|

시장보고서

상품코드

1907244

북미의 건설용 화학제품 시장 : 점유율 분석, 산업 동향 및 통계, 성장 예측(2026-2031년)North America Construction Chemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

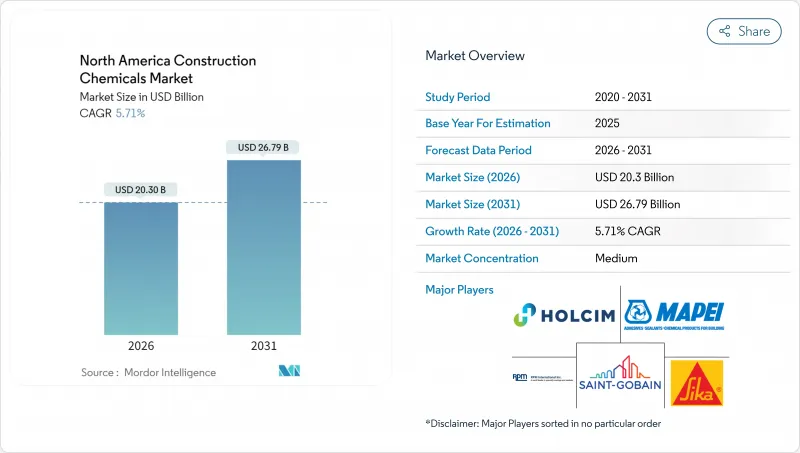

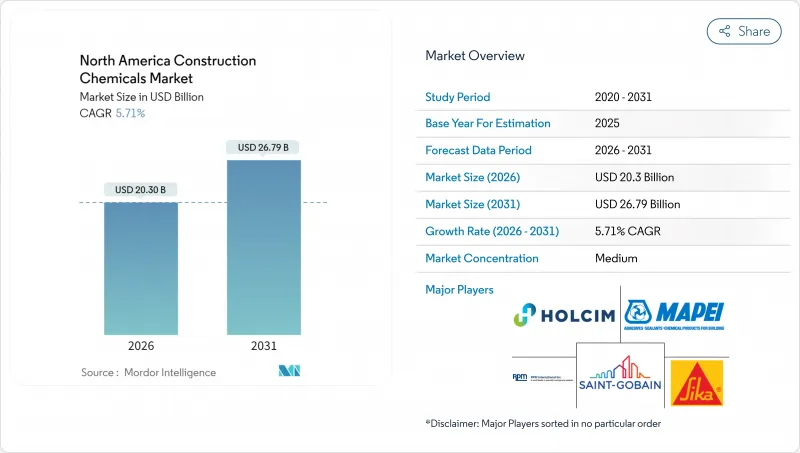

북미의 건설 화학 시장은 2025년 192억 달러로 평가되었고, 2026년 203억 달러에서 2031년까지 267억 9,000만 달러에 이를 것으로 예측됩니다. 예측 기간(2026-2031년) CAGR은 5.71%로 성장이 예상됩니다.

인프라 근대화 프로그램, 클린 조달 규칙, AI 탑재의 배합 설계 플랫폼의 대두가 함께 제품 수요를 확대하는 동시에 사양 책정의 길을 재정의하고 있습니다. 인프라 투자 및 고용법(IIJA)에 의한 자금 제공을 받은 고속도로, 교량, 물 인프라의 개수는 원재료 가격 상승을 상쇄하면서 내용 연수를 연장할 수 있는 고효율 혼화제를 필요로 하는 대량 콘크리트 용도의 안정된 수요 기반을 창출하고 있습니다. 주 수준의 탄소 함량 규제로 구매자는 낮은 GWP 방수막과 시멘트계 보강재 대응 혼화제를 선택하게 되어 인증된 지속가능 화학제품의 고가격대 시장이 형성되고 있습니다. 데이터센터 및 반도체 메가 프로젝트는 내화성 코팅, 정밀 실런트, 속 경화형 경화제의 급속한 보급을 촉진하고 있습니다. 한편 에너지 절약 기준 강화로 첨단 외장 시스템용 고성능 접착제 수요가 증가하고 있습니다. 석유 유래 수지의 가격 변동 및 숙련 노동자 부족은 여전히 비용면에서의 역풍입니다만, 원료 조달을 수직 통합한 공급자나, 시공 기술을 간소화한 기업은 이익률 리스크를 경감하고 있습니다.

북미의 건설용 화학제품 시장 동향 및 인사이트

인프라 프로젝트에 대규모 투자

IIJA(인프라 투자 및 고용법)에 의한 자금 조달을 배경으로 한 다수의 교통 인프라 개량 및 교량 보수 사업이, 보호 도료, 보수용 모르타르, 수처리 화학제품에 대한 지속적이고 대량 수요를 창출하고 있습니다. 2022년 고속도로 건설 지수 상승에 상징되는 비용 인플레이션은 구매력을 저하시키고, 각 기관은 라이프사이클 내구성을 중시한 성능 기준 사양으로의 이행을 촉진하고 있습니다. 캐나다 연방 및 주 프로그램은 특히 동결 융해 사이클을 견딜 수 있도록 설계된 방수 시스템에서 미국의 기세를 반영합니다. 가속 노화 시험 프로토콜 하에서 자산 수명 연장을 입증할 수 있는 공급업체가 여러 해에 걸친 프레임워크 계약을 획득하고 있습니다. 원재료 조달의 수직 통합은 입찰 가격 변동에 대한 헤지 수단으로 부상하고 있으며 원료 가격 변동에도 불구하고 생산자가 고정 가격 약속을 지킬 수 있습니다.

엄격한 에너지 절약 기준이 고성능 혼화제 촉진

타이틀 24, IECC, 주 에너지 기준의 통합은 벽과 지붕에 요구되는 최소한의 단열 성능을 향상시키고, 연속 단열 어셈블리를 지원하는 첨단 실란트 및 접착제 시스템의 채택을 추진하고 있습니다. 이와 동시에 이 프로젝트는 매장 탄소량의 저감도 요구되고 있어 강도를 손상시키지 않고 시멘트 함유량을 삭감하는 혼화제에 대한 이중 압력이 발생하고 있습니다. 콘크리트 생산자는 높은 플라이 애쉬와 슬래그의 대체 비율을 허용하는 고성능 감수제를 지정하는 경향이 강해지고 있으며, 엄격한 탄성 계수 목표를 달성하기 위해 나노 실리카 블렌드를 통합하는 경우도 볼 수 있습니다. 크래들 투 게이트 방식의 환경 제품 선언(EPD)과 기술 모델링 지원을 제공하는 화학제품 공급업체가 공공 부문 입찰에서 범용품 공급업체를 대체하고 있습니다. 상업용 건물에서는 에너지 모델링 툴이 단열 성능과 구조 성능 시뮬레이션을 연동시켜 얇은 슬래브 단면에서 화학 성능의 허용 오차를 더욱 엄격하게 하고 있습니다.

석유 유래 수지 가격의 변동성

미국 국제무역위원회(USITC)의 덤핑 조사 개시 후 에폭시 수지의 스팟 가격이 급등하고 고순도 비스페놀 A 원료에 의존하는 특수 도료의 이익률이 압박되었습니다. 멕시코 걸프에 공장을 세우는 제조업체는 운송 비용면에서 우위를 가지고 있지만 허리케인 관련 가동 중단 위험에 여전히 노출되어 있습니다. 헤지 전략은 아시아의 이중 조달과 현지 탱크 저장 시설의 건설을 통한 공급 충격의 평준화를 포함합니다. 최종 사용자는 석유 유래 성분을 바이오 에폭시로 대체하는 하이브리드 시스템의 시험 도입이 진행되고 있지만, 이러한 블렌드 제품은 여전히 가격 프리미엄이 붙고 규격 승인도 한정적입니다. 다년간 공급 계약에서는 원료 가격 변동을 전가하기 위해 동적 가격 조항이 표준화되어 있습니다.

부문 분석

방수 솔루션은 2025년 시점에서 북미 건설화학제품 시장의 32.62%를 차지하였고, 2031년까지 연평균 복합 성장률(CAGR) 6.09%로 확대될 것으로 전망됩니다. 이것은 엄격한 방습 관리 기준에 따라 건축 외관의 무결성에 대한 관심이 높아지고 있음을 반영합니다. 시트계 시스템 대신에, 시공 공수를 삭감해 복잡한 형상에 대응 가능한 액상 도포형 방수시트가 보급됨으로써, 본 부문은 시장 전체를 웃도는 성장률을 나타내고 있습니다. 제조업체 각사는 에너지 효율이 높은 구조체에 있어서 이중의 성능 목표를 달성하기 위해, 증기 투과성을 유지하면서 신장성을 실현하는 목적으로, 폴리머 개질 아스팔트와 반응성 실란을 배합하고 있습니다. 유체 멤브레인을 지오텍 스타일로 보강하는 하이브리드 시스템은 표준 제품보다 높은 가격대에서 제공됩니다. 표면처리제 및 양생제는 프리캐스트 생산자의 동향과 마찬가지로 이형성의 향상과 수화 제어를 중시하여 공장의 생산 효율 향상을 도모하고 있습니다. 한편, 콘크리트 혼화제 제조업체는 수축 억제제를 통합 방수 패키지에 통합하여 시공업체가 단일 보증 하에서 다기능 솔루션을 조달할 수 있도록 합니다.

콘크리트 혼화제는 여전히 중요한 제품군이며, 포틀랜드 시멘트의 50% 치환 수준에서 25MPa의 강도를 실현하는 고성능 감수제가 견인하고 있습니다. 이것은 저탄소 입찰에서 매우 중요한 성능입니다. 섬유 감기용 에폭시 수지나 초속 경화 모르타르를 포함한 보수 및 재생용 화학제품은 노후화된 교량 스톡 증가에 의해 수요가 확대되고 있으며, 많은 연방 프로젝트에서는 이미 이러한 시스템을 덱 오버레이로 지정하고 있습니다. 접착제, 실란트, 바닥용 수지는 상업용 외관 개수와 고교통량 소매점포의 개조 수요에 힘입어 안정된 수요를 유지하고 있습니다. VOC 규제 및 NFPA 285 규격의 요구가 계속되고 있는 가운데, 배합 제조업체는 저용제형 또는 수성 화학제품으로의 이행을 강요받고 있어 원재료 포트폴리오와 이익률 구조의 재구축이 진행되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트 서포트(3개월간)

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 인프라 프로젝트에 대한 대규모 투자

- 엄격한 에너지 절약 기준이 고성능 혼화제 수요 촉진

- 레디믹스트 콘크리트 및 프리캐스트 공법의 급속한 보급

- 순환형 경제의 의무화가 저탄소 건설자재 촉진

- 화학약품 투여 정밀도를 높이는 AI 탑재 혼합 설계 플랫폼

- 시장 성장 억제요인

- 석유 유래 수지 가격의 변동성

- 노동력 부족에 의한 신규 프로젝트 개시 지연

- 방화 규제의 변경에 의한 용제계 화학제품 억제

- 밸류체인 분석

- 규제 상황

- Porter's Five Forces

- 신규 참가업체의 위협

- 공급기업의 협상력

- 구매자의 협상력

- 대체품의 위협

- 산업 간 경쟁

제5장 시장 규모 및 성장 예측

- 제품별

- 접착제

- 핫멜트

- 반응성

- 용제계

- 수성

- 앵커 및 그라우트

- 시멘트계 고정재

- 수지 고정

- 콘크리트 혼화제

- 가속제

- 공기혼입제

- 고성능 감수제

- 지연제

- 수축 억제제

- 점도 조정제

- 가소제

- 기타

- 콘크리트 보호 코팅

- 아크릴

- 알키드 수지

- 에폭시 수지

- 폴리우레탄

- 기타 수지

- 바닥용 수지

- 아크릴

- 에폭시 수지

- 폴리아스파르트산 수지

- 폴리우레탄

- 기타 수지

- 보수 및 개수용 화학제품

- 섬유 포장 시스템

- 주입 그라우팅

- 마이크로 콘크리트 모르타르

- 개질 모르타르

- 철근보호재

- 실란트

- 아크릴

- 에폭시 수지

- 폴리우레탄

- 실리콘

- 기타 수지

- 표면 처리용 화학약품

- 양생제

- 이형제

- 기타

- 방수 솔루션

- 화학제품

- 방수 시트

- 접착제

- 최종 사용자 분야별

- 상업용

- 산업 및 공공시설용

- 인프라

- 주택용

- 지역별

- 미국

- 캐나다

- 멕시코

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율(%) 및 랭킹 분석

- 기업 프로파일

- 3M

- ARDEX Americas

- Arkema(Bostik)

- Ashland

- Dow

- Henkel AG & Co. KGaA

- Holcim Group

- Kingspan Group

- LATICRETE International, Inc

- MAPEI SpA

- RPM International Inc.

- Saint-Gobain

- Sika AG

- Xypex USA

제7장 시장 기회 및 장래 전망

제8장 CEO를 위한 주요 전략적 과제

AJY 26.01.26The North America Construction Chemicals Market was valued at USD 19.20 billion in 2025 and estimated to grow from USD 20.3 billion in 2026 to reach USD 26.79 billion by 2031, at a CAGR of 5.71% during the forecast period (2026-2031).

Infrastructure modernization programs, buy-clean procurement rules, and the rise of AI-enabled mix-design platforms are simultaneously expanding product demand and redefining specification pathways. Highway, bridge, and water-infrastructure upgrades funded by the Infrastructure Investment and Jobs Act (IIJA) fuel a steady pipeline of large-volume concrete applications that require high-efficiency admixtures capable of extending service life while offsetting raw material inflation. State-level embodied-carbon mandates are steering buyers toward low-GWP waterproofing membranes and supplementary-cementitious-material-compatible admixtures, creating premium pricing niches for verified sustainable chemistries. Data-center and semiconductor megaprojects drive the rapid adoption of fire-resistant coatings, precision sealants, and quick-turn curing compounds, while energy-efficiency codes increase demand for high-performance adhesives within advanced envelope systems. Petro-derived resin price swings and skilled-labor shortages remain cost headwinds; however, suppliers with vertically integrated feedstock positions and simplified application technologies are mitigating margin risk.

North America Construction Chemicals Market Trends and Insights

Substantial investments in infrastructure projects

Many transportation improvements and bridge repairs, financed by the IIJA, are translating into consistent, high-volume demand for protective coatings, repair mortars, and water treatment chemicals. Cost inflation-characterized by growth in highway-construction indices during 2022-has eroded purchasing power, prompting agencies to shift toward performance-based specifications that emphasize lifecycle durability. Canadian federal and provincial programs mirror the U.S. momentum, particularly for waterproofing systems engineered to withstand freeze-thaw cycles. Suppliers that can document extended asset life under accelerated-aging protocols are winning multi-year framework contracts. Vertical integration in raw material sourcing is emerging as a hedge against bid volatility, allowing producers to honor fixed-price commitments despite fluctuations in feedstock prices.

Stringent energy-efficiency codes spurring high-performance admixtures

Convergence of Title 24, IECC, and provincial energy codes has elevated the minimum thermal performance required of walls and roofs, driving adoption of advanced sealants and adhesive systems that support continuous-insulation assemblies. The same projects must now also demonstrate lower embodied carbon, creating dual pressure for admixtures that reduce cement content without compromising strength. Concrete producers increasingly specify superplasticizers that allow higher fly-ash or slag substitution ratios, and some are integrating nano-silica blends to meet stringent modulus targets. Chemical suppliers offering cradle-to-gate EPDs and technical modeling support are displacing commodity providers in public-sector bids. In commercial buildings, energy modeling tools are linking thermal and structural simulations, further tightening tolerances on chemical performance at thinner slab profiles.

Volatility in petro-derived resin prices

Epoxy resin spot prices spiked after USITC launched an antidumping inquiry, squeezing margins in specialty coatings that rely on high-purity bisphenol-A feedstock. Manufacturers with Gulf-Coast plants enjoy freight advantages but remain vulnerable to hurricane-related outages. Hedging strategies include dual-sourcing from Asia and building on-site tank storage to smooth supply shocks. End-users are trialing hybrid systems that replace petro content with bio-based epoxies, but these blends still command price premiums and face limited code approvals. Dynamic pricing clauses have become standard in multi-year supply contracts to pass through feedstock price fluctuations.

Other drivers and restraints analyzed in the detailed report include:

- Rapid adoption of ready-mix and precast methods

- Circular economy mandates favoring low-carbon construction materials

- Labor shortages slowing new project starts

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Waterproofing Solutions accounted for 32.62% of the North America construction chemicals market in 2025 and is projected to grow at a 6.09% CAGR through 2031, reflecting heightened focus on building-envelope integrity under stricter moisture-management codes. The segment outpaces overall market expansion as liquid-applied membranes replace sheet systems to cut labor hours and accommodate complex geometries. Manufacturers are blending polymer-modified asphalt with reactive silanes to achieve elongation while maintaining vapor permeability, meeting dual performance targets in energy-efficient assemblies. Hybrid systems that reinforce fluid membranes with geo-textile fabrics command premiums over standard products. Surface-treatment chemicals and curing compounds follow the same trend as precast producers, who emphasize release cleanliness and hydration control to accelerate plant throughput. Meanwhile, concrete-admixture suppliers are incorporating shrinkage-reducing additives into integrated waterproofing packages, enabling contractors to source multi-functional solutions under a single warranty.

Concrete Admixtures remain a significant product group, driven by superplasticizers that deliver 25 MPa strength at 50% replacement levels of portland cement-a critical capability for low-carbon bids. Repair and rehabilitation chemicals, including fiber-wrapping epoxies and ultra-rapid-setting mortars, benefit from the aging bridge stock, with many federal projects already specifying these systems for deck overlays. Adhesives, sealants, and flooring resins maintain steady demand tied to commercial facade upgrades and high-traffic retail refurbishments. VOC restrictions and NFPA 285 compliance continue to push formulators toward low-solvent or water-borne chemistries, reshaping raw-material portfolios and margin profiles.

The North America Construction Chemicals Market Report is Segmented by Product (Adhesives, Anchors and Grouts, Concrete Admixtures, Concrete Protective Coatings, Flooring Resins, Repair and Rehabilitation Chemicals, and More), End-User Sector (Commercial, Industrial and Institutional, Infrastructure, and Residential), and Geography (United States, Canada, and Mexico). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- 3M

- ARDEX Americas

- Arkema (Bostik)

- Ashland

- Dow

- Henkel AG & Co. KGaA

- Holcim Group

- Kingspan Group

- LATICRETE International, Inc

- MAPEI S.p.A.

- RPM International Inc.

- Saint-Gobain

- Sika AG

- Xypex USA

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Substantial investments in infrastructure projects

- 4.2.2 Stringent energy-efficiency codes spurring high-performance admixtures

- 4.2.3 Rapid adoption of ready-mix and precast methods

- 4.2.4 Circular economy mandates favouring low-carbon construction materials

- 4.2.5 AI-enabled mix-design platforms boosting chemical dosage accuracy

- 4.3 Market Restraints

- 4.3.1 Volatility in petro-derived resin prices

- 4.3.2 Labor shortages slowing new project starts

- 4.3.3 Fire-safety rule changes curbing solvent-borne chemistries

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Industry Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product

- 5.1.1 Adhesives

- 5.1.1.1 Hot-Melt

- 5.1.1.2 Reactive

- 5.1.1.3 Solvent-borne

- 5.1.1.4 Water-borne

- 5.1.2 Anchors and Grouts

- 5.1.2.1 Cementitious Fixing

- 5.1.2.2 Resin Fixing

- 5.1.3 Concrete Admixtures

- 5.1.3.1 Accelerator

- 5.1.3.2 Air-Entraining

- 5.1.3.3 Super-plasticizer

- 5.1.3.4 Retarder

- 5.1.3.5 Shrinkage-Reducer

- 5.1.3.6 Viscosity-Modifier

- 5.1.3.7 Plasticizer

- 5.1.3.8 Other Types

- 5.1.4 Concrete Protective Coatings

- 5.1.4.1 Acrylic

- 5.1.4.2 Alkyd

- 5.1.4.3 Epoxy

- 5.1.4.4 Polyurethane

- 5.1.4.5 Other Resins

- 5.1.5 Flooring Resins

- 5.1.5.1 Acrylic

- 5.1.5.2 Epoxy

- 5.1.5.3 Polyaspartic

- 5.1.5.4 Polyurethane

- 5.1.5.5 Other Resins

- 5.1.6 Repair and Rehabilitation Chemicals

- 5.1.6.1 Fiber-Wrapping Systems

- 5.1.6.2 Injection Grouting

- 5.1.6.3 Micro-concrete Mortars

- 5.1.6.4 Modified Mortars

- 5.1.6.5 Rebar Protectors

- 5.1.7 Sealants

- 5.1.7.1 Acrylic

- 5.1.7.2 Epoxy

- 5.1.7.3 Polyurethane

- 5.1.7.4 Silicone

- 5.1.7.5 Other Resins

- 5.1.8 Surface-Treatment Chemicals

- 5.1.8.1 Curing Compounds

- 5.1.8.2 Mold-Release Agents

- 5.1.8.3 Other Types

- 5.1.9 Waterproofing Solutions

- 5.1.9.1 Chemicals

- 5.1.9.2 Membranes

- 5.1.1 Adhesives

- 5.2 By End-User Sector

- 5.2.1 Commercial

- 5.2.2 Industrial and Institutional

- 5.2.3 Infrastructure

- 5.2.4 Residential

- 5.3 By Geography

- 5.3.1 United States

- 5.3.2 Canada

- 5.3.3 Mexico

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 3M

- 6.4.2 ARDEX Americas

- 6.4.3 Arkema (Bostik)

- 6.4.4 Ashland

- 6.4.5 Dow

- 6.4.6 Henkel AG & Co. KGaA

- 6.4.7 Holcim Group

- 6.4.8 Kingspan Group

- 6.4.9 LATICRETE International, Inc

- 6.4.10 MAPEI S.p.A.

- 6.4.11 RPM International Inc.

- 6.4.12 Saint-Gobain

- 6.4.13 Sika AG

- 6.4.14 Xypex USA

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment