가 견인하는 아시아태평양에서는 2022년에 3억 6,203만 달러의 매출을 기록했고, 2028년에는 10억 6,000만 달러로 급증할 것으로 예측되며, 2023년부터 2028년까지의 CAGR은 20.37%로 견조한 성장세를 보일 전망입니다. 2023년부터 2024년도까지 예산이 59.4억 루피에 이르는 인도는 MLCC가 특히 무인항공기(UAV)의 방위 능력을 향상시키는 데 있어 매우 중요한 역할을 담당하고 있음을 강조하고 있습니다.

- 유럽은 국방비의 현저한 증가를 보였으며 2020년부터 2021년까지 3% 증가를 반영하여 2021년까지 1억 1,605만 달러에 달했습니다. 2022년 러시아와 우크라이나 간의 분쟁이 발생한 가운데 유럽은 방위력을 강화했으며, 그 결과 방위비는 14% 증가한 3,450억 달러로 급증했습니다. MLCC는 이러한 상황에서 중요한 역할을 수행하고, 군용기 및 방위 시스템에서 신호의 무결성을 확보하고, 2028년까지 3억 3,116만 달러라는 이 분야의 예상 수익 목표에 공헌하고 있습니다.

- 북미는 세계 군사비의 지배적 세력으로 방위에 많은 투자를 하고 있으며, 2022년 누적 지출은 9,120억 달러에 달했습니다. 특히 미국의 항공우주 및 방위 부문은 3,910억 달러의 경제 공헌을 하고 있으며, MLCC는 군용기 및 전자전방위 시스템의 확실한 운용에 매우 중요한 역할을 하고 있습니다.

- 중동, 아프리카 및 남미를 포함한 세계 기타 지역은 지정 과제, 테러 위협 및 국방 지출 증가를 위해 노력하고 있습니다. 이러한 지역 전체에서 항공우주 및 방위용 MLCC 시장은 경제역학, 지정학적 영향, 방위 우선순위의 수렴을 반영하고 있으며, MLCC는 항공우주 및 방위 시스템의 신뢰성과 효율을 확보하는 중요한 부품으로 부상하고 있습니다.

세계의 항공우주 및 방위용 MLCC 시장 동향

모니터링 솔루션 개선에 대한 수요 증가가 시장을 뒷받침

- MLCC 수요는 항공우주 및 방위(A&D) 분야, 특히 군용기나 UAV와 같은 전자전방위 시스템 등의 용도로 높아지고 있습니다. 이러한 산업에서는 특정 기능을 가진 부품을 활용하는 신뢰할 수 있는 파워 일렉트로닉스 시스템이 필요합니다. MLCC는 높은 신뢰성, 고품질 인자에 의한 최적 성능, 효과적인 EMI 억제, 노이즈 감소, 라인 필터링, 에너지 축적 기능, 고주파 노이즈 디커플링, 전압 레귤레이션 기능을 제공하기 때문에 이러한 요구를 충족시키는 데 매우 중요합니다. MLCC는 UAV 및 기타 항공우주 및 방위 전력 전자 시스템의 안정적인 작동을 보장하는 데 매우 중요합니다.

- UAV의 생산 대수는 2021년 384만 7,000대에서 2022년에는 444만 8,000대로 14%의 대폭 증가를 기록했습니다. 이러한 성장으로 인해 특히 UAV용, 특히 고전압 전원 용도을 위한 MLCC 수요가 크게 증가하고 있습니다. MLCC는 UAV에서 전원 바이패스 커패시터, DC-DC 컨버터의 입출력 필터, 평활 커패시터, 디지털 회로 및 LCD 모듈의 필수 부품으로서 중요한 역할을 하고 있습니다. A&D 기업은 특정 요구 사항을 충족하고 시스템 성능을 향상시키는 MLCC의 가치와 중요성을 점점 더 인식하고 있습니다.

- 소형화와 기능 강화 등 MLCC의 진보는 수요를 증대시키고 있습니다. 그 결과, 보다 고성능인 자동 조종 시스템의 개발이나 기능을 손상시키지 않고 MLCC를 컴팩트하게 통합함으로써 용이해진 실시간 UAV 용도의 확대로 이어지고 있습니다. 고신뢰성과 고속 응답 시간 등 MLCC의 기능 향상이 실시간 UAV 용도의 채용에 박차를 가하고 있습니다.

지정학적 긴장 증가 및 노후화된 군용기를 대체하기 위한 근대화 계획이 군사 지출을 촉진하고 있습니다.

- MLCC는 방위용 전자 기기에 필수적인 부품으로, 중요한 에너지 저장 및 신호 필터링 기능을 제공합니다. MLCC 수요는 방위비의 변동에 직접 영향을 받으며, 특히 미사일 시스템이나 방위 통신기기 등의 분야에서는 지출 증가가 수요 증가를 촉진합니다. 그러나 COVID-19 팬데믹 시 국방 지출의 감소는 업계가 의료 기술에 중점을 옮겨 MLCC 시장에 부정적인 영향을 미쳤습니다. 방위비의 안정화에 따라 방위용 전자기기의 MLCC 수요는 회복될 것으로 예상됩니다.

- COVID-19 팬데믹은 세계의 우선순위가 의료기술 및 실험용 시험장치로 이동했기 때문에 방위전자에 중대한 영향을 미쳤습니다. 이 때문에 고신뢰성 방위용 전자 기기에 대한 수요가 감소하여 고전압 방위 시장을 안정시키기 위한 노력이 필요하게 되었습니다. 팬데믹은 많은 방위 수직 플랫폼에도 악영향을 미치고, 예기치 않은 혼란에 직면했을 때의 적응성과 회복력의 중요성을 부각시켰습니다.

- 2012년부터 2016년까지 정부의 긴축 재정의 결과로 방위 시장은 정체되었습니다. 그러나 2017년부터 2019년까지는 현저한 호전이 일어나 항공기나 우주 전자기기 등 특정한 좁은 최종 시장 분야에서 현저한 성장이 보였습니다. 그러나 2020년에는 팬데믹이 이 성장 궤도를 방해하여 방위용 전자기기 수요가 11% 감소했습니다. 미국의 주도권이 교체됨에 따라 2022년까지의 국방 지출은 억제되었습니다. 그럼에도 불구하고 2023년에는 미사일과 미사일 방위 시스템에 초점을 맞춘 소규모의 정밀한 유럽 방위 전자 시장에 새로운 비즈니스 기회가 생길 것으로 예상되었습니다.

항공우주 및 방위 MLCC 산업 개요

항공우주 및 방위용 MLCC 시장은 적당히 통합되어 상위 5개사에서 44.17%를 차지하고 있습니다. 이 시장 주요 기업은 다음과 같습니다. Murata Manufacturing, Samsung Electro-Mechanics, Taiyo Yuden, Walsin Technology Corporation 및 Yageo Corporation(알파벳순 정렬).

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 주요 요약 및 주요 조사 결과

제2장 보고서 제안

제3장 서문

- 조사 전제조건 및 시장 정의

- 조사 범위

- 조사 방법

제4장 주요 산업 동향

- 무인 항공기 생산

- 세계의 무인 항공기 생산 대수

- 군사 지출

- 세계의 군사 지출

- 규제 프레임워크

- 밸류체인 및 유통채널 분석

제5장 시장 세분화

- 차량 유형별

- 유인 항공기

- 무인 항공기

- 케이스 사이즈별

- 0 201

- 0 402

- 0 603

- 1 005

- 1 210

- 기타

- 전압별

- 600V-1100V

- 600V 미만

- 1100V 이상

- 정전 용량별

- 10μF-100μF

- 10μF 미만

- 100μF 이상

- 유전 유형별

- 클래스 1

- 클래스 2

- 지역별

- 아시아태평양

- 유럽

- 북미

- 세계 기타 지역

제6장 경쟁 구도

- 주요 전략 동향

- 시장 점유율 분석

- 기업 상황

- 기업 프로파일

- Kyocera AVX Components Corporation(Kyocera Corporation)

- Maruwa Co ltd

- Murata Manufacturing Co., Ltd

- Nippon Chemi-Con Corporation

- Samsung Electro-Mechanics

- Samwha Capacitor Group

- Taiyo Yuden Co., Ltd

- TDK Corporation

- Vishay Intertechnology Inc.

- Walsin Technology Corporation

- Yageo Corporation

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

- 세계 개요

- 개요

- Porter's Five Forces 분석 프레임워크

- 세계 밸류체인 분석

- 시장 역학(DROs)

- 정보원 및 참고문헌

- 도표 일람

- 주요 인사이트

- 데이터 팩

- 용어집

The Aerospace and Defence MLCC Market size is estimated at 1.09 billion USD in 2024, and is expected to reach 2.86 billion USD by 2029, growing at a CAGR of 21.39% during the forecast period (2024-2029).

Optimized avionic MLCC selection enhances aerospace and defense systems

- The aerospace and defense industries are witnessing a rapid transformation with the increasing adoption of advanced avionics technologies, including AI, IoT, and 5G communications. These trends drive the need for MLCCs with higher capacitance, lower ESR, and improved reliability to support cutting-edge electronic systems in aircraft. Case sizes 0 201 and 0 402 MLCCs are popular for compact and lightweight electronic circuits in avionics. Their small form factor and high capacitance make them ideal for miniaturized devices, such as flight control systems, navigation systems, and communication equipment in UAVs and other small aircraft. The trend toward miniaturization and weight reduction in avionics drives the demand for case sizes 0 201 and 0 402 MLCCs.

- Case sizes 0 603 and 1 005 MLCCs balance compactness and capacitance, making them versatile components in various avionic applications. They are commonly used in cockpit displays, sensor systems, and power distribution networks in manned and unmanned aerial vehicles. The increasing adoption of advanced avionics systems in modern aircraft enhances the demand for case sizes 0 603 and 1 005 MLCCs.

- Case size 1 210 MLCCs offer higher capacitance values and are well-suited for power management, energy storage, and filtering applications in avionics. These larger-sized MLCCs are commonly utilized in critical avionic systems like radar systems, satellite communications, and advanced avionics control units. The evolving need for more powerful and sophisticated avionic technologies contributes to the demand for case sizes 1 210 and other MLCCs. The demand for UAVs and MAVs is growing, and MLCCs play a vital role in ensuring stable and efficient electronic components for successful operation.

The global aerospace and defense MLCC market thrives amid rising defense expenditures and geopolitical dynamics

- The aerospace and defense MLCC market experiences robust growth globally. In Asia-Pacific, led by China and India, the segment generated USD 362.03 million in 2022, with a projected surge to USD 1.06 billion by 2028, showcasing a robust CAGR of 20.37% from 2023 to 2028. India, with a substantial INR 5.94 lakh crore budget for FY 2023-24, emphasizes MLCCs' pivotal role in advancing defense capabilities, particularly in unmanned aerial vehicles (UAVs).

- Europe witnessed a noteworthy uptick in defense spending, reaching USD 116.05 million by 2021, reflecting a 3% increase from 2020 to 2021. Amid the Russia-Ukraine conflict in 2022, Europe reinforced its defense capabilities, resulting in a 14% surge in defense expenditures to USD 345 billion. MLCCs play a vital role in this context, ensuring signal integrity in military aircraft and defense systems and contributing to the sector's envisioned revenue target of USD 331.16 million by 2028.

- North America, as the dominant force in global military expenditures, invests significantly in defense, with a cumulative expenditure of USD 912 billion in 2022. The aerospace and defense sector, particularly in the United States, contributes USD 391 billion to the economy, with MLCCs playing a pivotal role in ensuring the reliable operation of military aircraft and electronic warfare defense systems.

- The Rest of the World, encompassing the Middle East, Africa, and South America, grapples with geopolitical challenges, terrorism threats, and increased defense spending. Across these regions, the aerospace and defense MLCC market reflects a convergence of economic dynamics, geopolitical influences, and defense priorities, with MLCCs emerging as critical components ensuring the reliability and efficiency of aerospace and defense systems.

Global Aerospace and Defence MLCC Market Trends

Growing demand for improved surveillance solutions is propelling the market

- The demand for MLCCs is rising in the aerospace and defense (A&D) sectors, especially in applications such as military aircraft and electronic warfare defense systems like UAVs. These industries require reliable power electronic systems that utilize components with specific functionalities. MLCCs are crucial in meeting these demands as they offer high reliability, optimal performance with a high-quality factor, effective EMI suppression, noise reduction, line filtering, energy storage capabilities, decoupling of high-frequency noise, and voltage regulation capabilities. MLCCs are critical in ensuring the dependable operation of UAVs and other aerospace and defense power electronic systems.

- The production of UAVs experienced a significant 14% increase from 3.847 million in 2021 to 4.448 million in 2022. This growth has led to a substantial rise in the demand for MLCCs, particularly for UAVs, specifically for high-voltage power supply applications. MLCCs play critical roles in UAVs as power supply bypass capacitors, input/output filters in DC-DC converters, smoothing capacitors, and essential components in digital circuits and LCD modules. A&D companies are increasingly recognizing the value and significance of MLCCs in meeting their specific requirements and enhancing the performance of their systems.

- Advancements in MLCCs, including smaller sizes and enhanced capabilities, have increased demand. This has led to the development of more capable autopilot systems and the expansion of real-time UAV applications facilitated by the compact integration of MLCCs without compromising functionality. Improved capabilities of MLCCs, such as high reliability and fast response times, have fueled the adoption of real-time UAV applications.

Growing geopolitical tensions and the modernization plans to replace aging military aircraft are propelling military spending

- MLCCs are vital components in defense electronics, providing crucial energy storage and signal filtering capabilities. The demand for MLCCs is directly influenced by fluctuations in defense spending, with increased spending driving higher demand, particularly in areas such as missile systems and defense communication equipment. However, the decline in defense spending during the COVID-19 pandemic negatively affected the MLCC market as the industry shifted focus to medical technology. As defense spending stabilizes, the demand for MLCCs in defense electronics is expected to rebound.

- The COVID-19 pandemic had significant implications for defense electronics as global priorities shifted toward medical technology and laboratory test equipment. This led to a decline in demand for high-reliability defense electronics, requiring efforts to stabilize the high-voltage defense markets. The pandemic also adversely affected many defense vertical platforms, highlighting the importance of adaptability and resilience in the face of unexpected disruptions.

- Between 2012 and 2016, government-imposed sequestering resulted in a stagnant defense market. However, a notable turnaround occurred from 2017 to 2019, with remarkable growth in specific narrow end-market areas such as aircraft and space electronics. However, the pandemic disrupted this growth trajectory in 2020, causing an 11% decline in defense electronics demand. The shift in the US leadership restrained defense spending through 2022. Nonetheless, 2023 was expected to bring new opportunities in the small and precise European markets for defense electronics, focused on missiles and missile defense systems.

Aerospace and Defence MLCC Industry Overview

The Aerospace and Defence MLCC Market is moderately consolidated, with the top five companies occupying 44.17%. The major players in this market are Murata Manufacturing Co., Ltd, Samsung Electro-Mechanics, Taiyo Yuden Co., Ltd, Walsin Technology Corporation and Yageo Corporation (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Aerial Vehicle Production

- 4.1.1 Global Unmanned Aerial Vehicles Production

- 4.2 Military Spending

- 4.2.1 Global Military Spending

- 4.3 Regulatory Framework

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

- 5.1 Vehicle Type

- 5.1.1 Manned Aerial Vehicle

- 5.1.2 Unmanned Aerial Vehicle

- 5.2 Case Size

- 5.2.1 0 201

- 5.2.2 0 402

- 5.2.3 0 603

- 5.2.4 1 005

- 5.2.5 1 210

- 5.2.6 Others

- 5.3 Voltage

- 5.3.1 600V to 1100V

- 5.3.2 Less than 600V

- 5.3.3 More than 1100V

- 5.4 Capacitance

- 5.4.1 10 μF to 100 μF

- 5.4.2 Less than 10 μF

- 5.4.3 More than 100 μF

- 5.5 Dielectric Type

- 5.5.1 Class 1

- 5.5.2 Class 2

- 5.6 Region

- 5.6.1 Asia-Pacific

- 5.6.2 Europe

- 5.6.3 North America

- 5.6.4 Rest of the World

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Kyocera AVX Components Corporation (Kyocera Corporation)

- 6.4.2 Maruwa Co ltd

- 6.4.3 Murata Manufacturing Co., Ltd

- 6.4.4 Nippon Chemi-Con Corporation

- 6.4.5 Samsung Electro-Mechanics

- 6.4.6 Samwha Capacitor Group

- 6.4.7 Taiyo Yuden Co., Ltd

- 6.4.8 TDK Corporation

- 6.4.9 Vishay Intertechnology Inc.

- 6.4.10 Walsin Technology Corporation

- 6.4.11 Yageo Corporation

7 KEY STRATEGIC QUESTIONS FOR MLCC CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms