|

시장보고서

상품코드

1684081

남미의 건설용 화학제품 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)South America Construction Chemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

■ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송일정은 문의해 주시기 바랍니다.

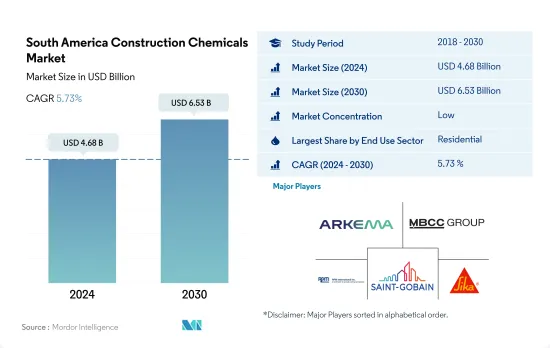

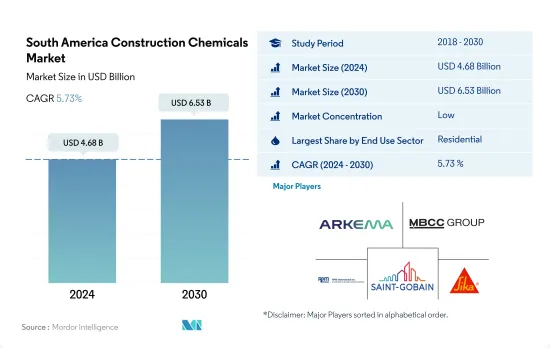

남미의 건설용 화학제품 시장 규모는 2024년에 46억 8,000만 달러로 평가되었고, 2030년에는 65억 3,000만 달러에 이를 전망이며, 예측 기간인 2024-2030년 CAGR 5.73%로 성장할 것으로 예측됩니다.

Procrear 2023 및 Minha Casa, Minha Vida 주택 계획이 남미의 건설용 화학제품 수요에 미치는 영향

- 남미의 건설용 화학제품 수요는 2022년에 5.89% 증가했지만, 이는 주로 건설 활동의 급증에 의한 것입니다. 특히 브라질에서는 2022년 신규 주택 바닥 면적이 전년 대비 4.1% 증가했습니다. 상업 부문과 인프라 부문이 견인역이 되어 남미의 건설용 화학제품 시장은 2023년 금액 기준으로 2022년 대비 5.55% 성장한 것으로 평가됩니다.

- 남미에서는 아르헨티나와 브라질이 건설용 화학제품의 소비를 독점하고 있습니다. 특히 양국의 주택 부문이 가장 수요가 높고, 2022년의 모든 최종 사용자 부문에서 차지하는 비율은 각각 30%와 43%였습니다.

- 대부분의 남미 국가에서는 산업 부문과 시설 부문이 건설용 화학제품의 주요 소비자입니다. 그러나 브라질에서는 주택 부문이 2위를 차지하고 있으며, 이 지역에서 2위의 최종 사용자 부문이 되고 있습니다. 브라질과 아르헨티나를 제외하면 2022년 이 지역 기타 국가 전체 수요에 차지하는 산업 및 시설 부문 비율은 45%였습니다.

- 예측에서 브라질과 아르헨티나는 주로 주택 부문을 원동력으로 삼아 건설용 화학제품에 대한 수요가 가장 급증할 전망입니다. 아르헨티나의 'Procrear 2023' 및 브라질의 'Minha Casa, Minha Vida'와 같은 국가적인 주택 이니셔티브는 신축 주택의 건설 및 기존 주택의 개축에 박차를 가하게 됩니다. 그 결과 예측 기간 2023년부터 2030년까지 CAGR 6.36%로 성장할 전망이며 주택 부문이 가장 급속한 수요 증가를 하게 됩니다.

남미의 건설용 화학제품 시장에서 브라질의 우위성 확대

- 2022년에는 주택 부문이 남미의 건설용 화학제품 주요 소비자로 부상하여 전체 분야 총 수요의 약 35%를 차지했습니다. 대규모 주택 부문이 있는 브라질이 이 수요의 선두를 끊었습니다. 2023년을 평가하면 이 지역에서 가장 수요가 급증한 것은 상업 및 인프라 부문이었습니다.

- 이 지역에서 가장 큰 경제 강국이자 가장 인구가 많은 나라인 브라질은 당연히 건설 생산량에서도 선도하고 있습니다. 그 결과 브라질은 건설용 화학제품 소비량도 가장 많습니다. 특히 브라질 주택 부문이 큰 점유율을 차지하고 있어 2022년 국내총소비량의 약 43%를 차지했습니다.

- 브라질에 이어 아르헨티나는 건설용 화학제품의 두 번째 소비국입니다. 아르헨티나에서만 2022년에 3억 7,850만 달러 수요가 있었습니다. 이 수요는 주로 2022년에 2억 2,330만 달러 이상을 차지하는 이 나라 주택, 공업 및 시설 부문이 견인하고 있습니다.

- 브라질 주택 및 산업 및 시설 부문에서는 2030년까지 신설 바닥 면적이 크게 증가할 것으로 예상되며(2022년 대비 각각 37%, 30%) 건설용 화학제품에 대한 수요가 급증할 것으로 전망됩니다. 그 결과 남미에서는 브라질이 건설용 화학제품 시장의 확대를 선도할 것으로 예측되며, 2023년부터 2030년까지 CAGR 6.11%로 성장이 예측됩니다.

남미의 건설용 화학제품 시장 동향

이 지역의 외국 직접투자(FDI) 증가는 향후 수년간 시장 수요를 뒷받침

- 2022년 남미의 상업 부문은 아르헨티나의 9.16% 감소로 크게 견인되었으며 신규 바닥 면적 건설이 16.2%로 크게 감소했습니다. 그러나 이 분야는 2023년에는 회복을 향해 생산량이 4.75% 증가한 것으로 평가되었습니다. 이 성장은 2022년에 이 지역의 다양한 산업이 외국 직접투자(FDI)를 유치함으로써 경제 성장과 상업 건축의 급증에 기인하고 있습니다. 2022년 라틴아메리카 카리브해 경제위원회(ECLAC)는 이 지역의 FDI가 55.2% 증가했다고 보고했습니다.

- 이 부문의 건설량은 2020년에는 15.9%, 2021년에는 3.29%의 현저한 성장을 보였습니다. 이 성장은 남미 정부가 인프라와 건설 부문을 선호한 결과입니다. 남미 정부는 규제를 완화하고 민간 및 유틸리티에서 건설, 유지 보수 및 프로젝트 개발을 허용했습니다. 이 움직임은 중요한 이정표, 기한, 경기 회복 목표를 달성하는 것을 목적으로 하고 있습니다.

- 남미의 상업 부문에서는 신규 바닥 면적 건설이 견조한 성장을 보이며 예측 기간(2023-2030년) CAGR은 수량 기준 4%를 나타낼 것으로 예측되고 있습니다. 이 지역에서는 상업 시설의 건설 상황에 현저한 변화가 있습니다. 2023년에 시작된 파울리니아 데이터센터와 포르투알레그리 데이터센터 i와 같은 주목할 만한 프로젝트는 이 지역에서 가장 큰 것이었습니다. 또한 투자자들은 브라질 오피스 빌딩, 쇼핑 센터, 로지스틱 파크에 주목하고 있으며 앞으로 수년간 시장 수요를 촉진할 것으로 예상됩니다.

남미에서는 저렴한 주택 제도와 보조금이 주택 부문 건설 증가에 영향을 미칩니다.

- 2022년 남미의 주택 부문은 전년 대비 3.35% 증가했습니다. 그러나 아르헨티나는 이 지표에서 9.16%의 현저한 침체를 보였습니다. 2023년에는 2022년보다 3.3% 증가할 것으로 예상되었습니다. 이 성장은 도시화의 진전, 1인당 소득 증가, 전체적인 경기 확대 등의 요인에 의한 것으로, 이들 모두가 주택 수요를 부추기고 있습니다.

- 2020년 COVID-19 팬데믹을 배경으로 남미에서는 신규 바닥 면적 건설이 전년대비 11.83% 증가로 대폭 증가했습니다. 이는 남미 정부의 의도적인 움직임으로 가계 소득의 급격한 감소를 바탕으로 경기후퇴를 완화하고 노동자를 지원하기 위해 건설 부문을 우선시했습니다. 그 결과 검역을 포함한 건설 활동의 한계가 완화되었습니다.

- 남미의 일부 국가에서는 증가하는 인구를 위해 주택을 더 합리적인 가격으로 만들기 위한 이니셔티브를 개발하고 있습니다. 예를 들어, 브라질은 2023년 2월 저소득자를 대상으로 전국 연방 주택 프로그램을 재개했습니다. 2023년 10월, 세계은행은 에콰도르에 대한 1억 달러의 대출 패키지를 승인했습니다. 볼리비아는 저가 주택공급을 확대하고 적정한 가격을 유지하려고 노력하고 있으며 주택 수요를 더욱 환기시키는 태세입니다. 그 결과, 남미의 주택 분야는 예측 기간 중(2023-2030년) 4.09%의 연평균 복합 성장률(CAGR)을 나타낼 것으로 예측됩니다.

남미의 건설용 화학제품 산업의 개요

남미의 건설용 화학제품 시장은 세분화되어 상위 5개사에서 26.38%를 차지하고 있습니다. 이 시장 주요 기업은 다음과 같습니다. Arkema, MBCC Group, RPM International Inc., Saint-Gobain 및 Sika AG.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 주요 요약 및 주요 조사 결과

제2장 보고서 제안

제3장 서문

- 조사 전제조건 및 시장 정의

- 조사 범위

- 조사 방법

제4장 주요 산업 동향

- 최종 용도 분야의 동향

- 상업

- 산업 및 시설

- 인프라

- 주택

- 주요 인프라 프로젝트(현재 및 발표됨)

- 규제 프레임워크

- 밸류체인 및 유통채널 분석

제5장 시장 세분화

- 최종 용도 분야별

- 상업

- 산업 및 시설

- 인프라

- 주택

- 제품별

- 접착제

- 서브 제품별

- 핫멜트

- 반응성

- 용제계

- 수계

- 앵커 및 그라우트

- 서브 제품별

- 시멘트계 고정재

- 수지 고정

- 기타 유형

- 콘크리트 혼화제

- 서브 제품별

- 촉진제

- 공기혼입 혼화제

- 고범위 감수제(초가소제)

- 지연제

- 수축 저감 혼화제

- 점도 조정제

- 감수제(가소제)

- 기타 유형

- 콘크리트 보호 페인트

- 서브 제품별

- 아크릴계

- 알키드

- 에폭시

- 폴리우레탄

- 기타 수지

- 바닥용 수지

- 서브 제품별

- 아크릴

- 에폭시

- 폴리아스파라긴

- 폴리우레탄

- 기타 수지 유형

- 보수 및 재생 화학제품

- 서브 제품별

- 섬유 포장 시스템

- 주입 그라우트재

- 마이크로 콘크리트 모르타르

- 개질 모르타르

- 철근 보호재

- 실링재

- 서브 제품별

- 아크릴

- 에폭시

- 폴리우레탄

- 실리콘

- 기타 수지

- 표면 처리 약품

- 서브 제품별

- 경화 컴파운드

- 이형제

- 기타 제품 유형

- 방수 솔루션

- 서브 제품별

- 화학제품

- 멤브레인

- 접착제

- 국가별

- 아르헨티나

- 브라질

- 기타 남미

제6장 경쟁 구도

- 주요 전략 동향

- 시장 점유율 분석

- 기업 상황

- 기업 프로파일

- Ardex Group

- Arkema

- CEMEX, SAB de CV

- Fosroc, Inc.

- Henkel AG & Co. KGaA

- Kryton International Inc.

- LATICRETE International, Inc.

- MAPEI SpA

- MBCC Group

- MC-Bauchemie

- Normet

- RPM International Inc.

- Saint-Gobain

- Selena Group

- Sika AG

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

- 세계 개요

- 개요

- Porter's Five Forces 분석 프레임워크(산업 매력도 분석)

- 세계 밸류체인 분석

- 시장 역학(DROs)

- 정보원 및 참고문헌

- 도표 일람

- 주요 인사이트

- 데이터 팩

- 용어집

The South America Construction Chemicals Market size is estimated at 4.68 billion USD in 2024, and is expected to reach 6.53 billion USD by 2030, growing at a CAGR of 5.73% during the forecast period (2024-2030).

Procrear 2023 and Minha Casa, Minha Vida housing schemes' influence over South America's construction chemicals demand

- The demand for construction chemicals in South America witnessed a 5.89% increase in 2022, primarily attributed to a surge in construction activities. Notably, Brazil saw a 4.1% rise in new residential floor areas in 2022 compared to the preceding year. With the commercial and infrastructure sectors leading the way, the construction chemicals market in South America was projected to grow by 5.55% in 2023, in terms of value, when compared to 2022.

- Argentina and Brazil dominate the consumption of construction chemicals in South America. Notably, the residential sector in both countries commands the highest demand, accounting for 30% and 43% of the total demand, respectively, across all end-user sectors in 2022.

- Across most South American countries, the Industrial and Institutional sectors are the primary consumers of construction chemicals. However, in Brazil, the residential sector takes the second spot, making it the region's second-largest end-user sector. Excluding Brazil and Argentina, the Industrial and Institutional sector held a 45% share of the overall demand in 2022 across the other countries in the region.

- Projections indicate that Brazil and Argentina will witness the swiftest surge in construction chemical demand, primarily driven by their residential sectors. National housing initiatives, such as Argentina's Procrear 2023 and Brazil's Minha Casa, Minha Vida, are set to spur the construction of new homes and the renovation of existing ones. Consequently, the residential sector is poised to witness the fastest growth in demand, with a projected CAGR of 6.36% during the forecast period (2023-2030).

The growing dominance of Brazil in South American construction chemicals market

- In 2022, the residential sector emerged as the leading consumer of construction chemicals in South America, accounting for approximately 35% of the total demand across all sectors. Brazil, with its sizable residential sector, spearheaded this demand. Looking ahead to 2023, the commercial and infrastructure sectors are poised to witness the most significant surge in demand in the region.

- Brazil, as the region's largest economy and most populous nation, naturally takes the lead in construction output. Consequently, it also boasts the highest consumption of construction chemicals. Notably, Brazil's residential sector commands the lion's share, representing about 43% of the nation's total consumption in 2022.

- Following Brazil, Argentina stands out as the second-largest consumer of construction chemicals. Argentina alone accounted for a massive demand worth USD 378.5 million in 2022. This demand is primarily driven by the country's residential and industrial/institutional sectors, which accounted for over USD 223.3 million in 2022.

- With Brazil's residential and industrial/institutional sectors projected to witness a significant increase in new floor areas by 2030 (37% and 30%, respectively, compared to 2022), the demand for construction chemicals is expected to surge. As a result, Brazil is anticipated to lead the expansion of the construction chemicals market in South America, with a forecasted CAGR of 6.11% from 2023 to 2030.

South America Construction Chemicals Market Trends

Growing foreign direct investments (FDIs) in the region to aid the market demand in the coming years

- In 2022, the commercial sector in South America saw a significant decline of 16.2% in new floor area construction, largely driven by a 9.16% drop in Argentina. However, the sector was poised for a rebound in 2023, with a projected 4.75% increase in volume output. This growth can be attributed to economic growth and a surge in commercial construction, as various industries in the region attracted foreign direct investments (FDI) in 2022. In 2022, the Economic Commission for Latin America and the Caribbean (ECLAC) reported a robust 55.2% rise in FDI in the region.

- The construction volume in the sector witnessed a notable growth of 15.9% in 2020 and a further 3.29% in 2021. This growth was a result of South American governments prioritizing the infrastructure and construction sectors. They eased restrictions, allowing construction, maintenance, and project development activities in private and public ventures. This move aimed to meet crucial milestones, deadlines, and economic recovery goals.

- The commercial sector in South America is projected to witness robust growth in new floor area construction, registering a CAGR of 4% in volume during the forecast period (2023 to 2030). The region is witnessing a notable shift in its commercial construction landscape. Notable projects like the Paulinia Data Center and Porto Alegre Data Center I, initiated in 2023, are among the largest in the region. Additionally, investors are eyeing office buildings, shopping centers, and logistic parks in Brazil, which are expected to fuel market demand in the coming years.

Affordable housing schemes and subsidies in South America to influence higher construction in the residential sector

- In 2022, the residential sector in South America witnessed a 3.35% surge in new floor area construction compared to the previous year. However, Argentina saw a notable decline of 9.16% in this metric. In 2023, the sector was projected to maintain its growth trajectory, with a construction volume expected to be 3.3% higher than in 2022. This growth can be attributed to factors like increasing urbanization, rising per capita income, and overall economic expansion, all of which are fueling the demand for housing.

- Amidst the backdrop of the COVID-19 pandemic in 2020, South America saw a significant uptick of 11.83% in new floor area construction compared to the previous year. This was a deliberate move by the South American government, which prioritized the construction sector to mitigate the economic downturn and support workers, given the sharp decline in household incomes. Consequently, restrictions on construction activities, including quarantines, were eased.

- Several South American nations are rolling out initiatives to make housing more affordable for their growing populations. For example, in February 2023, Brazil relaunched its nationwide federal housing program, targeting low-income individuals. In October 2023, the World Bank approved a USD 100 million financing package for Ecuador, specifically aimed at bolstering affordable and resilient housing. Bolivia's efforts to ramp up the supply of low-cost housing and maintain reasonable prices are poised to further stoke the demand for residential spaces. As a result, the residential sector in South America is projected to witness a CAGR volume of 4.09% during the forecast period (2023-2030).

South America Construction Chemicals Industry Overview

The South America Construction Chemicals Market is fragmented, with the top five companies occupying 26.38%. The major players in this market are Arkema, MBCC Group, RPM International Inc., Saint-Gobain and Sika AG (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End Use Sector Trends

- 4.1.1 Commercial

- 4.1.2 Industrial and Institutional

- 4.1.3 Infrastructure

- 4.1.4 Residential

- 4.2 Major Infrastructure Projects (current And Announced)

- 4.3 Regulatory Framework

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size, forecasts up to 2030 and analysis of growth prospects.)

- 5.1 End Use Sector

- 5.1.1 Commercial

- 5.1.2 Industrial and Institutional

- 5.1.3 Infrastructure

- 5.1.4 Residential

- 5.2 Product

- 5.2.1 Adhesives

- 5.2.1.1 By Sub Product

- 5.2.1.1.1 Hot Melt

- 5.2.1.1.2 Reactive

- 5.2.1.1.3 Solvent-borne

- 5.2.1.1.4 Water-borne

- 5.2.2 Anchors and Grouts

- 5.2.2.1 By Sub Product

- 5.2.2.1.1 Cementitious Fixing

- 5.2.2.1.2 Resin Fixing

- 5.2.2.1.3 Other Types

- 5.2.3 Concrete Admixtures

- 5.2.3.1 By Sub Product

- 5.2.3.1.1 Accelerator

- 5.2.3.1.2 Air Entraining Admixture

- 5.2.3.1.3 High Range Water Reducer (Super Plasticizer)

- 5.2.3.1.4 Retarder

- 5.2.3.1.5 Shrinkage Reducing Admixture

- 5.2.3.1.6 Viscosity Modifier

- 5.2.3.1.7 Water Reducer (Plasticizer)

- 5.2.3.1.8 Other Types

- 5.2.4 Concrete Protective Coatings

- 5.2.4.1 By Sub Product

- 5.2.4.1.1 Acrylic

- 5.2.4.1.2 Alkyd

- 5.2.4.1.3 Epoxy

- 5.2.4.1.4 Polyurethane

- 5.2.4.1.5 Other Resin Types

- 5.2.5 Flooring Resins

- 5.2.5.1 By Sub Product

- 5.2.5.1.1 Acrylic

- 5.2.5.1.2 Epoxy

- 5.2.5.1.3 Polyaspartic

- 5.2.5.1.4 Polyurethane

- 5.2.5.1.5 Other Resin Types

- 5.2.6 Repair and Rehabilitation Chemicals

- 5.2.6.1 By Sub Product

- 5.2.6.1.1 Fiber Wrapping Systems

- 5.2.6.1.2 Injection Grouting Materials

- 5.2.6.1.3 Micro-concrete Mortars

- 5.2.6.1.4 Modified Mortars

- 5.2.6.1.5 Rebar Protectors

- 5.2.7 Sealants

- 5.2.7.1 By Sub Product

- 5.2.7.1.1 Acrylic

- 5.2.7.1.2 Epoxy

- 5.2.7.1.3 Polyurethane

- 5.2.7.1.4 Silicone

- 5.2.7.1.5 Other Resin Types

- 5.2.8 Surface Treatment Chemicals

- 5.2.8.1 By Sub Product

- 5.2.8.1.1 Curing Compounds

- 5.2.8.1.2 Mold Release Agents

- 5.2.8.1.3 Other Product Types

- 5.2.9 Waterproofing Solutions

- 5.2.9.1 By Sub Product

- 5.2.9.1.1 Chemicals

- 5.2.9.1.2 Membranes

- 5.2.1 Adhesives

- 5.3 Country

- 5.3.1 Argentina

- 5.3.2 Brazil

- 5.3.3 Rest of South America

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Ardex Group

- 6.4.2 Arkema

- 6.4.3 CEMEX, S.A.B. de C.V.

- 6.4.4 Fosroc, Inc.

- 6.4.5 Henkel AG & Co. KGaA

- 6.4.6 Kryton International Inc.

- 6.4.7 LATICRETE International, Inc.

- 6.4.8 MAPEI S.p.A.

- 6.4.9 MBCC Group

- 6.4.10 MC-Bauchemie

- 6.4.11 Normet

- 6.4.12 RPM International Inc.

- 6.4.13 Saint-Gobain

- 6.4.14 Selena Group

- 6.4.15 Sika AG

7 KEY STRATEGIC QUESTIONS FOR CONCRETE, MORTARS AND CONSTRUCTION CHEMICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

샘플 요청 목록